Over the past decade or so of Bitcoin's development, while prices have generally moved upward, the process has been tortuous, with many early participants being purged from the market as bulls and bears alternate. For example, between April 14 and May 19 of this year, the price of BTC fell from nearly $65,000 to $30,000, shrinking investor assets by more than 50% in a short period of time. Knowing how to get higher yields from the BTC in hand, reducing the losses in a bear market, and gaining more in a bull market has become a significant issue for the current BTC holders.

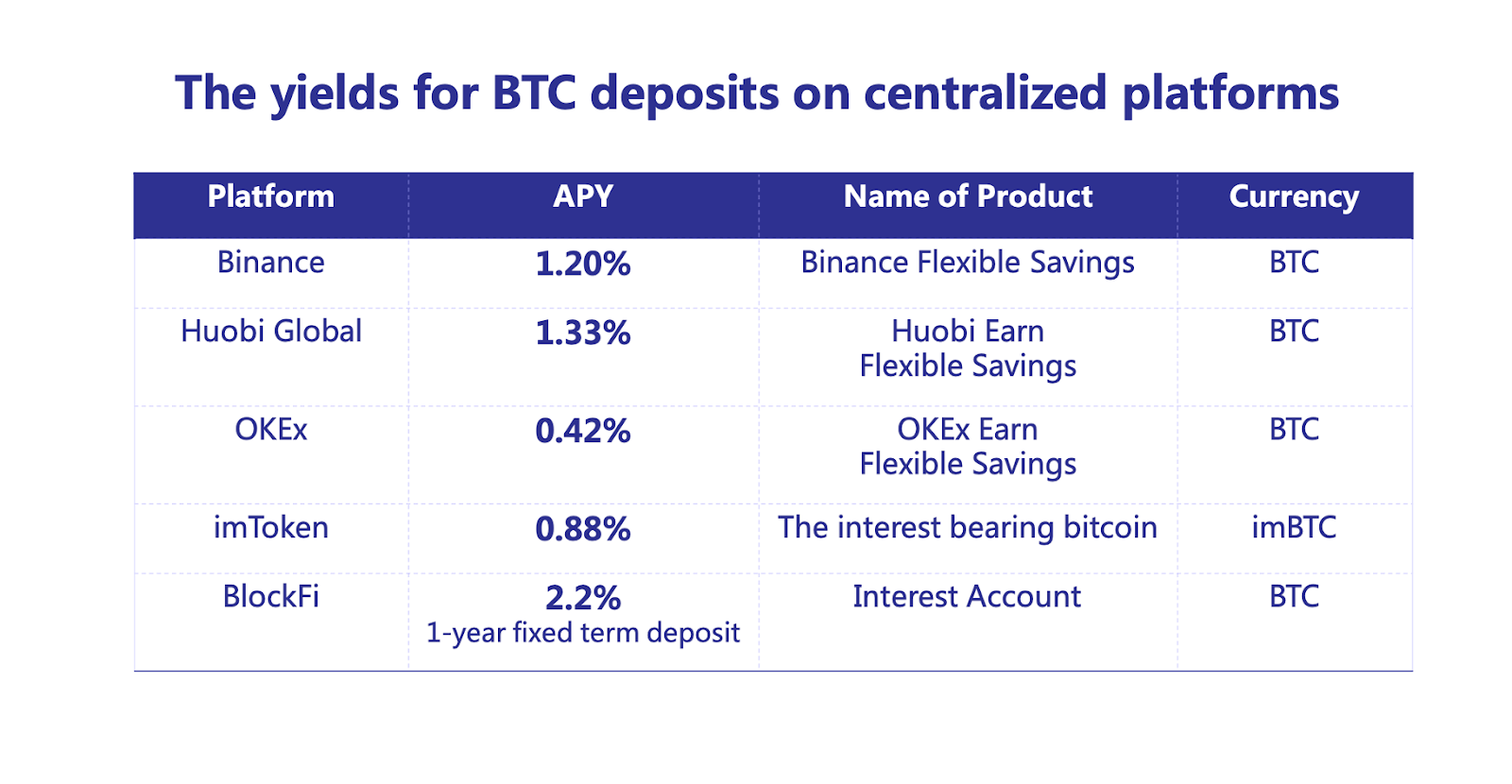

The current situation for BTC returns: The yield from centralized platforms is only 1%

Centralized exchanges, wallets, and lending platforms usually provide financial services. They borrow tokens from users with lower interest rates and then lend them out at higher rates. Cryptocurrency holders can deposit their holdings of Bitcoin and other assets to the platforms to earn a small return. Traders also need to borrow tokens from exchanges in leveraged trading.

