By William Nuelle

Compiled by: TechFlow

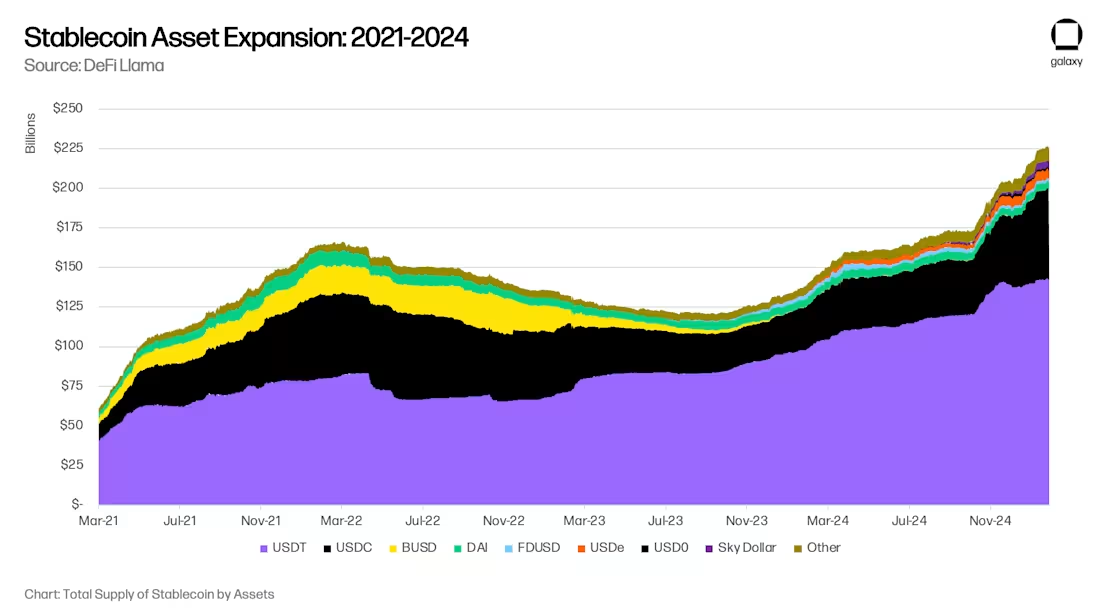

After a sharp 18-month decline in global stablecoin assets, stablecoin adoption is reaccelerating. Galaxy Ventures believes that there are three main long-term drivers for the reacceleration of stablecoins: (i) the adoption of stablecoins as a savings tool; (ii) the adoption of stablecoins as a payment tool; and (iii) DeFi as a source of above-market returns, which absorbs digital dollars. As a result, the supply of stablecoins is currently in a rapid growth phase, reaching $300 billion by the end of 2025 and eventually $1 trillion by 2030.

The growth of stablecoin assets under management to $1 trillion will bring new opportunities to the financial market and also bring new changes. Some changes we can currently predict, such as bank deposits in emerging markets will soon shift to developed markets, and regional banks will shift to global systemically important banks (GSIBs). However, there are some changes that we cannot foresee at present. Stablecoins and DeFi are foundational, not marginal innovations, and they may fundamentally change credit intermediation in new ways in the future.

Three trends driving adoption: savings, payments, and DeFi yields

Three adjacent trends are driving the adoption of stablecoins: using them as a savings vehicle, using them as a payment vehicle, and using them as a source of above-market returns.

Trend 1: Stablecoins as a savings tool

Stablecoins are increasingly being used as savings instruments, especially in emerging markets (EM). In economies such as Argentina, Turkey, and Nigeria, where the national currencies are structurally weak, inflationary pressures and currency depreciation have led to organic demand for the US dollar. Historically, as stated by the International Monetary Fund (IMF), the circulation of the US dollar in many EM markets has been restricted and has been a source of financial stress. Argentina's capital control measures (Cepo Cambiario) have further restricted the circulation of the US dollar.

