Author: a16z New Media

Compiled by: Deep Tide TechFlow

Deep Dive: a16z's latest weekly chart report uses extensive data to dissect a core argument: the tech industry's dominance over the global economy continues to accelerate. The top ten companies by market capitalization already exceed the combined GDP of the G7 (excluding the US), and AI may reshape organizational structures once again, much like the railroads spurred the development of modern corporations. Furthermore, stablecoins are shifting from transfer tools to real-world payment scenarios, and trust among young Americans in traditional media has plummeted to historic lows.

Software has devoured the world

We certainly have our own biases, but the importance of technology to the global economy is indeed hard to overestimate.

You could even say that software has truly eaten the world:

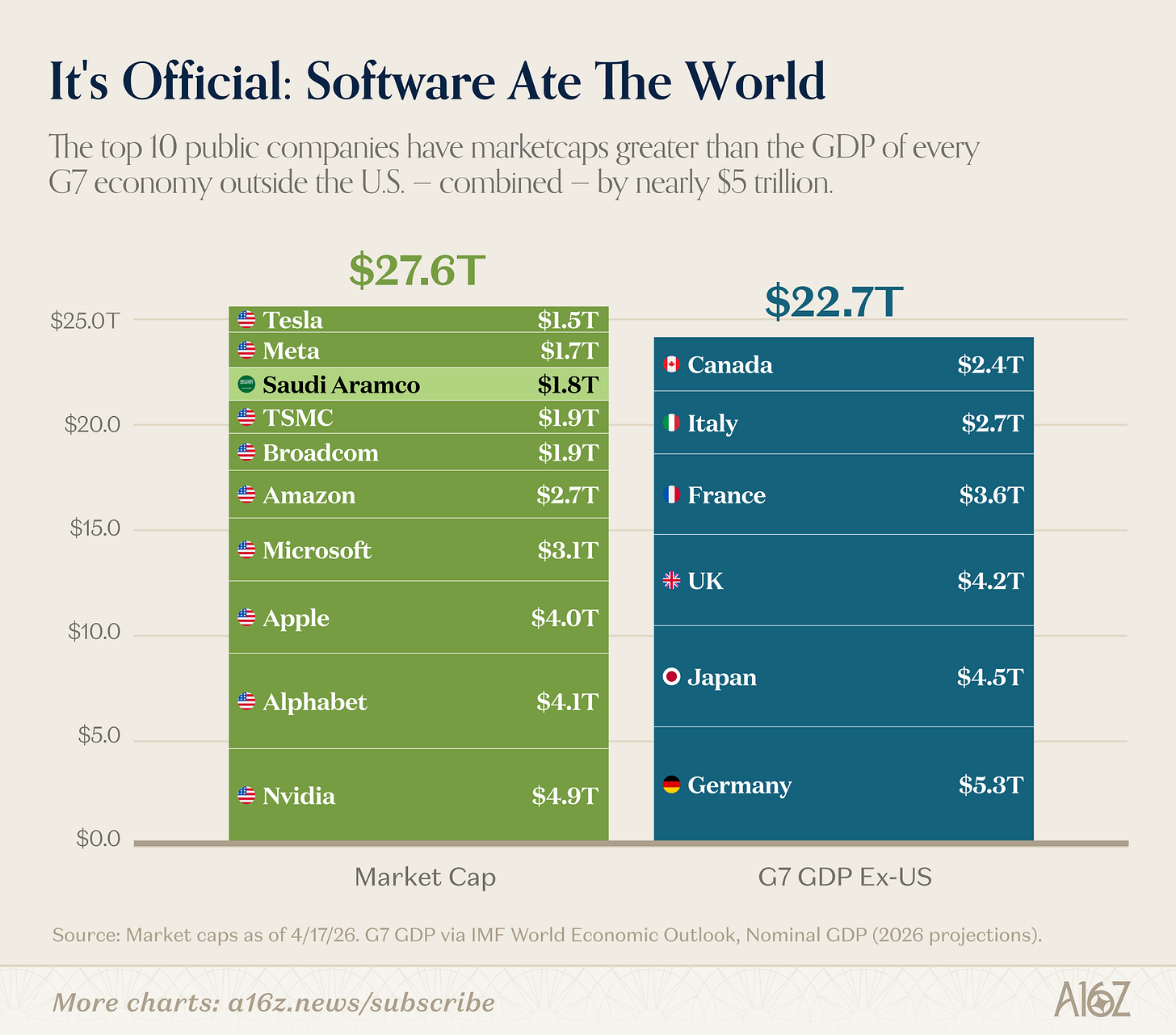

Caption: Top 10 Global Companies by Market Capitalization vs. GDP of G7 Countries (excluding the US)

The combined market capitalization of the world's top ten listed companies is larger than the combined GDP of all the G7 countries (excluding the United States). Even excluding Saudi Aramco, which no one would classify as a "tech company," the conclusion remains the same. (However, Saudi Aramco was indeed founded in San Francisco!) [^1]

To be fair, the top ten are more like "technology + semiconductors (plus Tesla and Apple, which are harder to categorize)" than pure software companies. But the conclusion remains the same: technology is not just a big business, it is the biggest business.