Taking Binance as an example, the annualized interest rate of a USDT demand deposit in Binance Wealth Management is 2%, but in leveraged trading, the hourly interest rate for traders to borrow USDT from Binance is 0.00375%, which is equivalent to 32.85% per annum. In a bull market, because there is a large demand for borrowing USDT for leverage, the interest rate at which users borrow USDT will increase accordingly.

Because BTC has a larger market capitalization, users who have more inventory tend to believe that BTC will continue to rise, so for the BTC assets that they don't need to use in the short term, they are optimistic about the price in the long run, and are more willing to keep their bitcoins for interest generation. On the other hand, the demand for borrowing BTC is relatively low, and as the ratio of other coins to the Bitcoin price is more likely to decrease, the main reason for users to borrow BTC is for short positions. As a result, the interest rates on deposits and borrowing are lower for BTC compared to other tokens. According to data shown on the official websites of Binance, Huobi, and OKEx, the annual percentage yield (APY) for BTC deposits is only about 1% (the data in this article was collected on June 11).

Sorting out the financial management of BTC in the gradually emerging decentralized protocols

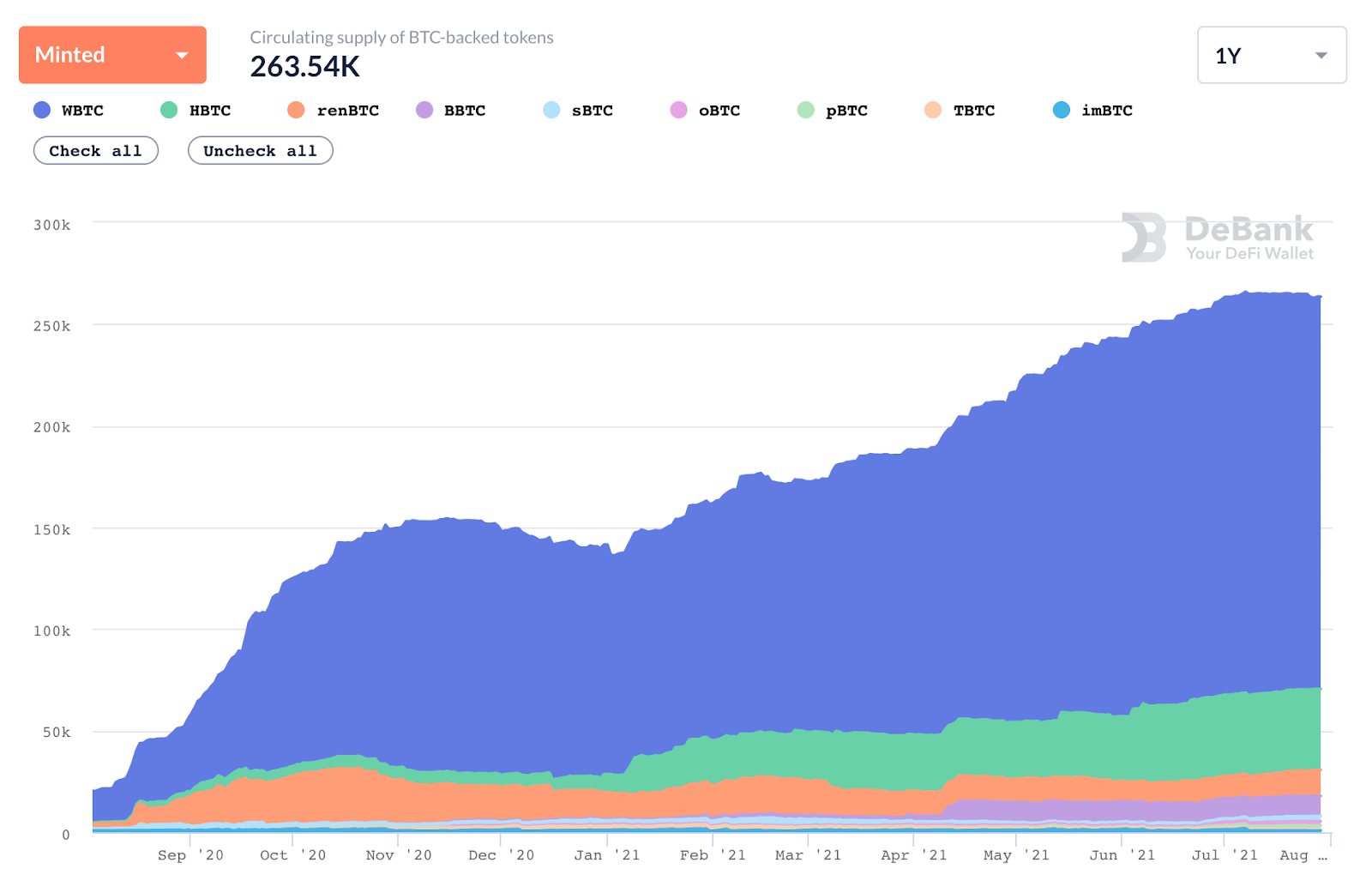