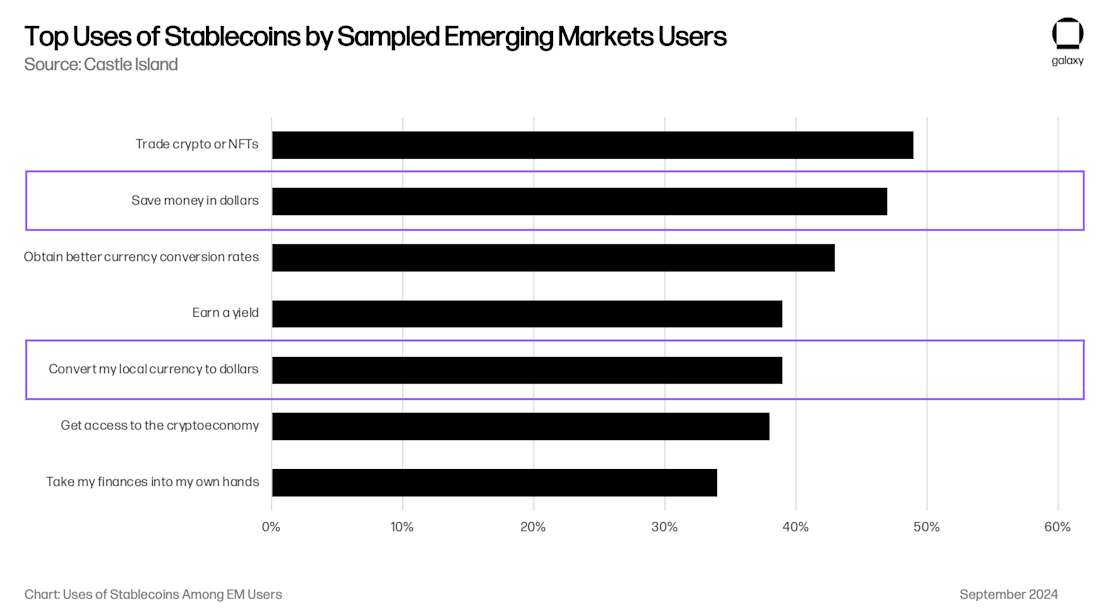

Stablecoins bypass these limitations, allowing individuals and businesses to easily and directly access USD-backed liquidity over the internet. Consumer preference surveys show that access to USD is one of the top reasons for using cryptocurrencies among users in emerging markets. A study conducted by Castle Island Ventures showed that two of the top five use cases were “saving in USD” and “converting my local currency to USD”, with 47% and 39% of users citing this as reasons for using stablecoins, respectively.

While it’s hard to know the scale of stablecoin-based savings in emerging markets, we know the trend is growing rapidly. Stablecoin-settled card businesses like Rain (portfolio company), Reap, RedotPay (portfolio company), GnosisPay, and Exa are tapping into this trend, allowing consumers to spend their savings at local merchants through the Visa and Mastercard networks.

Looking specifically at the Argentine market, fintech/crypto app Lemoncash said in its 2024 Crypto Report that its $125 million in “deposits” accounted for 30% of Argentina’s centralized crypto app market share, second only to Binance’s 34% and beating out Belo, Bitso, and Prex. This figure implies that Argentina’s crypto apps have an asset under management (AUM) of $417 million, but Argentina’s true stablecoin AUM is likely at least 2-3 times the stablecoin balances in non-custodial wallets like MetaMask and Phantom. While these amounts may seem small, $416 million represents 1.1% of Argentina’s M1 money supply, $1 billion represents 2.6%, and growing. Then consider that Argentina is just one of the emerging market economies to which this global phenomenon applies. Emerging market consumer demand for stablecoins is likely to scale horizontally across markets.

Trend 2: Stablecoins as a payment tool

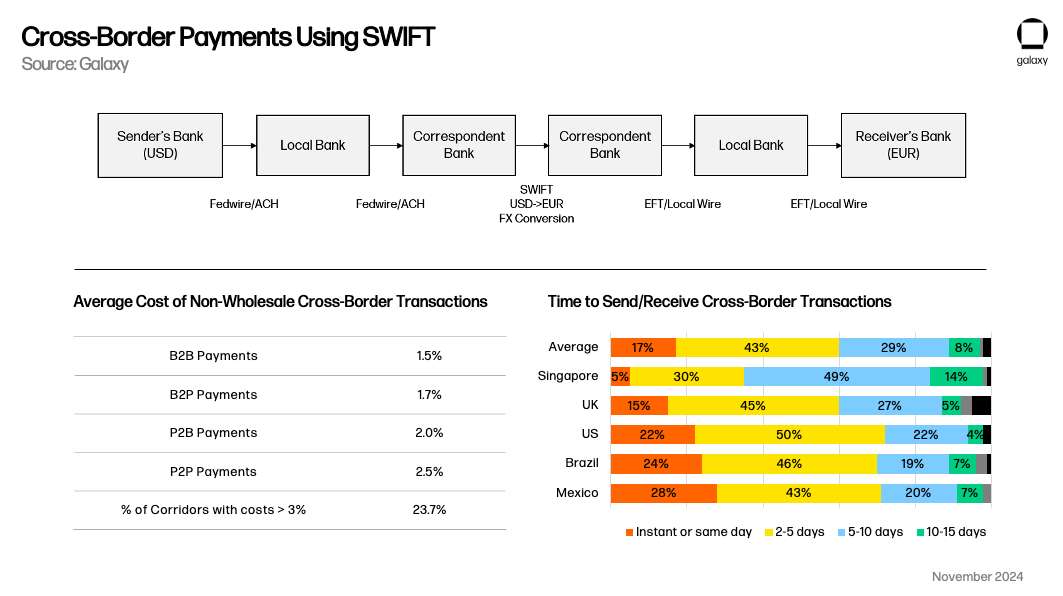

Stablecoins have also emerged as a viable alternative payment method, especially competing with SWIFT for cross-border use cases. Domestic payment systems tend to operate in real time domestically, but stablecoins have a clear value proposition compared to traditional cross-border transactions that take more than 1 business day. As Simon Taylor points out in his article, over time, stablecoins may function more like a meta-platform that connects payment systems.

