By now for most following the recent apace movements of the

DeFi sector within the blockchain industry, the amount of bitcoin value

utilized within these DeFi applications, via their respective layer 1

protocols, has skyrocketed well past our expectations. Ethereum, which has been

designated as the default protocol for DeFi, has seen the bulk of this trend

propagated onto its ecosystem. At the time of this writing, there is over

38,000 BTC being used on Ethereum, which now represents 1% of the total ETH marketcap.

Of course, this amount of BTC is only a measly 0.181% of the total amount of

bitcoins available, but if we see the recent trend persist going forward, it’ll

be interesting to see the effects this could have on the Bitcoin network

itself.

And Ethereum isn’t the only layer 1 protocol that is

allowing for these innovative bitcoin-backed tokens…

The most popular option for these bitcoin-backed tokens has

been WBTC (Wrapped Bitcoin), which was developed and launched by BitGo in early

2019. To give you a sense of the rapid popularity of these tokens, mostly due

to the DeFi frenzy, there were only 3,911 WBTC on June 1 compared to a current

amount, as of this writing, of over 26,000 WBTC. That equates to a 570%

increase in a span of 2 months.

There are now a concoction of different bitcoin-backed

tokens sprucing up onto the other formidable layer 1 protocols as well. For

example, the smart contract protocol, Tezos, has announced their own native

bitcoin-backed token, tzBTC, which is currently under development and testing.

Polkadot, with the engineering support of Interlay, also announced their

development and testing plans for PolkaBTC. Below is a timeline encapsulating

all the bitcoin-backed tokens that are either launched or recently announced on

the major layer 1 protocols with Ethereum carrying the bulk of it.

