Macroeconomic Review

Trump's policy context

1. The path to reducing inflation

- Russia-Ukraine ceasefire: promotes peace between Russia and Ukraine, releases Russian oil and gas resources, and reduces global energy prices.

- The situation in the Middle East: may trigger new conflicts, pushing up oil prices in the short term but can be controlled through diplomacy.

- Tariff war: Raising import tariffs will lead to a mild economic recession in the short term and suppress inflation.

- Strategy toward China: Use tariffs to put pressure on China, start negotiations or implement economic containment.

2. Path to lower interest rates

- Intervene with the Federal Reserve: Pressure the Federal Reserve to cut interest rates and expand its balance sheet to stimulate global liquidity.

- Digital currency: Promote legislation, accelerate the development of digital currency, and weaken the Federal Reserve’s monetary control.

3. Stimulate economic path

- Tax cut policy: Make the Big Beautiful Act tax cuts permanent and increase disposable income for businesses and individuals.

- Tariff differentiation: Differentiated tariffs are imposed on manufacturing industries (e.g. Apple) to protect domestic industries.

- Attracting foreign investment: Through visits abroad (such as Saudi Arabia, Qatar, and the United Arab Emirates), over one trillion US dollars of investment has been locked in.

- Energy development: Expand oil and natural gas extraction and increase energy export revenue.

- Territorial Expansion: Explore the acquisition of Greenland, Canada, Mexico, Panama and other places to expand the economic territory.

4. Political familialization

- Wealth expansion: Accumulating family wealth through digital currency policies.

- Political legacy: purge dissidents, consolidate loyal teams, and ensure policy continuity.

Logical summary

Trump's policies are centered on economic stimulus, stimulating growth by reducing inflation (energy + tariffs), lowering interest rates (Fed + digital currency), attracting investment and energy development, and consolidating power and family interests through territorial expansion and political purges. The overall strategy is aggressive in the short term and relies on diplomacy and policy execution in the long term.

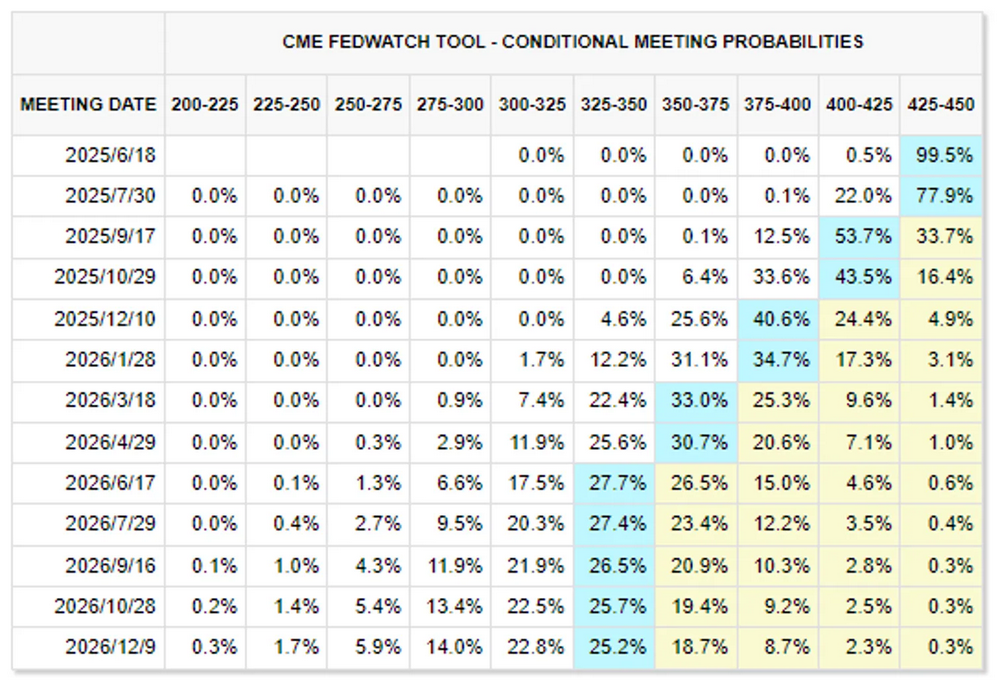

Neutral interest rate

The current market forecast is a 25bp rate cut on September 17, 2025, and two rate cuts in 2025 to 4.00%, with the neutral interest rate rising to 3.50%. Whether to start cutting rates ahead of schedule is the focus of the game between the Federal Reserve and the Trump administration. Trump's tariffs are now visibly turning into a long-term game, and the tariff recession is slowly beginning to emerge. At the same time, the Federal Reserve is secretly releasing water as U.S. Treasuries have rebounded in the past two weeks and have continued to QT. In the past week, the Federal Reserve has continued to reduce its holdings of U.S. Treasuries and tighten liquidity, resulting in a bullish adjustment in BTC, the float of global M2.