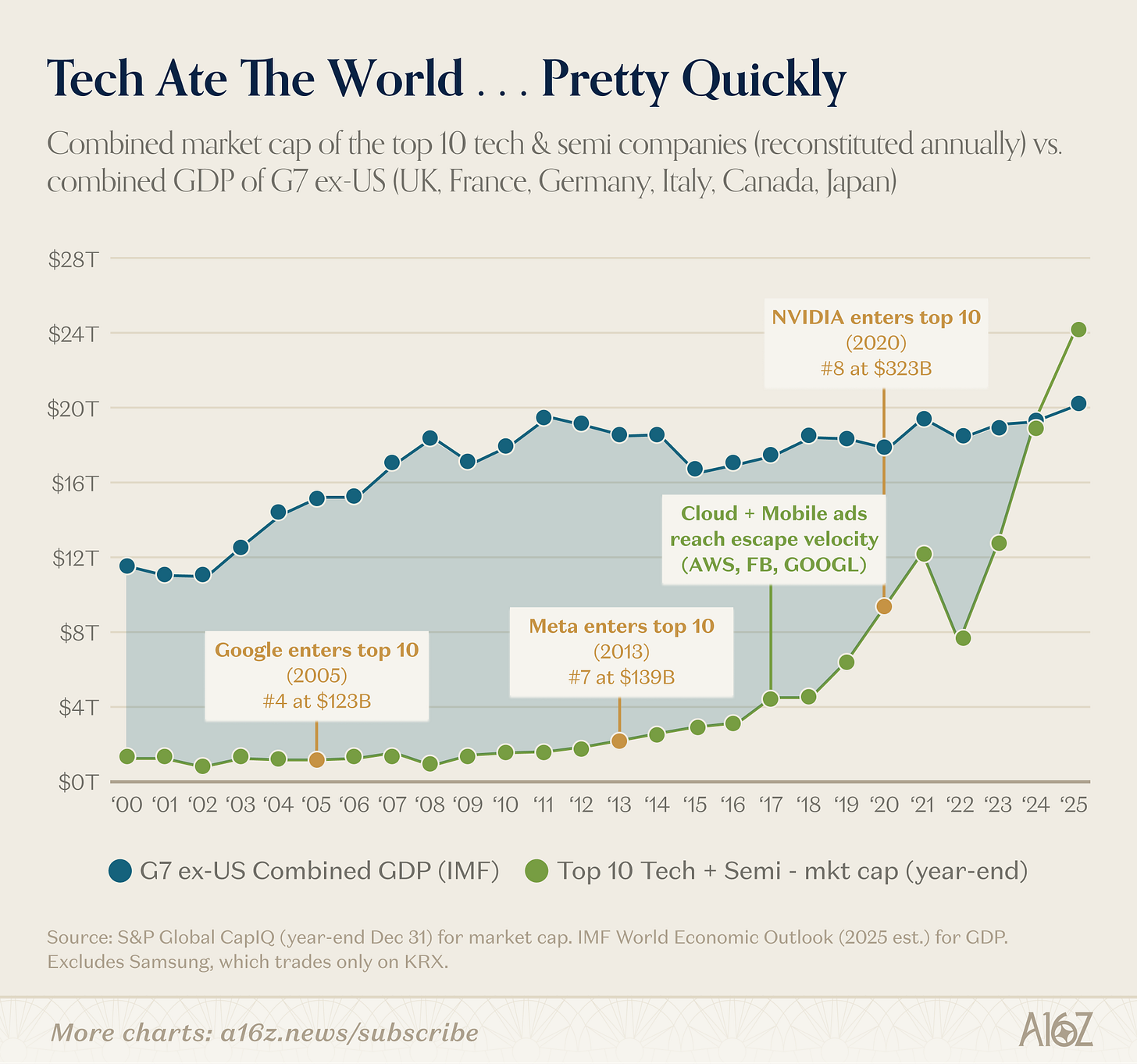

Moreover, technology is taking over the world very quickly:

Caption: Market capitalization of the top 10 tech companies vs. GDP of the G7 (excluding the US), time series.

The market capitalization of the top ten technology companies was once a fraction of the GDP of the G7 (excluding the United States), until cloud computing truly took off in 2016-2017. Since then, in less than a decade, the combined market capitalization of these companies has exceeded the GDP of the entire world excluding China.

The rise of technology is not simply a matter of a new batch of winners.

The largest companies are much larger than they were 10 years ago:

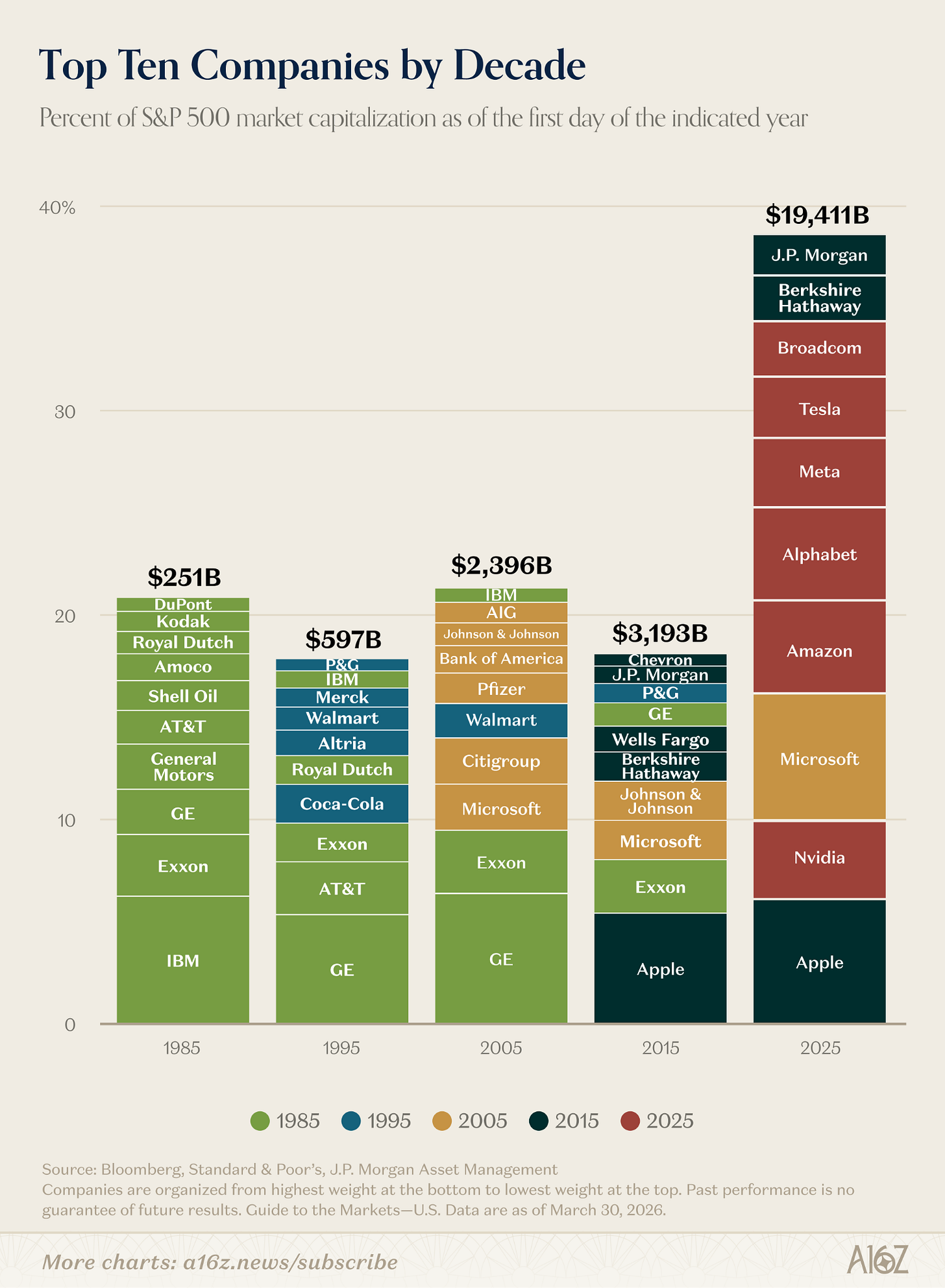

Caption: Changes in market capitalization and percentage of the top ten companies in the S&P 500

The combined market capitalization of the 10 largest companies in the S&P 500 is about six times that of 2015, and their share of the total market capitalization of the index has also doubled.

There was indeed a "reshuffling". The composition of the top ten has changed dramatically compared to the previous decades. By 2025, only three companies were continuations of the previous decade, and only one (Microsoft, a technology company) remained from the decade before that.

If you were an investor in 2015 and tried to model tech stocks using the largest companies in the index at the time, you would have underestimated the upside potential by about six times. Technology fundamentally " broke the model ," redefining the ceiling on how big a company can go.

And the ceiling looks like it's still moving upwards.

