Author: Cosmo Jiang, Pantera Capital

Compiled by: Deep Tide TechFlow

Deep Dive: Pantera Capital's annual report reveals the harsh reality of the crypto market in 2025—it wasn't a year driven by fundamentals, but rather by macroeconomics, positioning, and market structure. Bitcoin only fell 6%, but most tokens plummeted by 60%, demonstrating extreme market divergence. For investors and professionals looking to survive in 2026, understanding these drivers is more important than blind optimism.

2026 Market Outlook

The returns in the crypto market in 2025 will not be driven by fundamentals. It will be a year dominated by the macro environment, positioning, fund flows, and market structure effects—especially for assets other than Bitcoin.

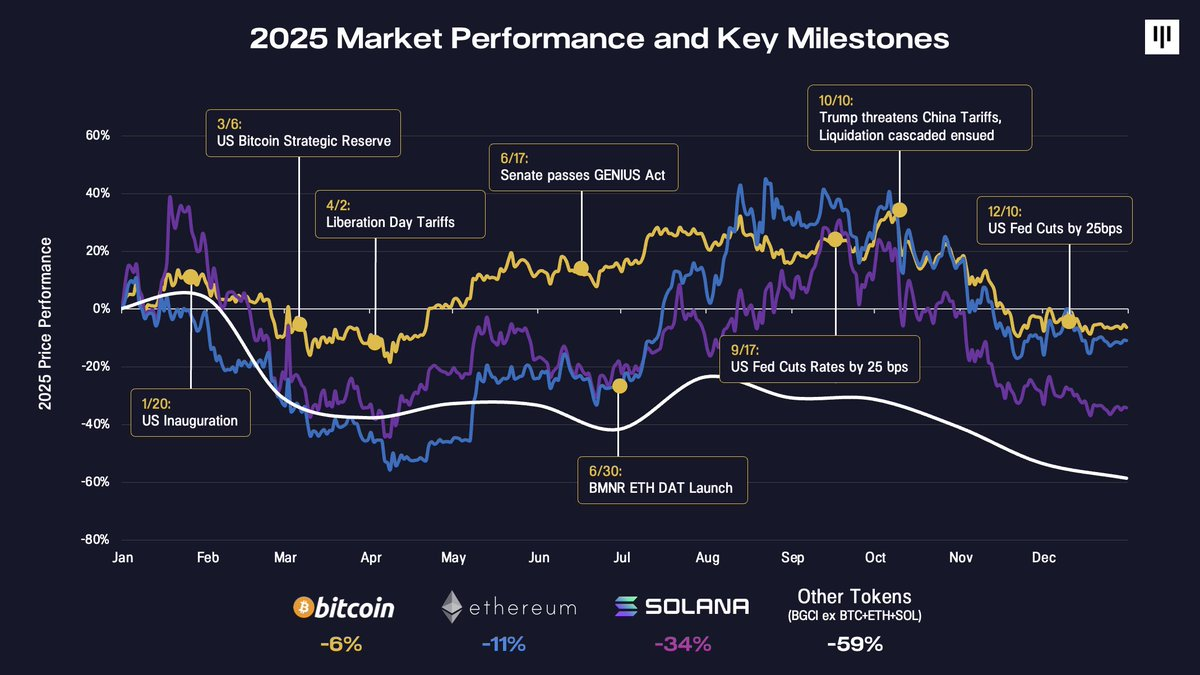

Reviewing the timeline of major macroeconomic and policy turning points throughout the year helps to understand why market trends are so disjointed.

The year began with the US presidential inauguration, which ultimately proved to be a classic "news-driven sell-off" moment and an early warning sign of volatility. In the following months, risk appetite fluctuated wildly—from optimism surrounding the announcement of the US Strategic Bitcoin Reserve to renewed pressure from "Liberation Day" tariffs. Constructive progress arrived mid-year, including the passage of the GENIUS Act, the rise of digital asset treasuries (DATs) such as Bitmine Immersion, and the Federal Reserve's interest rate cuts, which stabilized market sentiment for several months.

The fourth quarter saw a decisive turning point, with multiple challenges emerging simultaneously. The sell-off on October 10th triggered the largest cascading liquidations in crypto history—surpassing the Terra/Luna crash and the FTX collapse—wiping out over $20 billion in notional positions. The market needs time to digest this shock. Meanwhile, key marginal buyers (DATs) throughout the year began to exhaust incremental purchasing power. This downward momentum was amplified by seasonal pressures, including tax-loss selling (particularly in ETFs and DATs), portfolio rebalancing, and systemic CTA flows at year-end.

