Preface

Trump's election as the US president in 2024 is a landmark event for the global crypto industry, because cryptocurrency-friendly policies are one of his core governing philosophies. This was followed by a series of favorable policies such as the Bitcoin national reserve, the Stablecoin Act, and Circle becoming the first stablecoin stock. The cryptocurrency industry is gradually moving towards compliance and embracing regulation.

At the same time, many listed companies began to learn from Strategy's successful model as a BTC hoarder. There are tens of thousands of listed companies in the world, and the market value of a large number of listed companies has shrunk severely, and liquidity is extremely scarce. By becoming a hoarder, many shell companies can obtain new financing to supplement their liquidity. So much so that some companies that have nothing to do with cryptocurrency or finance have also joined the ranks of hoarders. For example, ECD, an American luxury car modification company, obtained $500 million through equity financing and became one of the Bitcoin hoarders.

However, recently, listed companies have more and more options for hoarding coins, and many cryptocurrencies in the top 100 cryptocurrencies have been listed as candidates for listed companies. In fact, the tokens of many projects are not suitable for long-term holding. Moreover, many tokens are relatively centralized, and the founding team has a relatively large decision-making power, so it is difficult for hoarders to play a larger role. This article will discuss in detail the binary relationship between hoarders and cryptocurrencies, as well as thoughts on the proposition of decentralization.

1. Cryptocurrency from the perspective of listed companies

There is no doubt that the primary appeal of listed companies to choose financing to purchase cryptocurrencies is market value management. According to Coingecko statistics, there are currently 34 listed companies holding BTC. At the same time, the management of several companies took the initiative to transform the company into a hoarder of cryptocurrencies such as ETH, SOL, and HYPE in 2025 to imitate the successful path of Strategy. In fact, this strategy has indeed brought significant growth to the stock prices of listed companies.

Sharplink (NASDAQ:SBET) previously focused on sports betting. In May 2025, the company announced that it had completed approximately $425 million in private equity financing and would purchase a large amount of ETH as its main treasury reserve asset. The company's stock price rose from $2.97 to $124 in 10 days, an increase of more than 40 times. Cypherpunk Holdings, an early blockchain project investment company, changed its name to SOL Strategies (CYFRF) in September 2024. From the name, it can be seen that the company is the Solana version of Strategy. The company's stock price rose from $0.08 to $4.24 in 3 months, an increase of more than 50 times [1].

Table 1: Purchases of cryptocurrencies by listed companies in the United States and Europe

A large number of listed companies have transformed themselves into coin hoarders as a panacea to boost stock prices, and the crypto assets they purchase have expanded from BTC to SOL, HYPE, and BNB. In fact, many companies buy coins as a follow-up behavior. The management does not fully understand cryptocurrencies and lacks long-term strategic planning for buying coins. This chapter will stand from the perspective of listed companies and select suitable cryptocurrencies for purchase based on their different needs.

1.1 In terms of financing costs, PoS public chain tokens > PoW public chain tokens

The public first became aware of the fact that listed companies hold coins when Strategy purchased more than 20,000 BTC in one go in 2020. The company's CEO Michael Saylor declared that he would only buy BTC and never sell it in the future. Coinciding with the BTC bull market from 2020 to 2021, Strategy's popularity continued to be exposed, and the purchase of cryptocurrencies to help listed companies turn around has become a classic case of capital market operations.

Bitcoin is a representative public chain of PoW (proof of work). Its mechanism is to continuously perform hash collisions in the mining pool through the computing power of CPU, GPU, ASIC and other chips, and finally complete the block generation of the blockchain to obtain BTC rewards. Strategy Before buying BTC, Bitcoin mining companies such as Marathon, Riot, Cleanspark and other companies have some unsold cryptocurrency assets on their balance sheets because their main business is to mine BTC through mining machines.

For listed companies, the problem of PoW public chain assets such as BTC is similar to that of gold. After purchase, they can only be used as strategic reserves, but it is difficult to achieve "money making money" through other means. PoS public chains give more weight to the tokens themselves. The approval of PoS public chain transactions requires nodes to produce blocks, and becoming a node requires staking a certain number of governance tokens. The number of tokens staked by Ethereum network nodes is fixed at 32 ETH, while Solana network nodes have no limit on the number of stakes. Holders of governance tokens can share a certain proportion of transaction gas fees as rewards (the sharing mechanism of different public chains is different).

