Author: TechFlow

Do you think alt season is coming? This question has become a popular topic on crypto Twitter.

The current mainstream view is that the overall altcoin season is still a long way off, most altcoins lack liquidity, and investors will turn their attention to US stocks, Bitcoin and RWA (stablecoin).

When everyone thought that the altcoin season would not come, some altcoins were rising against the trend.

For example, Maple Finance’s token SYRUP has risen by 400% since the beginning of this year and has reached ATH as of press time.

Grayscale has previously added Maple Finance to the list of TOP20 tokens worth paying attention to in Q2 2025, but there is still little analysis of this project in the Chinese region.

Amidst more information noise, we seem to have forgotten a clear main line in this version that is not directly relevant to most people - the entry of institutions.

Crypto products that serve individuals, such as Launchpad and Meme, are emerging one after another, but competition is gradually involuted, and the lack of liquidity in the circle is also lowering their base;

Service agencies are another way. The product is not so intuitive and requires more thresholds, but it is an opportunity that is more easily overlooked in the current version of institutional entry.

Maple Finance has obviously benefited from the new version.

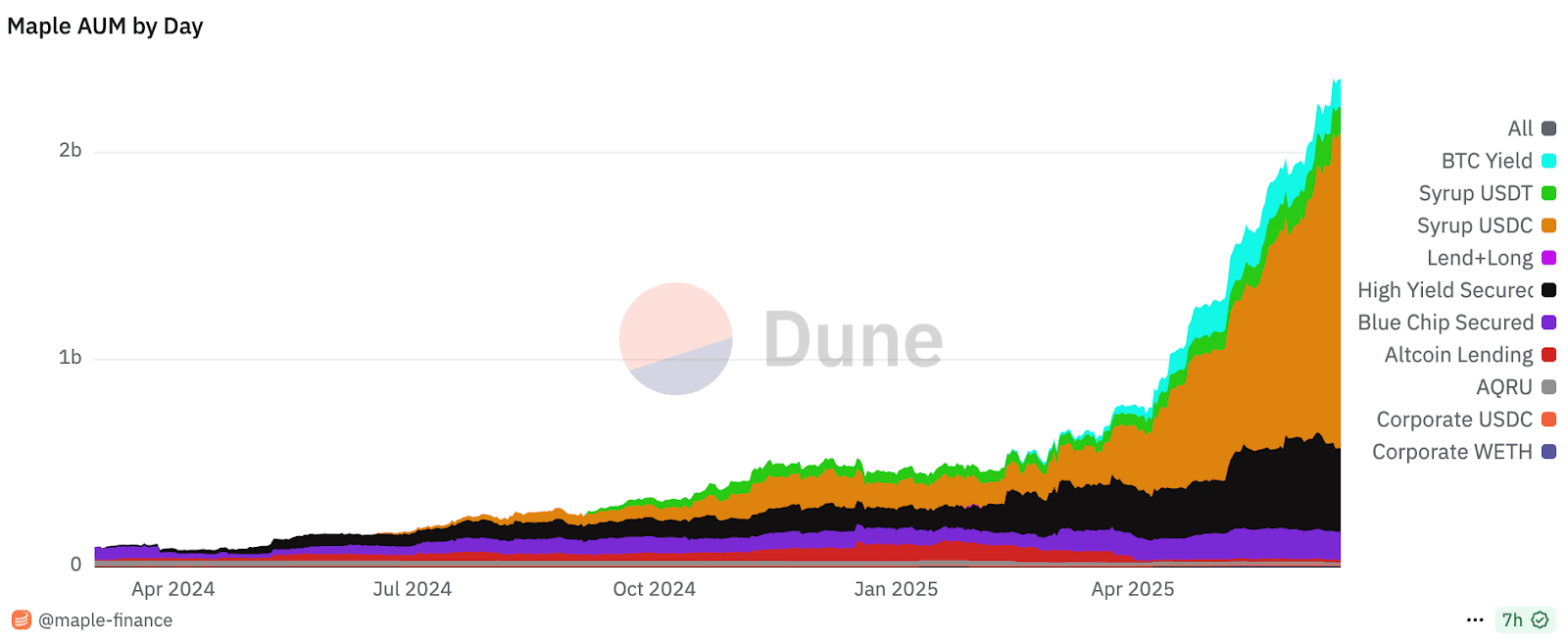

The project focuses on providing institutions with low-collateralized loans and RWA investments, such as tokenized U.S. Treasuries and trade receivables pools, with its assets under management (AUM) exceeding US$2 billion in June 2025, serving traditional hedge funds, DAOs and crypto trading firms.