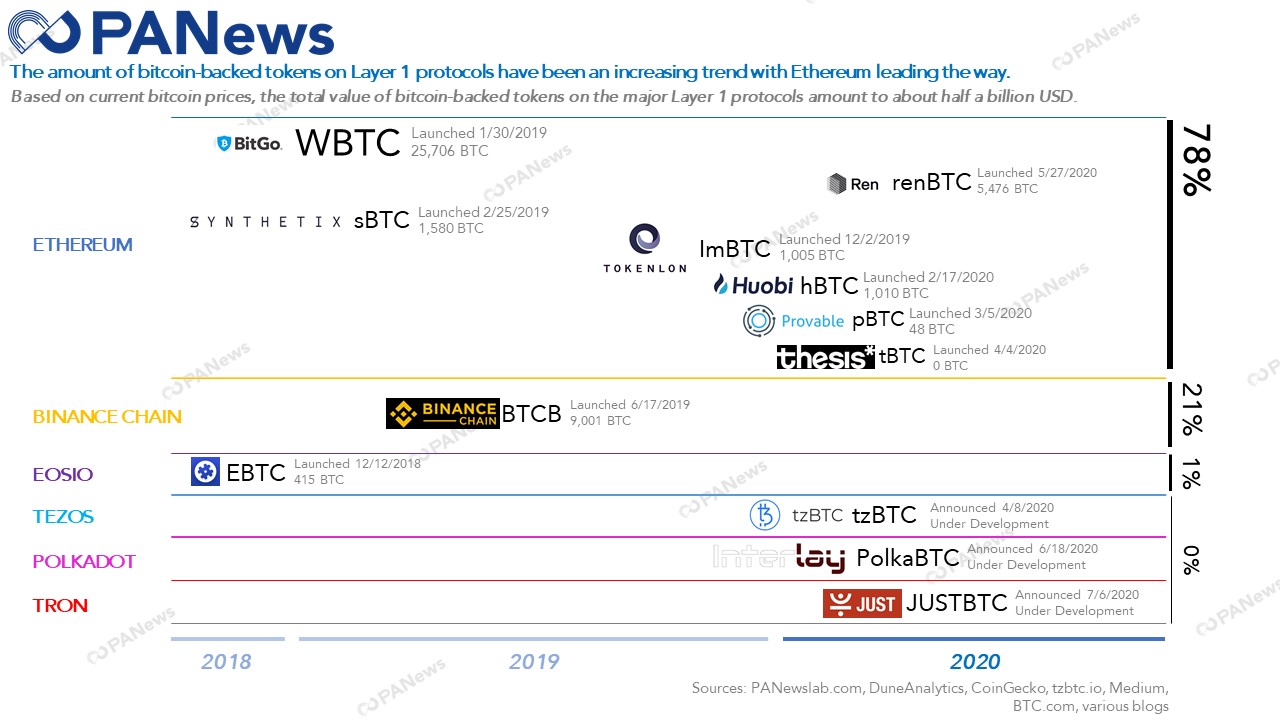

(Figure 1) A timeline of

all the bitcoin-backed tokens on the major layer 1 protocols, including their

current amount of locked bitcoins and the team behind it.

In retrospective, the advent of these bitcoin-backed tokens is just genius. It allows bitcoin maximalists to use the application ecosystem of other layer 1 protocols, albeit being able to HODL their bitcoins. A WIN-WIN you could say. The way how most of the bitcoin-backed tokens work is simple. Holders of bitcoin just simply deposit their BTC in another controlled wallet address while simultaneously the token standard on whatever protocol mints a 1 for 1 bitcoin backed token. There are different nuances to this process but for the most part, they all essentially encapsulate the swapping of your bitcoins for a bitcoin-backed token that is compatible with the layer 1 protocol standard.