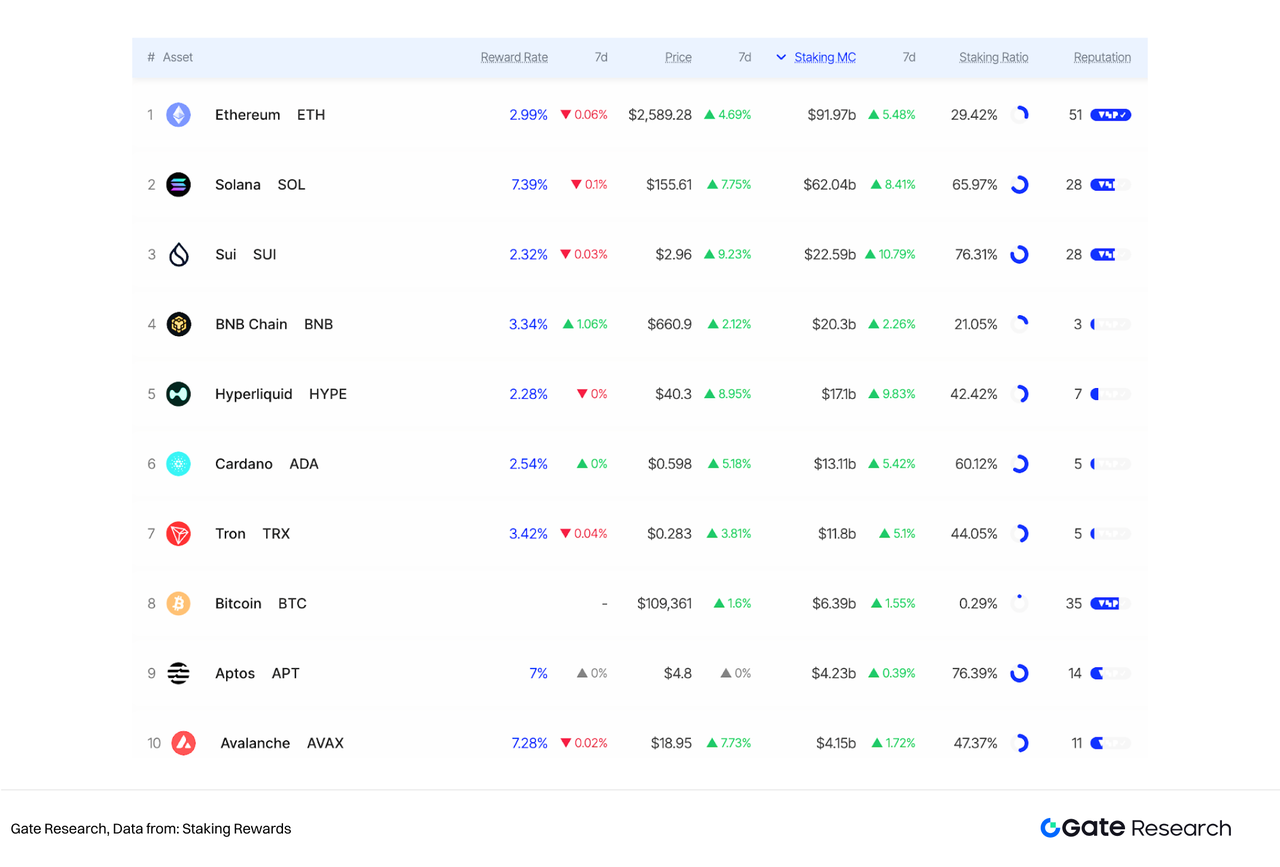

Figure 1: Staking Rewards statistics of the staking yields of mainstream cryptocurrencies

For listed companies that rely on debt financing, by holding the governance tokens of the PoS public chain and staking the tokens, they can obtain an annualized return of 2% to 7% [2]. This part of the income may cover the company's debt financing costs. Even if the company's performance declines, companies holding PoS public chain tokens do not need to worry about interest repayment issues.

1.2 How do listed companies choose PoS public chain cryptocurrencies?

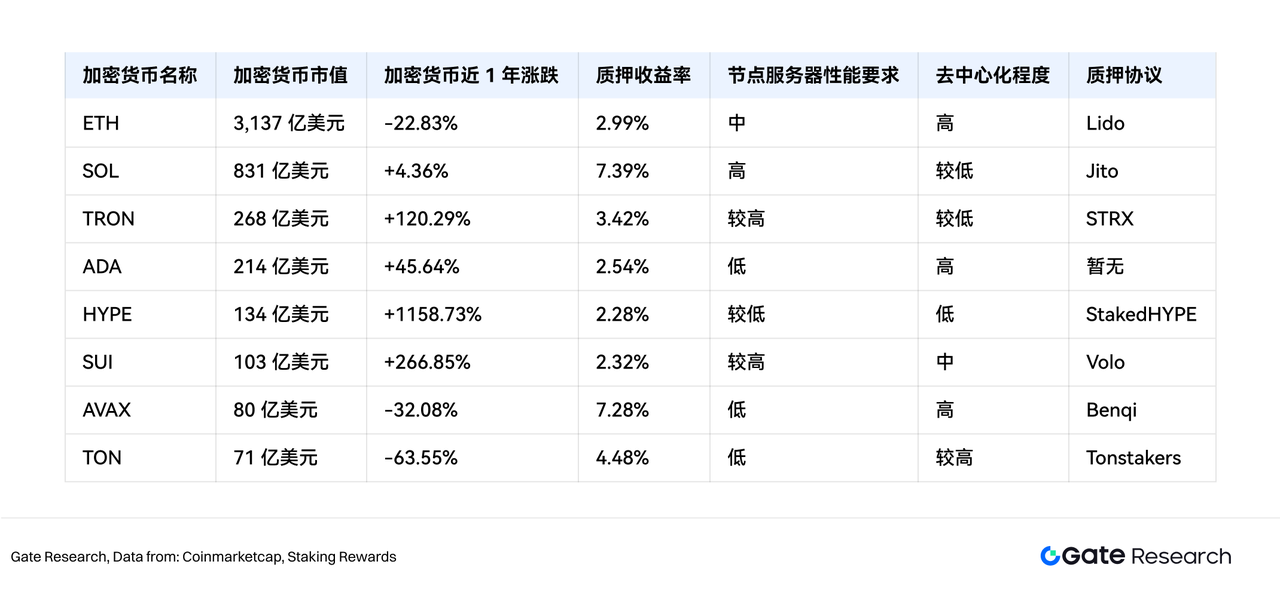

Compared with Strategy's "Buy and Hold" strategy for BTC, it is a more complex and systematic project for listed companies to screen and purchase governance tokens of PoS public chains. Some listed companies may prefer to purchase cryptocurrencies with greater price volatility; some listed companies may prefer to purchase cryptocurrencies with a higher degree of decentralization; and some listed companies are unable to complete the construction of their own nodes, so they need to purchase cryptocurrencies with mature liquidity staking platforms. The following table summarizes the characteristics of various tokens from multiple dimensions, which is a comprehensive reference for listed companies that plan to purchase cryptocurrencies [3].

Table 2: PoS public chain token core information

Note: Data is as of July 3, 2025

The staking yield can be compared to the stock dividend rate. Based on the needs of listed companies, the needs of becoming a PoS token hoarder can be divided into three categories: (1) obtaining high staking returns, covering financing costs and having positive cash flow. (2) obtaining high asset appreciation and driving stock price growth. (3) occupying a core position in the ecosystem and strategically deploying around the public chain ecosystem. The following will screen out suitable targets based on the different goals of listed companies.

1.2.1 Pursuing high returns from staking: SOL has high staking returns and stable public chain transaction volume

For listed companies with high costs for issuing additional stocks or bonds, cryptocurrencies with high staking yields are very attractive. According to Staking Rewards data, the 7-day annualized returns of public chains such as Polkadot, Cosmos, and Celestia are all over 10%. However, due to their own high inflation rates, the price preservation ability of these cryptocurrency assets is very weak. The above three types of crypto assets have fallen by 42%, 36%, and 71% respectively in the past year [4]. The staking income cannot cover the decline in the currency price. It is not the best choice for listed companies.

