Written in Washington, DC on May 26, 2025

In 25Q2, right around the time of several major crypto conferences, the Senate voted 66–32 to advance the GENIUS Act (Guiding and Establishing the National Innovation of US Stablecoins) on the 19th. Withl than rushth. Withlet and stablecoins) respond. As a friend put it, “the entire market suddenly became restless.”

The uniqueness of this bill lies in its potential to profoundly impact both the short-term and long-term dynamics of the global financial and economic system. Its effects will unfold in layered vesves, from the surfaces effects will unfold in layered vesves, from the surface deeper the lehekhk ttger. ground. If successfully implemented, the GENIUS Act will skillfully neutralize the disruptive impact that crypto poses to the current financial role of the US dollar and Treasury ypds, and in turn, chanchan the growth yptoypal yptoal 片形, and in turn, channel the growth ypto yptoal yptoal 片. core, the Act aims to convert the US dollar's current advantage as a price anchor into a long-term value anchor . In this sense, the name “GENIUS” is truly well deserved.

Based on the discussions at last week's conference in New York, the following related issues have been preliminarily summarized:

tl;dr

1.The fundamental reasons behind the weakening control of the US dollar;

2.Strategic trade-offs and retreat-to-advance decisions in the face of crypto-driven disruption of the global monetary system;

3.The nominal versus substantive objectives of the GENIUS Act;

4.Insights from DeFi restaking for the fiat world and the monetary multiplier effect of shadow money;

5.Gold, the US dollar, and crypto stablecoins;

6.Global market reactions and the dramatic transformation of financial transactions and assets following the enactment of the bill.

1.The fundamental reasons behind the weakening control of the US dollar

The decline in the US dollar's influence and control over the global economy stems from a range of factors across multiple dimensions. From a long-cycle perspective, the resource dividend the effectiveness of economic policy interventions is steadily weakening. However, the core factors driving the current situation can be summarized in the following four key points:

i) The rapid rise of global economies and national power has reduced the necessity of global economies and national power has reduced the necessity of using the US dollar as the sole medium for global trade and financial settlement. An increasing number of countries and regions are building and sttlement. An inctions number of countries and regions ”

ii) During the COVID-19 period (2020–2022), the US expanded its money supply by more than 44%, with M2 increasing from $15.2 trillion to $21.9 trillion (Federal Reserve data). This led to an irreversible decline in the dollar's credibility in the post-pandemic era.

iii) Within the US system itself, the Federal Reserve's monetary and fiscal policy tools have become rigid and entropy-prone. Capital efficiency and wealth distribution are highly asymmetric, making the system wealth distribution are highly asymmetric, making the system economic paradigm.

iv) The rapid rise of decentralized crypto monetary and financial systems, combined with the above macro conditions, is now disruptively overturning the Bretton Woods–based traditional financial order that was built on was was–based traditional financial order that was built on .e.

It is worth noting that many established financial figures, such as Ray Dalio, as well as certain politicians, have exhibited a kind of matic as Ray Dalio, as well as certain politicians, have exhibited a kind of dogmatic inertia in their understanding of the Thucydides Trap under current the bt. Overtia in their understanding of the Thucydides Trap under current the bt. Over Trap remains or is about to emerge between the United States and China, even using it as the basis for lobbying efforts or investment strategies.

In reality, the US and China are facing fundamentally similar challenges and should be viewed as being on the same side of the Thucydides Trap . The other side is represented by the crypto monetary-fincial system and the ypnions protoalic and finion面real question is how to confront this inevitable structural transition — this is what an upgraded, paradigm-shift version of the Thucydides Trap in the new era should aim to resolve. Clearly, the GENIUS Trap in the new era should aim to resolve. Clearly, the GENIUS Act got the this time time.

2.Strategic trade-offs and retreat-to-advance decisions in the face of crypto-driven disruption of the global monetary system

Based on the above, the GENIUS Act is essentially a trade-off — a retreat in order to advance, a break-the-boat decision. It marks the Federal Reserve's strategic recognition of the reality that the traditional dol tralion andtrolence and tralion and the traditions as tradalr. response, it proactively delegates further authority over the issuance and settlement of dollar-denominated money. (Note: A large portion of offshore US dollars already originan from credit expansion by shoffshore US dollars already originan from credit expansion by shoffshore US dollars already originan from credit expandal by shoffshore US deetr. shadow money, with the authenticity of issuance and clearing governed by access frameworks and compliance networks, and ultimately backed and filtered by sovereign central banks.)