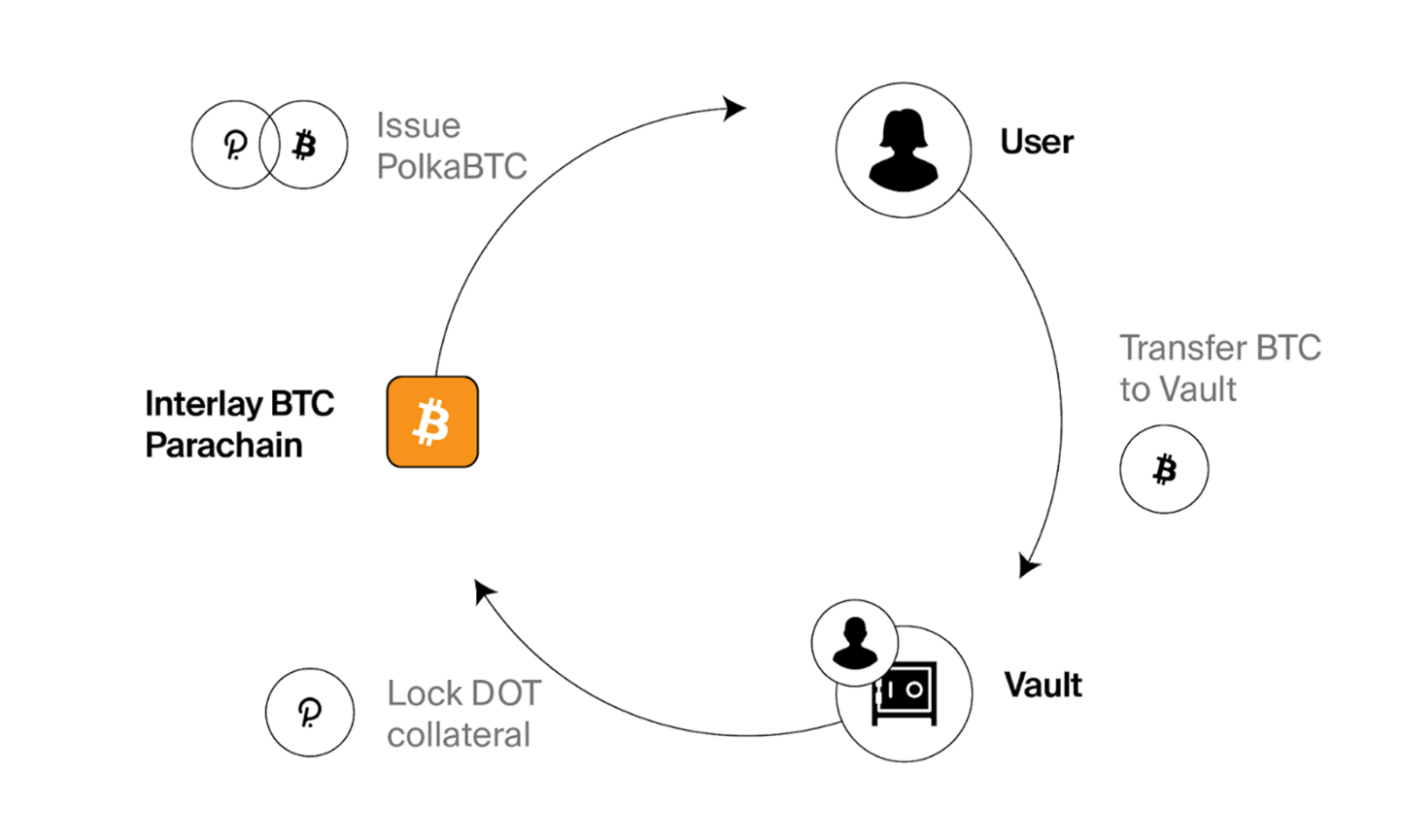

Let’s take the recently announced PolkaBTC by Polkadot and Interlay for example. A user transfers BTC to a vault of their choosing which then sends locked DOT collateral to an Interlay BTC Parachain. That will then send the user PolkaBTC. The redeem BTC process is just a mirror reflection.

(Figure 2) An overview of

the issuance process for users to “swap” BTC for bitcoin-backed tokens on the

Polkadot network.