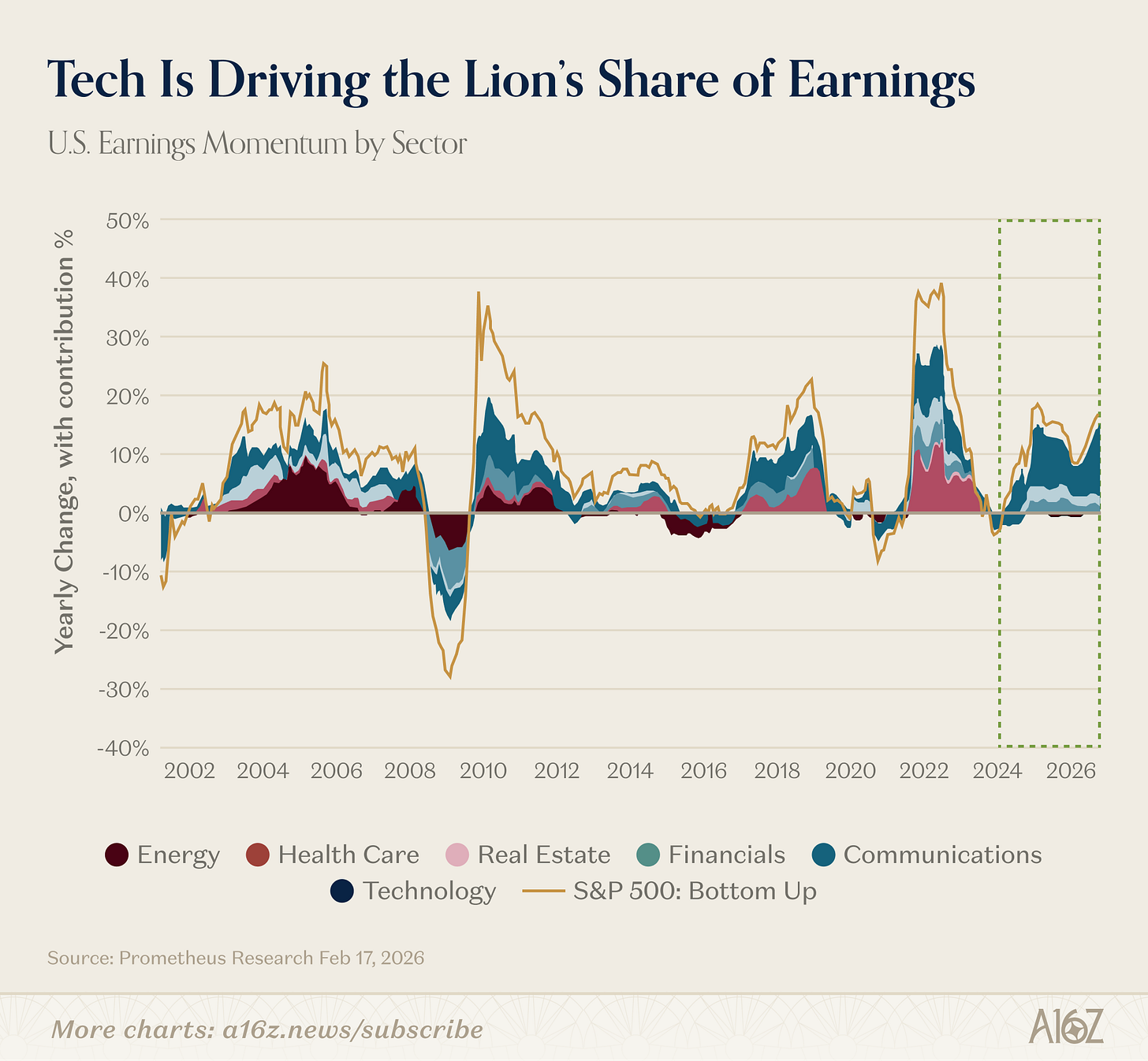

In fact, technology's central role in the global growth story has recently strengthened. As we showed last week, the technology sector's earnings expectations are growing at approximately twice the rate of the rest of the market . Looking further back, you'll find that technology is contributing a historically large proportion of overall market earnings growth:

Caption: The contribution of each industry to the overall market profit growth

Since 2023, technology has contributed more than 60% of the overall market's profit growth.

Apart from the brief period of glory in the energy industry at the beginning of the 21st century, no other industry has played such a central role in profit growth for so long.

Today, it can be said that technology is not a cycle, but the cycle itself.

Railway GPT

We just said that technology is an unprecedented event, but that's not entirely accurate.

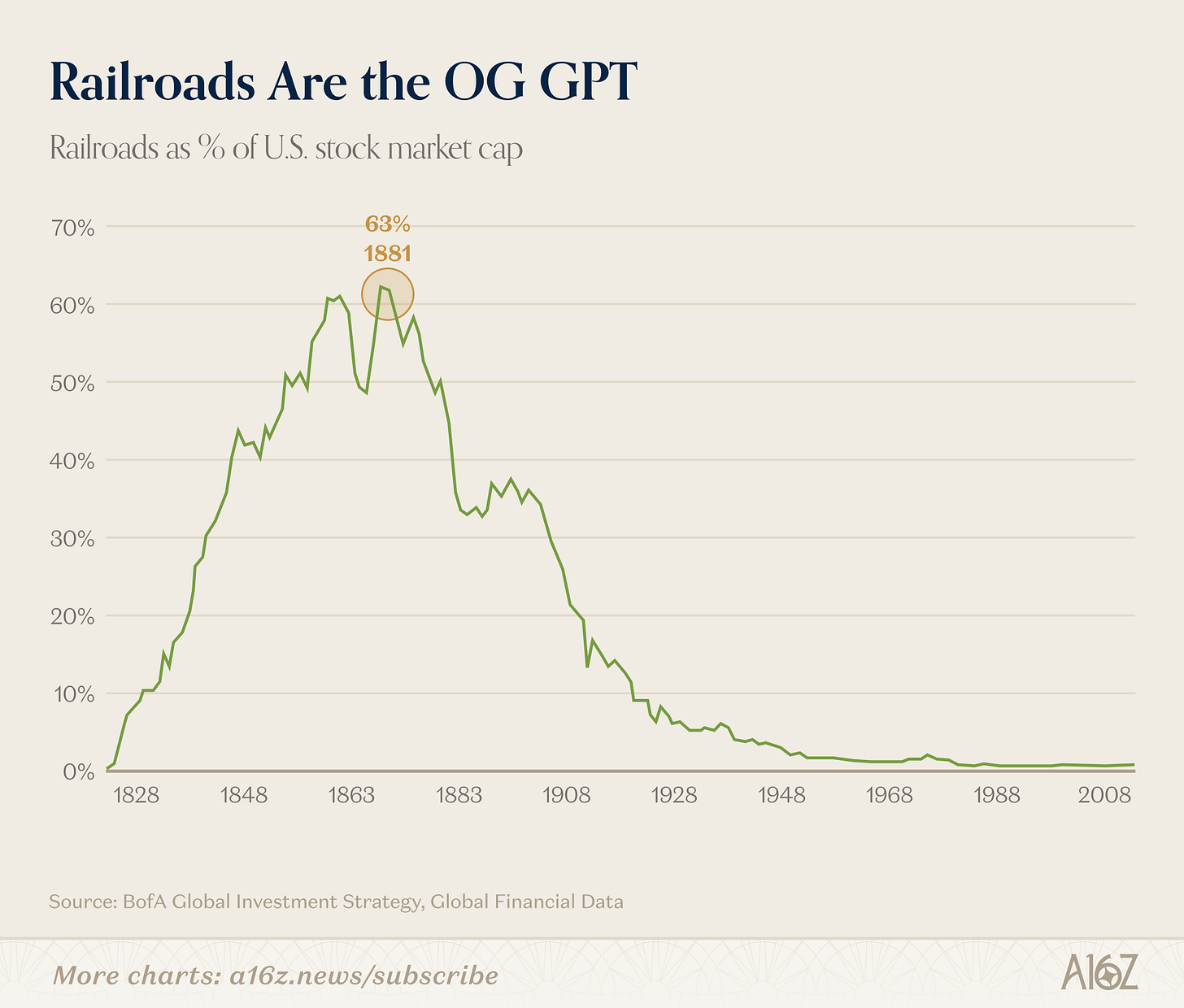

In the industrial age, no industry was more dominant than railroads:

Caption: The railway industry's share of the total market capitalization in the United States (historical peak was approximately 63%).

