The blockchain industry in 2021 was thriving. According to the records of CoinMarketCap, the total market value of the digital currency expanded from $755.740 billion on January 1, 2021, to $2,248.668 billion on December 31, 2021, marking an annual increase of 196.27%. In such a booming market, most digital currencies registered considerable incomes.

While the overall secondary market has been flourishing, the primary market has also been successful. According to PAData, a data news column under PANews, investmentand financing in the blockchain field maintained rapid growth in 2021 globally, attracting more than $30 billion in funds to crypto start-ups.This article reviewed investment and financing events disclosed throughout 2021. The core findings are as follows:

1) A total of 1,205 independent projects disclosed 1,351 investment and financing events throughout 2021. Overall, a 'V'-shaped trend of 'explosion-recession-explosion again' is shown. The number of investment and financing events disclosed reached 153 in December, the highest in the whole year.

2) The total amount of investment and financing disclosed throughout 2021 was $30.51 billion. In general, the amount increased over time, reaching a peak of about $5.098 billion in November.

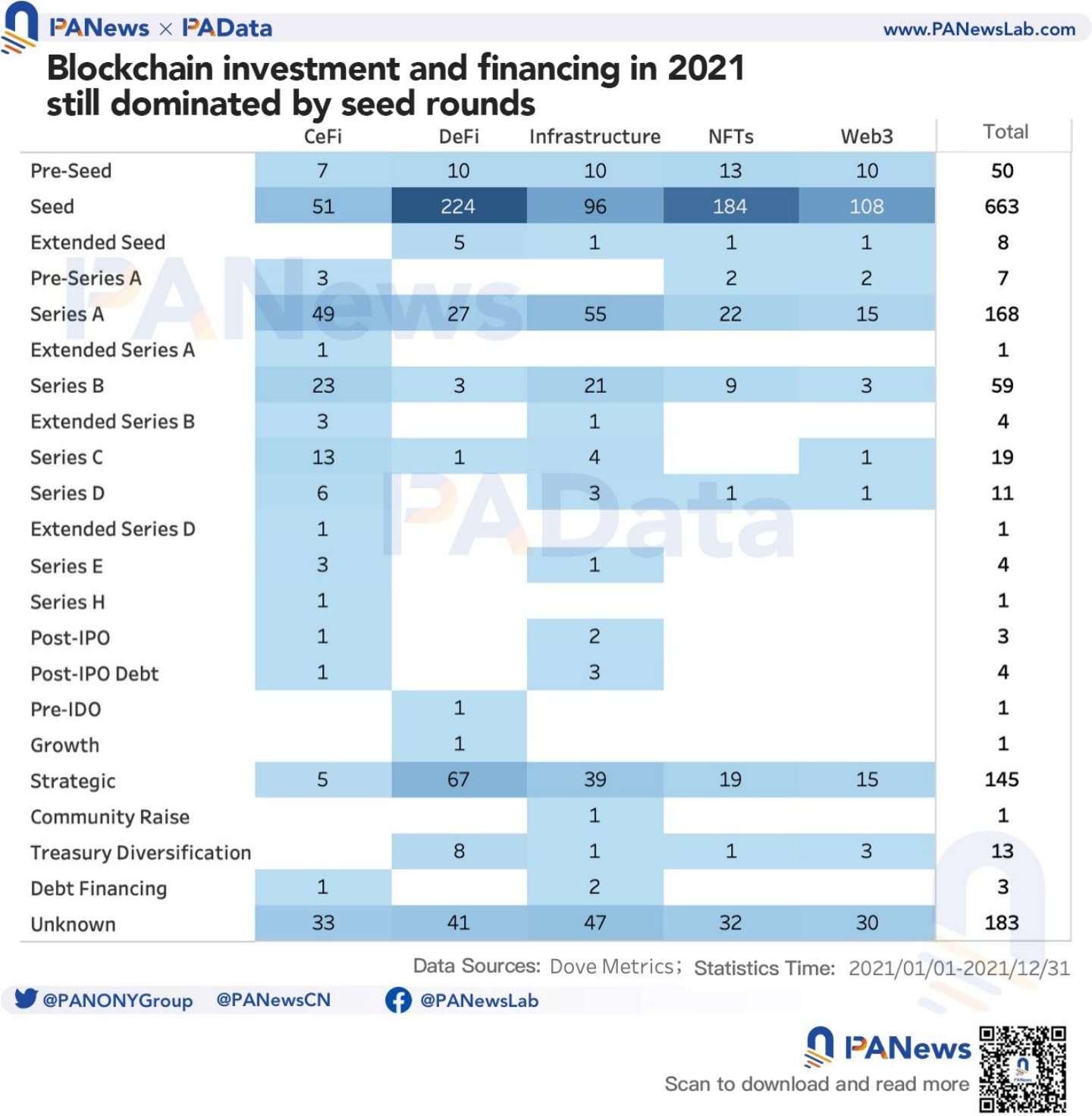

3) Among the financing events, 663 were seeds, 168 were Series A, and 145 were strategic investments. These three types accounted for about 83.56% of the total, while other series of investment and financing events accounted for much less. It is worth noting that there have been many financings after Series C in the fields of CeFi and infrastructure.