In a way, bitcoin-backed tokens represent an accelerated way

of interoperability between blockchains. It’s a streamline way of opening up

the gateway for more use cases between protocols rather than being stuck in a

silo effect. And with bitcoin being perhaps the most popular crypto, this

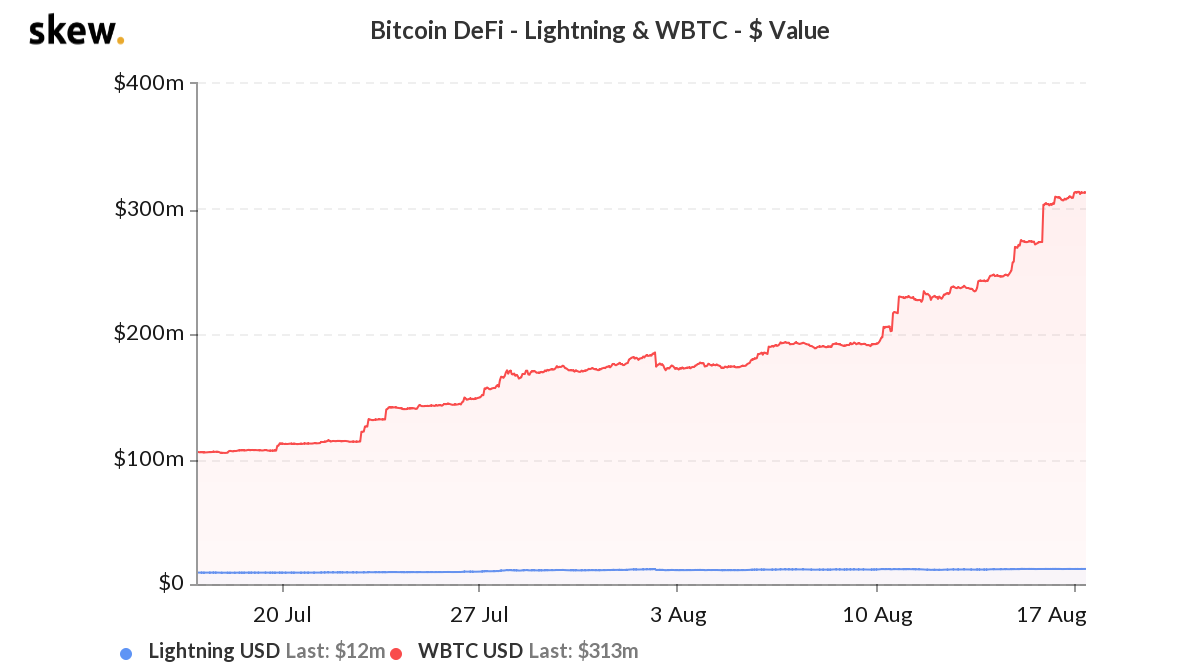

reinforces its use cases outside of just holding bitcoin. In fact, Ethereum

projects including WBTC and imBTC hold 70% more bitcoins than Lightning or

Liquid. Lightning and Liquid also strive to galvanize the leading

cryptocurrency’s utility, similar to the goals of tokenized bitcoin projects.

But these protocols have a niche focus of improving the speed and privacy of

small and large off-chain bitcoin transactions.

(Figure 3) The fortuitous

growth of WBTC outpacing the bitcoin Lightning network over the past few

months. The amount of value on the Lightning network has basically been flat

compared to the exponential growth of bitcoin in WBTC.

But as innocent as this new use case has been for the

blockchain and crypto community, there are implications to this that

inadvertently could be divisive rather than innocuous. And it is never too

early to postulate on what that might be.

Below are some points that are worth to think about.

·

Bitcoin being emblematic of real estate.

People just wanting to hold bitcoin and use it on DeFi – I think one could

state that the belief in Bitcoin is still prevalent as the asset of choice to

have. As the mantra has been pervasively propagated to just HODL, as have our

bitcoin holders have done. Just HODL. Because although Ethereum has been

getting more of the attention in the past year due, bitcoin is still king in

crypto. It’s been the first and most battle tested blockchain project to date.

And don’t forget, it’s been the reason why all of us are here reading this

today. Without Bitcoin, there will probably be either no blockchain industry or

maybe even some other superior form of it might have spurred up. But who knows?

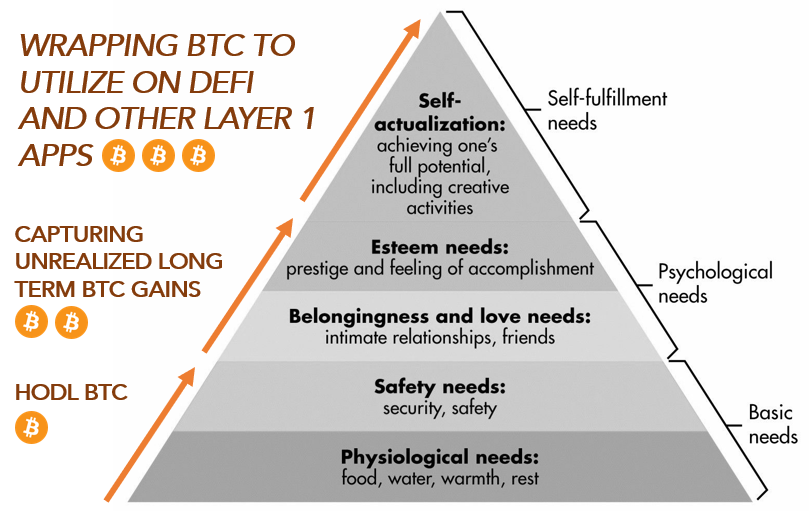

It is worth nothing that our propensity of wanting to hold bitcoin and be used

in other forms can be synonymously compared with real estate. We all want to

own real estate in its essential nature of providing us a shelter but it’s also

leveraged as an investment vehicle by taking out home equity loans (allowing us

to be equipped with short term liquidity), investment real estate (renting it

out to the market), house flipping, or even in niche cases where owning a home

in a certain district will grant your children to attend a prestigious grade

school. Owning a home satisfies our most basic of Maslow’s hierarchy of needs,

but what we do with that home allows us to realize our self-fulfillment needs.