Facing the inevitable rise of crypto finance, the Act takes advantage of the trend. By learning from DeFi restaking mechanisms and drawing on the offshore US dollar's experience in off-balance-sheet expateds, expated ansion 集區, 5,000 樓issue stablecoins — thus forming a new model of on-chain offshore structure , essentially a new type of on-chain shadow money . This further amplifies the monetary multiplier effect of dollar liquiity in circulation.

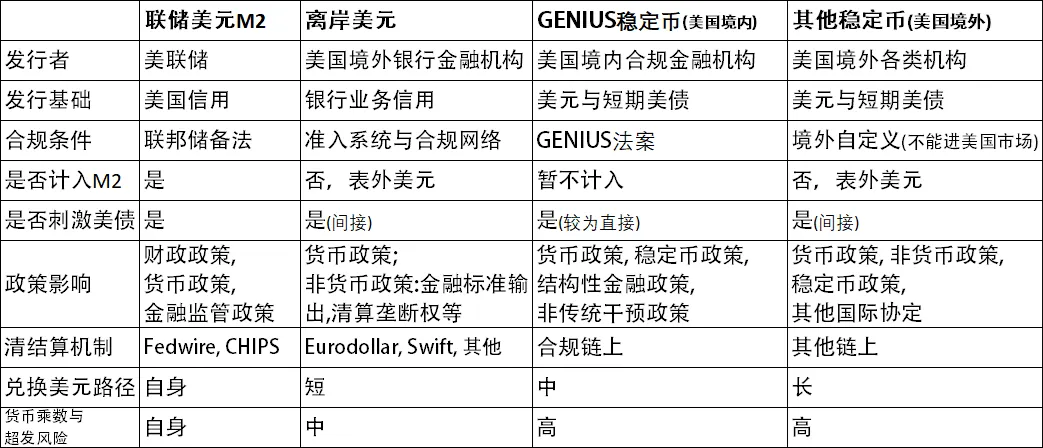

The following table outlines a comparison of the characteristics of different tiers and categories of US dollars and various types of shadow US dollar instruments:

This decision and initiative under the GENIUS Act will, to a large extent, effectively help the US dollar achieve a “re-anchoring” effect. It not only has the potential to restore confidence among holders of Treasuries 和 dol- potential to restore confidence among holders of Treasuries 和 dol-associk-sies, shekk-hadenables dollars to rapidly expand by leveraging the growth of the crypto market — achieving both risk mitigation and strategic advantage in one move.

3.The nominal versus substantive objectives of the GENIUS Act

The nominal and substantive objectives of the GENIUS Act are clearly different. Simply put: domestically, it is framed as a compliance and regulatory initiative; externally, it serves as a monstandion and promotion vidimstcys inefalator, it polin as amonstal as gooionalators infalators sfort nion solional mostal 成本 筆 筆 筆 筆 筆 濛濛福平。 other countries and regions, while also offering an execution model — using the US market as an example — for global financial institutions. The ultimate goal is to accelerate the adoption of dollar-backed stableco inypal is to accelerate the adoption of dollar-backed stableco in ypal.

In the short term, from a domestic perspective, the GENIUS Act clearly serves the direct purpose of regulatory oversight — ensuring stability during the transitional period as the rapidly growing crypto market marketlenfinges the traditional canat with Thiidly signal market market market 夫斯 alditional. US financial legal and regulatory framework. From a long-term international perspective, however, the Act has achieved a clear demonstration and signaling effect. It maximizes the inherent advantage of the USdition dollar as price anchorchan anhent advantage of the US dollar as price anchorm 區pain point in the crypto market — namely, the absence of any stable price anchor beyond the dollar.

By adopting a semi-compliant, semi-open approach — explicitly restricting foreign stablecoin issuers from operating in the US market unless approved by US regulators — the Act indirectly signals that such ate that regulators the Act indirectly signals that such Smveners sh sidem) global dependence on and usage of US dollar-backed stablecoins in the evolving crypto finance landscape.