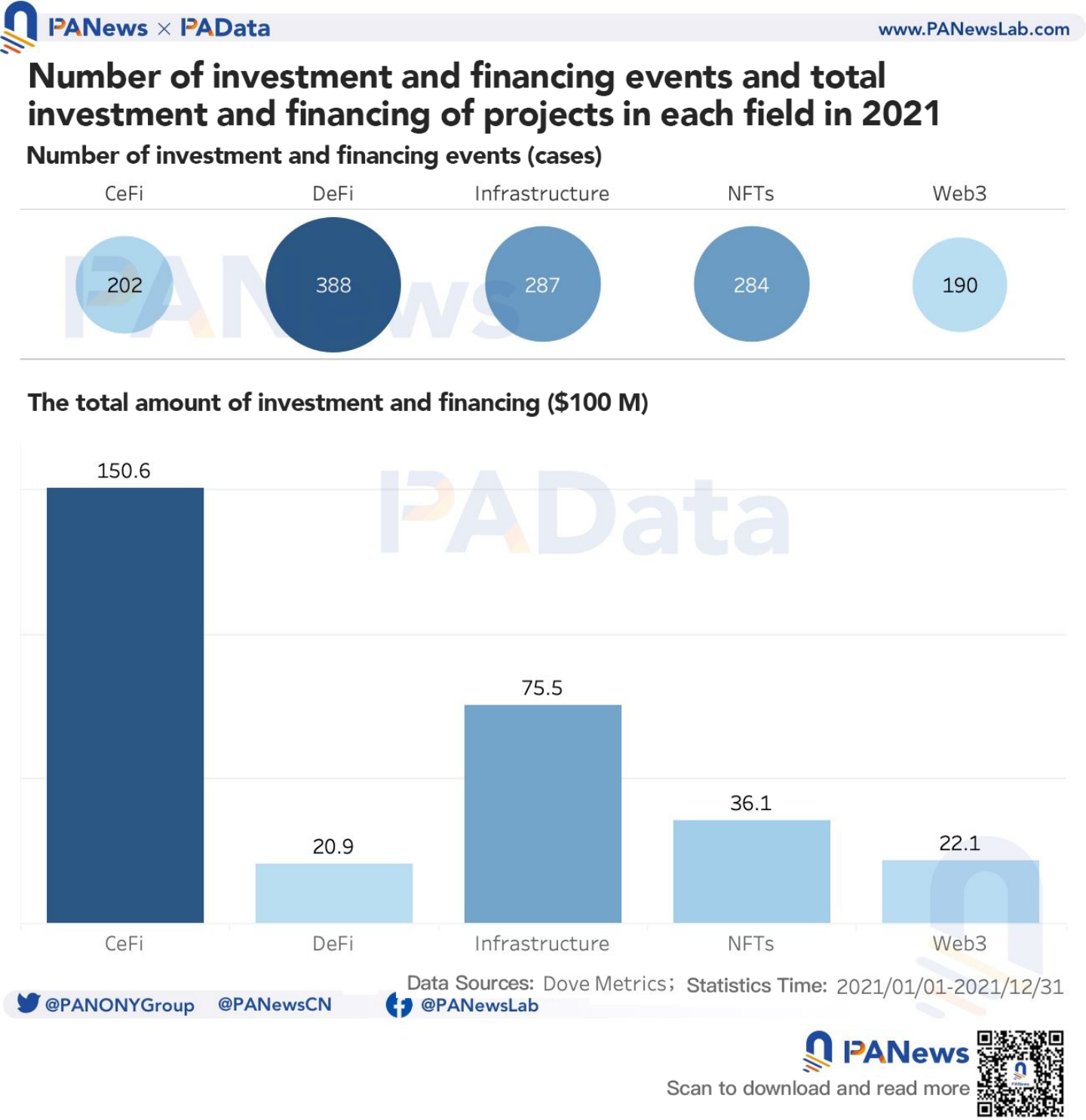

4) The number of investment and financing events in DeFi was the largest, but the total amount was the lowest. The number of investment and financing events in CeFi was smaller, but the total amount was the highest. As relatively new fields, NFTs and Web3 have disclosed total investment and financing of $3.61 billion and $2.21 billion, respectively, higher than those of DeFi.