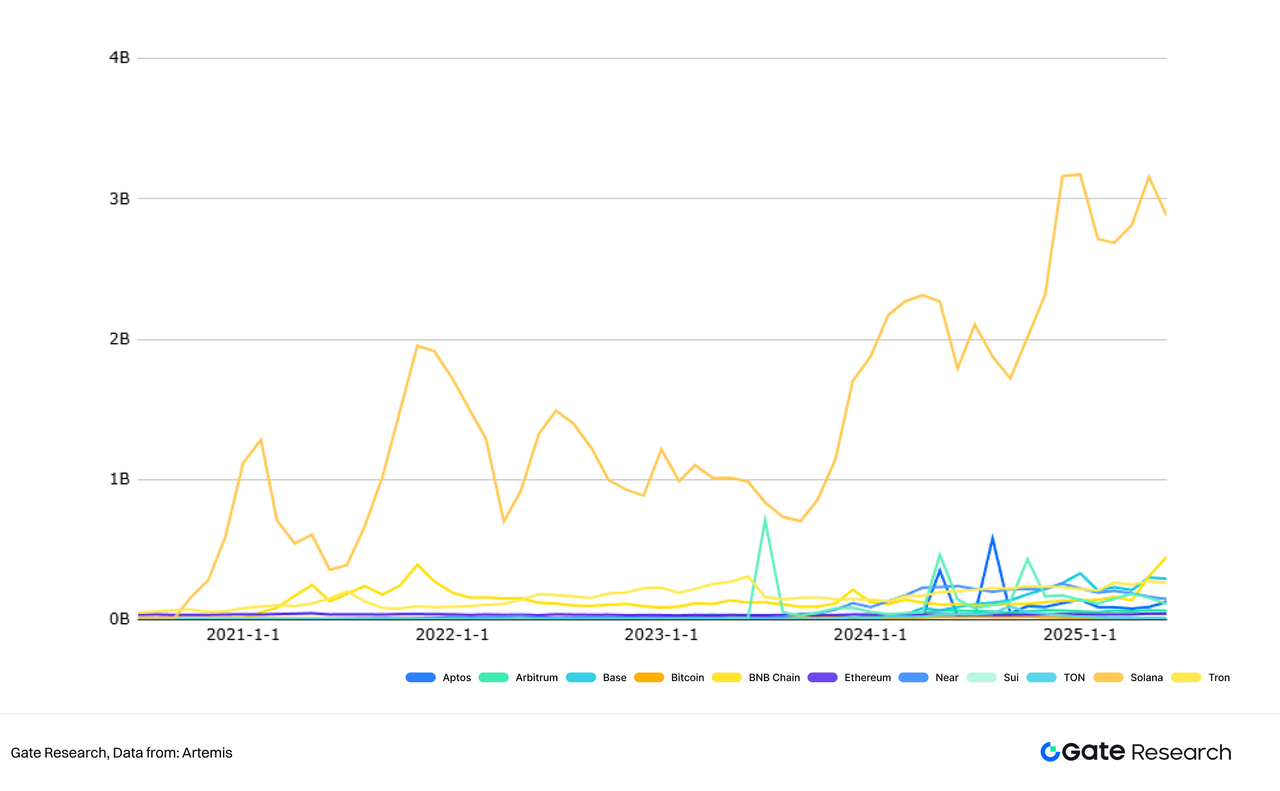

In contrast, while SOL has a higher staking yield, the token price has maintained an upward trend in the past two years, with the maximum retracement of the coin price in the past two years being 52%, which is relatively stable. In Solana's staking income model, the node staking yield = (blockchain rewards + MEV income + Tips income) / total staking amount.

On both the numerator and denominator of the formula, the blockchain reward in the numerator accounts for the highest proportion, and the amount of blockchain rewards is related to the transaction volume of the public chain. The transaction volume of the Solana public chain has maintained rapid growth in the past five years, and Solana's monthly transaction volume in June was 2.97 billion. On the denominator side, the current SOL staking rate has reached more than 65%, so there will be no situation where a large number of SOLs join the staking nodes and cause the yield to decline. Overall, the 7% reward for staking Solana network nodes is relatively stable. [5]

Figure 2: Monthly transaction volume of major public chains in the past five years

From the perspective of listed companies, in the business model of becoming a SOL hoarder through private placement or bond financing and obtaining positive capital flow through node staking, the relatively difficult step is to build a node yourself. Solana network nodes require high-performance servers as hardware support, with the minimum configuration of a 64-core processor, 256G memory, and 1T hard drive. In addition, becoming a network node also requires high-speed network bandwidth to provide support. In terms of software, becoming a Solana node requires downloading Git, Rust, and Docker, and configuring the node requires certain code knowledge.

It can be seen that if a listed company builds its own Solana network node, it needs a high technical threshold. If the company determines that the process of building its own node is relatively complicated, the listed company can choose between the liquidity pledge platform or the RPC node service.

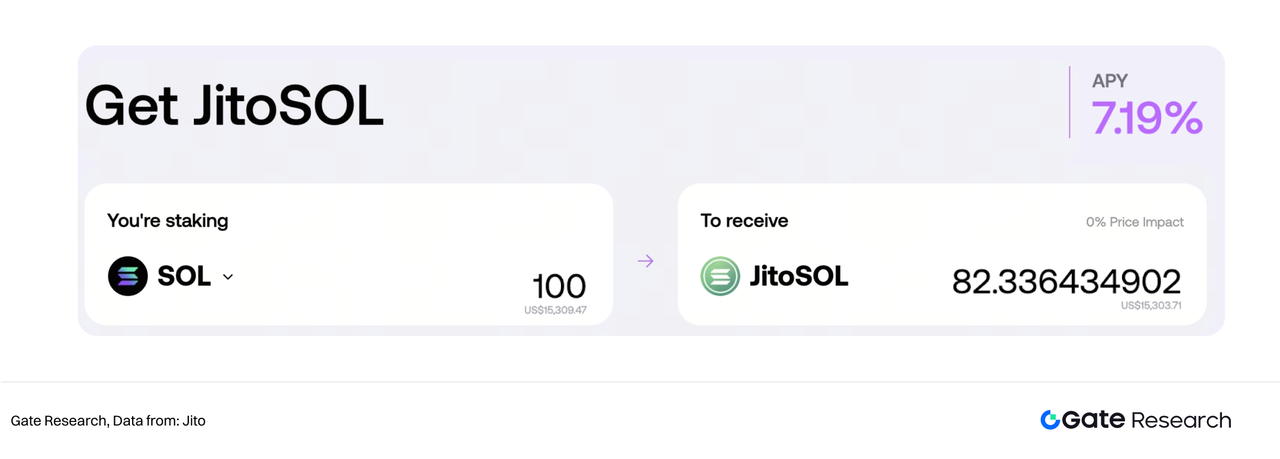

Jito is currently one of the main liquidity staking platforms for the Solana network. Its staking operation is relatively simple. Just connect your wallet and enter the corresponding amount to get an annualized return of 7.19% (as of July 3, 2025). However, using the staking platform will reduce the return to a certain extent, and the platform will not display the direct commission ratio [6]. Professional staking platforms can obtain higher Tips and MEV floating returns through staking, while pledgers receive a fixed annualized return.