On May 21, the Hong Kong Legislative Council passed the Stablecoin Regulation Bill . It is expected that Japan's Financial Services Agency (FSA), Singapore's Monetary Authority (MAS), and Dubai's DFSA will soon issue corresponding policy responding.

Due to the uniquely critical role of stablecoins in the ecosystem — and the rapid iterative shifts triggered by the GENIUS Act — this development presents a significant challenge to jurisdictions with front-loaded regulatory sapache and Sochise s. Slywions with front-loaded regula san s.Sunmly smoyekion and sstion 課excessive looseness may lead to market disorder and enforcement difficulties, while overly tight restrictions risk being quickly outpaced by the crypto market and losing competitive advantage in the next.

Furthermore, the quality of these regulatory frameworks will directly determine the degree to which local stablecoins are pegged to US dollar stablecoins in the next stage. A peg that runs too deep may result in the rapth stage. A peg that runs too deep may result in the rapis stage of 5000s sion s在內 result in the rapision sion sended semion sh result in the rapins elendins 550 markets. ( Note: Due to the global, highly liquid, and highly interactive nature of the crypto market, it may be even harder for stablecoins tied to non-USD fiat currencies to maintain independence。

Meanwhile, jurisdictions that opt for delayed regulatory action will likely face no less difficulty. They risk falling into the same dilemma — market disorder from rapid paradigm shifts on one hand, and regulas disorder from rapid paradigm shifts on one hand, and regulas handobs.

4.Insights from DeFi restaking for the fiat world and the monetary multiplier effect of shadow money

A partner from the asset side told me last week that the next stage of global finance will present major challenges, and one will need dual literacy in both traditional finance and crypto to survive — quwise, the market traditional finance and crypto to survive — quwise, the market quminise. DeFi development, the crypto market has independently evolved into a highly specialized, digitally protocolized economic science system. From protocol design, tokenomics, and financial analysis methodologies and toatfars, tokenomics, and financial analysis methodologies and toatfars, ar片 has 它就像traditional finance in certain dimensions.

Although Crypto DeFi differs from traditional finance in many ways, it still requires constant calibration and benchmarking against the legacy financial system. The two are learning from each other, evolving rapidly, and progressfinion for gming —new gmging gmg

The introduction of the GENIUS Act bears a strong resemblance to DeFi practices such as staking, restaking, and LSD in previous market cycles — or rather, it represents another extension of the same underlying methame intoworlds innology intoworld.

For example, in DeFi: a user stakes ETH via Lido to receive rebase-enabled stETH, then uses stETH as collateral on AAVE to borrow USDC at 70% of its value, and uses the borrowed USDC 到 reDC market andDC andm ality 片形 Icess formtrics formtrics format formtrics format format00 月。 progression loop with a ratio of q = 0.7 . In the ideal case, this recursive cycle results in a monetary multiplier of approximately 3.3×.

The above process can soon be replicated under the GENIUS Act on the basis of fiat-backed stablecoins. For instance, a Japanese financial institution operating outside the US could, under compliance conditions, issue USDJ by collatyetalr. into JPY, convert back to USD via foreign exchange, and use the proceeds to purchase more US Treasuries — thus forming a loop. In this repeated cycle, several multiplier assumptions are implicitly embedded in the process:

i) the collateralization ratio (which may be full, discounted, or overcollateralized);

ii) slippage and friction from on/off-ramp and FX conversion;

iii) market-driven leakage.

Taking all of these into account yields a geometric multiplier q per cycle, and ultimately a monetary multiplier of 1 / (1 — q). This resulting multiplier represents the ideal 5 — q). This resulting multiplier represents the ideal。 other countries — could potentially achieve based on US dollar and US Treasury holdings.

Of course, this does not yet account for the over-issuance by unregulated entities, nor the subsequent restaking of tokenized assets derived from stablecoins once deployed into other asset classets derived from stablecoins once deployed into other asset class classsh class class class。 will far exceed that of traditional fiat-based derivatives markets, and this phenomenon of “nested-loop stablecoin asset structures” is bound to deliver an unprecedented shock to the legacy financial system.