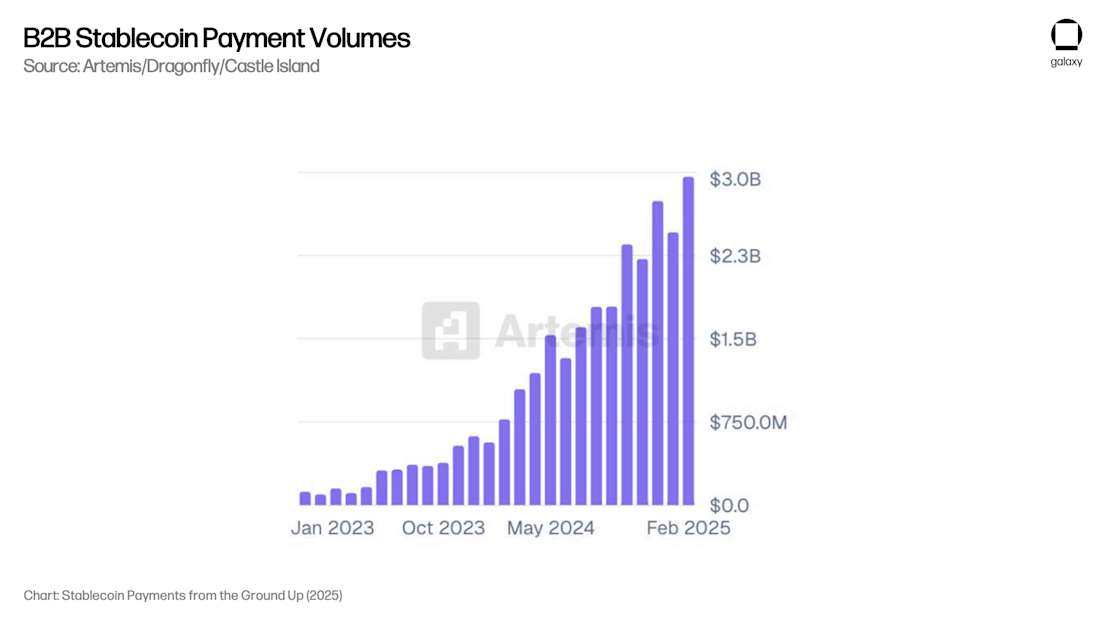

Artemis published a report showing that the B2B payments use case contributes $3 billion in monthly payments volume ($36 billion annualized) across the 31 companies surveyed. Galaxy, through conversations with custodians who handle the majority of these payments, believes that this number is over $100 billion annualized across all non-crypto market participants.

Crucially, Artemis’ report found that B2B payment volume grew 4x year-over-year between February 2024 and February 2025, demonstrating the scale of growth required to sustain AUM growth. There is no research on the velocity of money for stablecoins, so we cannot correlate total payment volume with AUM data, but the growth rate of payment volume suggests that AUM is growing accordingly due to this trend.

Trend 3: DeFi becomes a source of higher returns than the market

Finally, for most of the past five years, DeFi has been generating structurally higher than market dollar-denominated yields, allowing consumers with good technical skills to earn 5% to 10% returns with very low risk. This has and will continue to drive the popularity of stablecoins.