Figure 3: JITO staking page

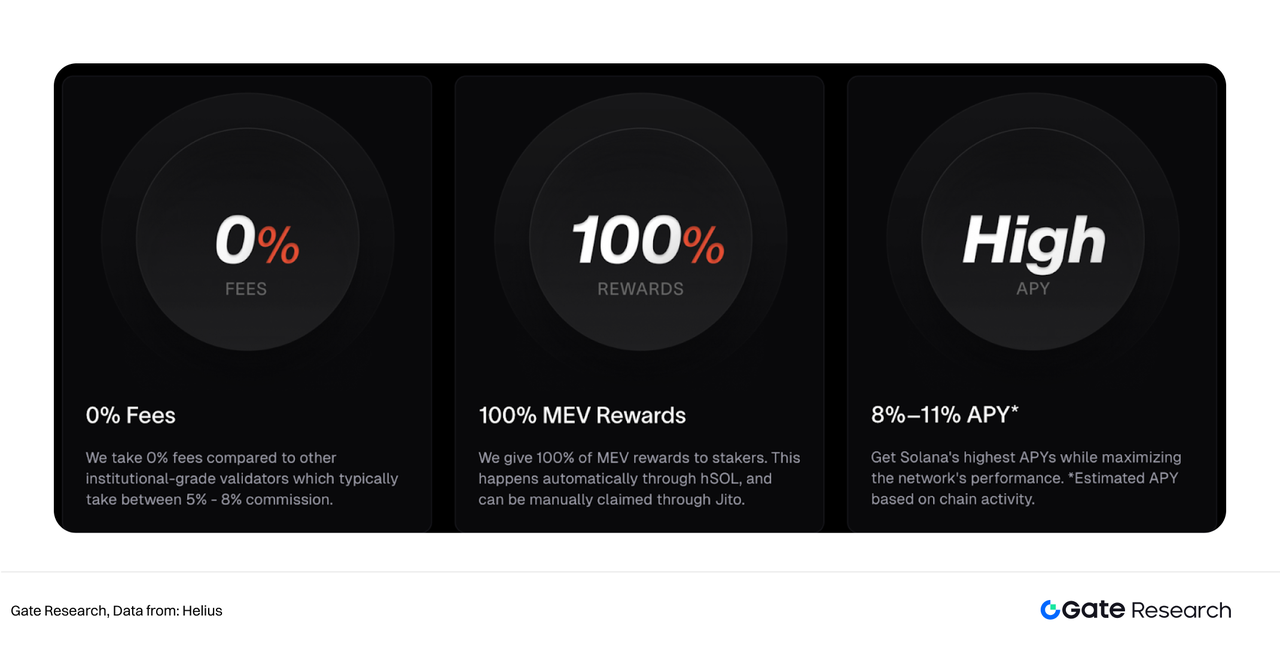

For companies that want to obtain excess returns through Tips and MEV, but want to reduce the threshold for node construction and fixed capital investment, they can choose RPC node services from node service providers such as Helius. Users rent bare metal servers from service providers, which ensure minimum latency (<50ms) and high throughput to meet the high performance requirements of Solana validators. In contrast to staking platforms such as JITO, where user returns are fixed and platform profits are floating; service providers such as Helius charge users fixed fees (different fees for different packages), while floating returns such as MEV and Tips belong entirely to users [7].

Figure 4: Solana Validator product provided by Helius official website

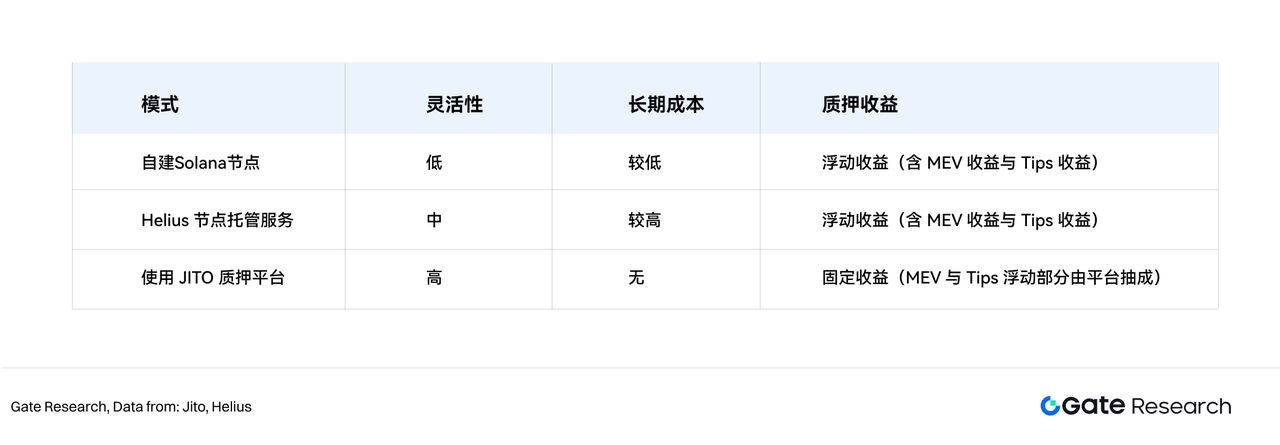

In summary, each of the three options has its own advantages and disadvantages. The pledge platform is suitable for lightweight hoarders with lower investment, the RPC node outsourcing service is suitable for medium-sized hoarders with certain investment, and self-built nodes are suitable for hoarders with relatively strong capital and certain technical construction capabilities. In addition, there are certain risks as a hoarder of SOL. The Solana network is relatively centralized, and there have been many main network downtime incidents before. Such incidents will have a certain impact on the token price.