Bitcoin closed slightly lower in 2025, down about 6%. Ethereum fell about 11%. From there, performance deteriorated sharply. Solana fell 34%, and the broader Universe token (BGCI excluding BTC, ETH, and SOL) fell nearly 60%.

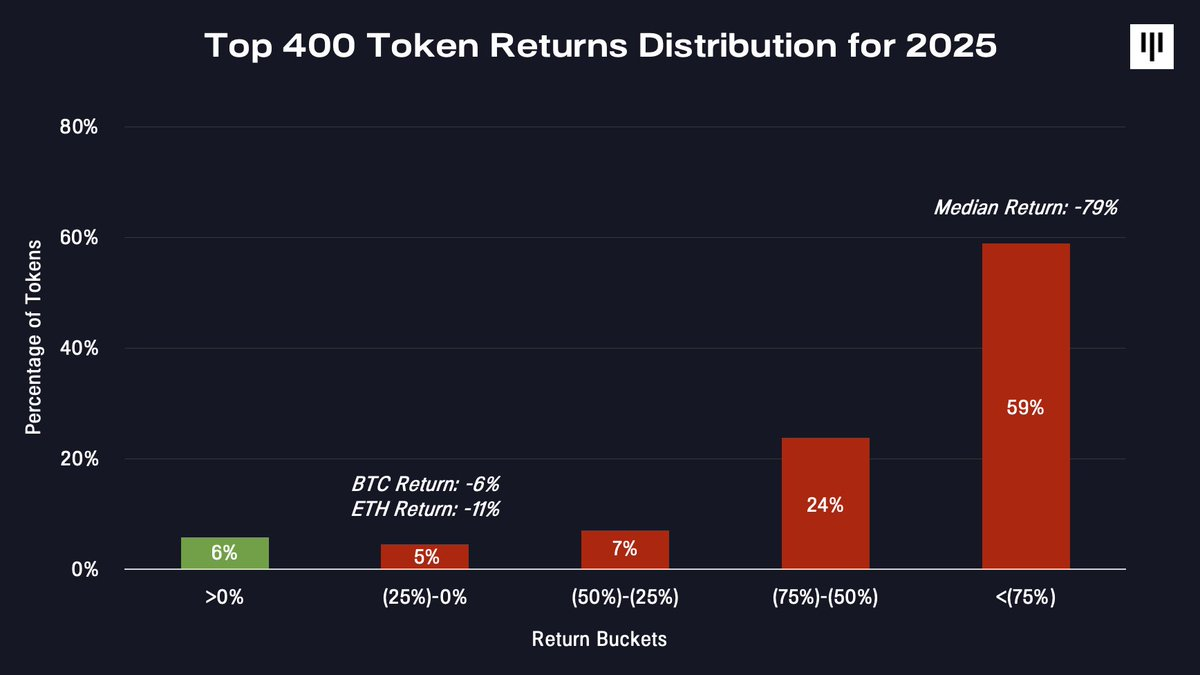

This is an extremely narrow market. This divergence becomes even more pronounced when observing the reward distribution of the token universe.

Only a small fraction of tokens generated positive returns. The vast majority experienced deep drawdowns—the median token fell by 79%.