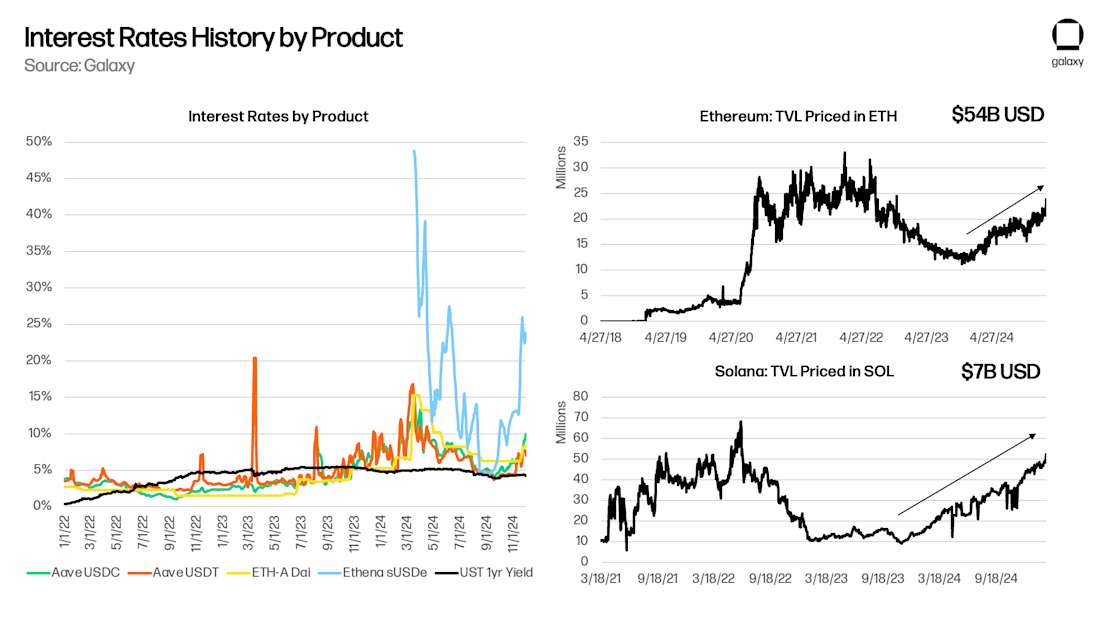

DeFi is a capital ecosystem in its own right, and one of its notable features is that the underlying “risk-free” rates such as Aave and Maker reflect the broader crypto capital markets. In my 2021 paper, “Risk-Free Rates in DeFi,” I showed that the supply rates of Aave, Compound, and Maker are reactive to underlying trades and other leverage demand. As new trades or opportunities emerge—such as yield farming on Yearn or Compound in 2020, underlying trades in 2021, or Ethena in 2024—DeFi’s underlying yields rise as consumers demand secured loans to deploy new projects and uses. As long as blockchain continues to generate new ideas, DeFi’s base yields should strictly exceed US Treasury yields (especially if tokenized money market funds are launched that provide base layer yields).

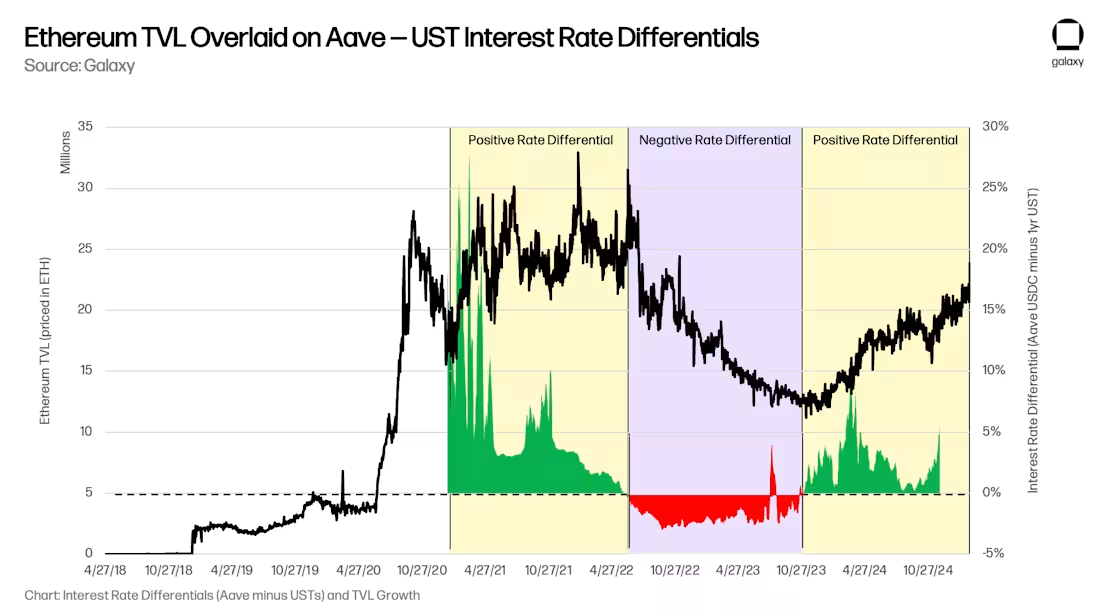

Since the “native language” of DeFi is stablecoins rather than USD, any “arbitrage” that attempts to provide low-cost USD capital to meet the needs of this specific micro-market will have the effect of expanding the stablecoin supply. Narrowing the spread between Aave and US Treasuries requires stablecoins to expand into the DeFi space. As expected, periods of positive spread between Aave and US Treasuries have led to growth in total value locked (TVL), while periods of negative spread have led to declines in TVL (a positive correlation):

Bank deposit issues

Galaxy believes that the long-term adoption of stablecoins for savings, payments and yield is a major trend. The adoption of stablecoins may disintermediate traditional banks because it allows consumers to directly access dollar-denominated savings accounts and cross-border payments without relying on banking infrastructure, thereby reducing the deposit base used by traditional banks to stimulate credit creation and generate net interest margins.