The BTC in decentralized protocols are all in the form of BTC-pegged tokens and are mainly on Ethereum. Since the “DeFi Summer” last year, there have been many more platforms for Bitcoin assets to gain revenue because of liquidity mining, and although the yield is getting lower, the booming of DeFi is attracting more and more funds. The number of BTCpegged tokens on Ethereum continues to grow, from 5,300 to 263,539 over the past year. The market is still dominated by centralized tokens like WBTC and HBTC.

We believe that the BTC-pegged tokens issued in a decentralized manner will become mainstream as these decentralized solutions become well established.

The token rewards for liquidity mining come from the cost of capital paid by the protocol to gain liquidity. The annualized return on liquidity mining in mainstream DeFi protocols has also dropped from several hundred percent when it first emerged a year ago to a few percent currently. On one hand, the price of governance tokens is typically higher when projects first go live due to limited liquidity. On the other hand, with the growing amount of funds entering this market, the tokens that can be distributed for the same scale of money will decrease. For example, the price of CRV, the governance token of Curve, a stablecoin exchange platform, has dropped from tens of dollars at launch to $2.40 now, but at the same time, more and more money is being deposited in Curve, and is now close to $10 billion including Factory Pools. For the Y pool, the comprehensive APY is now only about 2%, but over the last year, the APY was much higher, and the LP tokens of Y pool can also be used to obtain head DeFi tokens such as YFI.