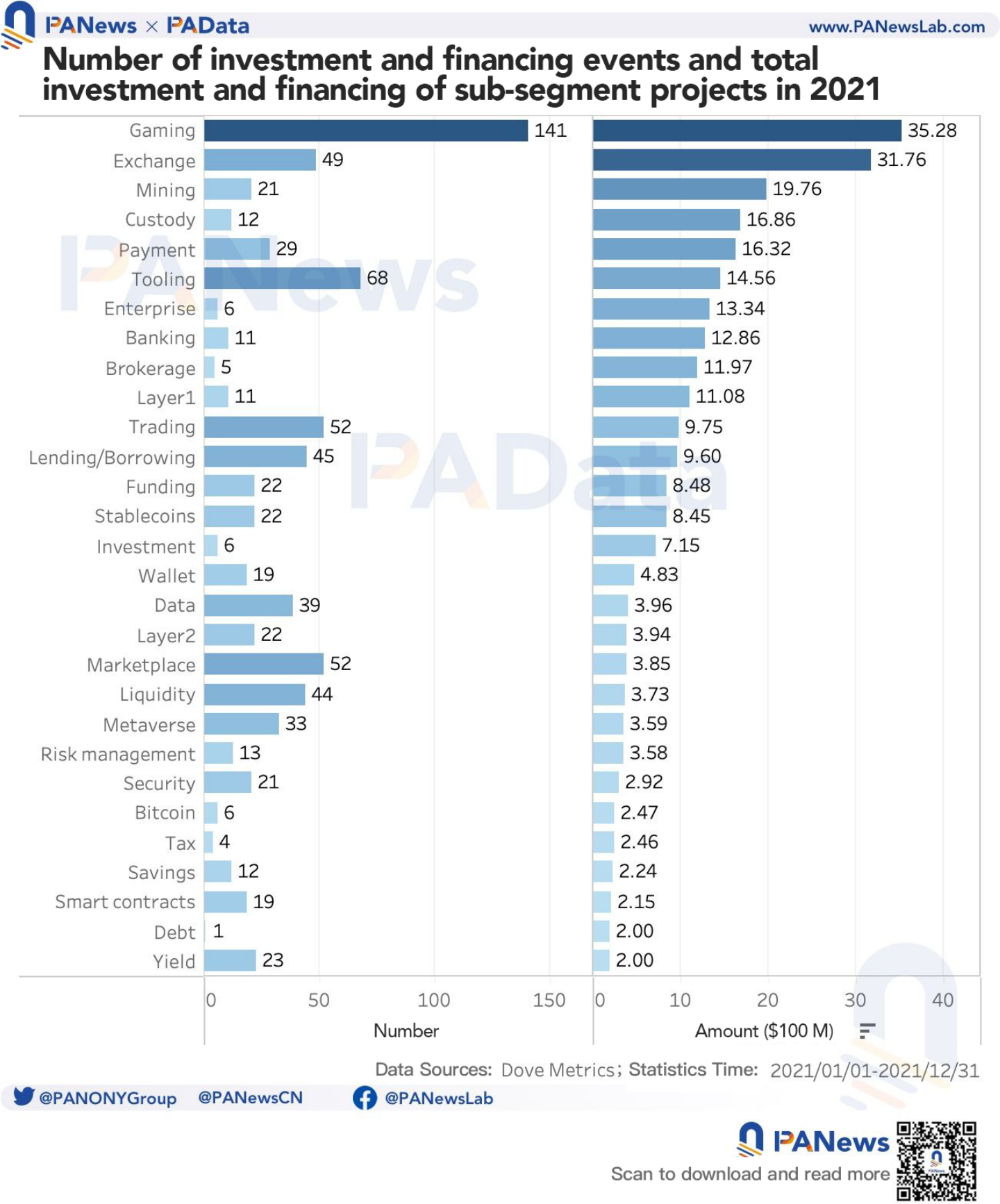

5) Looking at the main sub-segments, gaming disclosed a total of 141 investment and financing events, with a cumulative total of$3.528 billion, both of which ranked first among all sub-segments, making gaming the most favored sub-segment by capital in 2021 with no doubt. Most of the gaming projects were associated with NFTs while some were associated with Web3.

6) Among the 27 major investment institutions, Coinbase Ventures made the most investment moves throughout 2021, According to statistics, a total of 1,205 independent projects disclosed their financing in 2021. If counting the different rounds of investment and financing events disclosed by the same project during the year as separate events, then a total of 1,351 such events occurred in 2021 for these projects. Among them, fewer were disclosed in January and February - only 39 and 58 cases, respectively. Since then, the global blockchain investment and financing have experienced a 'V'-shaped trend of 'explosion-recession-explosion again'.Alameda Research, NGC Ventures, and Animoca Brands all made more than 78 investments throughout the year, involving more than 75 independent projects.

7) Different institutions have shown certain differences in their investment fields. For example, Coinbase Ventures mostly invested in infrastructure, and Digital Currency Group, Dragonfly Capital, Kenetic, and Binance Labs also showed more emphasis on investing in this area. NGC Ventures, Alameda Research, Polychain Capital, Defiance, and Mechanism focused on DeFi. Meanwhile, Animoca Brands focused mostly on NFTs and Web3.

1,205 projects disclosed 1,351 investment and financing events, with a total amount exceeding $30.5 billion

According to statistics, a total of 1,205 independent projects disclosed their financing in 2021. If counting the different rounds of investment and financing events disclosed by the same project during the year as separate events, then a total of 1,351 such events occurred in 2021 for these projects. Among them, fewer were disclosed in January and February - only 39 and 58 cases, respectively. Since then, the global blockchain investment and financing have experienced a 'V'-shaped trend of 'explosion-recession-explosion again'.

In March, there were 148 investment and financing events in the global blockchain field, an increase of 155.17% from the previous month. From April to July, although the number of investment and financing events declined, it remained at over 100 per month. In August, the number of investment and financing events dropped to 85, reaching a short-term low, but then began to recover month by month. By December, the number of investment and financing events reached 153, the highest in the whole year.