Table 3: Pros and cons analysis of three Solana node staking solutions

1.2.2 Pursuing value growth: HYPE transaction fee repurchase mechanism, the currency price has achieved a 10-fold increase

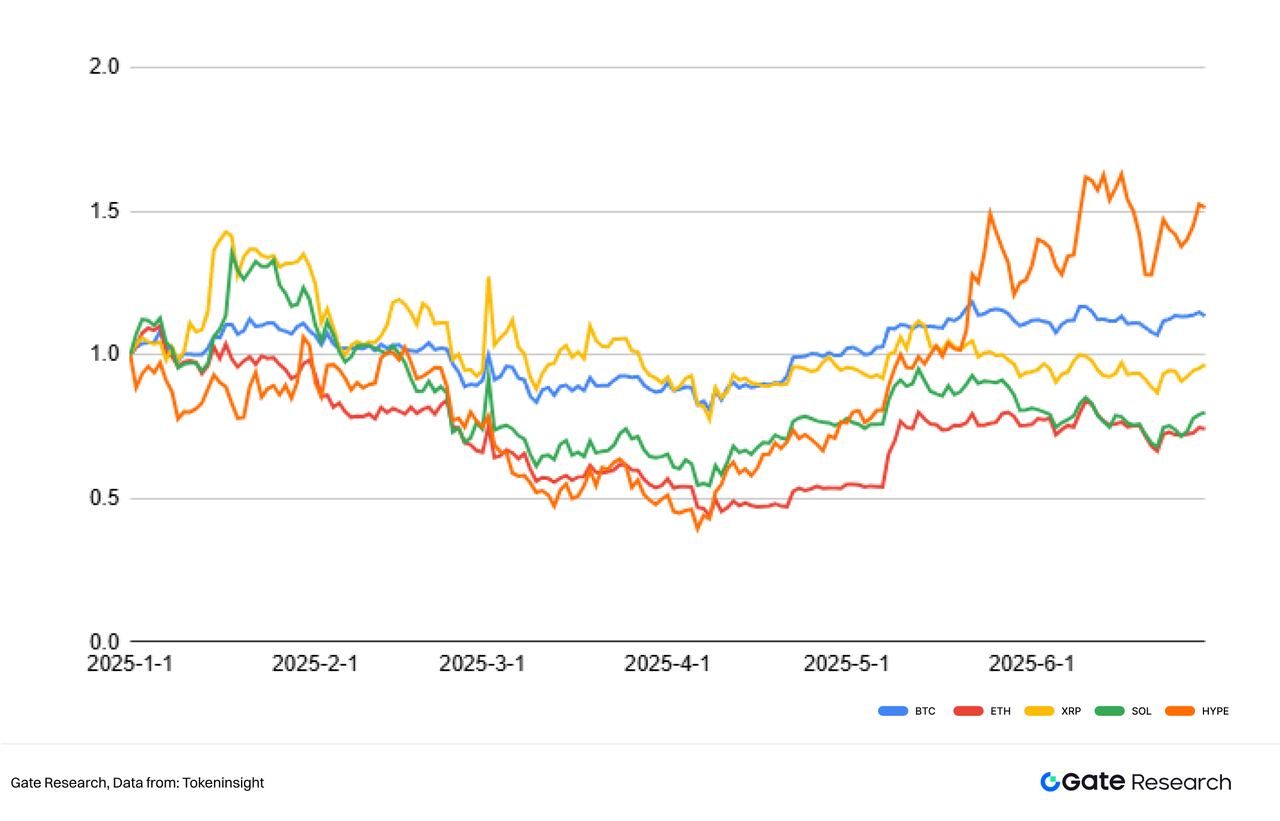

For listed companies with liquidity shortages, the first demand in the short term is still to increase the stock market value and maintain the normal operation of the company by reducing stock holdings. As a hoarder, a common way for listed companies to quickly increase their stock prices is to buy assets with high growth rates or high valuations. HYPE is the mainstream cryptocurrency with market value growth in the first half of 2025 [8]. If a listed company becomes a HYPE hoarder, its stock price will be linked to the price of the HYPE token, which may achieve rapid growth in the company's market value in the short term.

Figure 5: Price trends of HYPE and other mainstream cryptocurrencies in the first half of 2025 (normalized)

Compared with public chains such as SUI, TRON, and XRP, which have also achieved significant growth in market value in the past year, HYPE's advantage lies in its refined token supply and demand management, which ensures the scarcity of HYPE tokens. In the past six months, Hyperliquid's assistance fund has repurchased a total of $910 million worth of HYPE by reinvesting about 97% of gas fee income in HYPE repurchases. Currently, only 34% of the total supply is in circulation, 23.8% of the tokens held by the team will be locked until 2027-2028, and nearly 39% of the tokens are designated for community rewards and will be distributed gradually. Since the project has not accepted venture capital funds, there is no external selling pressure, which enhances the long-term value potential of HYPE.

Hyperliquid's operating nodes are more centralized than Solana's, with only 21 nodes in the entire network, which to a certain extent maintains the high efficiency of the public chain. Therefore, even if a listed company purchases a large amount of HYPE, it is difficult to become one of the 21 core nodes. StakedHYPE, the official staking platform of the public chain, will become an option for hoarders to obtain additional income through staking. The platform has attracted more than 10 million HYPE to join the staking [9]. Compared with other public chains, HYPE's staking yield is relatively low. The Staking Rewards website shows that the yield is only 2.28%.

1.2.3 Pursuing ecological layout: ETH has a high degree of decentralization and Layer2 development is easy

In the field of cryptocurrency, public chain redundancy is an obvious phenomenon. According to Coingecko statistics, the total number of public chains in the entire network has exceeded 200 [10]. In fact, most developers will choose major public chains such as Ethereum, Solana, Sui for product development, and the transaction volume of a large number of independent public chains has declined year by year.

From the perspective of listed companies, some companies are no longer satisfied with being just coin hoarders, but hope to build a second curve of business growth by hoarding coins and developing DeFi or GameFi projects on the public chain. Ethereum Layer2 modular blockchain has become the first choice for these companies due to its low development difficulty and high flexibility.

Rollups as a Service (RaaS) is a major trend in blockchain infrastructure in 2024-2025. RaaS platforms (such as Caldera, Conduit, and Zeeve) provide one-stop solutions, including SDKs, templates, testnet faucets, and block browsers, allowing companies to deploy Layer2 networks in minutes, while traditional self-built Rollups may take 6-9 months. For example, Caldera claims that it can complete Rollup deployment within 30 minutes. This convenience greatly reduces the technical threshold, allowing listed companies to focus on business innovation rather than infrastructure management [11].

In terms of Ethereum DA layer, Celestia and Near's data availability (DA) layer provide companies with efficient and low-cost solutions. Celestia separates data storage from execution through modular design and data availability sampling (DAS), significantly reducing transaction costs and improving scalability, making it suitable for DeFi applications; Near uses sharding architecture to achieve parallel processing and enhance performance in high-throughput demand scenarios. The seamless integration of both with the RaaS platform further simplifies the development process, enabling listed companies to quickly deploy customized Layer2 networks, accelerating ecological layout and innovative application development.

