Author: Ada, Deep Tide TechFlow

TF International Securities analyst Ming-Chi Kuo posted a message stating that OpenAI is collaborating with MediaTek and Qualcomm to develop mobile phone processors, with Luxshare Precision as the exclusive manufacturing partner, and mass production is expected in 2028. This news has also been confirmed and reported by multiple media outlets.

As soon as the news broke, supply chain stocks rose. Analysts began calculating MediaTek's increased orders, Luxshare Precision's optimized customer structure, and licensing revenue from Qualcomm's baseband solutions.

But the question is, why would a company that doesn't expect to turn a profit until 2030 and whose cumulative cash burn could reach as high as $115 billion make a mobile phone?

Subscription model trap

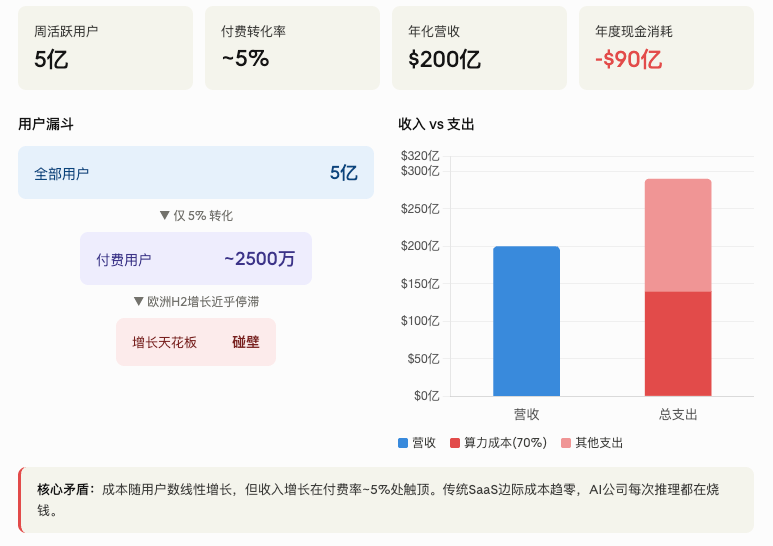

OpenAI achieved $20 billion in revenue per share (ARR) by 2025, representing a 3,628-fold increase since 2020. ChatGPT boasts 500 million weekly active users, placing it among the world's top-tier consumer internet products.

However, according to a Deutsche Bank report in October 2025, only about 5% of users actually paid.

The remaining 95% are free users, and every conversation consumes computing power, electricity, and GPU resources. Even Sam Altman has admitted that even the $200/month Pro subscription is losing money. Total cash burn in 2025 is estimated at $9 billion, with 70% of revenue evaporating directly at server costs.

Furthermore, according to a report by Deutsche Bank analyst Adrian Cox, ChatGPT's consumer-paying user base in Europe nearly stagnated in the second half of 2025. The ceiling for paid subscriptions may be much lower than imagined, and the subscription-driven growth model is hitting a wall.

The problem with the subscription model is that while costs increase proportionally with the number of users, revenue growth plateaus at a certain point. This is a problem that doesn't exist in traditional SaaS, but it's fatal for AI companies.

What should we do then?

Advertising is one option. OpenAI has already started testing ads in ChatGPT, and it poached Fidji Simo, Meta's monetization strategist, as its app CEO. But advertising means direct competition with Google, which generates hundreds of billions of dollars in cash flow annually from search advertising alone, and its moat is deep enough that OpenAI will likely find it difficult to wrest market share from its rival.

Enterprise services represent another path. Currently, enterprise revenue already accounts for over 40% of OpenAI's total revenue, and its growth is indeed rapid. However, Anthropic's annualized revenue from enterprise programming tools reached $30 billion in March 2026, and its secondary market trading price at one point surpassed OpenAI's. This path is also crowded with competitors.

That leaves a third option: hardware.

Hardware isn't a dream, it's financial anxiety.

In an interview with CNBC, OpenAI CFO Sarah Friar stated, "Hardware will be the next layer of value creation for ChatGPT and will help drive user upgrades and subscription growth."

In other words, OpenAI needs a platform to convert free users into paying users. Sell a phone bundled with a ChatGPT subscription, and the user will be automatically charged monthly. There's no need to wait for users to manually open their browsers to upgrade to the Pro version. The hardware locks in the entry point, and the subscription becomes the default option. It's the same principle as bundling iCloud storage to an iPhone.

So, the vision that Ming-Chi Kuo paints—redefining the mobile phone with AI agents, where users no longer need to open a bunch of apps but instead perform tasks directly through their phones—is certainly a compelling technological narrative. But the underlying driving force is more fundamental: OpenAI needs new monetization channels to fill that nearly $10 billion hole every year.

OpenAI's fundamental motivation for making smartphones has nothing to do with innovation. It needs a way to offload computing costs from its balance sheet, and hardware is that offloading vehicle. When users buy the phone, they implicitly agree to pay for cloud-based inference.