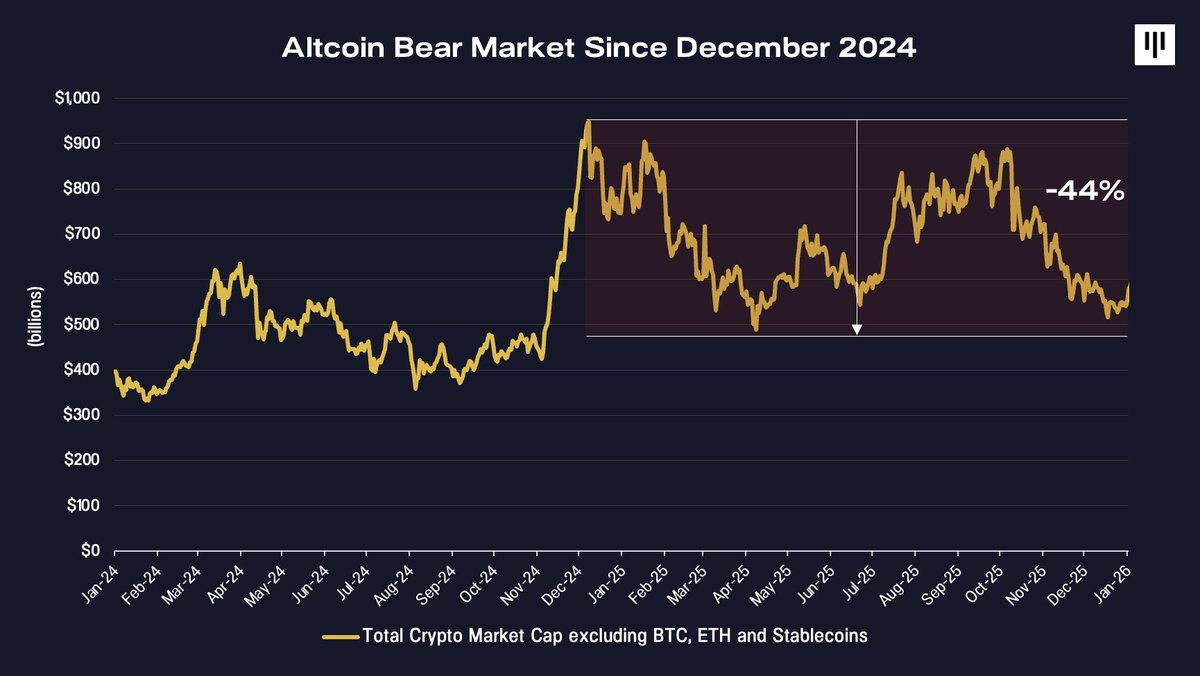

A year-long altcoin bear market

The most underestimated reality in 2025 may be that the non-Bitcoin token market actually entered a bear market as early as December 2024.

The total market capitalization of cryptocurrencies excluding Bitcoin, Ethereum, and stablecoins peaked at the end of 2024 and has been on a slow decline ever since—down about 44% by the end of 2025. From this perspective, it was a year that at least at times looked pretty good for Bitcoin, but for the rest of the market, it was a continuation of an unresolved bear market.

Portfolios with significant exposure to small- and mid-cap tokens are structurally struggling.

The divergence between Bitcoin and the broader token market reflects fundamental differences. Bitcoin benefits from a single, widely understood narrative—digital gold—and increasingly from mechanistic demand driven by sovereign states, governments, ETFs, and corporate treasuries. In contrast, other tokens represent a heterogeneous set of disruptive technologies with less standardized access, less institutional support, and more complex value capture dynamics.

This differentiation is evident in prices.

Structural resistance faced by tokens

In 2025, multiple forces intensified the pressure on the broader token complex.