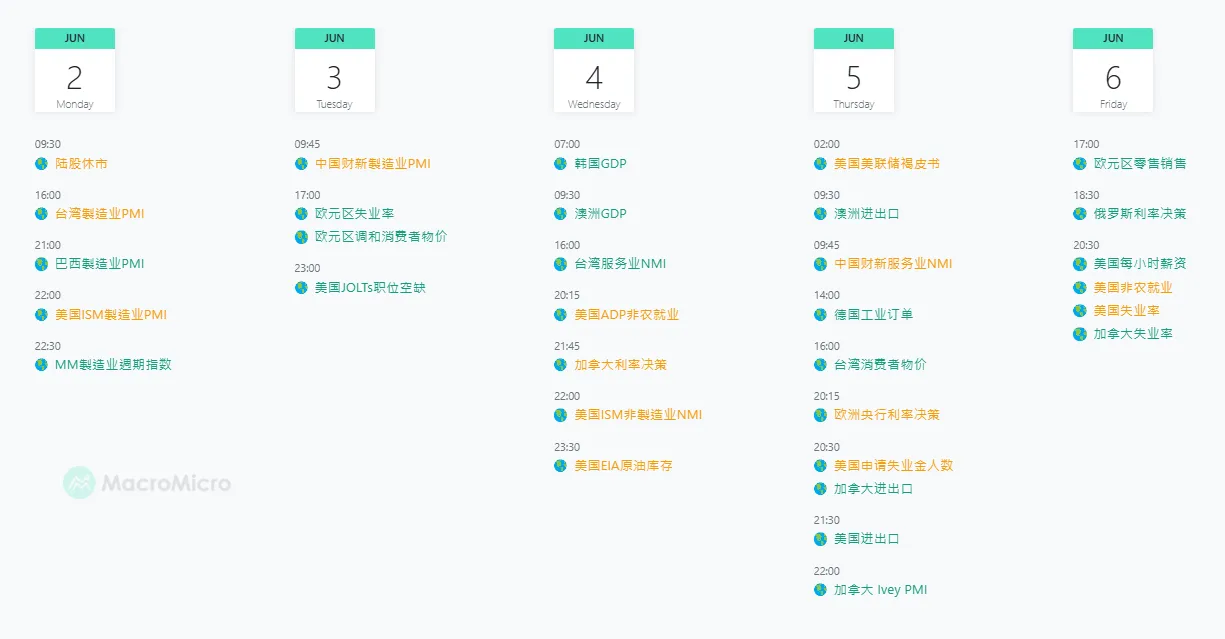

Next week's key events

Events (Central Bank Speeches and Policy Statements)