At its peak, railroads accounted for approximately 63% of the total market capitalization in the United States, which Bank of America called "the most dominant innovative industry in history."

Those who are bearish on the market like to use this railway map to tell a story: Look, railways used to account for 63% of the market, but after the bubble burst, they are now almost negligible.

But things are not that simple. The railway remains important to this day, but what has truly happened is that it has given rise to a completely new and previously unimaginable economic system, one that is far larger than the railway itself.

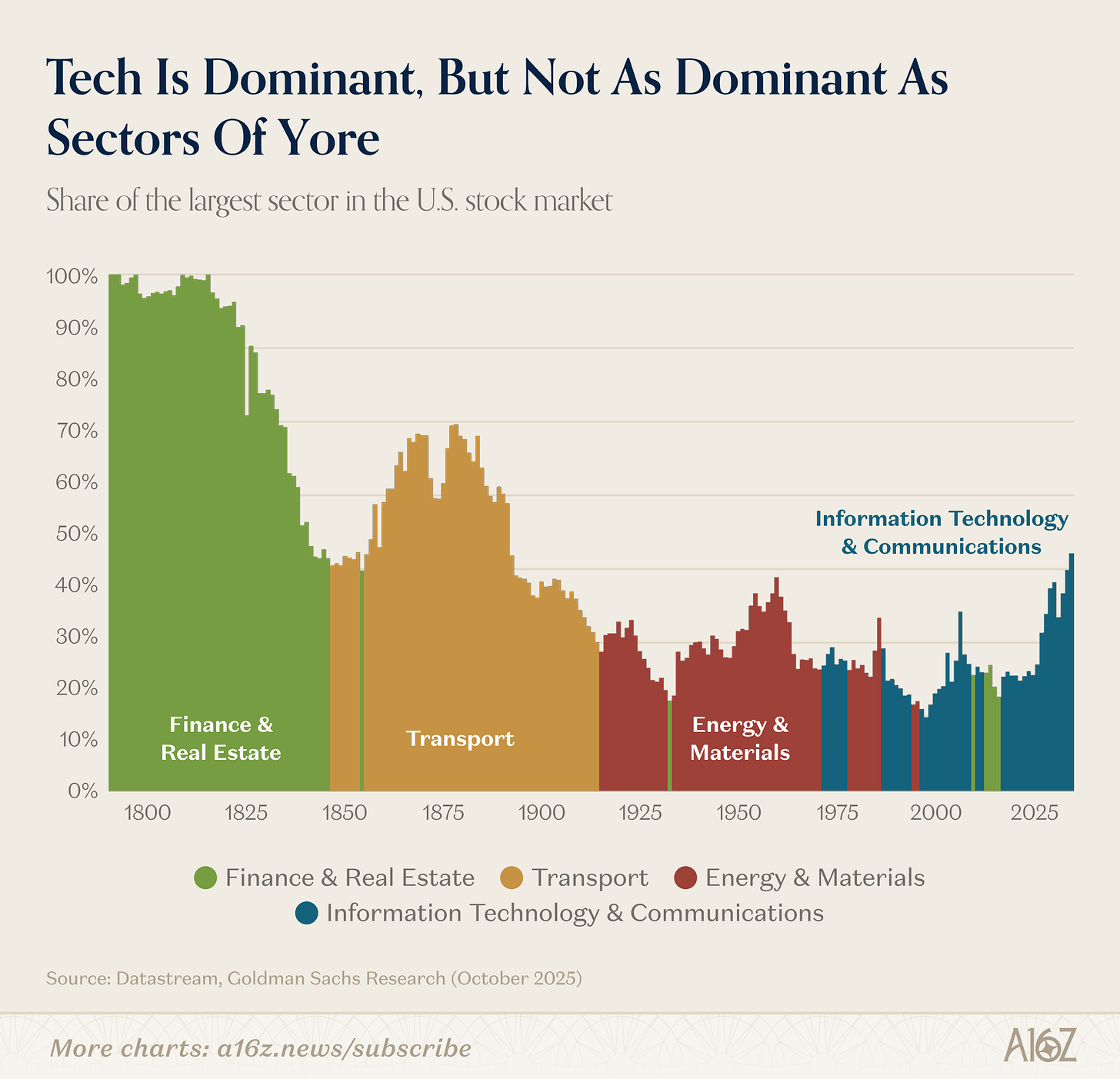

Caption: Changes in the market capitalization share of various sectors in the US stock market (19th century to present)

Railways relinquished their dominant position to industry, which in turn relinquished it to technology (with finance and real estate briefly taking over before the global financial crisis).

Although technology is huge today, it is far smaller in relative terms than the transportation industry (or real estate and finance) at their peak in the 19th century.

The economy has become larger and more complex. About 70% of the industries in the market today were either very small or did not exist at all in 1900.

