Author: noveleader&0xatomist , Castle Labs

Compiled by: Tim, PANews

Aave is the foundational money market in the DeFi space, renowned for its strong liquidity and high trust levels. The Aave protocol accounts for over half of the total value of loans (TVL) in the lending market, making it the platform of choice for both institutional and retail investors. It expands liquidity through cross-chain technology, combined with a conservative risk management strategy, building a solid business moat and continuously innovating to strengthen its advantages. From the dual-market structure of version V3 to the upcoming Liquidity Hub and Spokes in V4, Aave has not only solidified its market position but is also gradually evolving into the infrastructure layer of on-chain capital markets.

Market positioning

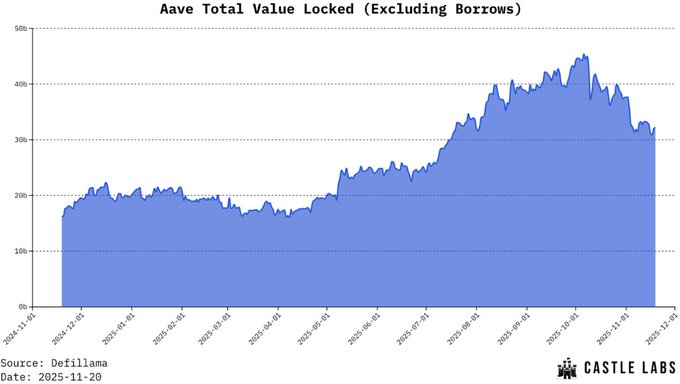

Aave, as the lending protocol with the largest TVL (TVL), holds a significant lead over its competitors. As of this writing, Aave's TVL is approximately $54 billion, more than five times that of Morpho (approximately $10.8 billion), the second-largest lending protocol. This scale advantage creates a strong competitive barrier, allowing it to attract institutional capital while still providing highly convenient access for retail investors seeking passive returns.

Aave's growth momentum remains stable, with its TVL recently reaching a record high. This growth is attributed to its first-mover advantage, continuous product iteration, and extensive multi-chain strategy.

The Aave protocol is currently deployed on 19 chains, but the vast majority of its liquidity (over 80%) remains concentrated on Ethereum, followed by Plasma. Among Layer 2 networks, Arbitrum has the most liquidity, followed by Linea and Base. This deployment reflects Aave's strategic choice: prioritizing Ethereum's liquidity depth and security, and then cautiously expanding to Layer 2 networks with continuously growing user activity.

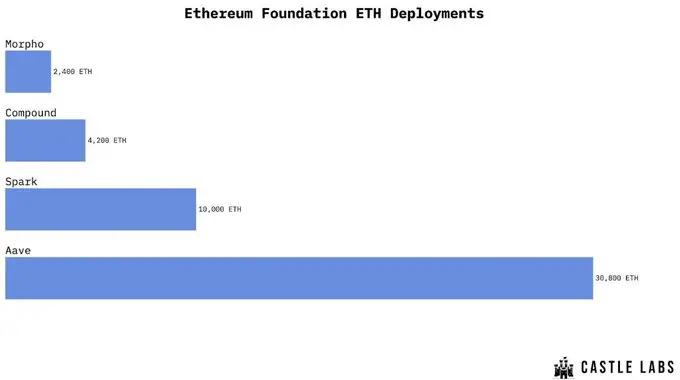

Aave's liquidity depth is uniquely attractive to high-net-worth individuals and institutional investors. These users can borrow and lend large sums without triggering a significant spike in borrowing rates. This advantage is evidenced by the Ethereum Foundation's deposit of 30,800 ETH into Aave in February 2025.

In addition, Aave has entered the RWA lending space through its Horizon Market, which currently has a market size of approximately $600 million. Aave accepts collateral from issuers such as Superstate and Centrifuge, consisting of tokenized components such as money market funds. Aave is positioning itself as a bridge between traditional institutions and DeFi, part of a broader strategy to facilitate institutional funding and complementing its existing massive on-chain user base.

