Original author: Arthur Hayes, co-founder of BitMEX

Original translation by Luffy, Foresight News

Last week, Arthur Hayes posted on social media that he had liquidated all his HYPE and NEAR positions and said he would explain the underlying logic in detail in an article this week—this article is a response to that.

Its core viewpoints are as follows:

The escalating situation in Iran, coupled with companies' inventory replenishment cycle, may drive energy prices further up.

Between now and the beginning of the third quarter, the market will see the IPOs of three major AI projects.

Trump may shift to an anti-AI stance before the midterm elections in an effort to win over more Republican voters.

The peak of this market cycle will most likely occur between now and September.

For investors in risky assets, it's now time to gradually take profits. The following is the original text:

Is all of this just my imagination, or is it really true that investing in artificial intelligence these days simply requires subscribing to Citrini Research's service and blindly buying all the stocks they recommend?

Am I dreaming? Or have oil prices already lost their influence on the economy and politics? This is why Trump and the Iranian Islamic Revolutionary Guard Corps were able to exchange barbs on social media, while a large number of ships were stranded in the Strait of Hormuz.

With the two-year U.S. Treasury yield 0.5 percentage points higher than the effective federal funds rate, the market is sending such a clear signal: will the Federal Reserve really hold off on raising interest rates at its next policy meeting?

Will all the benefits that artificial intelligence has created for the United States really end up in the hands of a few tech professionals?

The chaotic world before me forces me to conduct a reality check to determine whether I am truly awake or trapped in a dream. If the check proves it's all an illusion, I will immediately adjust my portfolio. This article is my test. After typing these words and organizing my thoughts, my portfolio will undergo significant changes, or it may remain unchanged.

My core judgment begins here: the current market situation is more like a dream. Within the entire investment system, the price of oil and other hydrocarbon energy sources is a core variable with a reverse transmission effect. The essence of human perception of the world is the conversion of energy into biological intelligence, and the logic of artificial intelligence follows the same pattern. This law will never be broken. The market may deviate from this common sense in the short term, but reality will ultimately prevail.

This article will begin with oil prices and ultimately focus on the US presidential election. The current situation could very well trigger a bursting of the artificial intelligence stock market bubble, dragging down the entire crypto market as well.

Once the dust settles, Bitcoin will have a chance to bottom out and rebound. I previously asserted that Bitcoin would never reach the $60,000 mark again, but that prediction has clearly been wrong, which is typical for market forecasts. I always adhere to one principle: opinions can be clear, but there's no need to be stubborn.

Next, we will proceed with the analysis.

Whether or not to negotiate has become the core issue at present.

Politicians always act in their own self-interest. The reasons behind Trump's unprovoked military action against Iran are likely known only to him. Faced with the constant stream of explanations from him and his advisors, the outside world is unable to discern the truth. At this point, dwelling on the causes is pointless; the real question is whether Trump and the Iranian Islamic Revolutionary Guard Corps will choose a ceasefire and, if so, how to end the standoff.

This conflict is now entirely dominated by Trump, and for him and the Republican camp, starting a war in an election year is undoubtedly a passive move.

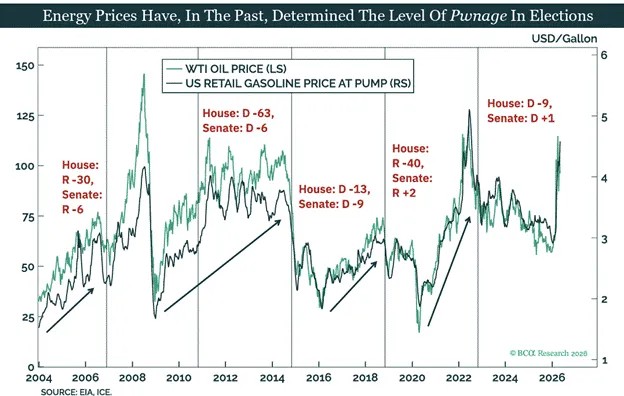

In the United States, the prices of necessities like gasoline and food often directly influence election results. Currently, navigation through the Strait of Hormuz is disrupted, and energy and food inflation continues to rise. The root cause of all this is the Trump administration's hasty action against Iran, launched without public consultation. Some may point the finger at Israel, but this argument is completely unfounded. Understanding American history reveals that domestic forces will never obey external orders.