SYRUP's counter-trend rise may have reflected the market's rediscovery of Maple's undervalued value.

The current market value of the token is about 700 million US dollars. Compared with some memes in the previous version that were purely driven by emotions and had a market value of 1 billion, do you think SYRUP is overvalued or undervalued?

Of course, products from different tracks cannot be compared solely based on market capitalization. We also need to know more about Maple Finance’s business.

Provide on-chain lending services for institutions

Maple Finance is a multi-chain DeFi platform (running on Ethereum, Solana, and Base) that specializes in providing on-chain lending and investing services to institutional clients such as hedge funds, DAOs (decentralized autonomous organizations), and crypto trading firms.

Simply put, you can understand it as an asset management tool that helps these large institutions borrow money, manage funds or invest on the chain, avoiding the complex processes and low returns of traditional banks.

Since its founding in 2019, Maple has grown into a mature platform with $2.4 billion in assets under management (AUM) and $1.8 billion in total value locked (TVL) in June 2025.

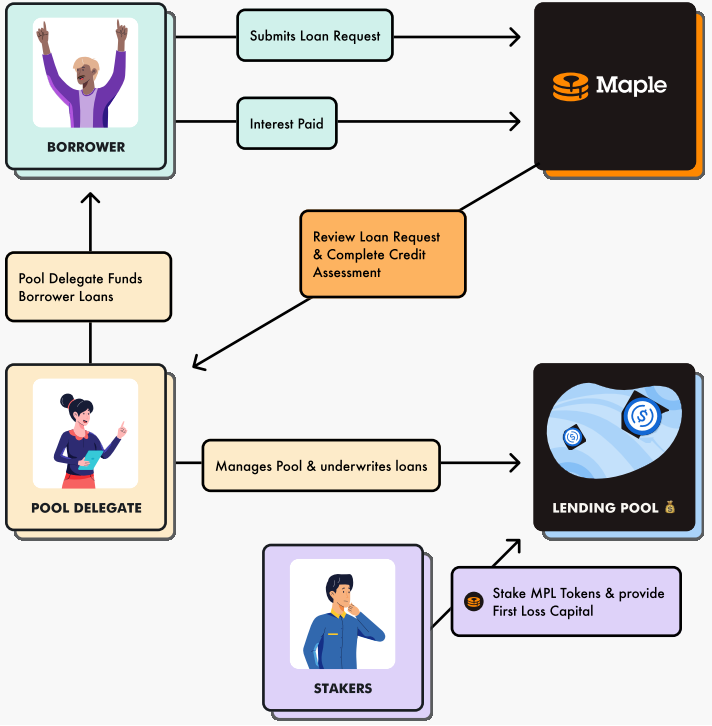

Although it is mainly aimed at institutional users, the roles involved in Maple Finance are divided into different roles. You can choose to lend, pledge, borrow and/or become a principal of a lending pool.

(Image source: consensys)

Borrowers are institutions that need funds, such as crypto trading companies, which use digital assets such as Bitcoin (BTC) or Ethereum (ETH) as collateral to borrow stablecoin USDC; these institutions often need to obtain liquidity quickly, but the approval process of the traditional financial system is too lengthy to meet their needs.

Lenders provide liquidity, such as depositing USDC or ETH, and earn interest; they are also common LPs in DeFi products. For LPs, Maple's appeal lies in its high annualized rate of return (APY) and transparent fund management mechanism.

Pool principals are professional teams responsible for assessing borrowers’ credit and ensuring loan safety. To reduce LP risk, Maple allows pool principals to conduct strict screening of borrowers and monitor loan performance in real time.

Stakers hold SYRUP tokens and stake them to share risk and rewards. If the loan defaults, their SYRUP can be used to cover the loss, while also receiving additional rewards from the platform when no problems occur.