Key data to watch next week

On-chain data analysis

1. Changes in short- and medium-term market data that affect the market this week

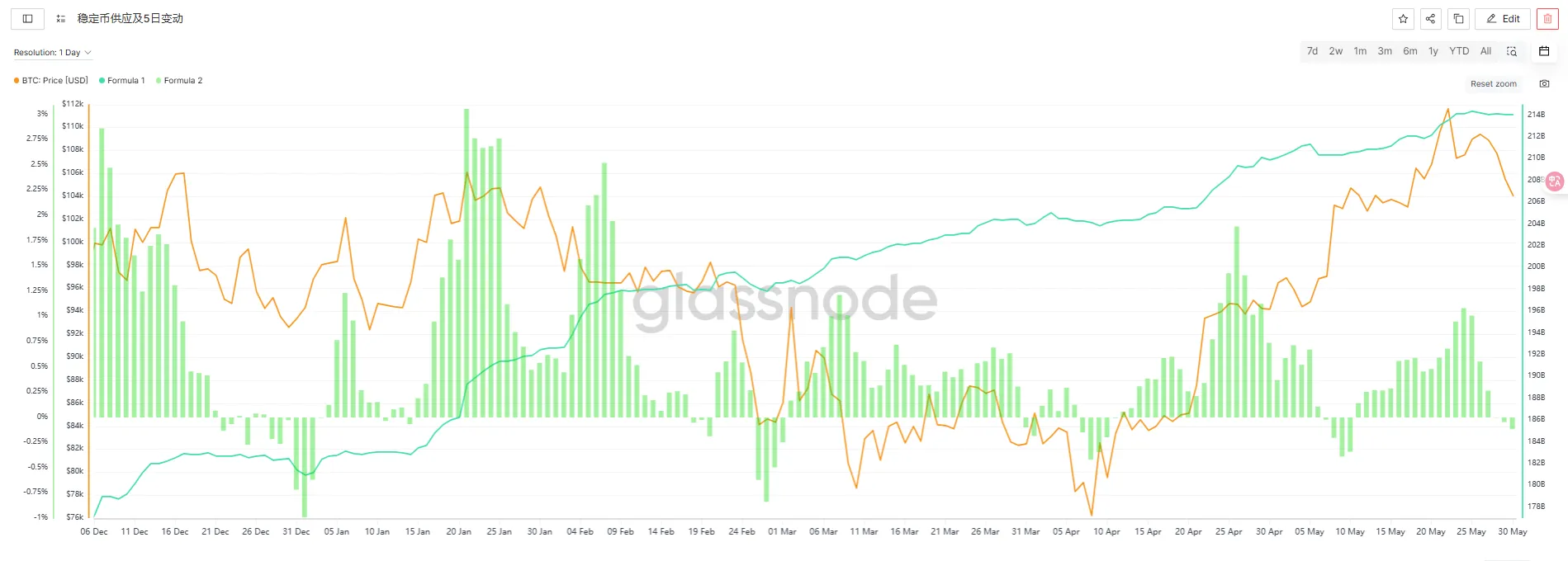

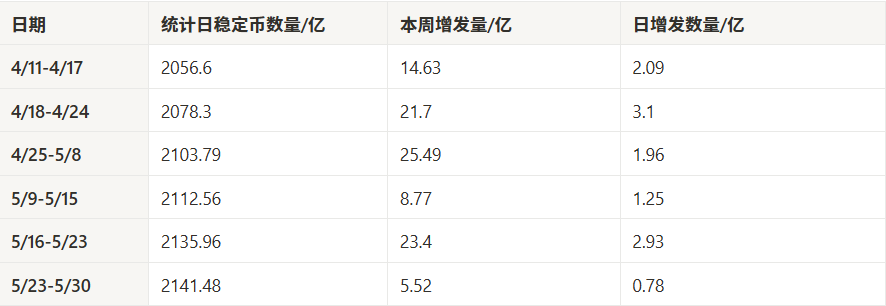

1.1 Stablecoin Fund Flow

The market volume has obviously shrunk this week, down 76.4% from the previous month. The market may start to cool down or be in a period of shock. The daily average issuance of 78 million is in a state of low liquidity, which often occurs when: the market lacks direction, trading volume shrinks; large investors and institutions wait and see; on-chain funds have no intention of entering the market, etc. If the downturn continues next week, it can be confirmed that this week is a complete "low issuance, low liquidity" period, and the market has entered a cooling period.

1.2 ETF Fund Flow

This week, the inflow volume dropped from 2.8 billion in the previous week to 670 million, and the inflow speed slowed down by 76%. It is almost the same as 5/5-5/9 (the periodic low point of ETF popularity), indicating that this wave of ETF market has come to an end. Last week, ETF inflows provided strong support for BTC, and the price once rose to 108,000. After the ETF volume shrank this week, the price subsequently fell back to 103,700, indicating that the current BTC price is highly dependent on ETF funds and lacks natural buying support from the market.

