作者:Frank,PANews

一直以来,不少公链都喜欢将自己的竞争对手标记为Solana,但似乎没有谁能够真正对Solana产生威胁。不过,最近Solana的联创Toly似乎很愿意和Base联创进行辩论。与此同时,近一段时间来,Base生态在各个方面的数据迎来爆发式增长,不仅多项指标在L2行列中处于领先地位,TVL、资金流入量等数据更是超过了Solana。

似乎,Base才是Solana心中最大的潜在对手?PANews对Base近期数据进行复盘,并和Solana进行了一番对比,看看Base的崛起是兵临城下还是又一次“狼来了”?

两位联创唇枪舌战不断

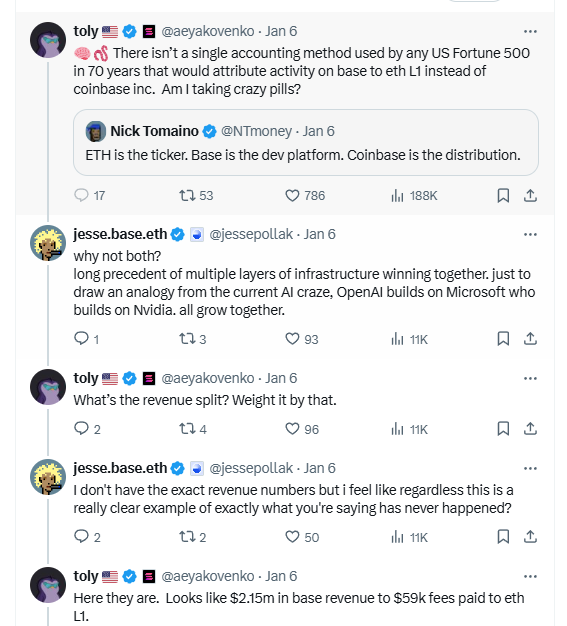

1月6日,Solana联合创始人Toly在社交媒体上评论,认为Base的发展并没有给以太坊生态带来真正的增长,而是Coinbase正通过Base吸走了以太坊的生态。对此言论,Base创始人Jesse在社交媒体上予以回击,他表示Base和以太坊并不是一种零和竞争的关系,Base和其他L2一样,都在以太坊整体的路线之内发展,随着Base的发展,以太坊也在发展壮大。

Toly随后则比喻道,正如谷歌和微软的竞争,都为Linux作出了贡献,但在价值捕获上,这是分开的。因此,没有任何一家美国500强公司使用单一的会计计算方法将Base的活动归因于以太坊,而是都计入到Coinbase公司。而Base产生的215万美元的收入,也仅支付给以太坊主网5.9万美元。

看似Toly在为ETH没有从Base捕获价值打抱不平,实际上,这场争论的背后可能无关于Base和以太坊的竞争,而是关于Solana与Base的竞争。虽然市面上有很多Solana的竞争对手,比如将Sui、Aptos或者Hyperliquid都定位自己为Solana的竞争者。但从Solana团队的表态来看,他们眼中最大的竞争者或许就是Base。

早在12月份,Pudgy Penguins宣布在Solana上发行代币,并在上线后给Solana网络创造力单日6690万笔交易的历史新高。在这个过程中,Jesse也曾公开喊话,称:“我和Base社区会张开双臂欢迎Pudgy Penguin及其代币PENGU”,这一举动也被社区认为是公开的向Solana抢生意。

除此之外,两者还在多个议论当中有来有往,比如Yuga Labs联合创始人Garga.eth吐槽以太坊生态,遭到Jesse的不满,而Toly则在下边评论添油加醋:“将ETH桥接至Solana,我绝对不反对ETH成为Solana上最好的货币”。此前,Jesse也多次发表过Base与Solana对比的言论。

BaseTVL和资金流入反超Solana

两人唇枪舌战的背后,是Base与Solana在数据上的暗流涌动。PANews将Base与Solana近一年来的几个数据指标进行了对比,能够看出,Base目前的整体数据仍不及Solana,但Base的增长速率正全面领先Solana,如果按照这个速率发展下去,Base将有可能在1~2年内从数据上超越Solana。