(Figure 4) A fundamental

look at Satoshi’s hierarchy of needs.

Owning bitcoin also satisfies our most basic of needs (security and safety of our wealth), but being able to cross chain the asset onto other smart contract protocols for our yield farming orgasm satisfies our psychological and self-fulfillment needs. This all may be a bit exaggerated for the time being but the similarities are evident. As ubiquitous as real estate is, bitcoin can have the same roadmap.

· Out with the old and in with the new. Eventually some of these users might just want to give up BTC and use ETH. Maybe a gradual realization to the increased utility of Ethereum might persuade some wrapped bitcoin users to just give up their BTC for ETH out of simplicity. They are already spending most of the time and usage on the Ethereum network anyways. This is a more of a far-fetched scenario. Persuading one that bitcoin is no longer the “it” crypto will take decades, probably centuries.

· Some

of these bridges or centralized wrapped tokens becoming security threats. As

useful and innovative one may think this is, there are security concerns to

this. For example, Wrapped Bitcoin is realistically just holding the locked

bitcoins of users in a centralized third-party custodian. So as secure and

trustless bitcoin may be when you hold your own keys, the step of giving your

bitcoins to a custodian for WBTC represents an unconscious centralized security

threat while you farm those yams on Ethereum. The renBTC design uses smart

contracts to lock Bitcoin, as opposed to trusted third-parties used by WBTC. In

an actual case of these bitcoin-backed token models going awry, the folks at

Thesis, which is the team behind tBTC had to stop their platform from taking in

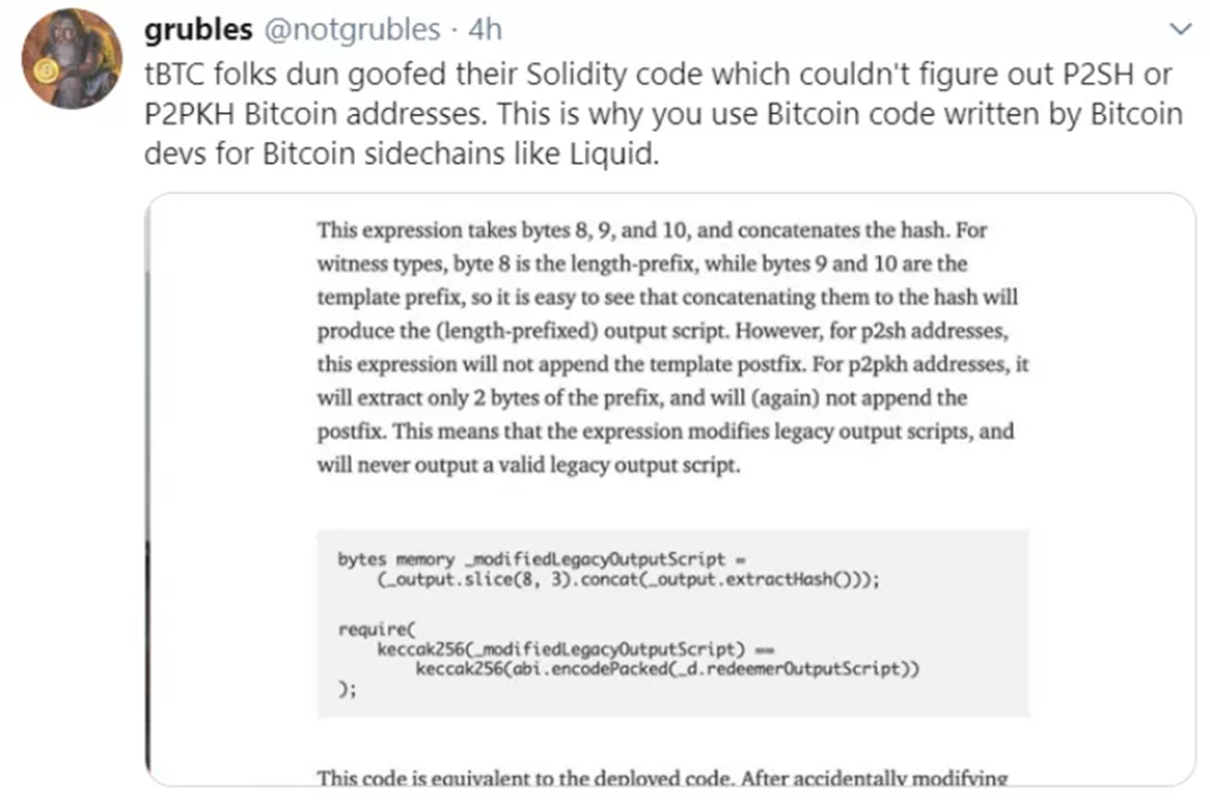

deposits after only a month from its launch date due to a bug in their code.

Community contributors started noticing issues when tBTC’s Solidity code wasn’t