As long as the war doesn't affect their own lives or cause casualties among family and friends, the American public is not opposed to war. Trump has repeatedly emphasized that only thirteen American soldiers died in this special military operation. This is also why the United States is keen on using advanced long-range weapons and waging "game-like wars."

Even though Trump's initiation of this Middle East war lacked a clear winning strategy and went against the expectations of many supporters, his base still chose to side with the Republican Party. The fact that some Republican lawmakers, due to wavering in their stance, faced pressure from within Trump's own party and lost their elections further confirms this.

Trump's core concern isn't that his base voters are unwilling to vote in the November election, but rather that soaring prices will cause a large number of swing voters to gravitate towards the Democrats. The cost of living has become the biggest obstacle in Trump's re-election campaign.

To win over swing voters, Trump needs to at least stabilize current oil prices. With supply chains only now beginning to absorb the pressure from rising energy and raw material costs, completely curbing inflation is unrealistic. All Trump can do now is manage market expectations of inflation, not change inflation itself.

Whether Trump is willing to reach a reconciliation with Iran depends entirely on the trend of oil prices.

As oil prices continue to rise, his stance tends to soften; however, once the market anticipates impending negotiations and oil prices subsequently fall, he changes his tune. After all, from a geopolitical perspective, the agreement reached in this round of negotiations is likely to be more passive than the agreement signed between the Obama administration and Iran. In the eyes of many voters, this is tantamount to "defeat," and the Republican Party will pay a price for it in the election.

Negotiations always require concessions from both sides, and the Iranian Islamic Revolutionary Guard Corps has similar considerations. When oil prices are too high, its major trading partners will pressure Iran to compromise with the United States; however, once Iran signals a willingness to negotiate and oil prices fall, the pressure from its trading partners will also decrease.

Given current oil price levels, neither the US nor Iran has any incentive to back down. While oil prices are significantly higher than before the war, they have not yet reached a level that could trigger a full-blown crisis. The commodity market is generally stable, there is no large-scale famine globally, and most countries can replenish their supplies of key industrial materials through other channels.

However, this delicate balance is destined to be unsustainable. The significant reduction in global supply of core energy sources, coupled with consistently stable prices, defies market principles.

Once global spare capacity is exhausted, spot prices will inevitably rise sharply, a consensus shared by many commodity analysts. The crisis has not yet fully erupted simply because global energy reserves were ample before the war.

If the stalemate between the US and Iran continues until the end of the second quarter, spot prices for hydrocarbon energy and various basic commodities will inevitably surge in the third quarter of this year.

To paraphrase Churchill: Politicians always find the right choice only after exhausting all other options.

Only when the situation completely spirals out of control will Trump and Iran truly sit down at the negotiating table. In my view, the current disruption to shipping in the Strait of Hormuz will most likely continue until the beginning of the third quarter.

Let's assume that oil prices will gradually rise amid fluctuations. In this context, how will the rising oil prices interact with Trump's campaign rhetoric?