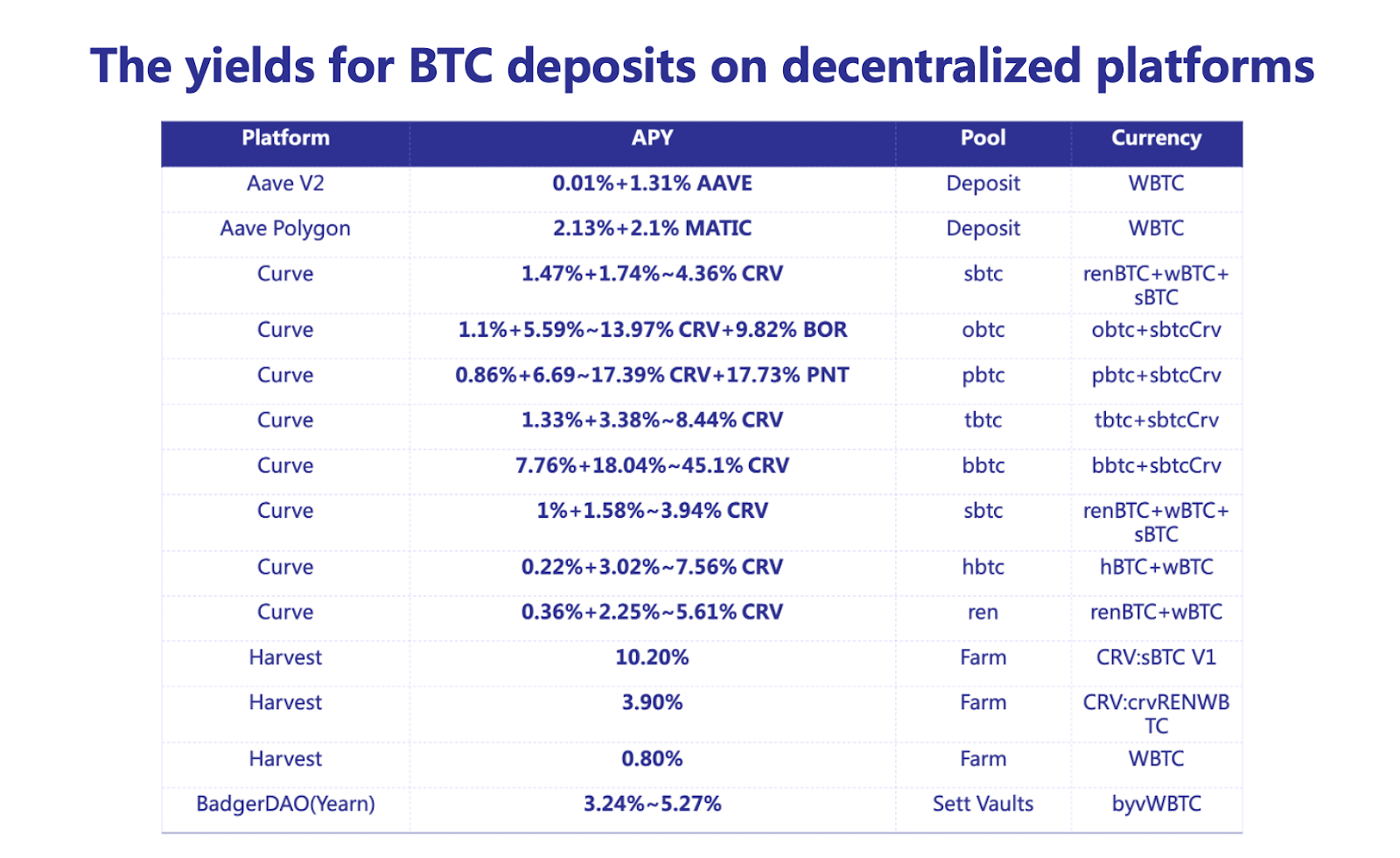

BTC-pegged tokens are widely used in various DeFi protocols. Taking WBTC, the largest issuance among all BTC-pegged tokens as an example, the current issuance is a total of 188,960 pieces, of which 20.98% are being deposited as collaterals in the lending protocol Aave V2, 14.26% in Compound. The Polygon Bridge, Maker, and SushiSwap respectively have 13.57%, 8.85%, and 3.9%.

In all these leading DeFi protocols which have high TVL (total value locked), the yield of WBTC is relatively low. Although adding the platform governance token bonus, the yields of Aave V2 and Aave Polygon are only 1.32% and 4.23% respectively, and the deposit yield of WBTC in Compound is only 1.02%.

In Curve, on the other hand, in addition to the fees rewards and CRV rewards, the APY of the oBTC and pBTC pools are 9.82% (BOR) and 17.73% (PNT) respectively based on their own governance tokens. For these “newcomers” in the BTC-pegged token market, higher returns are designed to incentivize users to use them.

Earnings Calculation of eBTC: Expected to reach an upfront yield of 30%

DeCus is a decentralized bridge that can build cross-chain assets in a secure and highly efficient way. Compared to other solutions for BTC-pegged tokens, DeCus will be launched with features such as complete decentralization, high capital utilization, no liquidation, and decoupling risks. The project has been back-tested by the project's economic model and is predicted to generate high returns for users initially.

To convert BTC into eBTC in DeCus, users will still need to deposit their native BTC 1:1 to the system, but the custodian character of DeCus, the Keeper, can carry out secure custody of the users’ native BTC without the need for an over-collateralization because of an ingenious overlapping grouping.

The total supply of DCS, DeCus governance tokens, is 1 billion. The protocol sets aside a large percentage of tokens, namely 45%, to incentivize the participants, 20% of which will be allocated to eBTC holders who join in the liquidity mining, 15% to the Keepers, 9% to DCS staking participants, and 1% to compensate for minting fees. In addition, the protocol also sets aside 15% of the tokens for the DAO community to use at the DAO's discretion.