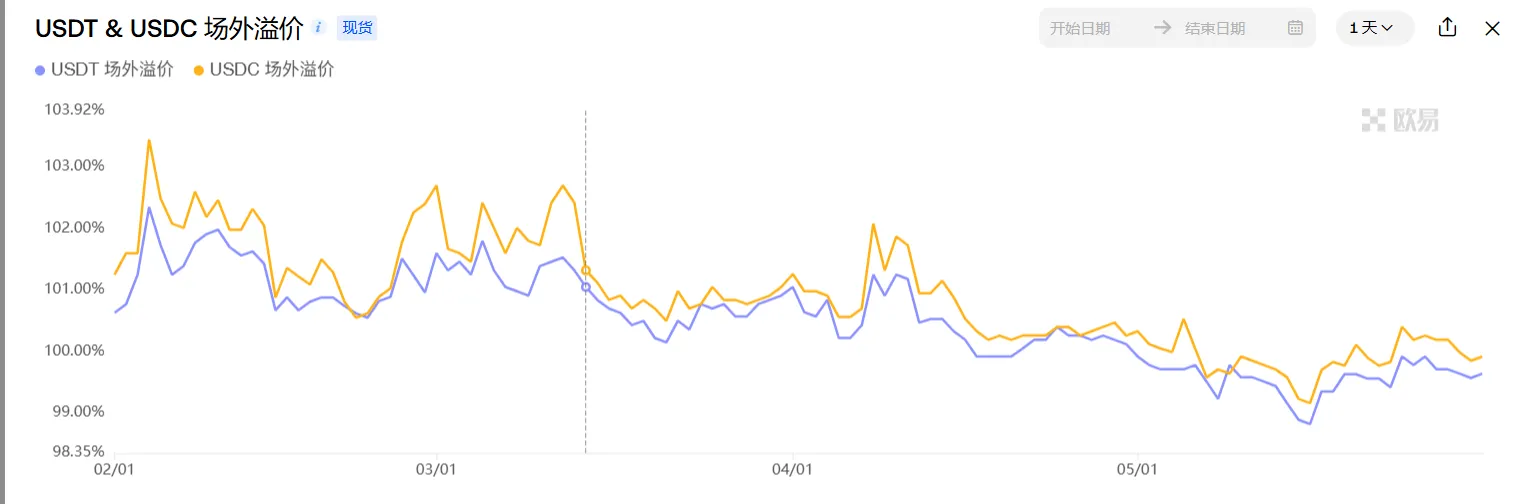

1.3 OTC Discounts and Premiums

From May 23 to 31, the overall OTC premium of USDT and USDC remained around 100.0%, with very little fluctuation, showing obvious wait-and-see sentiment among funds and slowing liquidity.

- USDT premium rebounded slightly to about 100.2% at one point, but overall it was still lower than the previous 2%-3% heat range;

- USDC premium is slightly higher than USDT, indicating that some cross-border or institutional funds still have preferences, but the intensity is limited;

- Overall, the premium of OTC stablecoins continues to be at "zero premium" or "discount edge", indicating that OTC buying is insufficient and the market lacks the motivation for new fiat currencies to enter.

1.4 MicroStrategy Purchase

Observing the price performance of MicroStrategy, it is obvious that it has fallen sharply, and the technical pattern does not support it. However, in this issue, we can see that MicroStrategy’s stock price did not actually create the previous high. The stock market’s enthusiasm for chasing highs for MicroStrategy is actually not as high as before. Although MicroStrategy has repurchased BTC, increased its net asset value, and brought incremental growth to the BTC market (we also mentioned in the last issue that it spent nearly US$4.5 billion since April 14), MicroStrategy’s stock price is at a premium compared to BTC. We should pay attention to when this round of the game will end.