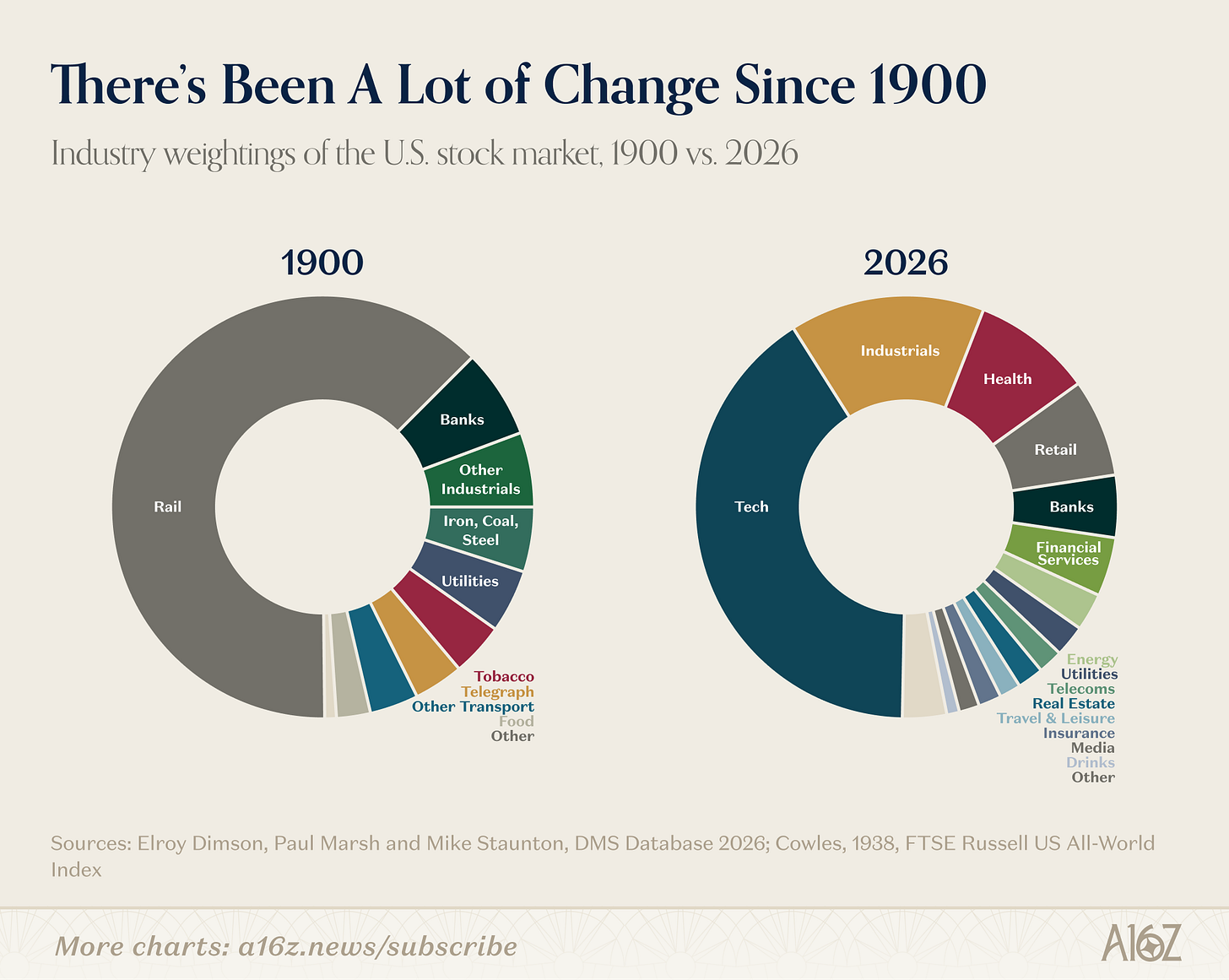

Caption: Industry composition of the US stock market in 1900 vs. today

In 1900, the American economy consisted primarily of textiles, steel, coal, tobacco, plus the railroads that transported them and the banks that financed them. Now, these industries combined represent only a small fraction of the economy.

So the more interesting question is not whether a platform's transformation is a bubble, but what new economy this technological leap will unlock.

Railways are an incredible, versatile technology. One dramatic (but unexpected) change it spurred was the birth of the modern corporate system. Before railways, a company was typically small enough to fit in one person's head. But railways have far too many train sets, too many stations, and too many simultaneous decisions.

In 1855, the director of the New York and Erie Railroad drew what is considered the first modern organizational chart: a hierarchical reporting tree, designed to address the increasingly complex scheduling problems of the railroad. In many ways, middle management, multi-divisional structures, professional management teams, and MBA degrees all originated from the organizational problems of railroad manufacturing.

The railroads changed more than just what the United States produced; they changed the very concept of "business." The railroads fostered middle management, what Alfred Chandler called the "visible hand."

The interesting thing about AI is that, compared to railways, AI may once again rewrite the mainstream organizational template that railways established more than a hundred years ago.

Last month, Jack Dorsey and the management team at Block published an article arguing that the value of AI in enterprises is not in providing everyone with a copilot, but in replacing the functions of middle management. The coordination work typically handled by management—absorbing and routing information, maintaining alignment, and pre-calculating decisions—can be delegated to technology in an AI company, allowing people to return to the periphery and focus their judgment on customer engagement and interpersonal interactions.

According to him, a 170-year-old corporate management model will be entrusted to technology to create entirely new organizational forms. This sounds like a big deal.

Whether Dorsey is right (and what kind of new companies will eventually emerge) is, of course, an open question. But these implications are far more important than whether tech stocks will pull back from their highs this quarter.

Stablecoin transaction volume shifts from transfers to payments

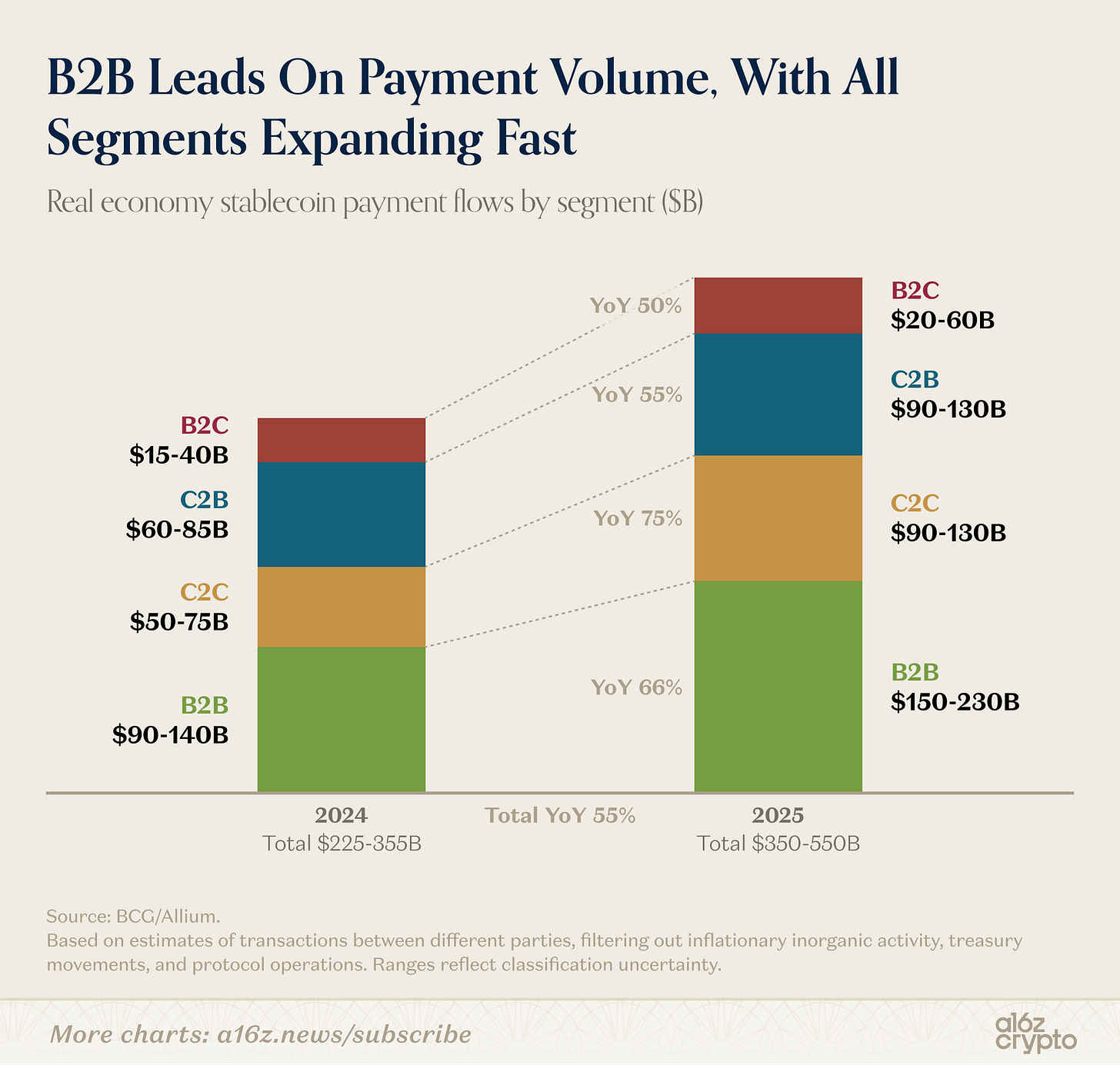

After stripping away the mechanical operations related to trading, fund management, and exchanges—which make up the bulk of stablecoin trading—real-world payment transactions between different parties were estimated to be between $350 billion and $550 billion last year.

Caption: Stablecoin payments broken down by type (B2B, B2C, C2B)

B2B business accounts for the majority of stablecoin payments (which is not surprising given the scale), but B2C and C2B are also growing.