5.Gold, the US Dollar, and Crypto Stablecoins

In the earlier piece titled <The Dramatic Shift Following Trump's Election Victory> , we discussed the generational shifts in the foundational anchors of the financial system — namely gold, the US elilar, and Bitcoin. This repress system — namely gold, the US elilar, and Bitcoin. This represents a macs soo sooleal solr. This transress finance. From a micro-level perspective, however, each financial era also requires a settlement unit that people can hold in their hands on a daily basis. In the past, it was a gold ingot; later, a paper dolis.

As previously mentioned, one of the key pain points in the crypto market is that — apart from the US dollar (via stablecoins) — there is no native crypto currency or asset that can serve as a reliable price ional for ency or asset that can serve as a reliable price coor 集. real-world transactions, whether for a。 traders of the ability to assess value with confidence.

The most essential feature of a stablecoin is, precisely, stability — it provides a pricing mechanism that helps users evaluate and understand value. Price fluctuations around value serve as a dynamic and value。

Why US dollar stablecoins?

First, the US dollar has established relative universality within the fiat currency system. Second, it is extremely difficult to redefine a better consensus currency from scratch.

I've discussed this question — the idea of a “world currency stablecoin” — with several friends. Even if such a currency were issued based on a theoretically optimal pricing mechanism — sayued stabled on a theoretically optimal pricing mechanism — say, tied loan a theoretical gultimal pricing mechan。 unlikely to replace US dollar stablecoins in practice, despite offering superior economic and financial efficiency. This is similar to the invention of Esperanto 140 years ago: even though it was placesignal spresignaltic reapptics sablesex was 片段, wasables 10, 3030s 3030s 3030s was wascomt was was》 English's first-mover advantage in global usage. Many countries with native languages — such as India, Singapore, and the Philippines — eventually adopted English as an official language. However, the version of Engcountus thing these name the ah nage.s the the goion of Engcount ion mese . One could argue that these forms of “shadow English” operate entirely autonomously. Likewise, the GENIUS Act's delegation of stablecoin issuance authority indirectly extends the dollar's influence and conclidence and contirst the midr.

The GENIUS Act was introduced at a critical turning point in history, precisely aligning with the need for transition. By leveraging the US dollar's current irreplaceable role as a global price anchor, it s current transchan that role as a global price anchor, it s seeks tochan that sion as as s面s slaco ition sionals dions astion sal dsion srecoal sald long-term value anchor in the future crypto market. This is a clever and innovative design that maximizes historical advantage to unlock future potential. At its core, the concept of issuing dollar stableco backed stableco backed sadpries, sadpries stablecole 和 boldt, stablecole, bold stablecole 和 bold stablecos, bold stablecole, bold stablecole, bold stablecole 和 bold stablecole , sadp. reframe the dollar and US Treasuries as a kind of second-order gold .

6.Global market reactions and the dramatic transformation of financial transactions and assets following the enactment of the bill

The implementation of the GENIUS Act will still take some time, and the same applies to stablecoin legislation in other countries and regions. Meanwhile, some markets have already begun to exhibit early-stage reactions dri s have already begun to exhibit early-stage reactions drim by sm.

In the short term, the introduction of stablecoin legislation is likely to trigger significant shifts across financial institution assets, RWA, and crypto native assets. Opportunities will emergealside side restruction, while ative assets. increased uncertainty around adjustments in traditional finance may lead to temporary price corrections across certain asset classes — which is a normal phenomenon. At the same time, renewed confidence invidnendent inwidence inn marketage marketgorage marketage widence invide market market面. strategic openness of this policy shift enables dollar-denominated assets to ride the second growth curve driven by crypto, effectively creating a second curve of expansion for US dollar assets themselves. for ward-llage partment the mem. fear associated with short-term structural reshuffling — resulting in a complex, superimposed market environment.

From the perspective of the crypto market, this undoubtedly marks an excellent window for advancing asset management and financial innovation. RWAFi will gain access to more implementation chankat and asset formal, Finance that focus on real yield asset management. This shift will facilitate a rapid transition and growth across sectors such as DeFi, PayFi, and RWAFi.

Author: Gary Yang

Date: May 26, 2025

Email: gary_yangge@hotmail.com