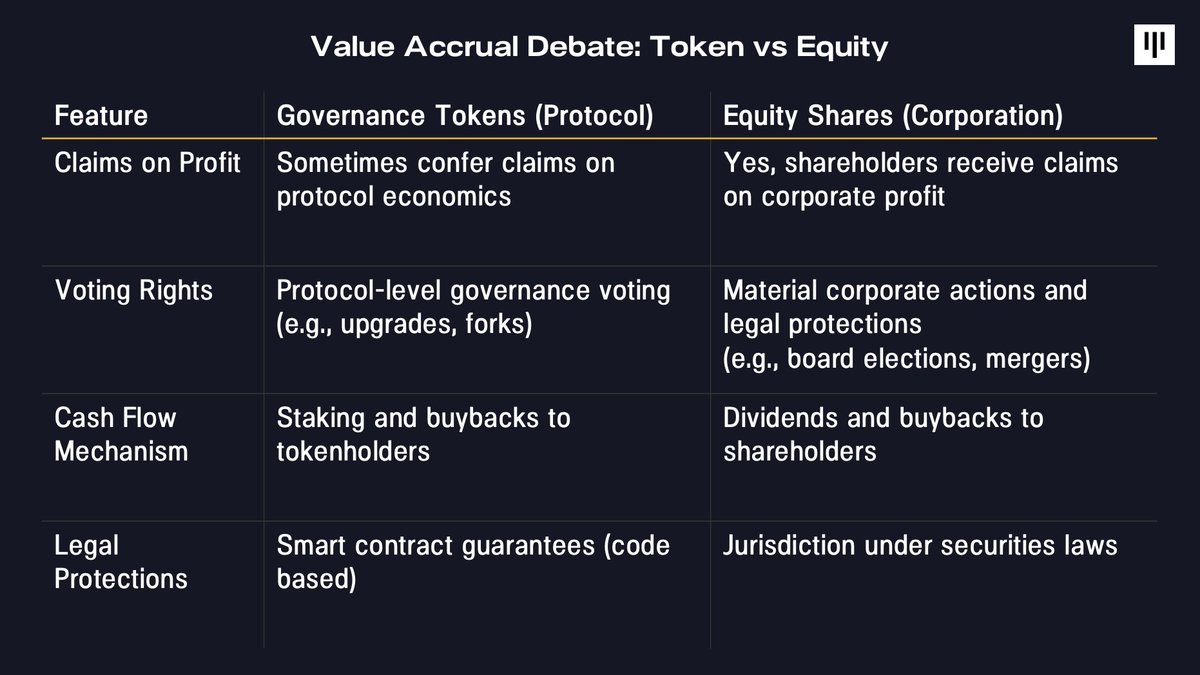

1. Value accumulation and investor rights

One of the most enduring challenges is the unresolved issue surrounding value accumulation. In traditional stock markets, shareholders benefit from clear legal claims to cash flow, governance, and residual value. In contrast, tokens typically rely on protocol-level mechanisms enforced by code rather than government agencies.

This year, several high-profile cases have brought this tension to the forefront, particularly those involving the acquisition or restructuring of token-based ecosystems without direct compensation to token holders, including Aave, Tensor, and Axelar. These events have reverberated throughout the market, undermining confidence even in projects with relatively strong token economics.

In this context, digital asset stocks outperformed tokens, benefiting from a clearer path to value capture at a time when investors were already seeking defensiveness.

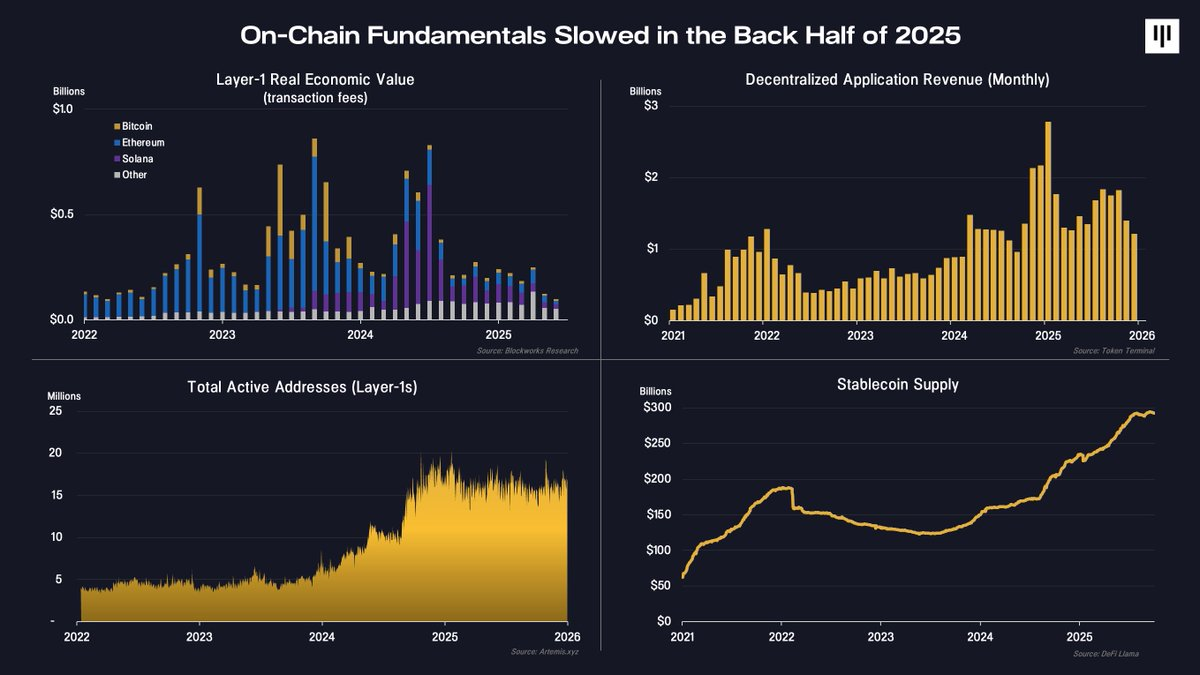

2. On-chain activity slowed down.

The fundamentals of the blockchain also softened in the second half of the year.

On key metrics—including layer-one network revenue, decentralized application fees, and active addresses—activity has slowed. Notably, stablecoin supply continues to grow, indicating continued adoption of blockchain for payments and settlements. However, much of the economic value associated with stablecoins flows to off-chain equity-based businesses rather than token-based protocols.

In reality, the underlying layer in use continues to exist, but marginal, procyclical activity is declining. This shift is directly reflected in token price movements.