In short, stablecoins are increasingly being used in everyday business activities. This is part of a larger trend, which a16z crypto discusses in detail in this article .

The next decade of journalism

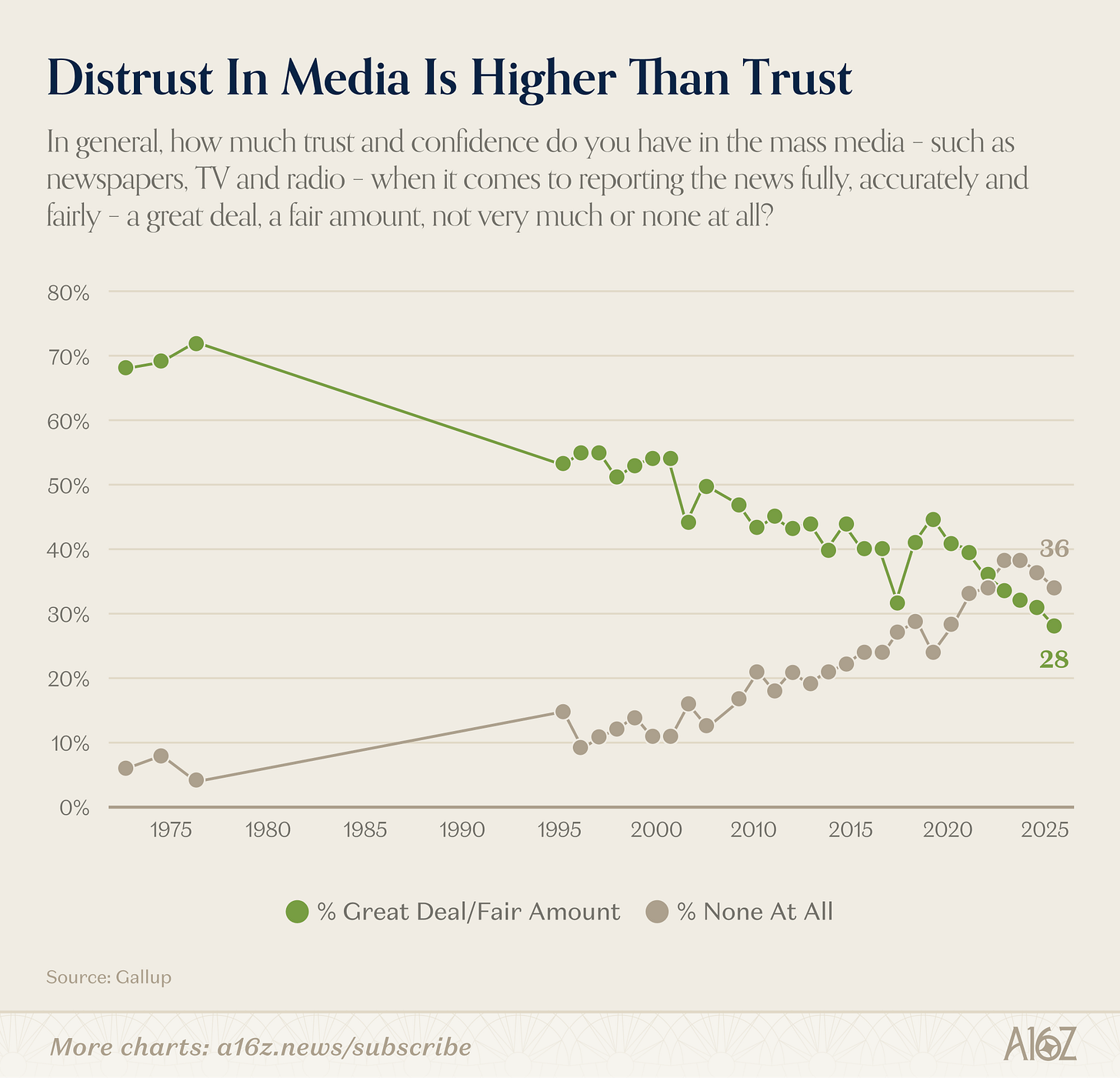

Americans’ trust in the mass media has recently hit a new low, marking one of the most spectacular slow-motion collapses in the history of modern polling.

Caption: Changes in Americans' trust in mass media (1975-2025)

In 2025, only 28% of Americans expressed “great” or “moderate” trust in mass media (newspapers, television, and radio). In 1975, this figure was 72%.

However, the overall level of trust does not tell the whole story.

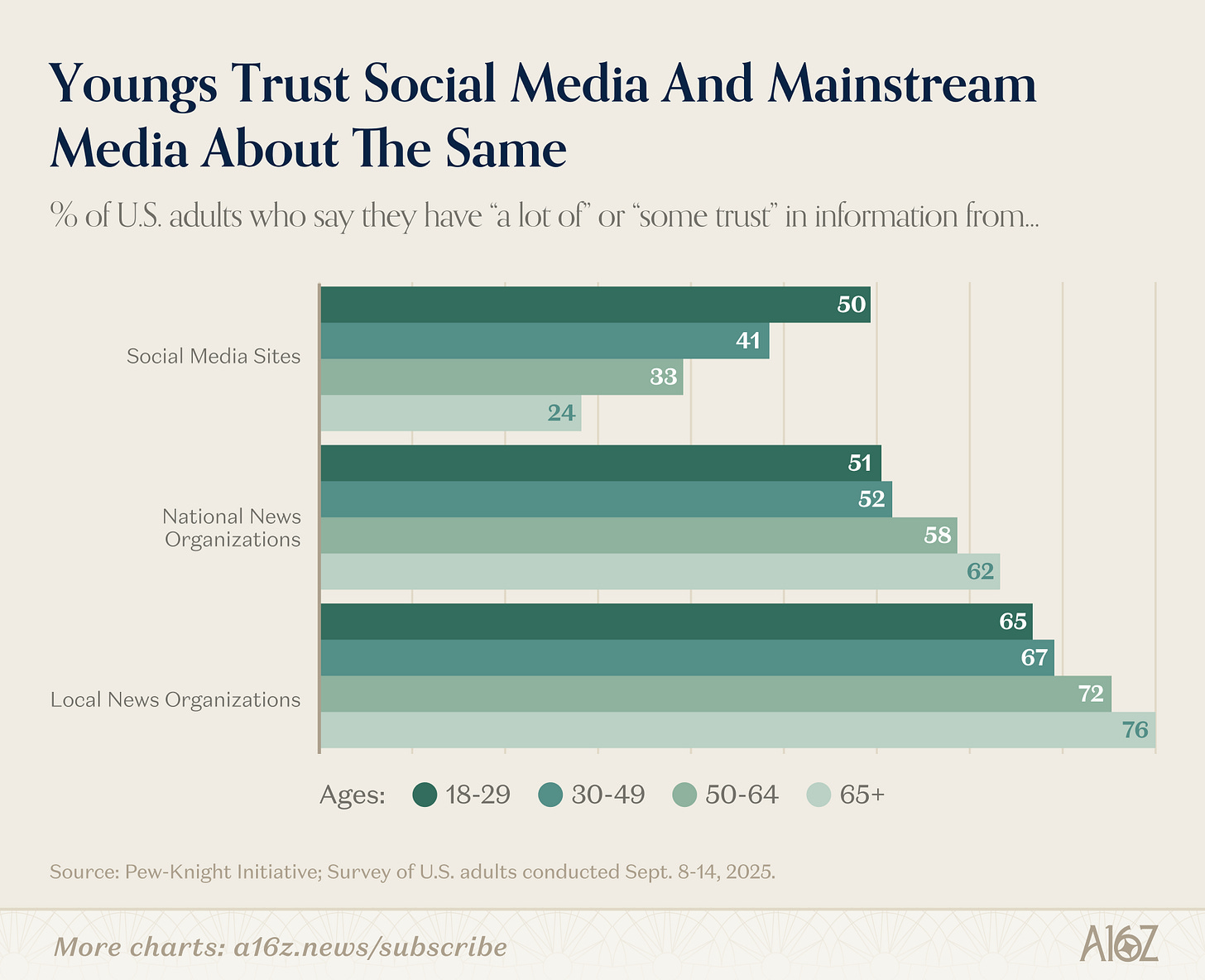

The real story lies in the generational divide, and the rift is enormous:

Caption: Comparison of trust levels between different age groups regarding traditional media and social media.