able to differentiate between P2SH and P2PKH bitcoin addresses.

(Figure 5) A prime

example of the technical risks of “wrapping bitcoin” that occurred with tBTC.

· Arbitrage trading between different bitcoin-backed tokens or even between Bitcoin itself. One could even envisage a scenario where new financial arbitrage occurs between bitcoin backed tokens and bitcoin itself leading to Bitcoin community members pitted against each other for extra margin. This could lead to a creation of more complex financial derivatives or trading pairs such as BTC/WBTC, BTC/renBTC, BTC/tzBTC, BTC/PolkaBTC, etc. As of this writing, EBTC (EOS BTC) is trading at $13,075 compared to bitcoin’s current price of $11,907. But this would not be something new as BTC arbitraging between different exchanges already exists.

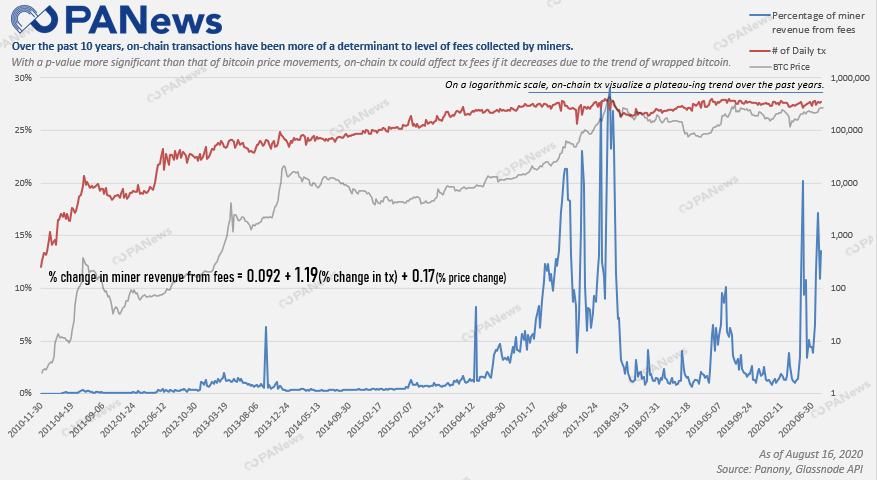

· A substantial decrease in Bitcoin’s on-chain activity. What if activity dies down on the Bitcoin network, forcing bitcoin miners to take matters into their own hands? Banning transfers to those bitcoin addressees from those bitcoin-backed token projects? If a large significant amount of all bitcoins just eventually freeze for the sake of being wrapped up in other blockchain networks, what happens to the on-chain activity of Bitcoin? Decreased on-chain activity could to a decreased amount of tx fees to miners. It would be close to nothing to have a transaction validated on the Bitcoin network eventually. Dormant bitcoins isn’t something new as the network has seen this become more prevalent. Earlier this year, a report by Digital Asset Data shows that more than 10 million BTC have not moved for a whole year which represents about 60% of all bitcoins. This also could lead to the conversation of are on-chain tx a determinant of price or is price a determinant of on-chain transaction. Fellow Messari community analyst George Adams puts it best stating:

