Author: Frank, PANews

On February 11, Arweave, a long-established decentralized storage protocol, launched the decentralized computing platform AO and issued an official announcement, stating that the first mainnet token minting has been completed and new token minting will be carried out at 18:20 Eastern Time every day. Unlike Story and Solayer, which were airdropped at the same time, the release of AO did not seem to cause much waves on social media. From a vision point of view, AO is closely related to the hottest AI topic at the moment, and Arweave, as a mature decentralized storage infrastructure, can provide a lot of support on the underlying network.

Arweave and AO, former stars that should have sparked discussion, have “fallen silent” due to the decline of the ecosystem, or are they just another gem being ignored by the market?

Low expectations for airdrops lead to low market enthusiasm

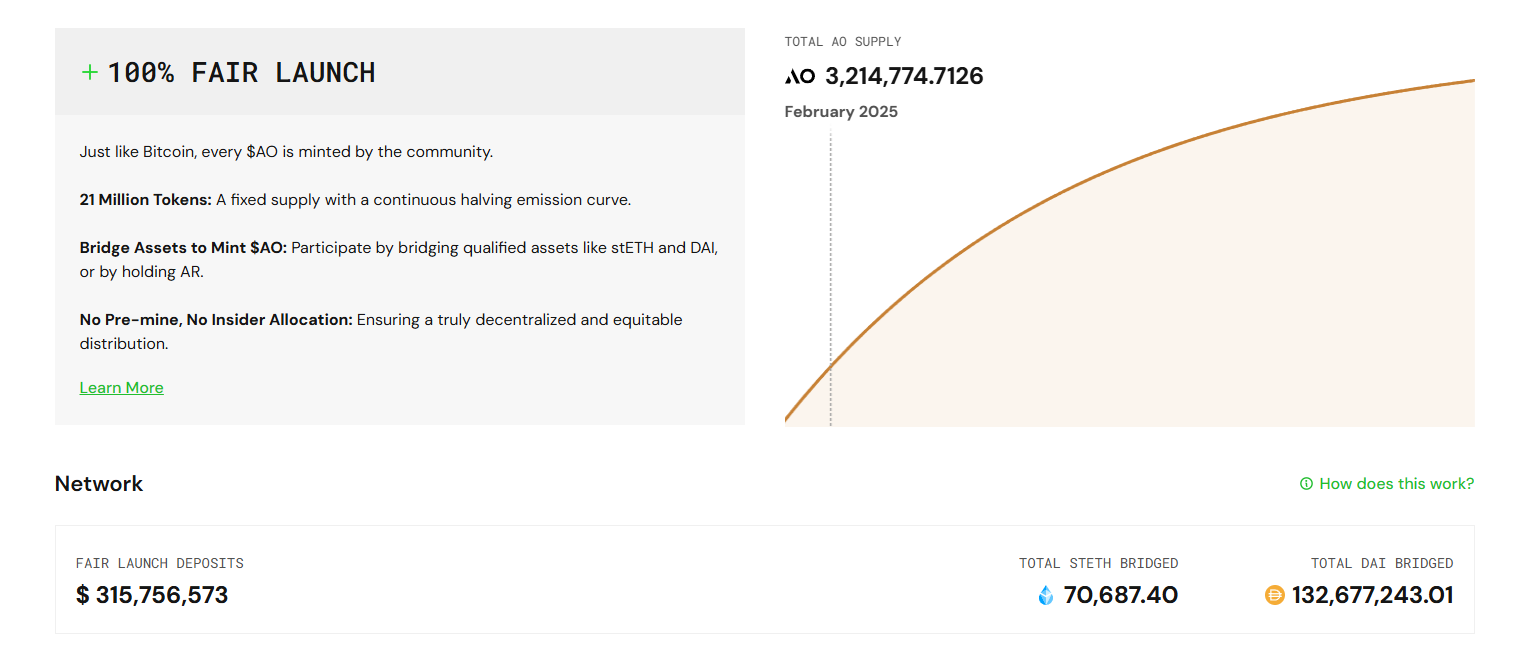

The first reason why AO was ignored may be that the token issuance did not bring much expectation to the market. According to the official introduction, the total issuance of AO tokens is 21 million, and a halving mechanism similar to Bitcoin is adopted. In the early reward distribution, 36% is allocated to AR holders, and 64% is used to incentivize cross-chain asset bridging (such as DAI, stETH). Data on February 12 showed that 3.214 million AO tokens have been minted.

As of February 11, 2025, the circulation of AR is 65.65 million. Calculated at this ratio, the current issuance ratio of AR to AO is 20.78:1. The exchanges that have launched pre-market trading include LBank and MEXC, but there is a huge gap in the pre-market prices of the two exchanges. The pre-market price of LBANK is about US$92, while the price of MEXC is only about US$35, a difference of more than 1 times. However, in terms of trading volume, LBANK's 24-hour pre-market trading volume is US$1.97 million, which is higher than the trading volume of MEXC. Therefore, the price of LBANK may be more in line with market expectations. Calculated at the current higher pre-market price of US$92, the circulating market value of AO is approximately US$290 million.