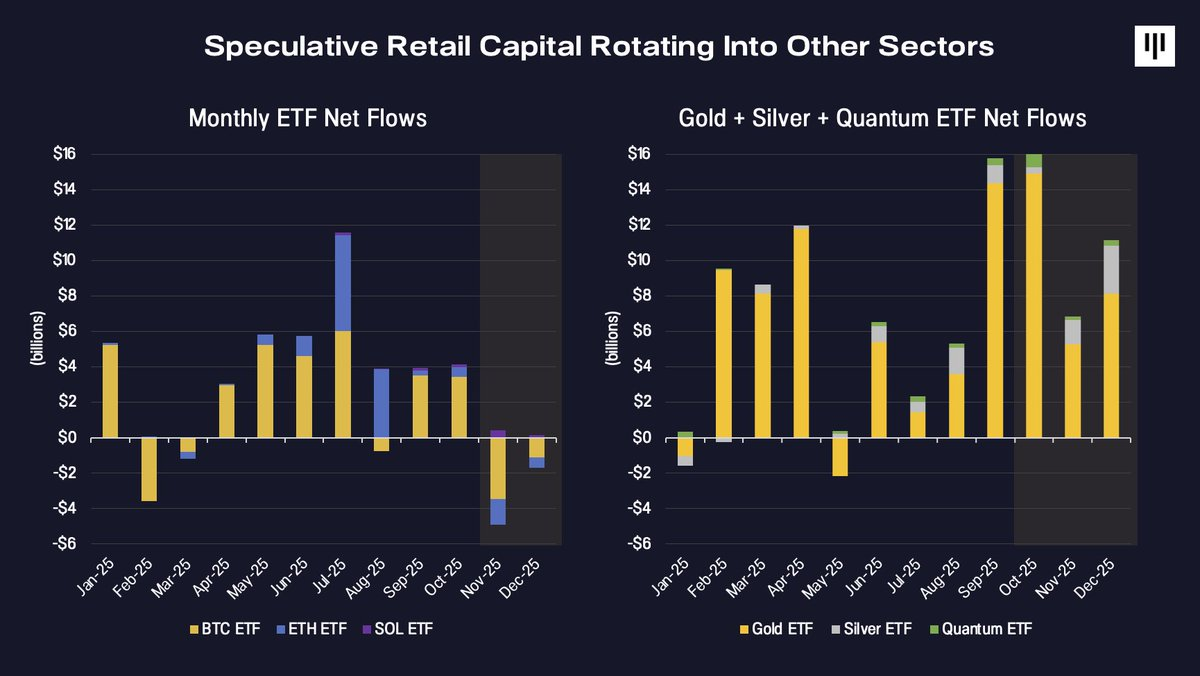

3. The rotation of speculative capital

Finally, the flow of funds reversed. Marginal capital supporting a broader spectrum of tokens has historically been driven by speculative retail investors. While institutional adoption continues to grow, it remains largely concentrated in assets accessible through ETFs, including Bitcoin, Ethereum, and, at the end of the year, Solana.

By 2025, speculative attention had shifted to other areas.

ETFs saw significant inflows into gold, silver, and emerging thematic trading (such as quantum computing), while inflows into digital asset ETFs slowed and turned negative by year-end. This rotation occurred just as token breadth deteriorated, reinforcing downward momentum.

Sentiment, Positions, and Historical Background

By the end of the year, sentiment had compressed to levels historically associated with surrender.

The Fear & Greed Index has reached readings last seen during periods of acute stress, including after the FTX crash. Meanwhile, perpetual futures funding rates have declined, indicating reduced leverage and less excessive speculation.

Seasonal factors also played a role. December has historically been a weak month for Bitcoin and the broader crypto market, with tax-loss sell-offs, portfolio rebalancing, and liquidity constraints creating mechanical pressures independent of fundamentals.