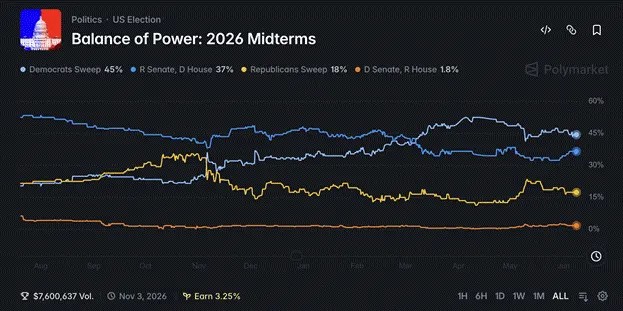

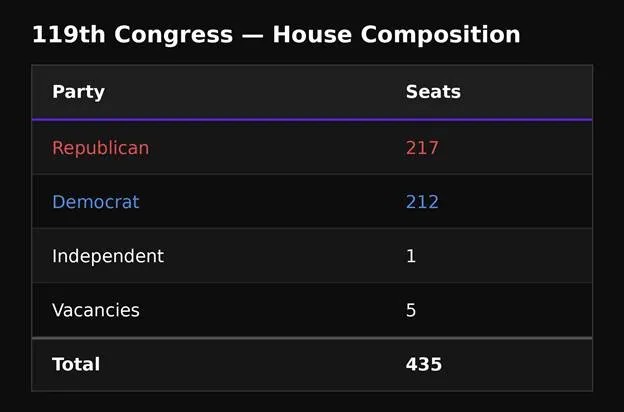

November Election Showdown: Republicans vs. Democrats

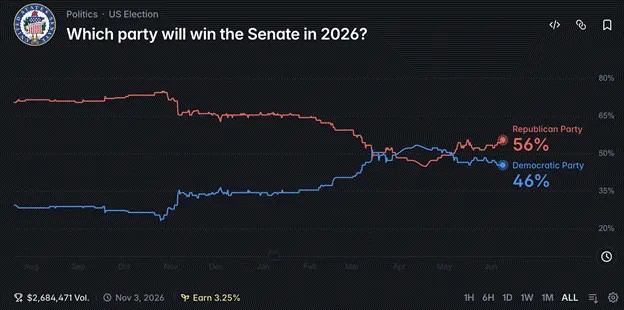

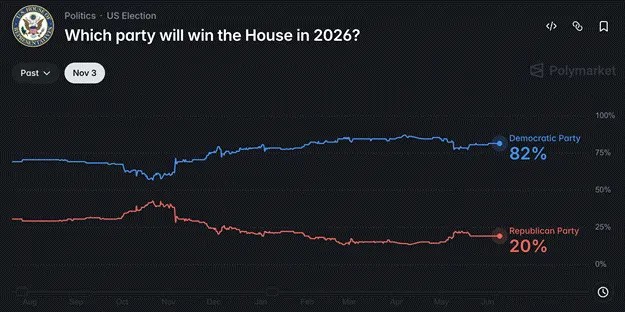

According to odds from the prediction market Polymarket, the Republicans can only retain control of the Senate by a narrow margin, while suffering a significant loss of seats in the House of Representatives.

While many believe the Republicans will lose the House, I disagree. Trump still has a chance to turn the tide, and the key lies in shifting public opinion and issuing statements regarding regulations and taxes related to data center construction and the artificial intelligence industry.

The current vote distribution among political parties is as follows (218 votes are needed to pass a bill):

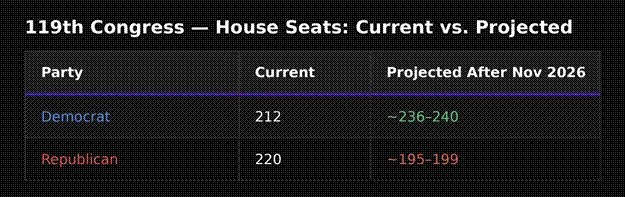

Based on Polymarket's current odds, the following is the projected party composition after the election:

The Republican Party's position in both the House and Senate is not optimistic after the election. However, the Republicans can change the situation through redistricting; when the existing rules are destined to fail, changing the rules becomes inevitable. Assuming Polymarket's prediction is correct, the Republicans need to gain 19 seats. Redistricting can reduce this number.

The following are the potential impacts of redrawing the selection area:

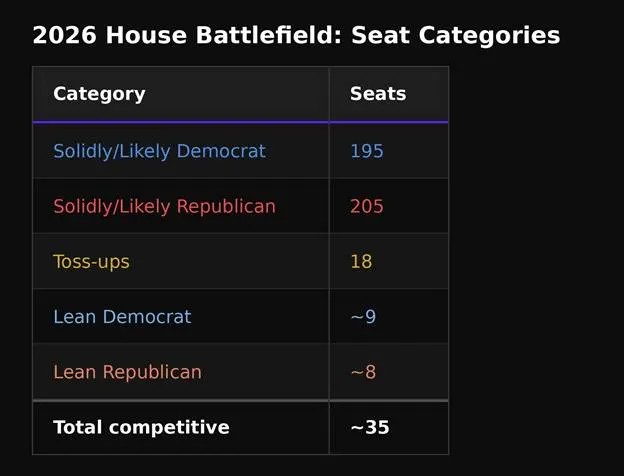

The Republicans now only need to win 11 more seats.

Next, let's look at which elections are close and, based on current polls, which districts might slightly lean towards the Republican Party within the margin of error.

The allocation of 35 seats remains highly uncertain. As mentioned earlier, high inflation and rising living costs are negative issues that Trump is unlikely to reverse. Another major topic currently affecting voters from both sides is the expansion of data centers and the impact of artificial intelligence on the job market.