1,206 of the 1,351 events disclosed the amount of investment and financing, totaling approximately$30.51 billion. In terms of time, the total amount disclosed has grown over time throughout 2021, reaching a peak of about$5.098 billion in November. In addition, the total monthly investment and financing disclosed in March, July, October, and December were all over$3 billion. On the contrary, the monthly total was lower in January, February, April, and August, all under$2 billion, especially in February when it was only$508 million.

In terms of specific projects, projects with total financing of more than$1 billion in 2021 were FTX, NYDIG, and Robinhood, with a total of about$1.321 billion,$1.3 billion, and$1 billion, respectively. Second, 10 more projects have raised more than $500 million in total, including MoonPay, Forte, Fireblocks, Revolut, Celsius Network, Sorare, Digital Currency Group, Genesis Digital Assets, Dapper Labs, and GRIID. In addition, 49 more projects have raised more than $100 million in total, including popular projects such as Circle, Solana, BitDAO, Avalanche Foundation, and Animoca Brands.

183 of the 1,351 investment and financing events did not disclose the round of investment and financing. Other than those, 663 of the remaining 1,168 events were seeds, accounting for 56.76%; 168 were Series Aand 145 were strategic investments, together accounting for 26.80%. There were several other rounds, such as 63 Series B(including extended Series B), 19 Series C, 12 Series D (including extended Series D), 4 Series E, and only 1 Series H. Overall, the investment and financing in the blockchain field in 2021 were still in the early stage, and the performance there was consistent with those in the previous two years.

Looking at the field of those projects, CeFi and infrastructure have seen more financing after the Series C, while the projects in DeFi, NFTs, and Web3 were more mostly seeds and Series Afinancing.

A large number of financing events in DeFi, the high total amount in CeFi, while gaming is quite favored

Which fields are the institutions investing in? The answer to this question has always been regarded as a bellwether for industry development. According to statistics, from the perspective of major categories, 388 out of the 1,351 investment and financing events in 2021 were in the DeFi field, accounting for about 28.72%, 287 were for infrastructure, and 284 in the field of NFTs, accounting for 21.24% and 21.02% respectively. The number of events in CeFi and Web3 was relatively small. Therefore, judging by the number of investment events, DeFi was still one of the areas where capital was most concerned.

But in terms of investment and financing amount, the situation is different. The total amount disclosed in the CeFi field is about$15.06 billion, the highest of all categories, while DeFi only disclosed$2.09 billion, the lowest of all categories. In addition, the total amount disclosed in the infrastructure sector was also relatively high, reaching$7.55 billion. NFTs and Web3 were relatively new fields but the total disclosed amount there was not small: about$3.61 billion and $2.21 billion respectively.

On major sub-segments, gaming was undoubtedly the most favored by capital in 2021. According to statistics, a total of 141 investment and financing events in the gaming field were disclosed in 2021, totaling$3.528 billion, both of which ranked first among all sub-segments. Among gaming projects, the vast majority were under the NFTs category, accounting for about 65.25%, followed by some under the Web3 category, accounting for about 26.95%.

In addition to gaming, the sub-segments with more disclosed investment and financing events in 2021 were tooling, trading, and marketplace, which counted at 68, 52, and 52 respectively. Other popular areas such as metaverse, lending/borrowing, and yield only disclosed 33, 45, and 23 events respectively, which were not too much. Areas like debt, tax, investment, brokerage, and enterprise saw even fewer such events, all less than 10.

The sub-segments with relatively more total disclosed investment and financing amount in 2021 included exchange, mining, custody, and payment, totaling$3.176 billion, 1.976 billion $1.686 billion, and $1.632 billion respectively. In addition, enterprise, banking, brokerage, and layer1 disclosed a total investment and financing amount of more than$1 billion. Areas with less disclosed investment and financing were yield, debt, smart contracts, savings, tax, and security, all under$300 million.

APP

APP