Bank deposit alternative

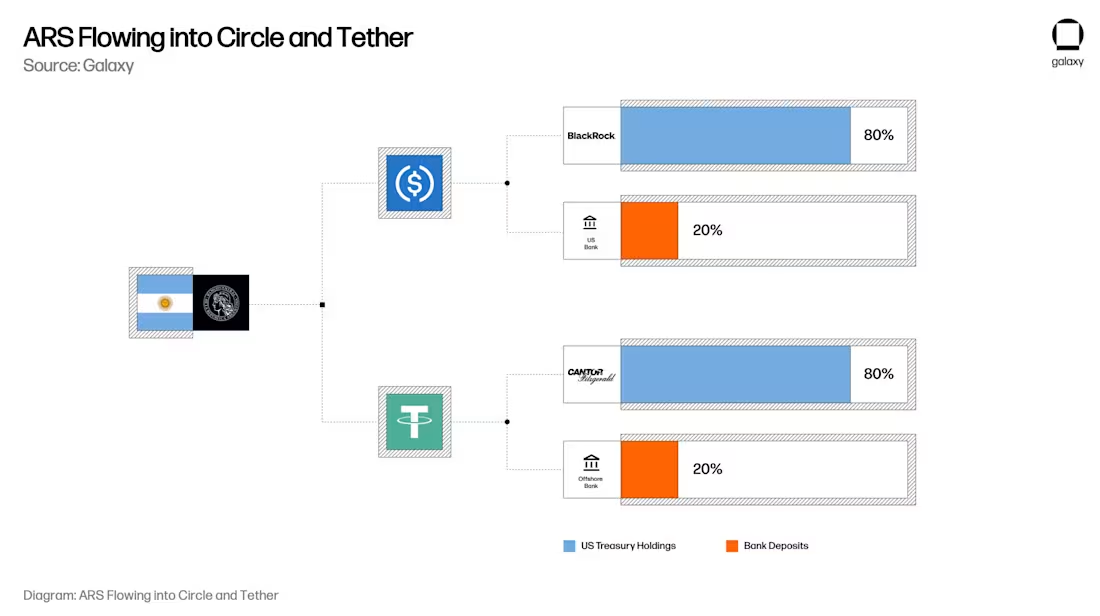

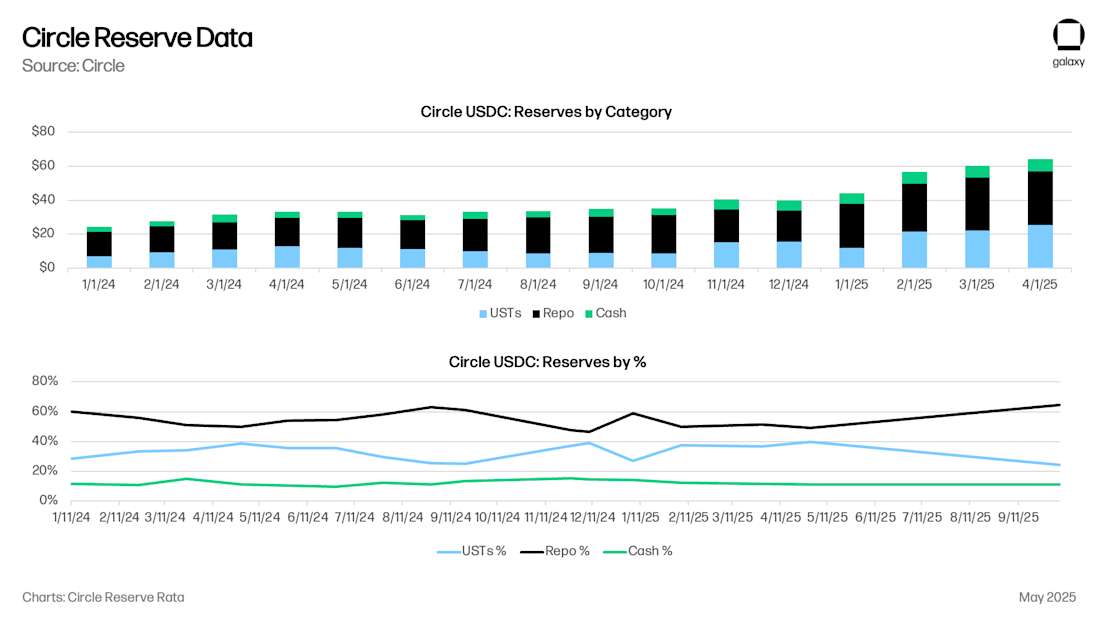

For stablecoins, the historical model is that every $1 is actually equivalent to $0.80 in Treasury bills and $0.20 in deposits in the bank accounts of stablecoin issuers. Currently, Circle has $8 billion in cash ($0.125), $53 billion in ultra-short-term U.S. Treasury bonds (UST) or Treasury repurchase agreements ($0.875), and $61 billion in USDC. (We will discuss repurchases later) Circle's cash deposits are mainly held at Bank of New York Mellon, in addition to New York Community Bank, Cross River Bank and other leading U.S. financial institutions.

Now picture that Argentinian user in your mind. The user has $20,000 worth of Argentinian pesos on deposit at the largest bank in Argentina, the Banco Nacional de Argentinos (BNA). To avoid inflation in the Argentinian peso (ARS), the user decides to add $20,000 of USDC. (The specific mechanics of the ARS disposal are worth considering separately because of the impact it may have on the USD/ARS exchange rate) Now, with USDC, the user’s $20,000 Argentinian pesos at BNA are actually $17,500 in short-term loans or repurchase agreements from the U.S. government, and $2,500 in bank deposits split between BNY Mellon, Bank of New York Mercantile Exchange, and Cross River Bank.