Aside from the ultra-wealthy, almost everyone is worried that data center construction will drive up costs and that artificial intelligence will take away jobs. Many regions have already introduced policies to postpone new data center projects, and there are growing calls for increased taxes on AI companies and subsidies for ordinary citizens. After all, the vast majority of people are not executives or high-paid employees in AI companies.

For voters in contested districts, these issues are extremely influential. Trump could easily win the remaining crucial seats by making statements about the artificial intelligence industry. At this stage, he only needs to make related remarks, without enacting any specific legislation. He only needs to promise the general public that if the Republicans win, they will begin to regulate the artificial intelligence industry after the election.

As a seasoned politician, Trump has always been adept at making campaign promises, but rarely delivers on them.

The handling of Epstein's files is a prime example. During his campaign, he loudly proclaimed a thorough investigation of those involved, but after taking office, he only released a small amount of information. Now, he could do the same thing: during his campaign, he promised to pass legislation to slow down data center expansion, impose a windfall profits tax on artificial intelligence companies, and use the revenue to distribute a new round of relief funds; after the election, once the Republican Party has secured power, he could gradually retract these statements.

Some may find it hard to understand why Trump would emulate the actions of left-wing Democratic politicians. But let's not forget that he launched the largest universal relief program in the United States since Roosevelt's New Deal, and he did not restrict the use of relief funds for everyday consumption by the lower classes.

For Trump, temporarily distancing himself from AI giants like Elon Musk and cultivating an image of supporting ordinary people is not difficult in order to maintain his political standing.

If Trump does indeed make tough statements regarding the artificial intelligence industry, the market will not see it as a mere campaign tactic, but rather as a sign that the US will substantially restrict capital expansion in the AI sector and increase industry taxes. Panic will spread immediately, and the AI stock market bubble will burst.

Previously, Elon Musk and Trump had a public spat on social media, with Musk's affiliated departments publicly questioning Trump. Trump subsequently announced he would cancel government contracts related to Musk's companies, causing Tesla's stock price to plummet 18% in a single day. This demonstrates the market's sensitivity to such controversies. Politics can support an industry, but it can also deliver a devastating blow in an instant.

The dispute was later proven to be just a publicity stunt, and the two quickly reconciled. Musk was even invited to attend the recent summit between Trump and Chinese leaders in Beijing.

However, the market believed it at the time, triggering a massive sell-off.

This is just the ripple effect caused by the personal conflict between the two. Once Trump, representing the Republican Party, clearly states his plan to impose heavy taxes on artificial intelligence models and related intelligent agents, the impact will be far greater than before. Similar remarks had previously circulated in South Korean political circles, causing the local stock index to nearly hit its daily limit down the following day, only returning to an upward trajectory after an emergency official denial.

The current market's optimistic expectations for the artificial intelligence sector are based on the premise that the industry's revenue will continue to grow exponentially and that the concentration of new technologies and wealth will not provoke public resistance. This idea is detached from reality and is more like being immersed in a dream.

Trump's statement will be the real test to shatter this illusion. Whether he will actually take action still depends on oil prices.

As the situation in Iran continues to push up oil prices and inflation worsens, Trump will have fewer campaign rhetoric options left, ultimately leaving him with no choice but to target the data center and artificial intelligence industries.

Trump's reasons for desperately avoiding Democratic control of the House of Representatives are quite clear. If the Democrats win the House, they can exercise subpoena power, repeatedly summoning Trump, his family, and key aides to testify and posing a variety of pointed questions. If the Democrats were to return to the White House in 2028, the Department of Justice, with its vast resources, would then launch a purge, investigating Trump's business entities.

Let's break down the entire logic: the US and Iran's inability to reach a reconciliation will inevitably lead to higher oil prices; rising prices will cause voter dissatisfaction, and Trump can only win votes by regulating and taxing the artificial intelligence industry.

Even if AI-related stocks halve in value between now and the November election, it would be an acceptable price for Trump to pay in exchange for escaping the endless investigations by the Democrats. After the election, he could easily reverse his previous statements regarding data centers and AI, and the industry would return to normal, with the S&P 500 potentially even challenging the 10,000 mark.

However, for investors, market movements are interconnected. The sharp decline in the artificial intelligence sector will completely alter market expectations for its future returns. Having experienced the impact of regulation and heavy taxes, investors can no longer be as blindly optimistic about this sector as before.