Core Functions and Architecture Design

Aave operates on a liquidity pool model, where users deposit assets into a shared liquidity pool and receive aTokens representing their positions. These tokens accumulate interest over time and can be used as collateral to borrow assets.

The Aave V3 platform has launched two distinct lending marketplaces, each with its own unique function.

- Aave Prime marketplaces are optimized for capital efficiency and support only blue-chip assets. Its signature "Efficient Mode" allows loan-to-value ratios of up to 95% for highly correlated assets such as wstETH and WETH, with a liquidation threshold of 96.5%. The current market size is approximately $1.17 billion.

- Aave Core has a broader market reach, exceeding $42 billion in size, and supports a variety of assets. Aave Core prioritizes risk control, limiting exposure to high-risk assets through an "isolation mode" and enforcing stricter loan-to-value ratio limits, typically below 85%.

This dual-market structure reflects Aave's pursuit of a balance between capital efficiency and system security. However, this structure also leads to a fragmentation of funds, as liquidity cannot flow freely between the Prime and Core markets. Addressing this issue is a key focus of the upcoming V4 version.

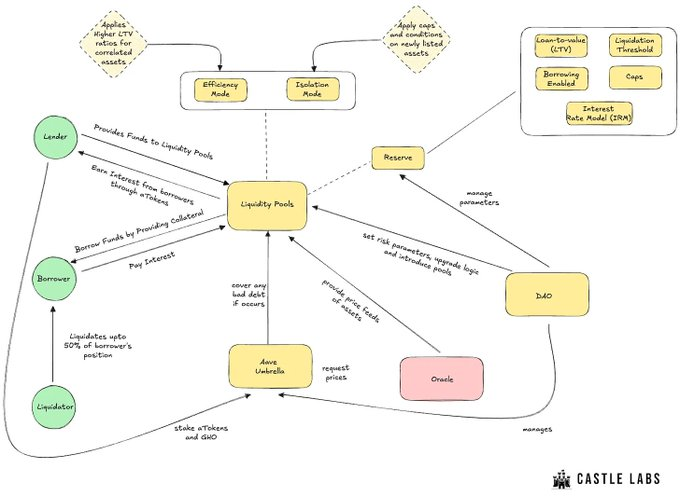

The diagram below illustrates the components within the Aave system, which work together efficiently to make Aave a leading money market protocol.

Liquidity pools and reserves

Each token market on Aave has a reserve fund, and its parameters are managed by the DAO.

- Loan-to-Value Ratio (LTV): This refers to the percentage of collateral value that can be lent out. For example, an LTV of 85% allows for a loan of $850 based on $1,000 of ETH collateral.

- Liquidation threshold: This level may trigger liquidation when the value of the collateral reaches this point. It is typically set slightly above the loan-to-value ratio to create a safety buffer.

- Lending Function Switch: Determines whether the reserve fund is open for lending.

- Limits: Upper limits on the amount of supply or borrowing, designed to prevent the system from being overly exposed to the risks of volatile assets.

- Interest rate model: This model dynamically adjusts borrowing costs based on capital utilization. High utilization rates drive up interest rates, thereby incentivizing repayments or increasing the supply of funds.

These parameters together construct an adaptive and decentralized risk framework for Aave, whose continuous update mechanism is driven by community governance and can reflect market changes in real time.

Aave Umbrella

Aave's Umbrella system (formerly Safety Module) provides a crucial safeguard mechanism. Users can stake aTokens or GHO to earn rewards, and these staked assets also serve as a backup fund for bad debts in the protocol. In the event of insolvency, the staked assets will be liquidated to cover losses. The corresponding sub-DAO has provided an initial bad debt guarantee of up to $100,000, building an effective insurance layer for the protocol.

liquidation mechanism

The liquidation mechanism is another key pillar ensuring the robust operation of the Aave protocol. Each lending position is monitored in real time by a health factor, calculated as follows:

Health Factor = (Value of Collateralized Assets × Liquidation Threshold) / Loan Value

When the health factor falls below 1, the position becomes liquidable. For example, if you deposit $1,000 worth of ETH as collateral and borrow $800 USDC at the 88% liquidation threshold, your health factor is 1.1. If the price of ETH falls to $900, the health factor will drop to 0.99, triggering the liquidation mechanism.