“I believe there's reflexivity between the two (positive feedback loop). For example- in Bitcoin, more on-chain volume = more demand for BTC, which increases price. And then a higher BTC price means more interest from people, which means more on-chain volume. So I think they feed each other.... although I don't have confidence in a first mover”

This question of who the first mover is as difficult as answering the age-old question of if the chicken or the egg came first. But based on what we know about finance and fundamental investing, the FUNDAMENTALS should be a driver of price (theoretically). Where in the case of Bitcoin, on-chain transactions should be the driver to its price. Many general crypto valuation frameworks would give a rebuttal on this stating that velocity is not necessarily always a driver of network value. But as all of them do agree on is that there are remedies to prevent a token suffering from the token velocity issue, and in bitcoin’s case, it’s the store of value factor. So then if take this thinking, then a decrease in on-chain tx should be a determinant of price and have a substantial impact on transaction fees paid to miners. So as a result, this could lead to the controversial hypothetical death spiral theory. For now, it’s statistically shown that on-chain tx has a significant correlation to that of the transaction fees collected by miners. And as we progress to the year of 2140, transaction fees will be the sole source of income for miners.

(Figure 6) After running

a multiple regression on % change in on-chain tx and % change in price with %

change of miner revenue from fees acting as the dependent variable (with 10

years of daily data), the p-value for % change in on-chain tx is way below the

threshold rendering this as being more significant.

(Figure 7) With on-chain

tx being statistically more determinant on % change in miner revenue from fees

with a 1.19 coefficient, it’s also interesting to note that on a logarithmic

scale, on-chain tx have been flat-lining for the past few years.

But let’s back this thinking up a bit. The relationship

between on-chain tx and price, regardless if it is liner or non-linear,

shouldn’t be too much taken for face value. As the real determinant should be

positioned as, if bitcoin price markets are rational vs irrational, or another

way of putting it: efficient vs inefficient.

This is all digressing a bit put I think you can see the implications of the initial innocuous effect of reducing on-chain transaction that could lead to a scenario where sustained low on-chain transaction start to effect network security.