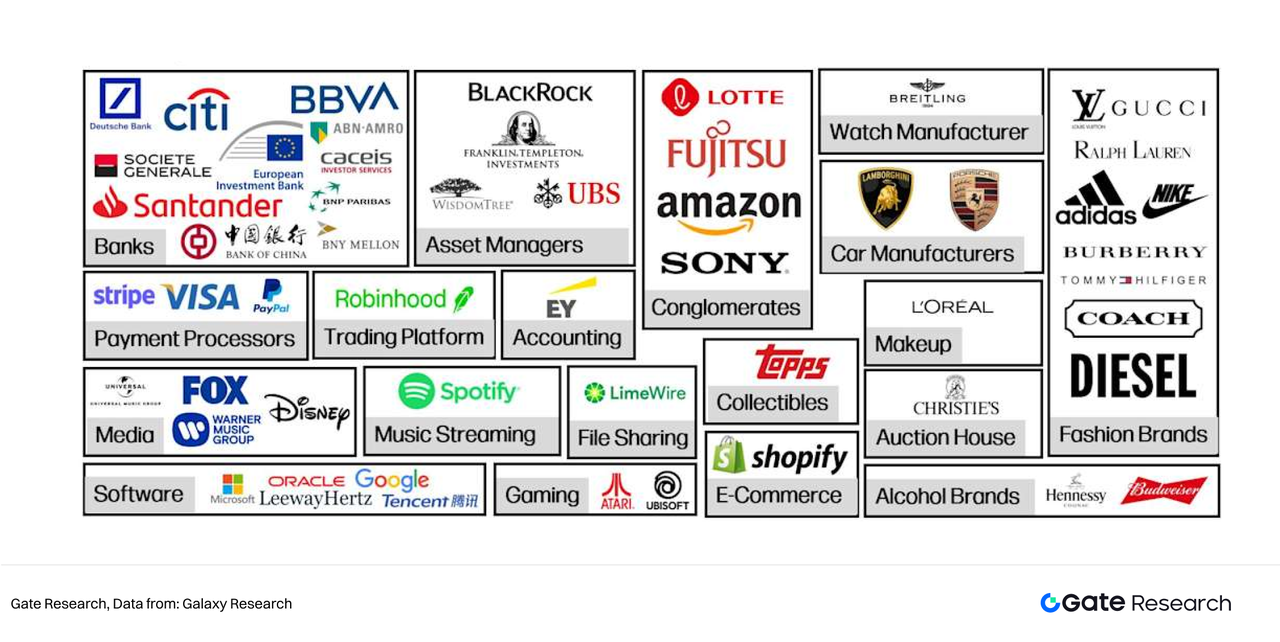

In addition, Ethereum is a highly decentralized network. Its founder Vitalik has always adhered to the concept of decentralization and encouraged the independent development of Layer 2. The Ethereum mainnet is only responsible for the consensus layer. Many well-known companies in non-blockchain fields around the world have joined the team to develop Ethereum Layer 2 [12].

Figure 6: Non-blockchain companies developing Ethereum Layer2

Finally, as ETH hoarders, listed companies have a large amount of spot ETH holdings and have a unique advantage in building staking, lending, payment and other applications on Layer2.

2. Viewing listed companies from the perspective of cryptocurrency projects

BTC is a special case in the cryptocurrency industry. The entire currency is highly decentralized. The Bitcoin Foundation has also fallen into a state of stagnation after a series of negative public opinions. Therefore, as a public chain project, BTC does not have a person with sufficient voice. In contrast, most public chain projects such as ETH, SOL, XRP, SUI, HYPE, etc. are more centralized, and the founders are all real names. At the same time, the ecological development of multiple public chain projects is controlled by their foundations. If we look at the holding of coins by listed companies from the perspective of the project party, we will make more considerations in terms of economic systems and strategic cooperation.

2.1 Coin hoarders are stabilizers that maintain the public chain ecosystem

For cryptocurrency project owners, coin hoarders are important currency stabilizers. Since coin hoarders only buy and do not sell, they can effectively reduce the volatility of cryptocurrency. Cryptocurrency is a highly volatile asset. In a bull market cycle, the market value of tokens can increase several times; but in a bear market cycle, the price of tokens falls by more than 50%, which may trigger a series of systemic risks such as the liquidation and sale of collateral assets on lending platforms.