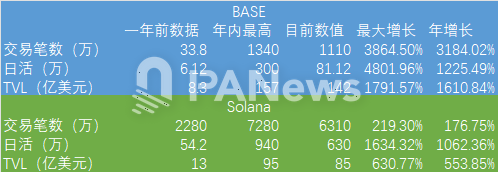

PANews选用了公链对比上几个常用的指标,如日活地址数、交易笔数、TVL等。数据选择一年前的数据到2025年1月10日的数据变化。

首先来看,Base的变化,一年前,Base的日交易笔数约为33.8万笔、日活地址数约为6.12万个,TVL量约为8.3亿美元。这几个数据在当时分别相当于Solana的1.48%、11.29%、63.85%。

截至2025年1月10日,Base的数据变化为日交易笔数约为1110万笔、日活地址数约为81.12万个,TVL量约为142亿美元。而目前这三个数据与Solana的比值为:17.59%、12.88%、167.06%。

Base这三项指标的年度增长分别为3184.02%、1225.49%、1610.84%。而同期的Solana这三项指标的增长率分别是176.75%、1062.36%、553.85%。

能够看出来,通过一年的发展,Base的交易笔数和日活数据相比Solana仍有较大的差距。而TVL方面,Base已经完成了反超。有趣的是,Jesse等主要团队成员为了庆祝这一数据,在1月9日直播剃了光头。

而在其他数据的增长率来看,Base的增长势头也比Solana更加激进。如果双方保持目前的增长效率,一年以后Base可能在交易笔数方面也会超过Solana。

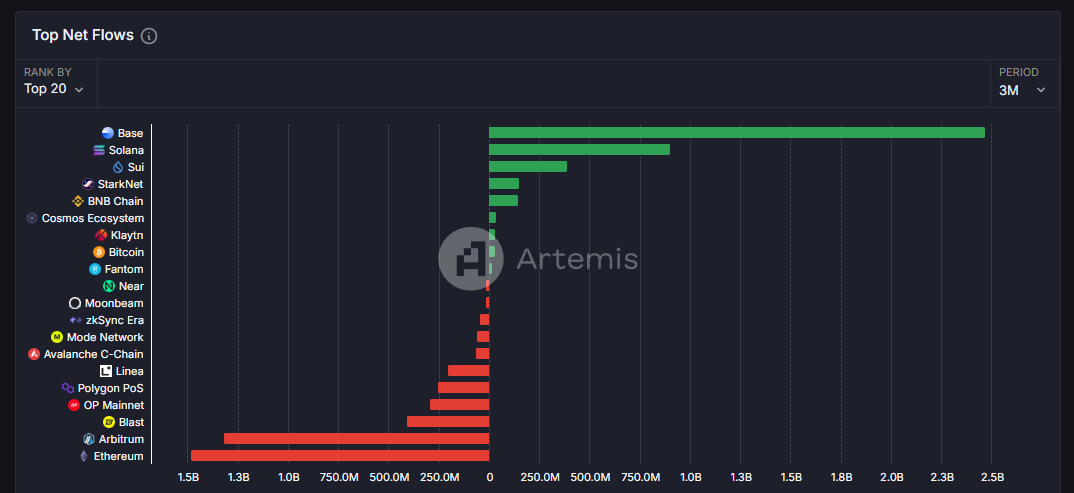

除了这些数据之外,更重要的一个指标也在悄然发生变化。过去的一年当中大多数时间内,Solana都是公链流入资金量最多的网络。而最近三个月的数据显示,Base以净流入25亿美元的资金量成为净流入最高的公链,Solana则以净流入9亿美元的资金量屈居第二。