California Dream: Where is the Liquidity Going?

Before analyzing the impact of the planned IPOs of SpaceX, Anthropic, and OpenAI on the global financial market, let me first explain a question: Since the end of the third quarter of last year, the US dollar liquidity has been continuously loose, but Bitcoin has failed to experience a corresponding surge. What is the reason behind this?

On November 30, 2022, ChatGPT was officially launched to the public, marking the beginning of an artificial intelligence super bubble. Around the same time, the scandal involving FTX founder SBF misappropriating user funds was fully exposed. After hitting a low of approximately $15,000 that year, Bitcoin surged to $125,000 in October 2025, a cumulative increase of over six times.

However, during the same period, Nvidia's stock price increased elevenfold, and many small and mid-cap tech stocks that rely on computing power and convert electricity into intelligence also experienced explosive growth. The performance of the artificial intelligence sector far outpaced the crypto market, and the gap between the two has continued to widen since the end of 2024.

Even with Bitcoin (white) reaching an all-time high, Nvidia (gold) still outperformed it.

Bitcoin (white) performed even worse after hitting an all-time high, and has since fallen by 50%.Nvidia (gold), the world's most valuable company, has still risen 10% since the end of 2025.

Based on my past logic of judging the crypto market based on fiat currency liquidity, Bitcoin should have seen a higher increase in the current environment, but the reality is quite the opposite. Where exactly did things go wrong?

I used to focus on the overall increase in fiat currency issuance, but I overlooked the specific flow of funds. I originally thought that liquidity would eventually flow into Bitcoin, driving up the price, but this time my judgment was wrong.

My conclusion is that almost all of the new dollar liquidity has been absorbed by the artificial intelligence (AI) sector. AI is a highly capital-intensive industry, and building massive data centers capable of operating AI requires enormous amounts of energy. Hydrogen, nuclear, and renewable energy sources are converted into electricity, which is then transmitted to data centers where specialized chips perform model training and inference calculations.

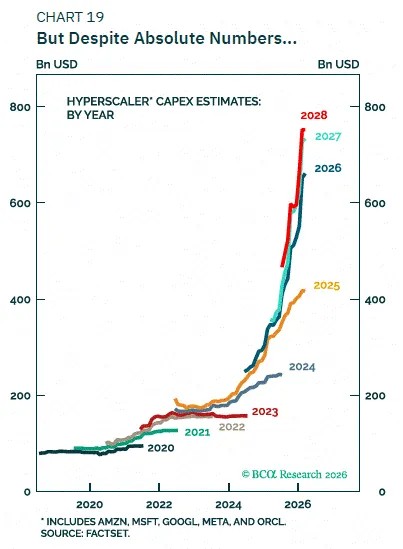

Starting in 2024, global capital expenditure on data centers began to surge, and this surge intensified in 2025, leading to a sharp increase in industry financing demand. According to publicly disclosed data, from November 2022 to the present, the total amount of debt financing in the field of artificial intelligence has reached US$1.5 trillion, which is exactly the same as the increase in the broad money supply M2 in the United States during the same period.

The answer is obvious: all the newly added US dollars have flowed into the artificial intelligence sector, and Bitcoin naturally doesn't get a share of the incremental funds.

Bitcoin's strong rebound from the low point of FTX's bankruptcy in 2022 is only possible because the massive debt expansion of the artificial intelligence industry is mainly concentrated after 2025. Of the $1.5 trillion in debt, $1.3 trillion was incurred from 2025 to the present.

Coincidentally, the peak price of Bitcoin will occur in October 2025, which coincides with an unprecedented level of capital expenditure in the field of artificial intelligence.

This interconnectedness is crucial. If the AI-driven stock market crashes, there will be no more surplus funds available to invest in Bitcoin.

Banks will tighten lending, and many institutions will discover that loans previously issued based on falsified revenue data harbor significant risks. When the stock prices of leading tech companies plummet by more than 50%, bank loan officers will begin to worry about the companies' inability to repay their debts, leading to a contraction in credit and further tightening of overall market liquidity. Coupled with the negative attitude of the US political establishment towards the artificial intelligence industry, it will be difficult for the industry to receive financial assistance in the short term.

Even if the government intervenes to bail out financial institutions, based on the current situation, such measures will likely only be implemented after the November election.