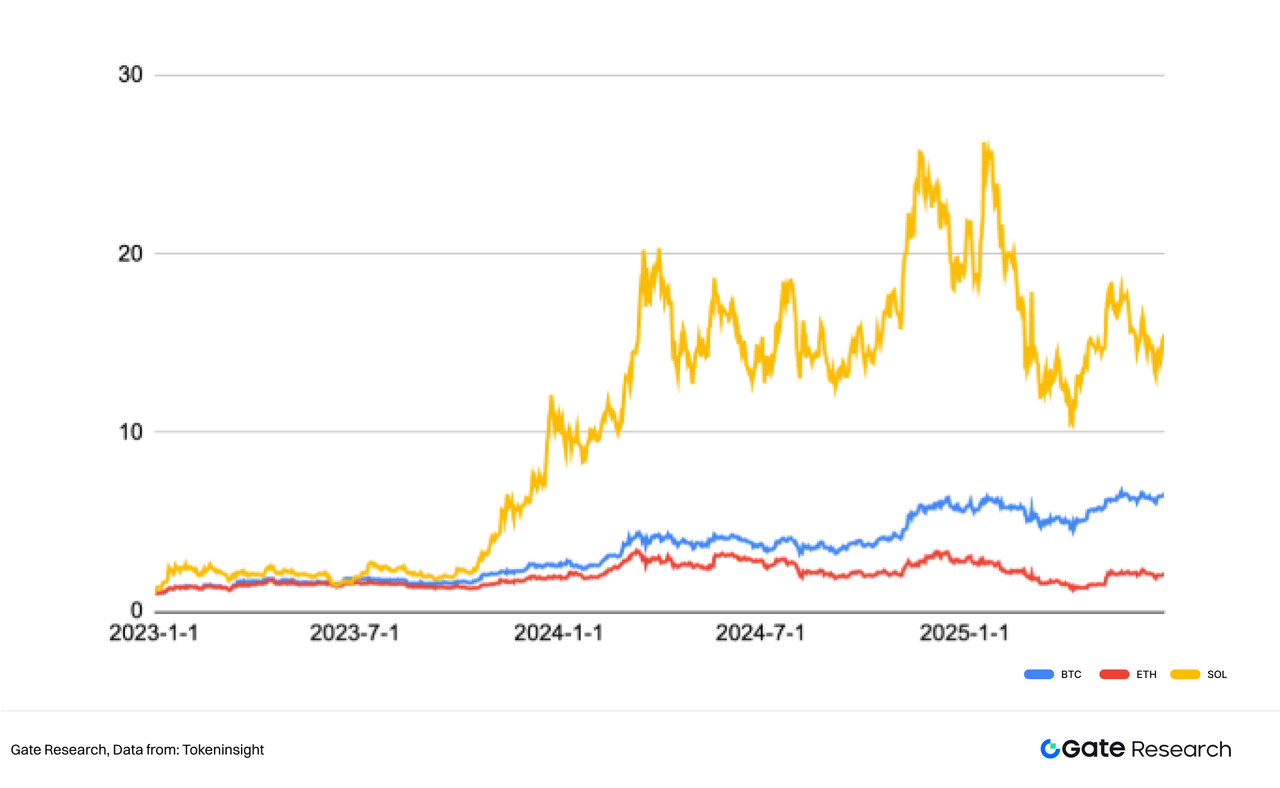

After Strategy continued to buy BTC, the volatility of BTC has significantly decreased in the past two years. In the first quarter of 2023, Strategy held more than 140,000 BTC. Until the second quarter of 2025, BTC experienced multiple rounds of corrections in the overall upward trend. The deepest correction occurred from January to April 2025, when the BTC price fell from US$109,000 to US$76,000, a correction of nearly 30%. In horizontal comparison, during the bull market from 2020 to 2021, the maximum correction of BTC was from US$63,500 to US$33,400, a correction of more than 47%. In vertical comparison, from January to April 2025, the maximum corrections of ETH and SOL reached 55% and 60% respectively. Although there are many reasons for the increased stability of BTC in this round of market, the firm holding of coin hoarders is an important factor [13].

Figure 7: Price trends of BTC, ETH, and SOL since 2023 (after normalization)

2.2 Cryptocurrency project owners are against listed companies

Listed companies buying cryptocurrencies has become an important way to boost stock prices, but there are very few cases of public chain project parties buying back listed company stocks. The core reason is that listed companies have sufficient funds and are centralized enough to implement a hoarding strategy; while most cryptocurrency project parties do not have sufficient funds. Even though the stock tokens supported by Xstocks have been launched on multiple public chains such as Ethereum, Solana, and Tron, the project team does not have enough decision-making power and motivation to buy back the stock assets of listed companies. Compared with the size of industrial companies aggregated in stock exchanges, the cryptocurrency industry is still a relatively small emerging industry.

Therefore, in the narrative of listed companies hoarding coins and cryptocurrency project parties, cryptocurrency project parties are the weaker party, and they cannot reversely choose which companies to be hoarders. But if we give cryptocurrency project parties the right to choose suitable listed companies as hoarders and strategic partners, we may be able to achieve the effect of 1+1>2.

2.2.1 Insurance companies/holding platforms are suitable for hoarding coins on PoW public chains

At present, the more representative PoW public chains include Bitcoin, Litecoin, Kaspa, etc. Unlike the PoS public chain that gives tokens more staking dividend mechanisms, the tokens of the PoW public chain are generated by mining with professional mining machines. If the PoS public chain is understood as a pipeline for transactions, the PoW public chain can be understood as a resource-rich mine. Therefore, the tokens of the PoW public chain cannot cover the financial expenses generated by the bond financing of listed companies through the sharing of gas fees. BTC, LTC, and KAS have strong hard currency attributes.

Due to the asset attributes of PoW public chain tokens, this type of asset is actually suitable for listed companies with stable cash flow, which can be purchased as assets for value preservation and appreciation. Companies with loss-making main businesses such as Strategy need very strong financing capabilities to hold BTC. Strategy has obtained convertible bond financing of more than $1 billion at 0 interest in the secondary market many times. Its strong capital market channels and connections are unmatched by many listed companies. At present, some companies are buying BTC by borrowing money, and the increase in their financial expenses in the future cannot be ignored.

For insurance and financial holding platforms, long-term holding of BTC, LTC, and KAS as a coin hoarder is obviously a more appropriate choice. For insurance companies, the cost of absorbing funds for annuity insurance is very low, which is why Warren Buffett, the stock god, once regarded insurance companies as one of his favorite business models. Since the insured will not receive dividends until many years later, the current annualized rate of return of mainstream annuity insurance is 5-10%. Insurance companies often establish a complex long-term investment portfolio to achieve the promised rate of return through a comprehensive configuration of risky assets + corporate bonds. Since PoW tokens such as BTC have designed a mechanism for the continuous halving of mining rewards, assets will only become increasingly scarce in the long run. By extending the holding period to 10-15 years, the token will experience at least two halvings, covering 10%+ It is not difficult to achieve an annualized rate of return.

In terms of holding platforms, high dividend rates are the biggest feature of such companies, but their price-earnings ratios are often only 3 to 10 times. Holding platforms refer to holding companies of multiple companies in different sectors. Representative ones in China include Fosun International, CITIC Group, Ping An of China, etc. Such companies do not need to raise debt financing, and they already have generous profit dividends from their subsidiaries. Such companies can use their annual profits to purchase BTC or LTC, which can not only increase the valuation of the company, but also do not need to pay high financing costs. From this, it can be inferred that some companies with low valuations but stable cash flow, such as construction, steel, water conservancy, and gas companies, are also more suitable to join the ranks of coin hoarders in terms of profit model.

For the governance of BTC, LTC, and KAS communities, listed companies with stable cash flows can become coin hoarders, which can ensure to the greatest extent that tokens will not be sold off in large quantities due to losses of listed companies. Cooperation with such listed companies can ensure the stability of the token economic system, and the ecology has stronger sustainable development capabilities.

2.2.2 Internet/cloud computing companies are suitable for hoarding coins on PoS public chains

Different from the cash flow requirements of PoW, the analysis in Chapter 1 shows that the requirements for hoarders of PoS public chain tokens are theoretically much lower than those of PoW public chain. SOL’s annualized staking yield (APY) can already fully cover the financing costs of issuing additional bonds, and ETH’s current annualized staking yield (APY) can also cover most of the financing costs.

Even if the staking income can cover the financing cost, it is still difficult for companies in traditional industries to build their own blockchain nodes. Large Internet companies have more idle servers, and the company has a certain technical foundation in hardware configuration, which is more suitable for hoarders to build their own nodes. Cloud computing companies, especially IaaS (Infrastructure as a Service), are more suitable for hoarders to build their own nodes. Because these companies are handy in setting up servers, and due to long-term operating experience, they can greatly reduce the probability of node downtime. For public chain foundations and cloud computing vendors, the effect of 1+1 greater than 2 can be achieved. In addition, cloud computing companies have stronger server performance and are more likely to achieve excess returns in MEV.