As consumers and businesses move savings from traditional bank accounts into stablecoin accounts like USDC or USDT, they are effectively moving deposits from regional/commercial banks to U.S. Treasuries and deposits at major financial institutions. The implications are far-reaching: while consumers maintain their dollar-denominated purchasing power by holding stablecoins (and through bank card integrations like Rain and RedotPay), the actual bank deposits and Treasuries backing these tokens will become more concentrated rather than dispersed across the traditional banking system, reducing the deposit base available to commercial and regional banks for lending, while making stablecoin issuers important players in the government debt market.

Forced credit crunch

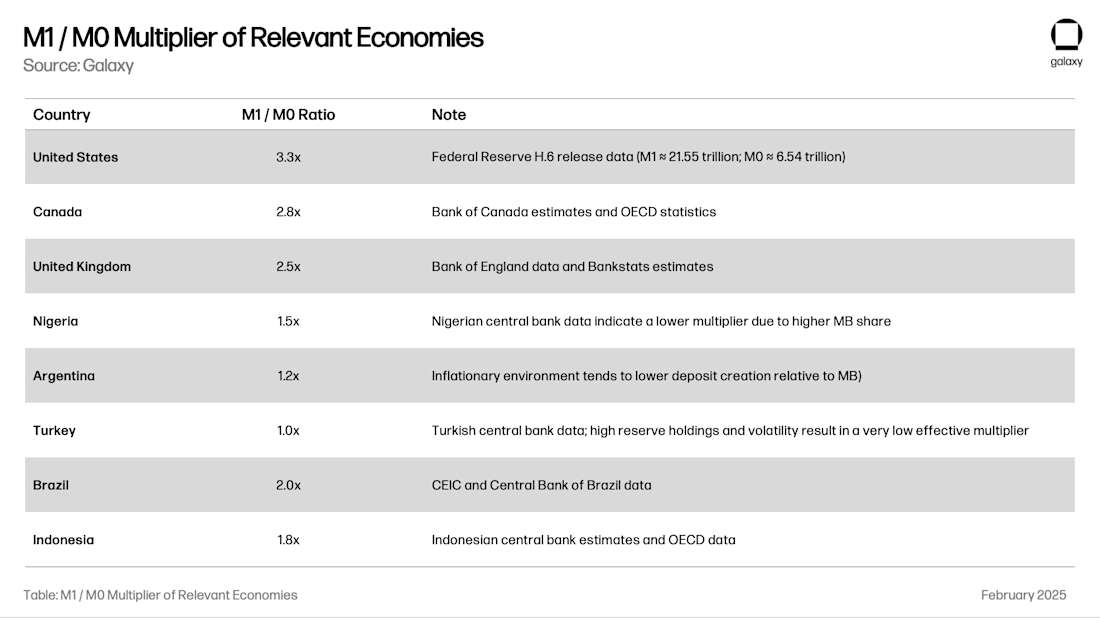

One of the key social functions of bank deposits is lending to the economy. Fractional reserve banking – the practice of banks creating money – allows banks to lend out multiples of their deposit base. The total multiplier for a region depends on factors such as local bank regulation, foreign exchange and reserve volatility, and the quality of local lending opportunities. The M1/M0 ratio (money created by banks divided by central bank reserves and cash) tells us the “money multiplier” of a banking system:

Continuing with the Argentina example, converting $20,000 in deposits to USDC would convert $24,000 in local Argentine credit creation into $17,500 in UST/repo bonds and $8,250 in U.S. credit creation ($2,500 x 3.3 times the product). This effect is imperceptible when M1 supply accounts for 1%, but it may be noticeable when M1 supply accounts for 10%. At some point, regional banking regulators will be forced to consider turning off this tap to avoid undermining credit creation and financial stability.