The link between Bitcoin and artificial intelligence stock prices means we must make judgments: Is there a bubble in the AI stock market, when will it burst, and what are the underlying causes?

The AI bubble is doomed to face a triple blow.

Three factors could burst the current AI bubble: rising energy costs, the market's inability to absorb the massive IPOs of SpaceX, Anthropic, and OpenAI, and Trump's anti-AI policy rhetoric.

The core logic of artificial intelligence is to maximize the efficiency of "energy-to-intelligence" conversion. Humans rely on consuming food to convert energy and generate intelligence, while artificial intelligence relies on electricity. Currently, most of the new electricity consumption of data centers depends on hydrocarbon energy sources such as natural gas.

Rising energy prices mean that the cost of operating artificial intelligence and generating computing power will increase accordingly, directly squeezing the profit margins of companies such as Google, Anthropic, and OpenAI.

As costs rise, companies will raise service prices, slowing the growth rate of user adoption of computing power and models. The ongoing geopolitical tensions between the US and Iran continue to drive up oil prices, ultimately eroding the profitability of AI companies. When the market begins to question the rationale for continued expansion of data centers, an industry turning point will arrive, with companies' expected price-to-earnings ratios shrinking significantly, and a bear market officially beginning.

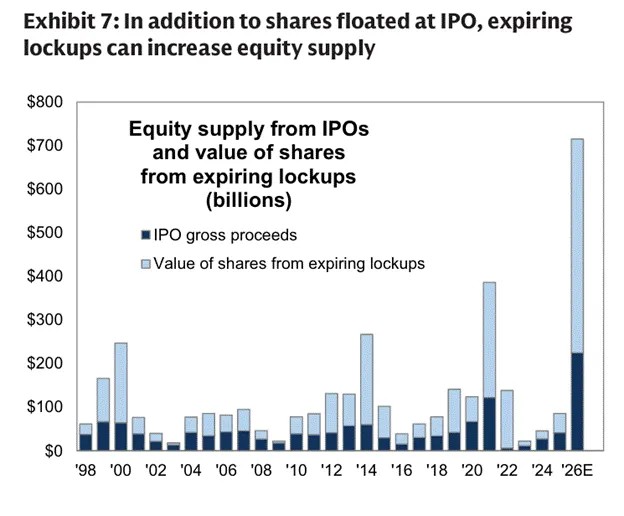

In addition, the lock-up periods for shares held by SpaceX, Anthropic, OpenAI, and other technology companies are gradually being lifted, coupled with large-scale IPOs. The overall financing scale even exceeds the total financing of all new shares raised during the dot-com bubble, making it unprecedented in scale. Whether the market can withstand such massive selling pressure is a big question mark.

The artificial intelligence sector has seen a sustained rise in recent years, based on investors' strong belief that industry profits will continue to accelerate. Once market confidence in the sector's prospects wavers, investors will lower their valuations of future earnings. The IPO performance of these giants will become a bellwether for market sentiment. If the IPO falls short of expectations, investors will assume the industry has peaked, triggering a collective sell-off.

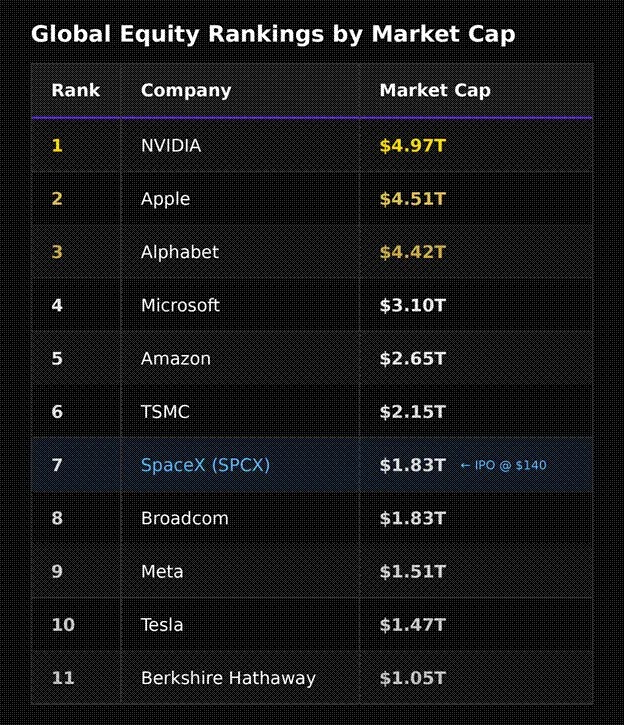

Let's take SpaceX, with its relatively complete information disclosure, as an example. The capital market has always followed the rule of "first come, first served." Elon Musk, a master of marketing, chose to go public first, allowing the company and early shareholders to cash out to the maximum extent possible. Crypto market participants can easily understand this model: extremely low circulating supply, completely diluted valuations yet persistently high valuations, similar to the operating logic of some altcoins.