According to previous official information, on average, each AR token holder may receive 0.016 AO tokens. Based on the pre-market price of $92, AR holders can get AO worth about $14.72 each in these months. This share has exceeded the value of a single AR. However, if we take into account the decline of AR in the past six months, from the highest point of $49.55 in May 2024 to $9.52 on February 11, the decline is more than 80%. During this period, users who hold coins need to expect the opening price of AO to rise to around $500 to make up for the decline.

As of February 11, the total number of AR holding addresses was 211,000. Based on this calculation, each address can get about 4.44 AO, worth $409 (but this data is only an estimate, and the specific value must comply with the airdrop rules). According to current official data, the top 100 AO holding addresses hold a total of 2.21 million tokens, accounting for about 70%, and the chips of large holders are relatively concentrated. From the overall scale of the airdrop, if the pre-market price of $92 is maintained, the scale can reach $290 million. If the price is only around $35, the scale of the airdrop will be as small as $110 million. Considering the sharp drop in the AR token, it is indeed difficult to arouse the enthusiasm of the market.

Network activity has indeed increased, but remains at a relatively low level overall

In fact, the overall activity of the Arweave network has never been high. Taking February 11 as an example, the daily active addresses of Arweave on that day were 3,366, but this data level is actually a relatively active stage compared with historical data. Before 2023, its daily active network basically maintained at around 1,000, and in 2024, the daily active data increased to 2,000. After entering 2025, perhaps due to the expectation of AO's airdrop, the daily active data generally reached more than 3,000, and the highest one day reached more than 5,000.

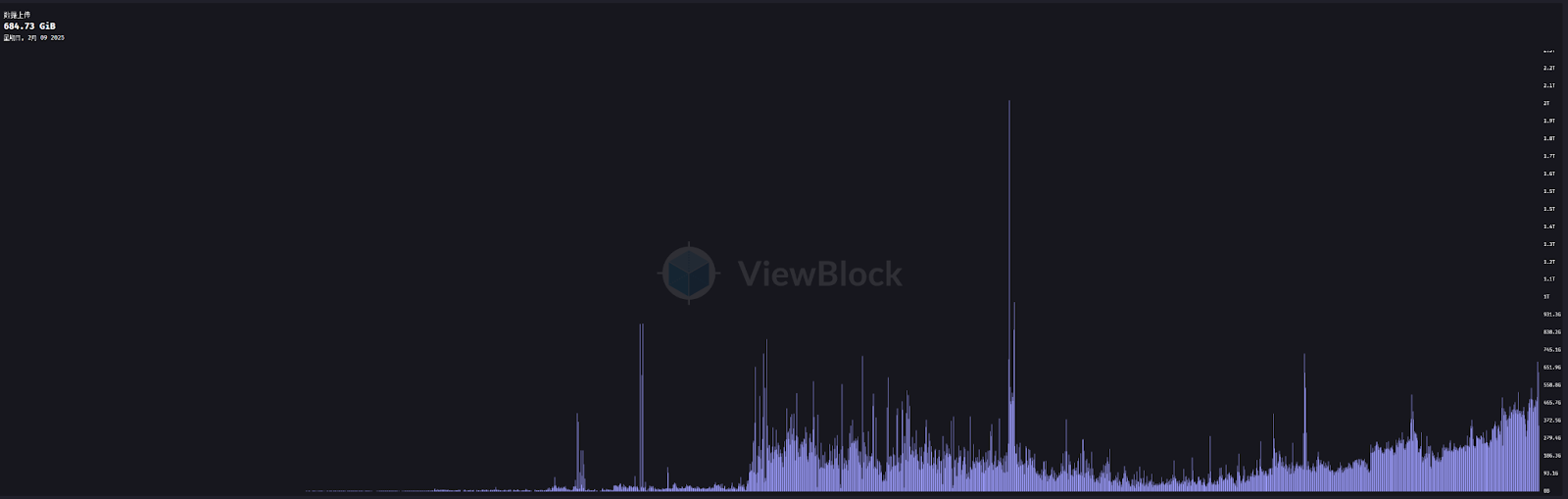

In addition, as a decentralized storage network, data upload volume may be one of the most important indicators of activity. On-chain data shows that Arweave's daily data upload volume has continued to grow since the end of 2023. The average daily data volume of more than 100GB has risen to more than 400. Although the highest point is still lower than the single-day peak of 2.02TB created in 2022, the overall upload volume does show a steady upward trend.

Judging from the activity of the network, ArDrive is the most active application in the Arweave network. About 90% of the daily data uploads are uploaded by ArDrive. ArDrive is a permanent storage application in the Arweave network that allows users to permanently save their files and is completely uncensored. In 2022, ArDrive completed a $17.2 million seed round of financing. In addition to ArDrive, another ecological project Irys contributed about 10% of the uploads.