OpenAI plans to IPO as early as Q4 2026, targeting a valuation of $1 trillion. Before going public, it must tell Wall Street a growth story beyond just "its model is getting better." Its revenue is being chased by Anthropic, its advertising is just starting out, and its AI agent is still in the conceptual stage. Smartphones are a good story. Billions of smartphones are sold globally every year; even a small slice of that revenue would be enough to drive a significant revenue curve.

Lessons from the past

The gap between a good story and a good business has been repeatedly demonstrated in the field of AI hardware.

Humane AI Pin raised $230 million, priced at $699 plus a $24 monthly subscription fee, but shipped fewer than 10,000 units. In February 2025, it was sold to HP for $116 million, rendering the product unusable and stopping all users' devices from functioning.

The Rabbit R1, the little orange box that was a sensation at CES, sold 100,000 units before facing massive returns. Users discovered that many of the demo functions were unusable. A 10-second delay in voice response rendered the device unusable for real-time interaction. By early 2026, media reports indicated the company was struggling to pay its employees' salaries. Furthermore, users discovered it was essentially just an Android app wrapped in a shell.

Both cases share a common cause of failure: mistaking technological novelty for product-market fit. The demo was phenomenal, with long waiting lists, leading the team to believe it represented market validation. However, users eventually found it less appealing than simply installing the ChatGPT app on their phones.

In an interview, Jony Ive publicly described Humane AI Pin and Rabbit R1 as "terrible products" and said the entire industry "lacks products that express new thinking." He then sold his io company to OpenAI for $6.5 billion.

The competitor in 2028 will not be today's iPhone.

OpenAI phones are expected to enter mass production in 2028. That's two years from now.

What will the mobile phone market look like two years from now?

Apple has already integrated Google Gemini and ChatGPT into the iPhone, Siri's major AI overhaul is expected to be released in 2026, Samsung Galaxy AI already covers its flagship and mid-range product lines, Google Pixel natively runs Gemini, and Android XR glasses are on the way.

In other words, by 2028, every mainstream mobile phone on the market will be an "AI phone." AI capabilities will become a standard feature, just like cameras, GPS, and fingerprint recognition.

So what differentiates OpenAI?

Ming-Chi Kuo's answer is that AI agents need to continuously understand the user's context, and only the mobile phone possesses all the user's real-time state information. OpenAI has the best model, therefore the resulting mobile experience will be different.

This answer has a glaring flaw: model capabilities can be provided through APIs. OpenAI is already selling its models to Apple and Samsung via APIs. If models are the core competitive advantage, then selling models to all mobile phone manufacturers would be more profitable and less risky than manufacturing mobile phones themselves.

Unless OpenAI believes that the revenue from selling model APIs alone is insufficient.

This brings us back to the core question: Is making mobile phones driven by technological ideals or by financial survival?

The history of technology is replete with examples of hardware failures, while the number of successful hardware ventures by software companies is also extremely limited. Google spent ten years developing the Pixel, yet its global market share remained below 2%. Microsoft also lost money for many years before barely breaking even with the Surface. These companies had at least tens of billions of dollars in cash flow to support their trial-and-error efforts, but OpenAI did not.

$852 billion bet

OpenAI's mobile phone story is essentially a narrative demand corresponding to its $852 billion valuation.

Model capabilities are converging, and the window of opportunity for a new model may only be a few months. Gemini, Claude, and Llama are all catching up. As models become commodities, the profit margin for selling models will only become thinner and thinner.

Subscription revenue has peaked, and a 5% paid conversion rate already reflects the market's true intentions. The enterprise market is also being eroded by Anthropic. On the secondary market, Anthropic's trading price has surpassed OpenAI's, indicating investors are voting with their feet.

Against this backdrop, "making smartphones" has given investors a new field of imagination. If OpenAI can sell 100 million AI smartphones, each with a $20 monthly subscription, that's $24 billion in new revenue annually. Adding that to the revenue from the hardware itself, total revenue instantly doubles.

This math problem is certainly easy to solve. But Humane and Rabbit also faced an easy math problem at the time; the solution looked good, but sales were dismal. Consumers are unwilling to pay for a phone without an app ecosystem—without WeChat, TikTok, or Google Play, even the most powerful AI agent cannot meet their daily needs.

Ming-Chi Kuo stated that OpenAI may adopt a subscription-based business model bundled with hardware sales. In other words, the hardware might be sold at a loss, with costs recouped through subscriptions. Another "loss-first, profit-later" story. OpenAI has been telling this story for the past three years, and investors have been listening to it for three years.

But how long can this story continue until mass production of smartphones in 2028? By then, OpenAI will have burned through over $100 billion. If smartphones don't sell, the flywheel will not only stop spinning, but it will turn backward.

CFO Sarah Friar has expressed doubts about OpenAI's IPO timeline, believing the company is not ready to go public, and has reservations about its massive spending plans of up to $600 billion over the next five years. According to Bloomberg, a research firm contacted hundreds of institutions and found that "not a single one is willing to buy OpenAI on the secondary market."

The most likely outcome of OpenAI's foray into smartphones isn't redefining the mobile phone industry, but rather adding another slide to its IPO roadshow. As for how much of that slide will ultimately materialize, none of the conditions will be entirely within OpenAI's control.