According to SpaceX's IPO filing with the U.S. Securities and Exchange Commission, the company's valuation in this IPO is nearly 100 times its revenue. More notably, the company is initially releasing only 4% to 5% of its shares. Given the current surge in the artificial intelligence sector, the stock price is likely to surge on its first day of trading, but such high market expectations also mean it will be difficult to sustain investor expectations.

After its IPO, SpaceX's market capitalization will reach $1.8 trillion, making it the seventh largest company in the world by market capitalization. If its stock price rises by another 50%, its market capitalization could surpass Amazon and rise to fifth in the world, but its profitability is completely inadequate to match this market capitalization level.

Nvidia's ability to maintain a high valuation relies on its considerable gross margin and revenue scale, while SpaceX focuses on space data center business. Industry analysts point out that the construction and operation costs of such facilities are four times that of ground-based data centers, and it is expected that cost break-even will not be achieved for at least ten years.

If the initial valuation is more rational, the subsequent stock price trend will be more stable. Participants in the crypto market understand this logic: if secondary market investors cannot profit, the unlocked shares of insiders will have no buyers, and the stock price will only continue to decline.

Looking at the pace of share unlocking, from now until early September, SpaceX's circulating shares will increase fivefold, with a massive influx of shares into the market, putting enormous upward pressure on the stock price. To make matters worse, Anthropic and OpenAI also plan to launch their IPOs in September, both companies aiming for a trillion-dollar market capitalization.

SpaceX may have some room for a brief surge between June and September this year, but when three extremely highly valued companies go public simultaneously, and a large number of new shares flood the market, market disappointment is bound to spread. Investors are expecting a surge in stock prices, and a slight upward fluctuation simply cannot meet their expectations.

In summary, the combined negative factors of rising energy prices, a wave of mega-IPOs, and Trump's regulatory stance on the industry make it difficult for these companies to meet market expectations in terms of listing performance. Once investors lose faith that AI-related companies can maintain exponential profit growth, the valuation of the entire sector will be revised downwards, and stock prices will collectively weaken.

Currently, there is a large amount of stock-pledged loans in the artificial intelligence field, and banks have provided huge amounts of credit for the industry's capital expansion. After the sector crashes, the banking system will suffer huge amounts of bad debts.

Amid the bursting of the global AI bubble and a general decline in various risky assets, Bitcoin is unlikely to exhibit independent price movements in the short term. Once the market has fully cleared, Bitcoin will likely be the first to bottom out. At that point, to rescue the overall economy, a new round of large-scale monetary easing will likely occur, and Bitcoin will begin a new upward trend. However, for now, the primary task is to protect the principal of your crypto assets.

Before sharing Maelstrom Fund's stock and crypto asset holding strategies, let's analyze the direction of the Federal Reserve's monetary policy.

The Federal Reserve Chairman's Dilemma

Newly appointed Federal Reserve Chairman Kevin Warsh is in a very delicate situation, with mixed reviews of his style of work, and it all depends on how he handles the Fed's current contradictory predicament.

The difference between the two-year U.S. Treasury yield and the effective federal funds rate directly reflects market sentiment; the chart also includes the near-month WTI crude oil futures price.

Trump nominated Kevin Warsh to be the Federal Reserve Chairman with the intention of pushing for interest rate cuts. Warsh had previously signaled that inflation caused by geopolitical conflicts was only a short-term phenomenon, while productivity gains brought about by artificial intelligence were a long-term trend, and the Federal Reserve could take this opportunity to lower interest rates.

However, the market gave a completely opposite signal. The two-year Treasury yield was 0.5 percentage points higher than the effective federal funds rate, which means that the market believes that, influenced by persistently high inflation, the Federal Reserve should choose to raise interest rates rather than lower them at its policy meeting on June 16-17.