Liquidators can receive discounted collateral as a reward by repaying up to 50% of a borrower's debt. This mechanism maintains the solvency of the Aave Protocol while also creating market opportunities for arbitrageurs and professional liquidation procedures.

Efficiency mode and isolation mode

The efficiency model maximizes borrowing capacity through highly correlated assets, such as ETH-collateralized derivatives. This model supports capital-efficient operations such as recursive lending, cyclical strategies, and leveraged staking.

The segregated mode effectively reduces the risks associated with new or highly volatile tokens by limiting the types of assets that can be borrowed and setting a risk exposure cap.

These mechanisms embody Aave's core philosophy: continuously improving capital efficiency in areas with manageable risks while always adhering to the principle of prudent expansion.

Aave V4 and Aave App

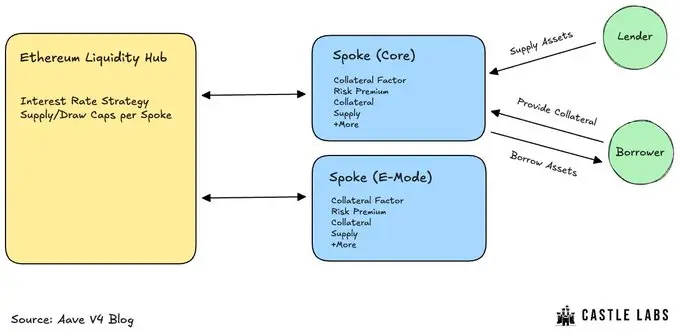

Aave V4, which recently launched its testnet, aims to address the issue of liquidity fragmentation and drive its development into a modular lending infrastructure.

At the heart of V4 is the Liquidity Hub, which aggregates liquidity from the Prime and Core markets. Funds will dynamically flow to where they are needed, rather than being locked in silos, thereby improving efficiency and reducing idle deposits.

Another complementary innovation is Spokes, a specialized marketplace instance integrated with Liquidity Hub. Each Spokes instance can be independently configured with parameters, such as supporting long-tail assets and setting supply and lending limits, while Liquidity Hub ensures that these parameters operate within system rules. Spokes is designed to enable edge innovation while ensuring the security of the core system.

In summary, these upgrades signify Aave's evolution from a single lending protocol into a foundational layer of on-chain capital markets. Through liquidity consolidation and modular design, Aave V4 is laying the groundwork for its continued role as a cornerstone of DeFi lending for years to come.

Another major update to Aave this week is the launch of the Aave App, a product that helps retail investors earn up to 6.5% annualized returns and provides balance protection of up to $1 million.

This is undoubtedly a significant leap forward, as it will help many retail investors access the previously inaccessible DeFi space. The Aave App also provides on-chain and off-chain services, further optimizing the user experience. Its annualized yield is highly competitive, surpassing traditional investment channels such as bonds and bank deposits, offering ordinary users a superior alternative.

Conclusion

Aave is solidifying its leading position as an on-chain bank, with two recent major developments perfectly aligned with its growth roadmap. The latest upgrade, Aave V4 (currently in testnet phase), marks its transition towards greater flexibility and modularity, with the Aave App attracting a "new user base" to the DeFi ecosystem. Furthermore, its RWA marketplace, Horizon, enhances the utilization of tokenized assets, enabling users to easily borrow funds using them as collateral.

As a leader in on-chain lending, Aave has established a dominant market position, becoming one of the preferred platforms for institutions, whales, and ordinary DeFi users to store on-chain stablecoins. Leveraging its scale advantage and robust risk control mechanisms, this leading position is expected to continue for the foreseeable future.

Ultimately, multiple protocols will emerge in the lending sector, some of which have carved out niche markets and continue to cultivate them. As a benchmark in this vertical field, Aave has always relied on its liquidity and scale advantages to build a moat and continuously drive industry innovation.