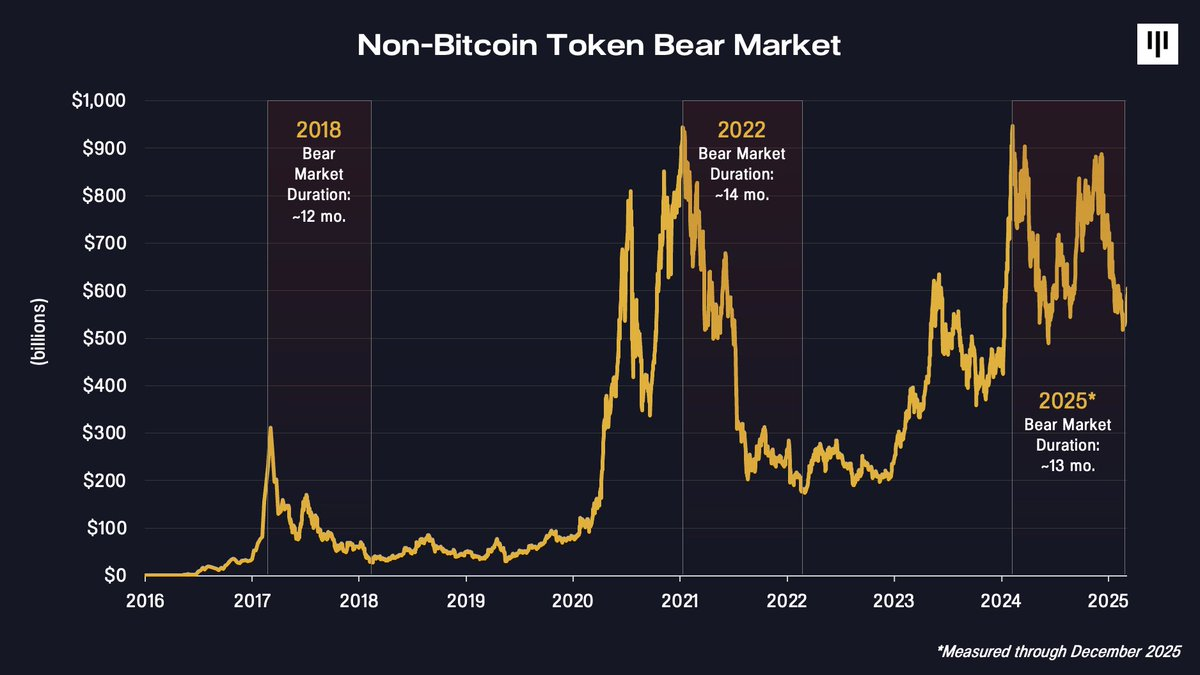

Importantly, from a longer-term perspective, the duration of the current non-Bitcoin pullback is very consistent with previous cycles.

The bear markets of 2018 and 2022 lasted approximately 12 to 14 months. The current pullback, calculated from the peak at the end of 2024, is now within the same range. This doesn't guarantee a bottom, but it does indicate that significant time- and price-based compression has occurred.

Why the outlook starts to improve from here

Despite the challenges ahead in 2025, there are several reasons to remain constructively optimistic about the future.