The younger the person, the less they trust traditional media and the more they trust social media. Conversely, the older they are, the more they trust traditional media and the less they trust social media.

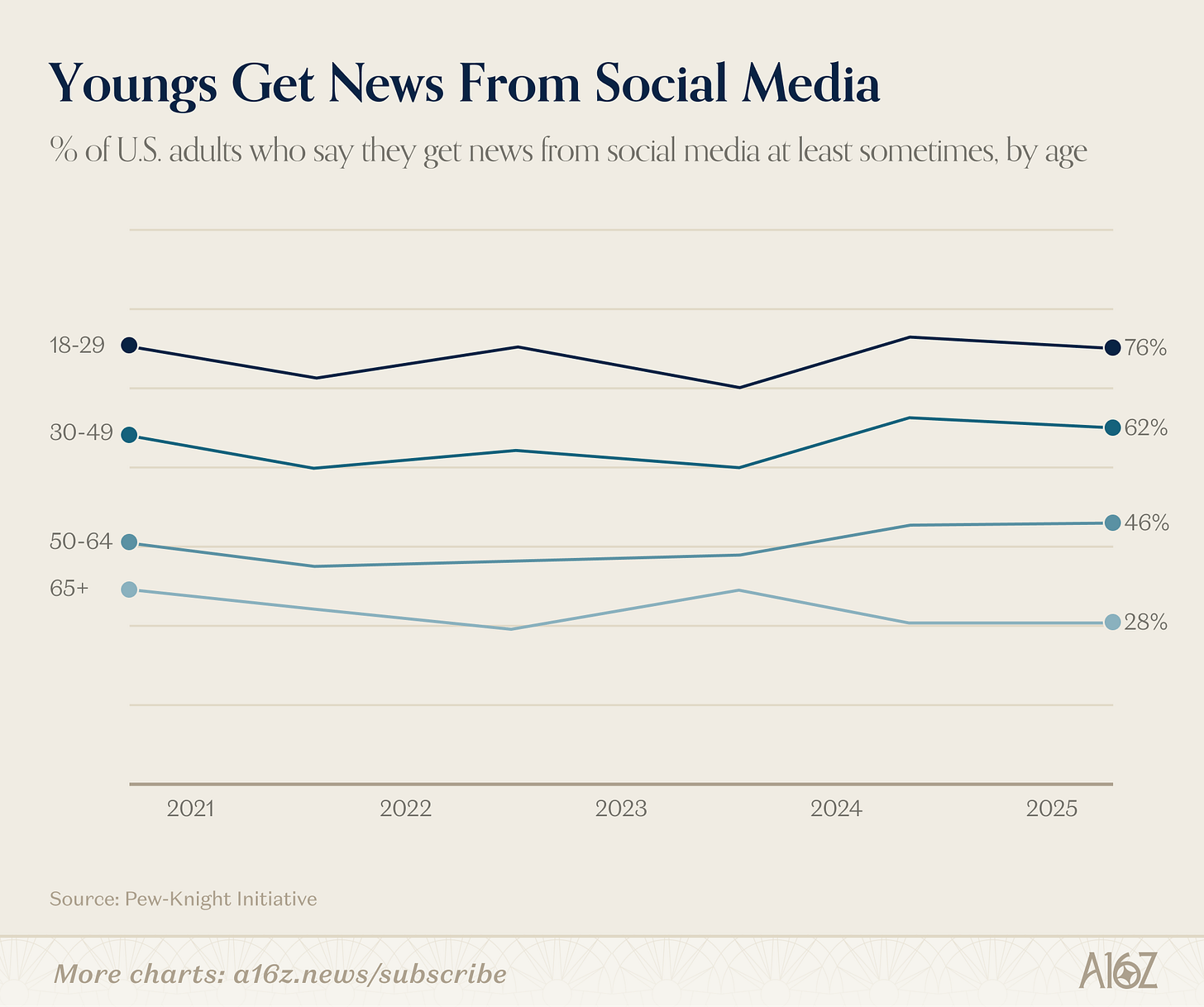

Beyond the trust gap, there is also a consumption gap:

Caption: The proportion of different age groups who obtain news through social media

Among adults under 30, 76% get their news from social media at least occasionally. This figure drops to only 28% for those over 65 (even slightly lower than five years ago).

Trust in mass media has indeed fallen from its peak, but a large part of this story is due to the changing media habits of the younger generation. Compared to their elders, young people have much lower trust in mass media and are also heavy users of social media alternatives.

Returning to the initial observation: the peak of 72% media trust in 1975 is often reminisced about as the golden age of journalism. But it is equally true that in the early 1970s, only a few television networks and newspapers monopolized the supply of information, with virtually no competition.

So it's reasonable to ask: how much of that "peak" level of trust came from excellent news, and how much from having no other choice? The two are certainly not contradictory—the late 1960s and early 1970s likely had both good news and a captivated audience. But it's hard to ignore the fact that the generation with the lowest trust in mass media grew up precisely in an environment with the most choices.

This is precisely the argument put forward by Martin Gurri in *The Revolt of the Public*: the disintegration of information monopolies in various fields (media, government, professional authority) exposes authority that was never truly won. The public sees what's behind the curtain, and trust declines accordingly.

Gurri also said that the public is good at tearing down the old, but not good at building the new. He may be right. But at least, the financial barrier to building new media alternatives has never been lower. Whether they can rebuild trust in news will be the core story of the next decade.

Goodbye, productivity boost.