CONCLUSION

The whole notion of being able to use your bitcoins on other

blockchain protocols is unanimously supported. We are not trying to give

warnings but rather highlight some of the caveats that could emerge down the

line. A significant reduction in Bitcoin’s on-chain network activity could

straddle the line between network security and usage. Perhaps prompting miners

to proactively pull out or take a more drastic approach. But we also see this

trend giving way to concomitants of how we use bitcoin. As pointed out earlier,

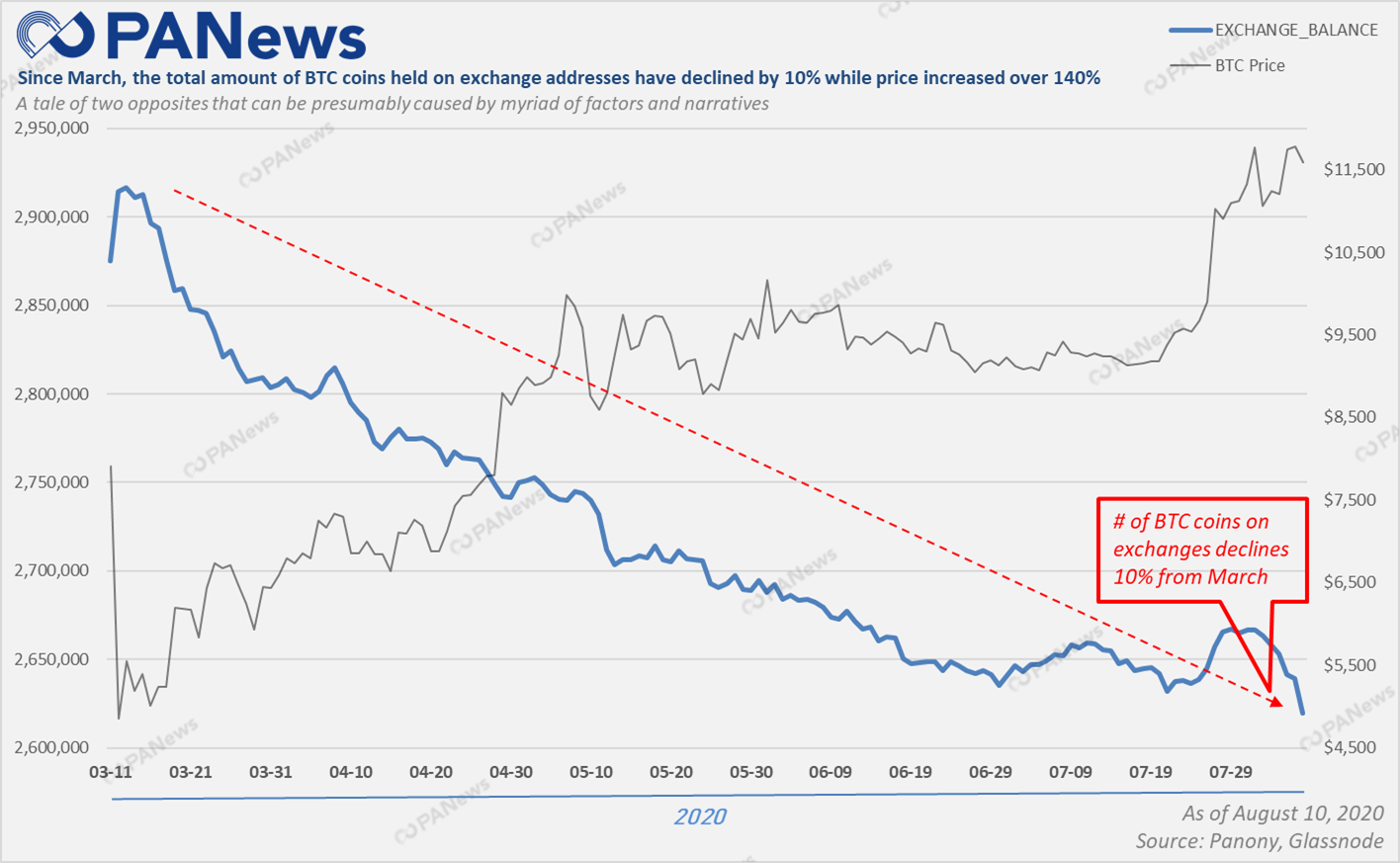

we already see a trend in the amount of bitcoins traded on exchanges slowly

pull out in this chart below.

(Figure 8) Through data

pulled from Glassnode’s API, there has been a opposite trend of bitcoin’s price

moving up while the number of BTC coins on exchanges taking a reverse dive down

10%.

Better yet this could be the point of when we crossover the

chasm towards mass adoption. The numbers speak for itself as the TVL in DeFi

smart contracts on Ethereum has just whiffed past the $6 billion mark as of the

time of this writing. And bitcoin-backed tokens is one of the reasons for that.

SOURCES

-

https://news.bitcoin.com/close-to-11-million-btc-havent-moved-in-over-a-year/

- https://www.coindesk.com/polkadot-is-latest-blockchain-to-explore-redeemable-bitcoin-tokens

- https://www.coindesk.com/ethereum-has-become-bitcoins-top-off-chain-destination

- https://www.youtube.com/watch?v=gJq9FcYZe0k&t=3680s

- https://explorer.binance.org/asset/BTCB-1DE

- Justin Sun’s Twitter