Currently, maintaining the current interest rate is the most probable outcome for the Federal Reserve. However, the market will focus on the post-meeting press conference and any adjustments to the reserve management program. Even if the Fed holds rates steady, the market will likely categorize it as either hawkish or dovish.

A hawkish stance on maintaining stable interest rates has the same impact as a rate hike. On the one hand, the unresolved US-Iran conflict and continuously rising oil prices; on the other hand, the simultaneous listing of three major AI giants and the resulting pressure on market supply. With multiple negative factors combined, all risky assets will experience varying degrees of correction.

The worst-case scenario is that Trump instructs Warsh to immediately raise interest rates in response to market demands, attempting to win voter support by suppressing prices. However, unless the Federal Reserve raises rates significantly and simultaneously sells bonds in the open market to reduce its balance sheet, it still won't be able to keep up with inflation. This scenario is strikingly similar to the situation in the 1970s: the Federal Reserve aggressively raised interest rates, but the力度 (intensity/strength) was consistently insufficient to curb inflation.

In the current environment, the likelihood of the Federal Reserve cutting interest rates is extremely low. Regardless of whether it ultimately chooses to raise rates or keep them unchanged, the market will interpret this as a signal of tightening liquidity, further dampening bullish sentiment in the artificial intelligence sector.

In summary, the upward trend in oil prices will ultimately become a negative factor for all risk assets. Next, let's discuss the specific holdings of the Maelstrom fund.

Portfolio layout

Everything in the world depends on energy. Given the prediction that energy prices will rise in the future, investing in energy-related assets is an inevitable choice.

The US and Iran remain deadlocked, disrupting shipping in the Strait of Hormuz and resulting in increasing daily losses of crude oil and natural gas supplies. While market sentiment is currently stable, a continuation of this standoff will inevitably lead to rising energy prices.

Various industry data all point to the same conclusion: affected by geopolitical conflicts, global energy inventories have fallen to recent lows and are still declining. Once inventories fall below a critical threshold, the entire energy supply system will face problems, and prices will experience an uncontrolled surge.

Even if the situation reaches the best possible outcome—an immediate ceasefire and normal shipping in the Strait of Hormuz—countries will still increase their purchases to replenish their stocks and build up their strategic reserves, pushing up oil prices.

Based on both scenarios, the medium- to long-term upward trend in crude oil and natural gas prices is established over the next three to six months, regardless of whether oil prices temporarily decline after a short-term peace agreement is reached. Therefore, we are heavily investing in US-listed energy production companies.

The energy sector has upside potential across various scenarios, and its current valuation is more favorable compared to the energy-dependent technology sector. Conversely, the prospects for assets that rely on cheap energy to maintain high valuations are less optimistic.

With oil prices climbing to $150 per barrel, it's difficult for the artificial intelligence sector to maintain its previous strong performance. Therefore, we have liquidated all our holdings in AI-related stocks.

New funds had been pouring into the artificial intelligence stock market, but once the sector experiences a rapid decline, even with the relatively resilient nature of crypto assets, it's difficult to attract further inflows. Based on this, we reduced our holdings of all non-core cryptocurrencies, selling HYPE, NEAR, and WLD last week, and liquidating our ZEC holdings due to the Orchard Pool vulnerability. Preserving our principal is more important than pursuing profits right now.

My current holdings consist only of Bitcoin and Ethereum. I don't have a significant need to liquidate my Ethereum holdings at the moment, so I will continue to hold them. I firmly believe that the bursting of the AI bubble will trigger a new round of financial turmoil, at which point the world will once again enter a cycle of monetary easing, and Bitcoin will initially fall before rising.

In the face of market volatility, we will hold our core positions for the long term while utilizing derivatives for short-term short-selling to capitalize on market fluctuations. After all, I don't want to give up the enjoyment of trading.

If the actual market movement turns out to be completely different from my prediction, and it turns out to be just a false alarm, that's fine too. Taking profits before embarking on the Mediterranean trip is a prudent choice. In early September, I will review the market movement and my previous assessment, and then buy back my shares based on market conditions.

Unlike investment institutions that need to realize fixed returns every year, Maelstrom Fund focuses more on long-term compound growth, and therefore has enough leeway to calmly cope with the intertwined changes in the market.