In the minting process of eBTC, the users deposit their native BTC to the designated multi-sig address managed by a group of Keepers, and then sends the proof of deposit to the smart contract, which is responsible for mint the corresponding amount of eBTC and sends them back to the user. The Keeper uses WBTC as collateral in the early stage and then changes to eBTC when the bootstrap of the project is successfully completed. Both types of major participants in the protocol, Keeper and User, participate with BTC assets and receive DCS tokens as rewards, so the participation of both characters can be regarded as BTC finance management.

The rates of return for Keepers and Users in DeCus can be roughly calculated by extrapolation as follows:

The liquidity mining of eBTC will allocate 20% of the total 1 billion DCS over 5 years, with 7.5% of the total allocated in the first year and 2/3 of the previous year's amount allocated each year thereafter.

With a DCS institutional round valuation price of $0.03, early investors' tokens will be released over 2 years linearly by block height. The original price for IDO on New Venture was $0.06, therefore the average price of DCS is predicted to be more reasonable at $0.05 in the first year.

Then the liquidity mining reward issued to eBTC in the first year will be: 1 billion * $0.05 * 7.5% = $3.75 million.

Assuming the minting volume of eBTC in the first year is 1000 with the BTC price being calculated at $40,000, and all of minted eBTC will be used for liquidity mining, then the liquidity mining yield of eBTC in the first year is: $3.75 million/1000/$40,000 = 9.38%.

The Keepers’ collateral rate will decrease as the number of Keepers increases. Assuming the Keepers’ collateral rate is 50%, the annualized return of a Keeper can be calculated as: $1 billion * $0.05 * 5.63%/$500/$40,000 = 14.1%.

The mintages of eBTC may be lower than the predicted 1,000 in the early stage after the system is launched. With only 600 eBTC minted, the annualized return of eBTC liquidity mining is: 1 billion * $0.05 * 7.5%/600/$40,000 = 15.6%.

And the Keepers’ annualized return will rise to: 1 billion * $0.05 * 5.63%/300/$40,000 = 23.5%

In addition to the predicted base return, there are many measures in DeCus' economic system designed to increase the return for Keepers and eBTC users.

Keepers’ use of eBTC as collateral will increase the weight of the DCS tokens allocation. Although WBTC can also be used as Keepers’ collateral, using eBTC within the DeCus ecosystem can provide the Keepers a higher weighting, i.e., a higher return than WBTC.

The calculation assumes that all of the minted eBTC will be used for liquidity mining, but in reality, some eBTC is used as Keepers’ collateral and cannot participate in the liquidity mining. Among the remaining eBTC in circulation, there may be some users who are not willing to stake their eBTC for mining. If the staking rate is 50%, then the yield of eBTC liquidity mining will be twice the calculated value.

The BTC price was $37,000 at the time of writing on June 11, while the forecast was uniformly calculated at $40,000. The DCS price was also uniformly calculated at $0.05, and the DCS price in the early stage after launch is likely to be higher than this value.

eBTC can be easily integrated with other protocols to receive governance tokens of other protocols as rewards. Protocols such as Curve are open to Stablecoin, ETH, and BTC assets, so they are likely to integrate eBTC to give CRV token rewards to eBTC holders, along with a share of transaction fees. 38 reward pools are already open in Curve.fi, and dozens of other liquid pools are also available in Curve Swaps integrated with Curve.fi Factory. Up to now, pBTC, BBTC, TBTC, oBTC, sBTC, renBTC, WBTC, HBTC can all receive CRV tokens as mining rewards.

According to the calculation before, with 600 eBTC minted and all of them used for liquidity mining, the annualized return is still 15.63%. However, in reality, some eBTC must be used as Keepers’ collateral, or the holders don’t want to use it for mining, so the actual rate of return may be higher, and the combined annualized return of early eBTC liquidity mining is likely to reach more than 30%.

Conclusion

There are multiple ways to earn with BTC assets in both centralized and decentralized platforms, but the deposit return of BTC is only about 1% in centralized platforms or established decentralized platforms.

Some brand new BTC-pegged tokens often encourage users to use them through higher yields. DeCus offers a highly capital-efficient, cross-chain custodian solution that allows the custodian to carry out secure custody of the underlying assets, i.e the native BTC and more to be supported in the future without the need for over-collateralization because of an ingenious overlapping grouping system. According to the calculations, the annualized return on liquidity mining of eBTC could reach 30% in the early phase of the project.

APP

APP