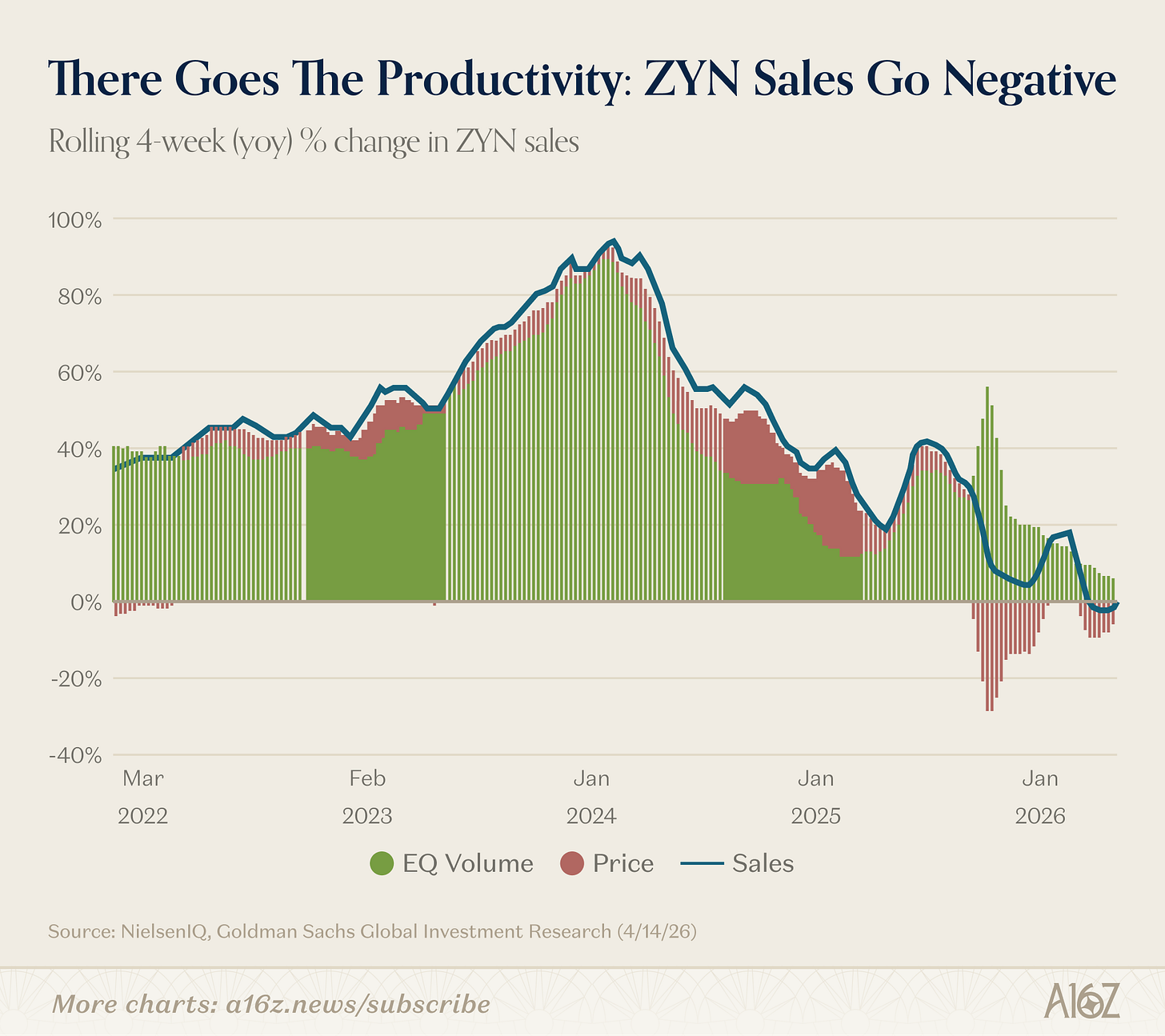

Zyn (nicotine bags) sales have entered uncharted territory: year-on-year growth has turned negative for the first time.

Caption: Zyn's year-over-year sales growth rate (4-week rolling) turns negative for the first time.

On a rolling 4-week basis, Zyn's year-over-year sales growth rate turned negative for the first time ever, albeit by a small margin.

In terms of sales volume, Zyn is actually still growing. However, due to numerous recent promotional activities, total sales revenue has slightly decreased.

Productivity boost is intact (laughs).

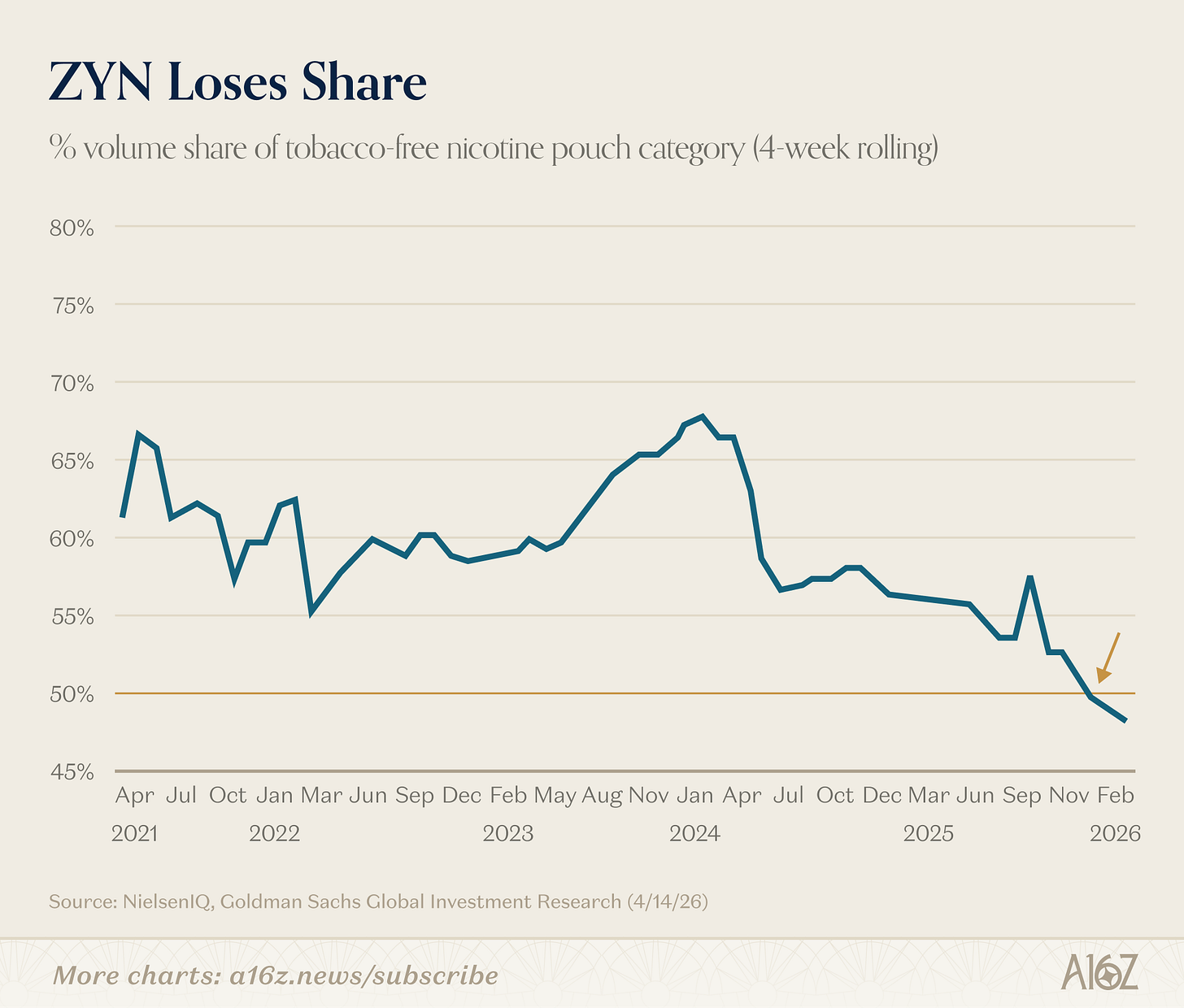

Another interesting detail: Zyn's market share in the nicotine bag market is no longer more than half.

Caption: Changes in Zyn's market share in the nicotine bag market.

Zyn's market share fell below 50% at the end of last year.

[^1]: Yes, we know that stock market capitalization and GDP are comparisons of stock and flow. But the charts are still quite appealing.