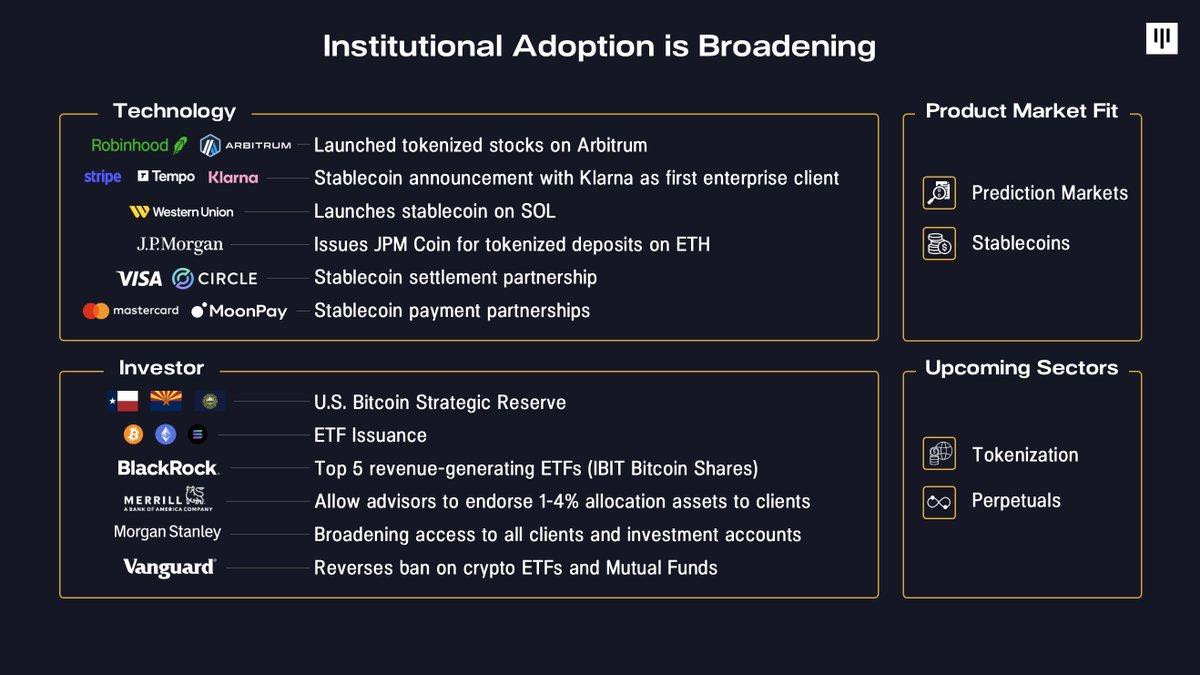

First, institutional adoption continues to expand. Enterprises are increasingly integrating blockchain into their core products—from Robinhood's tokenized stocks to Stripe's development of stablecoin infrastructure, and JPMorgan Chase's tokenization of deposits. On the capital side, sovereign reserves have been established, and securities firms, retirement platforms, and large asset management companies have significantly lowered the barriers to entry.

Secondly, product-market fit is becoming clearer. Stablecoins and prediction markets gained breakthrough attention and adoption as prominent use cases in 2025, while broader tokenization and perpetual futures are showing early signs of product-market fit.

Third, the macroeconomic backdrop is supportive. The US economy remains resilient, wage growth is outpacing inflation, and corporate profits are expanding. The Federal Reserve has now halted quantitative tightening, and liquidity conditions are improving. Historically, the combination of declining long-term yields and loose monetary policy has been constructive for risk assets, including digital assets.

Finally, penetration remains shockingly low. As Bitmine's Tom Lee stated, there are only 4.4 million Bitcoin addresses holding more than $10,000 worth of Bitcoin, compared to 900 million traditional investment accounts globally. According to a Bank of America institutional investor survey, 67% of professional investment managers still have zero exposure to digital assets. Even a modest shift in allocation over time represents a significant source of potential demand.

Conclusion

2025 was a challenging year for most token markets, characterized by extreme divergence, stronger performance from mainstream coins, and prolonged weakness outside of Bitcoin. However, it was also a year of driving institutional adoption, clarifying product-market fit, and compressing valuations across much of the ecosystem.

Opportunities may arise from a strong fundamental backdrop following a year-long bear market across the broader token sector. With sentiment clearing, leverage reduction, and significant repricing already behind us, forward positioning looks increasingly asymmetrical—provided fundamentals stabilize and broad-based returns to normalcy. Historically, periods of turmoil have laid the foundation for the next phase of growth.

[1] The performance of the Bloomberg Galaxy Crypto Index (BGCI) does not include deductions that would reduce performance. Any index is for informational purposes only and is intended as an example of general market performance. No index can be directly compared to the performance of the Pantera Fund, partly because the index is not actively managed. The investment results of the Pantera Fund are not intended to predict or imply future returns of the Pantera Fund.

PANTERA Retrospective – Looking Back at 2026

Author: @JonathanGieg

As we begin 2026, we anticipate an even more exciting year for cryptocurrency than last year. But before turning the page, we'd like to take a moment to reflect on what 2025 has brought.

2025 was a landmark year for Pantera. We deployed more capital than ever before, driving the majority of our new investments and expanding our global footprint in industries and regions we believe will define the next decade of cryptocurrency. Simultaneously, our portfolio received strong public market validation, with four portfolio company IPOs and significant strategic acquisitions.

Read about our progress by 2025:

Nine predictions for 2026

Author: @veradittakit

#1 Real-World Assets (RWA) Take Off

As of mid-December 2025, RWA's total value locked (TVL) reached $16.6 billion, accounting for approximately 14% of the total TVL of DeFi.

predict:

• Government debt and private credit could at least double.

• Tokenized stocks and equity may grow faster when the anticipated "innovation exemption" under the SEC's "crypto projects" is rolled out.

• An unexpected sector (carbon credits, mineral rights, or energy projects) is poised for explosive growth. This sector is characterized by fragmented liquidity, global distribution, and a lack of standards, issues that blockchain-based markets will help address.

#2 AI Revolutionizes On-Chain Security

AI-powered security and blockchain development tools have become incredibly powerful. Real-time fraud detection, 95% accurate Bitcoin transaction marking, and instant smart contract debugging are now available, detecting blockchain vulnerabilities worth millions of dollars.