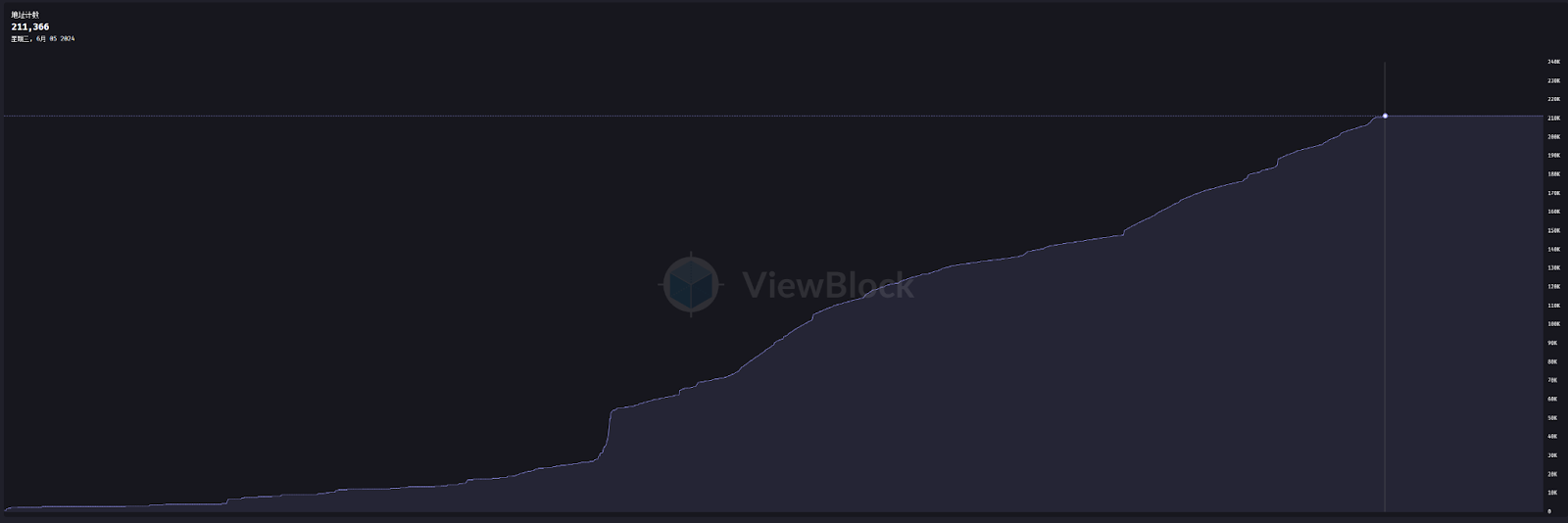

In addition, there is a strange data phenomenon in the Arweave ecosystem. Since June 1, 2024, the total number of Arweave addresses has not increased and has been fixed at 211,366. I don’t know whether the user growth of the ecosystem has completely stagnated or there is a problem with the browser’s data maintenance. However, just like AO’s lukewarm popularity, these detailed bugs are not discussed.

The AO ecosystem is still in its early stages

According to official data, the current TVL of the AO network is about 315 million US dollars. Compared with the 700 million US dollars in the test network stage, it has actually declined a lot. From this point of view, it seems that users are not very enthusiastic about the subsequent staking token incentives of the AO network.

From the perspective of ecological projects, several related ecological projects are still in the early stages of development. For example, AOX, the main cross-chain bridge in the AO network, announced on February 11 that its transaction volume exceeded 8 million US dollars and its TVL exceeded 3 million US dollars. Another ecological project, FusionFi, announced that its settlement amount exceeded 10 million US dollars.

Judging from the interaction on social media, some of the following projects are already running in the AO ecosystem.

Marketverse AI: AI Agent Project

StarGrid Battle Tactics: Game on Chain

Decent.land: EVM virtual machine

AOX: A cross-chain bridge

FusionFi Protocol: AgentFi

Permaswap: DEX

Astro Labs: Liquidity Provider and Stablecoin USDA Issuance

RedStone Oracles: Oracle Project

In general, the AO network is still a new generation product. There is no dedicated browser, no official ecological map, and the publicity has not yet clearly announced when AO will start formal trading. Even after a year of test network stage, the current ecological status seems to be still in the rough state. Therefore, the public may not know where to start with the expectations of AO.

From another perspective, perhaps AO’s innovative ideas at the technical level were the main reason for the market’s previous expectations. However, judging from the results of the mainnet launch, it is more like a test paper that has only completed the first half, and only partially explained the issue of the token mechanism. The core narrative of its claimed AI potential and performance upgrades through permanent storage has not yet produced actual results. For AO, the key to success lies in whether it can transform the technical narrative into practical applications, rather than relying solely on token incentives.