Overallocation of credit to the U.S. government

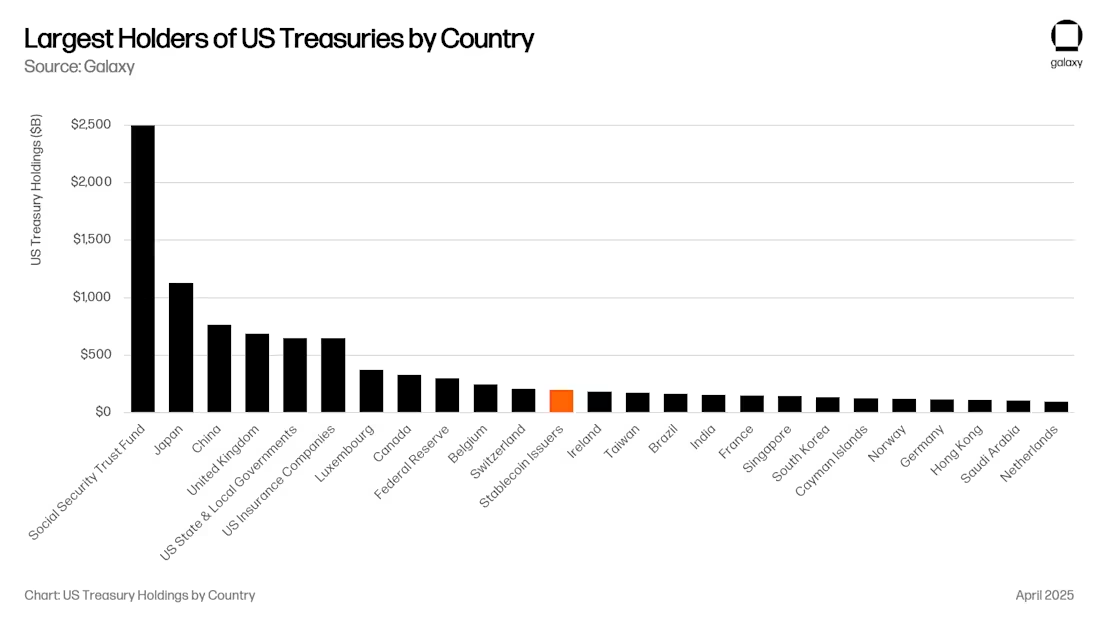

This is undoubtedly good news for the US government. Currently, stablecoin issuers are the twelfth largest buyer of US Treasury bonds, and their asset management scale is growing at the same rate as stablecoin asset management scale. In the near future, stablecoins may become one of the top five buyers of US Treasury bonds (UST).

The new proposal, similar to the Genius Act, would require that all Treasury backing be in the form of either Treasury repurchase agreements or Treasury bills with maturities of less than 90 days. Both of these would significantly increase liquidity in key parts of the U.S. financial system.

When the scale is large enough (e.g. $1 trillion), this could have a significant impact on the yield curve, as US Treasuries under 90 days would have a large, price-insensitive buyer, distorting the interest rate curve that the US government relies on for funding. That being said, Treasury repo (Repo) does not actually increase demand for short-term US Treasuries; it simply provides an available pool of liquidity for secured overnight borrowing. Liquidity in the repo market is primarily borrowed by major US banks, hedge funds, pension funds, and asset managers. For example, Circle actually uses most of its reserves for overnight loans collateralized by US Treasuries. The size of this market is $4 trillion, so even if the stablecoin reserves allocated to repo are $500 billion, stablecoins are a significant player. All this liquidity flowing to US Treasuries and US bank borrowing benefits US capital markets while global markets suffer.

One hypothesis is that as stablecoins grow in value to over $1 trillion, issuers will be forced to replicate bank loan portfolios, including a mix of commercial credit and mortgage-backed securities, to avoid over-reliance on any one financial product. Given that the GENIUS Act provides a path for banks to issue “tokenized deposits,” this outcome may be inevitable.

New asset management channels

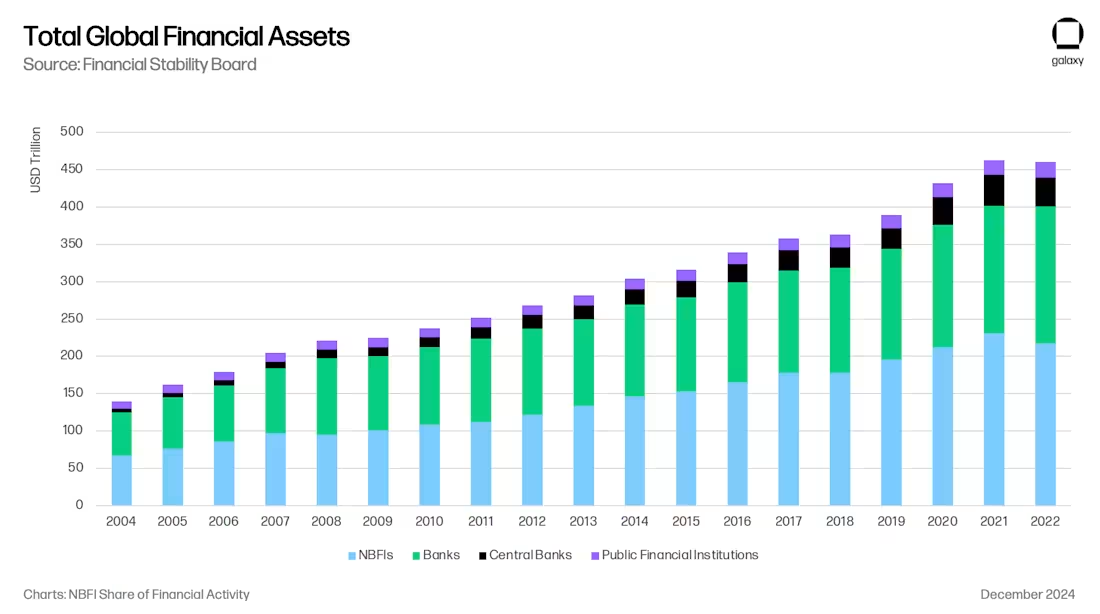

This all creates an exciting new asset management channel. In many ways, this trend mirrors the ongoing shift from bank lending to lending to non-bank financial institutions (NBFIs) in the wake of Basel III, which limited the scope and leverage of bank lending in the wake of the financial crisis.