Prediction: In 2026, imagine a larger shift towards on-chain intelligence, where deterministic, verifiable rules take over smart contract-based governance. Applications will scan code nearly in real-time, instantly identifying logical errors and vulnerabilities and providing immediate debugging feedback. The next major unicorn will be an innovative on-chain security company that improves security by 100 times.

#3 Prediction markets become acquisition targets

$28 billion was traded in the first 10 months of 2025, and the market is consolidating around institutional infrastructure. We reached an all-time high of $2.3 billion in the week of October 20th.

Prediction: This industry will see over $1 billion in acquisitions, excluding Polymarket and Kalshi. The winning platform will build built-in liquidity tracks and market discovery intelligence to pinpoint where and why funds are hidden. Forget the shiny new buttons. It's all about effortlessly empowering users with superpowers: instant access to hidden pools, smarter routing, and predictive order flow.

Sports-focused platforms like DraftKings and FanDuel have become mainstream, partnering with media outlets for real-time odds distribution. New entrants specializing in sports, such as NoVig, will vertically expand their presence, and new startups will emerge in the Asia-Pacific region, as it is a region to watch.

#4 AI as your personal encrypted co-pilot

As systems mature and deliver highly personalized experiences that meet customization expectations, consumer AI platform usage will surge. Seamless integration makes advanced AI feel effortless, transforming its use from cumbersome to instantaneous.

Prediction: Platforms like Surf.ai will attract a diverse audience from crypto enthusiasts to active traders in 2026 through intuitive, advanced AI models, proprietary crypto datasets, and multi-step workflow brokers. I believe that the sophisticated technology and accessible design make Surf the preferred tool for crypto research, offering instant on-chain market insights up to 4x faster than the general options available on other types of platforms.

#5 Banking giants prepare: G7-pegged stablecoins are imminent

Ten major banks are in the early stages of exploring the issuance of a G7-pegged stablecoin. Financial institutions are determining whether industry-wide stablecoins can offer the benefits of digital currency to individuals and institutions in a compliant and risk-managed manner. Meanwhile, a group of ten European banks are investigating the issuance of a euro-pegged stablecoin.

Prediction: Major banking alliances will launch their own stablecoins (regardless of whether these pilot projects succeed in 2026 or different alliances do so).

#6 Privacy, Payments, Sustainability: The Big Three in Institutions

Privacy technologies are thriving in institutional use, with transparent-confidential combinations from protocols like Zama, Canton, and others, though retail use has yet to find traction or scalability. Stablecoins have now reached $310 billion, more than doubling in market capitalization since 2023, expanding for 25 consecutive months. Perpetual swaps now account for approximately 78% of crypto derivatives trading volume, and the gap between perpetual contracts and spot options continues to widen.

Forecast: The gap between institutional and retail privacy will widen in 2026. Stablecoins have a long-term path to over $2 trillion, reaching at least $500 billion next year, and the momentum of perpetual contracts will continue into 2026.

#7 Institutional Macro Perspective

As of December 15, 17.9% of BTC holdings are now in the hands of listed companies and private companies, ETFs and countries.

Prediction: 2026 won't be about hype or memes. It will be about consolidation, genuine compliance, and institutional funding driven by open market liquidity. Cryptocurrencies will integrate into mainstream platforms, upgrade the financial landscape, and challenge current incumbents.

#8 The largest crypto IPO of all time

There were 335 US IPOs in 2025, a 55% increase from 2024; many of these were crypto-friendly, including nine blockchain IPOs. This included crypto-native companies like Circle Internet Group (which went public on May 27, 2025) and crypto-inclusive companies like SPACs; for example, Bitcoin Infrastructure Acquisition Corp went public on December 2, 2025.

Prediction: 2026 will be a bigger year for digital asset IPOs. Coinbase states that 76% of its companies plan to add tokenized assets in 2026, with some aiming for more than 5% of their overall portfolio. Morpho, as an example protocol, has a TVL of $8.6 billion by November 2025.

#9 Accelerated Integration of Digital Assets into the Treasury

Back in 2021, fewer than 10 publicly traded companies owned Bitcoin. By mid-December 2025, 151 publicly traded companies held $95 billion, and this number rose to 164 companies and $148 billion when including governments.

Prediction: 2026 will see a brutal pruning. In each major asset class, only one or two players will dominate. Everyone else will be acquired or left behind, except for a long-tail token winner to follow. It's also globalizing. Metaplanet in Japan has already been aggressive, so the US no longer has this trend due to the diversification of the global treasury landscape.

Wishing you all the best in 2026.

To learn more, please read our Pantera Blockchain Letter.