From the perspective of the project operators of ETH, SOL, and SUI, cloud vendors and Internet companies can empower public chains through their long-term experience in operating large computer rooms, and are ideal partners.

2.2.3 Software security companies are suitable for hoarding coins for Infra projects

Infrastructure is one of the most important concepts in the crypto industry. In fact, the public chain is the most important infrastructure in cryptocurrency, but the public chain is already an independent concept. Therefore, Infra mainly refers to oracles, cross-chain bridges, DID (decentralized identity) and DA (data execution layer) in non-public chain tracks.

In recent years, blockchain infrastructure projects have experienced many security incidents, including hackers exploiting vulnerabilities in cross-chain bridges to steal users' cross-chain funds; and oracle smart contracts being tampered with, resulting in serious deviations between on-chain and off-chain data. Therefore, the services provided by security companies are urgently needed by decentralized projects.

Compared with listed companies purchasing BTC and other PoW tokens as a means of market value management, and listed companies purchasing ETH or SOL to complete market value management and interest payments at the same time, security companies as hoarders of Infra projects are more of a commercial cooperation. First of all, as cryptocurrencies gradually become compliant and recognized by more people, their overall development ceiling is constantly rising. Therefore, the scale of the crypto security market has also expanded. Security companies need to expand this new market more. And project parties are generally willing to pay security companies with their tokens as compensation for their services. Listed companies can act as hoarders, which can not only preserve the value of the tokens they hold, but also participate more deeply in the crypto Infra project.

3. Conclusion: Thoughts on decentralization

The debate over "centralization" and "decentralization" in the cryptocurrency field has been going on since the birth of blockchain. Decentralization is the utopian vision proposed by Satoshi Nakamoto in the Bitcoin White Paper, which aims to empower individuals with sovereignty through distributed ledger technology and get rid of the centralized control of traditional finance. However, decentralization in practice often faces the challenges of inefficiency and coordination difficulties. Bitcoin is a benchmark for decentralization. Its founder Satoshi Nakamoto went into hiding after releasing the genesis block in 2009, leaving behind a decentralized ecosystem. According to Bitcoin Treasuries data, as of July 2025, the largest holders of BTC are iShares Bitcoin Trust (IBIT, 696,874 BTC), Binance (606,080 BTC) and Strategy (597,325 BTC), accounting for 3.3%, 2.9% and 2.8% of the total supply, respectively. Although the market value of BTC accounts for 54% of the total market value of cryptocurrencies, the number of single holders does not exceed 3.5%, showing its highly decentralized nature [14][15].

However, the role of Michael Saylor, founder of Strategy, is thought-provoking. He has continuously strengthened the decentralized consensus of BTC through public speeches and media interviews, and some people regard him as the "unofficial spokesperson" of BTC. In recent years, Strategy has repeatedly purchased BTC by issuing zero-interest convertible bonds, and may become the "quasi-center" of the BTC ecosystem in the future.

Compared with the decentralization of BTC, most public chains have "single-center" or "multi-center" characteristics.

Ethereum (ETH) is a classic example of decentralization. The Ethereum Foundation, represented by Vitalik, promotes technological upgrades (such as the merger in 2022), while Lido Finance (led by Lomashuk) controls about 32% of ETH staked through the staking platform. The two have similar interests in promoting ecological development, but they also have differences on proposals such as EIP-4844. If a listed company enters the Ethereum ecosystem by hoarding coins, once the ETH holding exceeds 3%, it may become the "third pole" to balance the game between the foundation and the staking platform. Nobel Prize winner in Economics Ostrom proposed in "The Governance of Public Affairs" (1990) that a decentralized governance structure can enhance system resilience through checks and balances. The participation of listed companies may verify this theory and bring new stability to Ethereum.

Compared with Ethereum, some public chains represented by Solana are more inclined to "single-centralization". Solana Labs and the Foundation lead the development of the ecosystem and support DeFi, GameFi and Meme projects. For single-centralized projects, it will be more difficult for listed companies to play a bigger role in the ecosystem by hoarding coins. The strategic cooperation between the two parties will be based on the needs of each other. Single-centralized public chains, where transaction volume and active accounts continue to decline, need listed companies as strategic partners to activate the popularity of public chains through funding and developer empowerment. Centralized public chains echo the strong central authority advocated by Hobbes in Leviathan: an influential entity may bring stability in disorder, but it may also undermine the original intention of decentralization.

Throughout history, "mono-centralization", "multi-centralization" and "decentralization" all have their representative works and clear supporting arguments. Hobbes's book "Leviathan" is a supporter of mono-centralization, advocating a strong central government to maintain social order. Ostrom's "Political Theory and Public Policy" emphasizes the prevention of power monopoly through checks and balances. Davidson's book "Sovereign Individual" predicts that digital technology will continue to advance and individuals will gain sovereignty through encrypted networks. In the future blockchain world, the three routes will still run in parallel. The governance structure of the project is constantly changing. Mono-central projects may gradually move towards multi-centers, and multi-center projects may also move towards decentralization. Listed companies and project parties need to clarify each other's roles in the ecosystem and do a good job of expectation management to establish a long-term win-win cooperation mechanism.

4. References

1. Yahoo, https://finance.yahoo.com/quote/CYFRF/

2. Staking Reward, https://www.stakingrewards.com/

3. Coinmarketcap, https://coinmarketcap.com/

4. Coinmarketcap, https://coinmarketcap.com/currencies/celestia/

5. Artemis, https://app.artemisanalytics.com/home

6. Jito, https://www.jito.network/staking/

7. Helius, https://www.helius.dev/validator

8. Tokeninsight, https://tokeninsight.com/en/cryptocurrencies

9. StakedHype, https://www.stakedhype.fi/stake

10. Coingecko, https://www.coingecko.com/en/chains

11. Caldera, https://caldera.xyz/rollups

12. Blockworks, https://blockworks.co/news/non-crypto-native-companies-ethereum

13. Tokeninsight, https://tokeninsight.com/en/cryptocurrencies

14. Bitcoin Treasures, https://bitbo.io/treasuries/microstrategy/

15. Binance, https://www.binance.com/zh-CN/proof-of-reserves

Disclaimer

Investing in the cryptocurrency market involves high risks and users are advised to conduct independent research and fully understand the nature of the assets and products purchased before making any investment decisions. Gate is not responsible for any losses or damages resulting from such investment decisions.