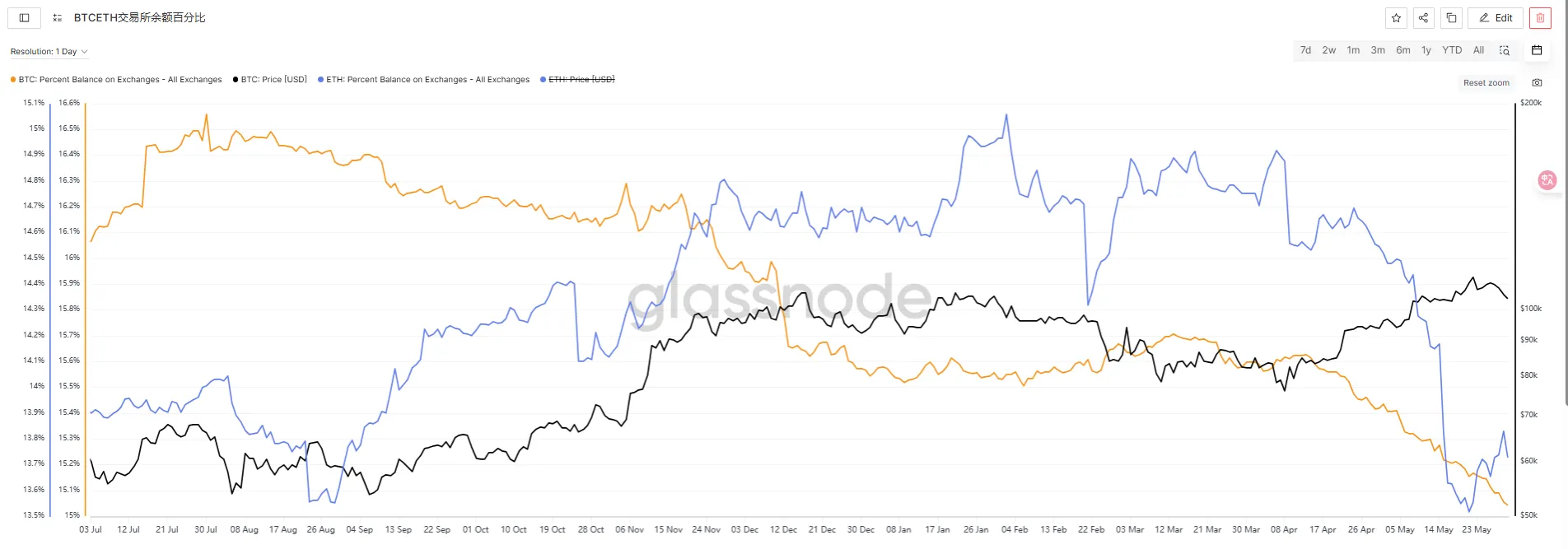

1.5 Exchange Balance

The proportion of BTC exchange balances continued to decline, falling to a one-year low of 15.046%, and the on-chain selling pressure was significantly reduced; this week, the proportion of ETH exchange balances rose from 13.52% to 15.83%. There is a certain amount of selling in the ETH market.