而这个数据的主要变化可能就在近期发生,近一年的净流入总额约为38亿美元,相当于近三个月(25亿)的净流入占到了全年65%。

从大选到Virtuals,Base靠AI正步步逼近

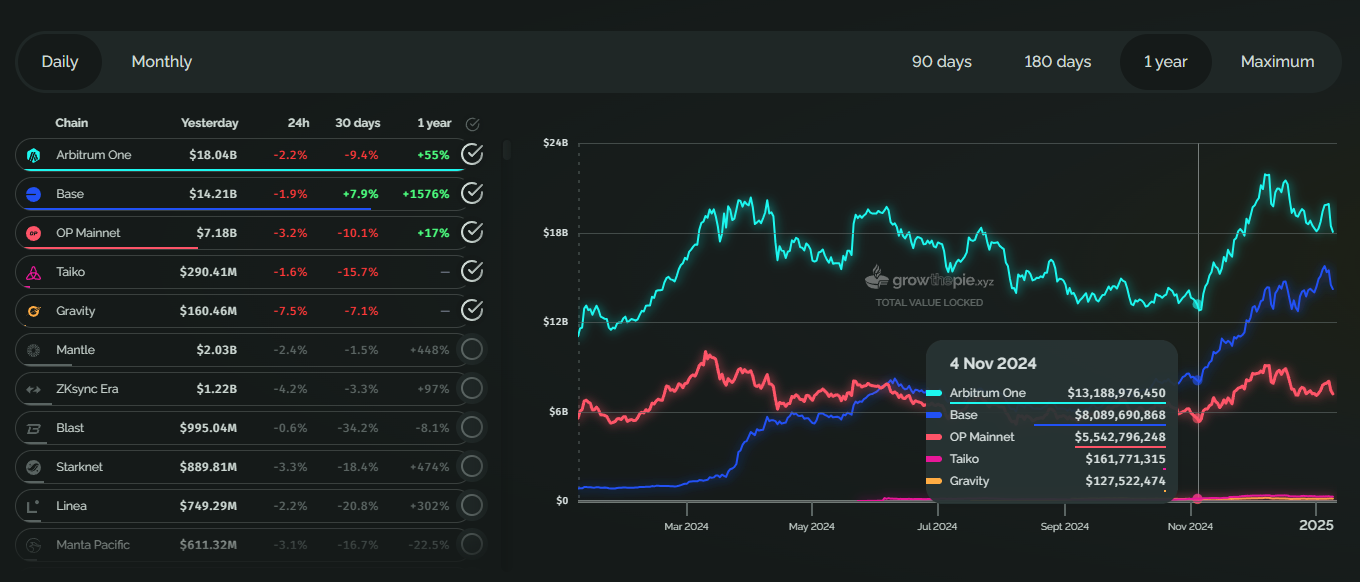

从细节的变化上来看,也确实如此。Base的TVL量似乎从11月3日开始迎来了大幅增长。不过这也不是Base的个例,Arbitrum在同期也迎来了一波高速发展。

这波增长的背后原因可能主要来自于美国大选后,特朗普当选带来的整体市场增长。而在近一个月来,Base引发关注的主要原因则是在长期与Solana竞争的MEME赛道,终于出现了一个与之可以匹敌的产品Virtuals Protocol。

各个网络纷纷推出Pump.fun仿盘后,基本都悄无声息。Virtuals Protocol却终于抓住了AI Agent的风口,成为当前最炙手可热的AI Agent一键发布平台。诞生了aixbt、G.A.M.E等多个市值超过亿的AI Agent代币。

从Dexscreener的数据来看,1月11日Solana上的DEX交易量为68.8亿美元,24小时新诞生的交易池为5324个,Base的交易量为21.2亿美元,24小时新上线的交易对为2673个。两者在MEME领域的差距正一步步缩小,Base似乎成为唯一一个能够在MEME方面接近Solana热度的公链网络。

不过,此前Sui上也有过短暂的爆发期,不过在热度下降之后,仍不可避免的再次陷入沉寂。Base相对的优势在于其资金的沉淀效果远强于Sui,因此只要TVL量没有断崖式下滑,或许这种热度仍能得到保持。

通过对比数据,能够发现Base正成为Solana最强的竞争对手,但问题在于Base始终缺少自己的治理代币,也就很难被市场定价,没有公链代币也让Virtuals protocol获得了base公链上更多的资金溢出效应。或许为了解决这一问题,1月4日消息,Base 开发人员Jesse Pollak发推表示,Coinbase正在考虑向其Base网络的美国用户提供代币化的COIN股票。

如果这目标能够实现,或许最大的意义并不是RWA的领域又多了一个重要资产,而是Base发展所带来的价值终于可以更直接的反映到Coinbase的股价上,而只能参与加密货币交易的投资者来说,也算变相能够参与到Base的治理和享受红利。以Base目前的数据表现来看,转换为代币的市值应该在百亿美元级别以上。1月11日,Coinbase的市值约为647亿美元,这一市值放到加密货币当中,排在BNB和SOL之后。不知一旦加成上Base的链上资金流入,Coinbase的市值是否能完成对BNB和SOL的反超。