Stablecoins siphon money from the banking system and, indeed, from specific sectors of the banking system (e.g., emerging market banks and developed market regional banks). As Galaxy’s Crypto Lending Report notes, we have already seen the rise of Tether as a non-bank lender (beyond U.S. Treasuries), and other stablecoin issuers may become equally important lenders over time. If stablecoin issuers decide to outsource credit investments to specialized firms, they will immediately become LPs of large funds and open up new asset allocation channels (e.g., insurance companies). Large asset managers such as Blackstone, Apollo, KKR, and BlackRock have achieved scale expansion in the context of a transition from bank lending to lending to non-bank financial institutions.

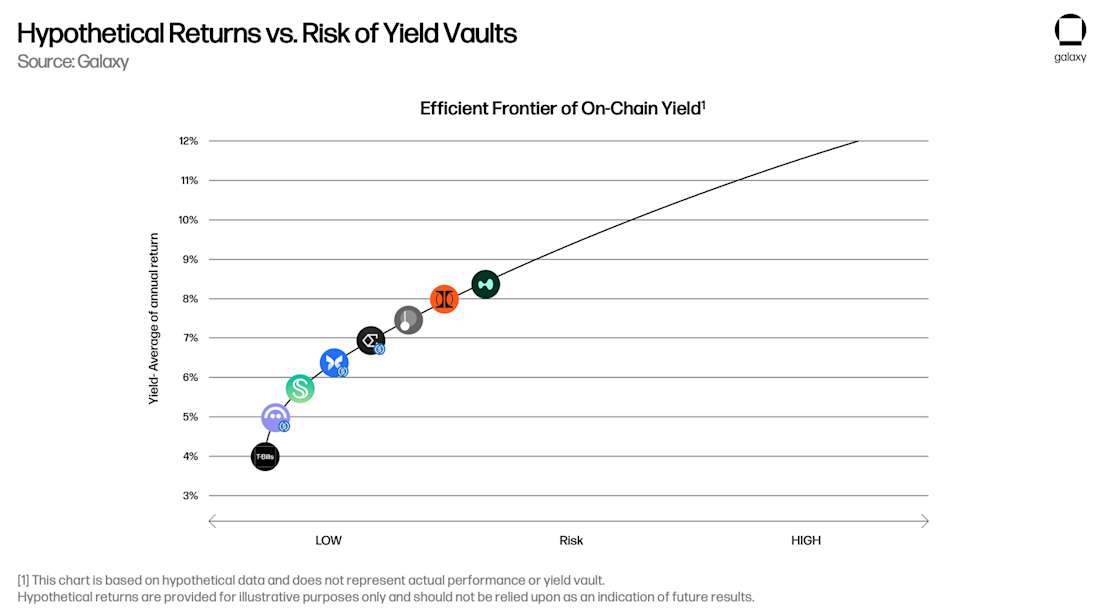

The Efficient Frontier of On-Chain Yields

Finally, it’s not just the underlying bank deposits that can be borrowed. Each stablecoin is both a claim on the underlying dollar and an on-chain unit of value itself. USDC can be borrowed on-chain, and consumers will need yields denominated in USDC, such as Aave-USDC, Morpho-USDC, Ethena USDe, Maker’s sUSDS, Superform’s superUSDC, and so on.

Vaults will open up another avenue for asset management by providing consumers with on-chain yield opportunities at attractive yields. We believe that in 2024, portfolio company Ethena will open the “Overton Window” for on-chain yields denominated in USD by connecting basis trading to USDDe. New vaults will emerge in the future, tracking different on-chain and off-chain investment strategies, which will compete for USDC/T holdings in applications such as MetaMask, Phantom, RedotPay, DolarApp, DeBlock, etc. Subsequently, we will create an “effective frontier of on-chain yields (Deep Tide Note: Help investors find the best balance between risk and return)”, and it is not difficult to imagine that some of these on-chain vaults will be dedicated to providing credit to regions such as Argentina and Turkey, where banks are at risk of losing this ability on a large scale:

in conclusion

The convergence of stablecoins, DeFi, and traditional finance represents not only a technological revolution, but also a restructuring of global credit intermediation, which reflects and accelerates the shift from bank to non-bank lending after 2008. By 2030, stablecoin assets under management will approach $1 trillion, thanks to its use as a savings tool in emerging markets, efficient cross-border payment channels, and above-market DeFi yields. Stablecoins will systematically drain deposits from traditional banks and concentrate assets in U.S. Treasuries and major U.S. financial institutions.

This shift presents both opportunities and risks: stablecoin issuers will become important players in government debt markets and potentially new credit intermediaries, while regional banks, especially in emerging markets, face a credit crunch as deposits migrate to stablecoin accounts. The end result is a new model for asset management and banking, in which stablecoins will serve as a bridge to the frontier of efficient digital dollar investments. Just as shadow banking filled the gap left by regulated banks after the financial crisis, stablecoins and DeFi protocols are positioning themselves as the dominant credit intermediaries in the digital age, with profound implications for monetary policy, financial stability, and the future architecture of global finance.