2. Changes in mid-term market data that affect the market this week

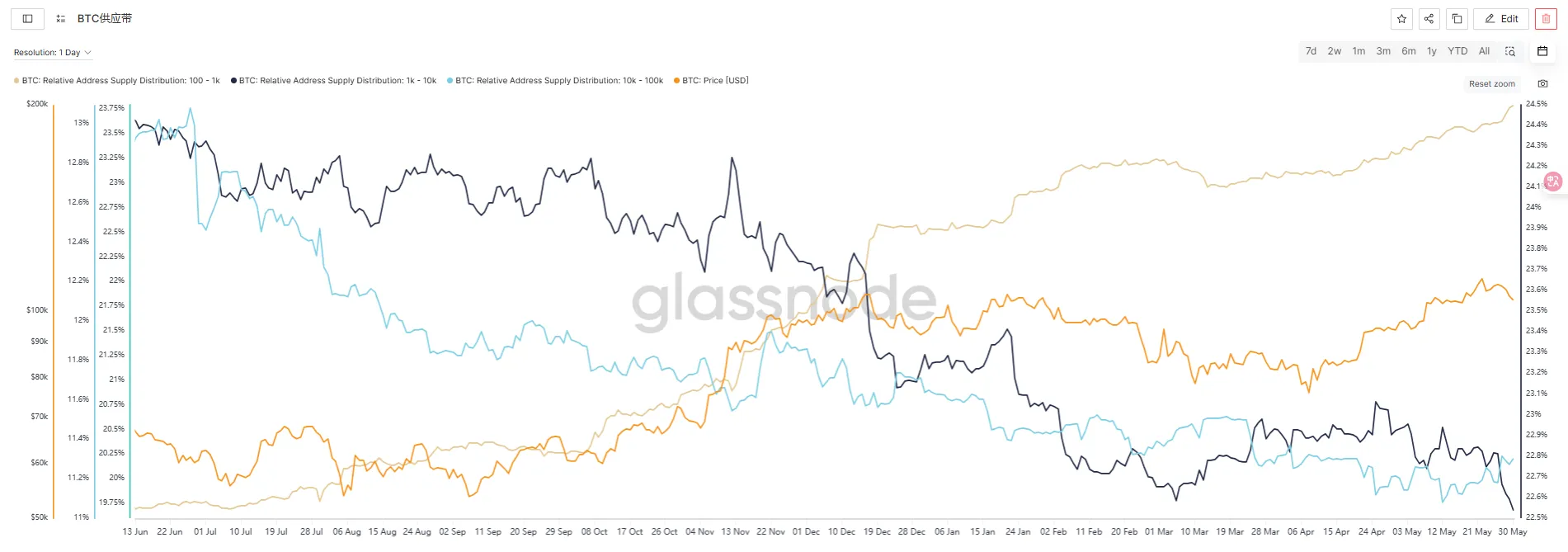

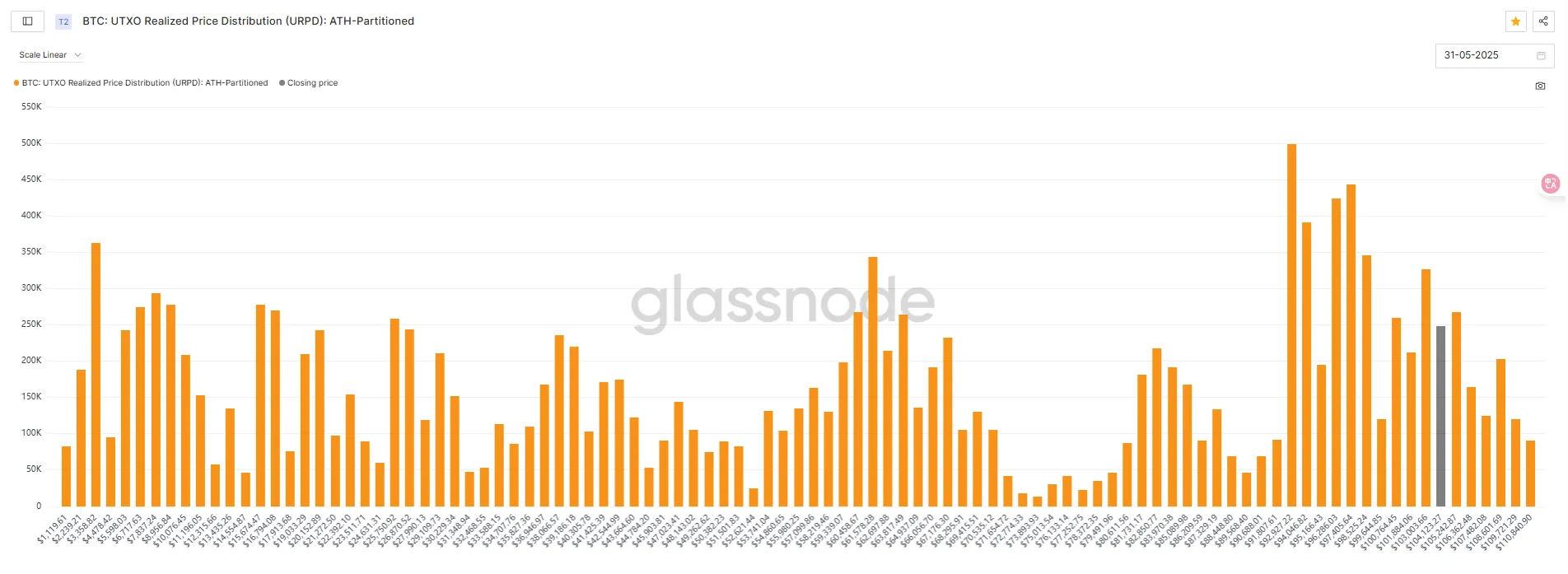

2.1 Coin holding address ratio and URPD

This week, the number of addresses holding 1K-10k coins showed a significant decline on the 26th and 27th, showing certain short-term bearish signs, but it was mainly absorbed by addresses holding 100-1k coins, so the short-term outlook is bearish. The medium- and long-term market structure has changed, and the URPD distribution of chips is relatively even, and there is no significant signal.

Combining the changing market conditions, funding data and on-chain data, the overall market is expected to continue to correct next week, especially after ETH rises again, which further confirms our confidence.

Special thanks

Creation is not easy. If you need to reprint or quote, please contact the author in advance for authorization or indicate the source. Thank you again for your support.

Written by: Sylvia / Jim / Mat / Cage / WolfDAO

Edited by: Punko / Nora

Thanks to the above partners for their outstanding contributions to this weekly report. This weekly report is published by WolfDAO for learning, communication, research or appreciation only.