Therefore, a simple process can be: the borrower makes a loan request, the pool principal reviews the qualifications, the lender provides funds, the pledger provides guarantees, the smart contract automatically executes lending and repayment, and the proceeds are distributed according to the above different role positioning.

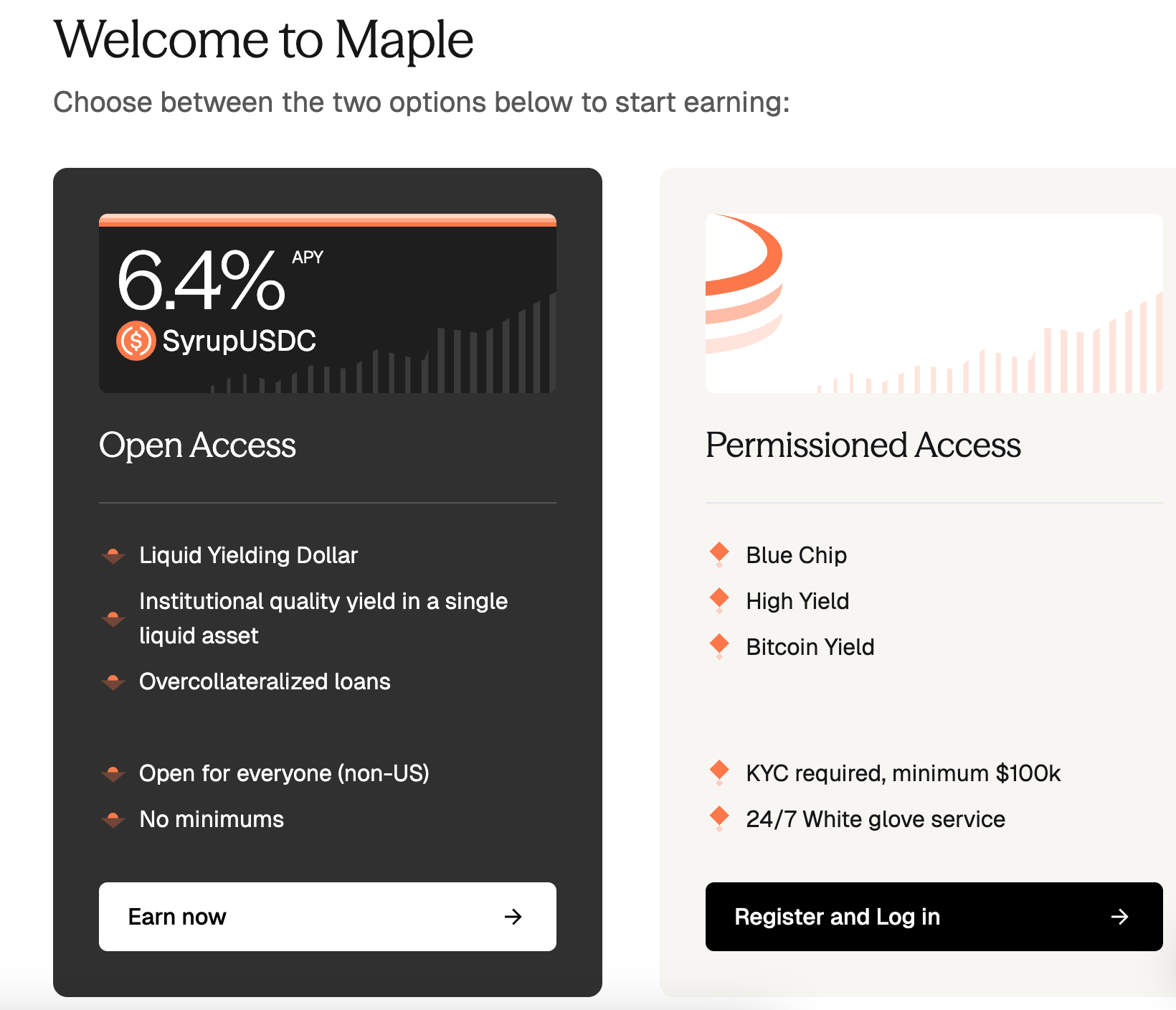

In terms of lending products, Maple is divided into two categories: "open access" and "licensed access".

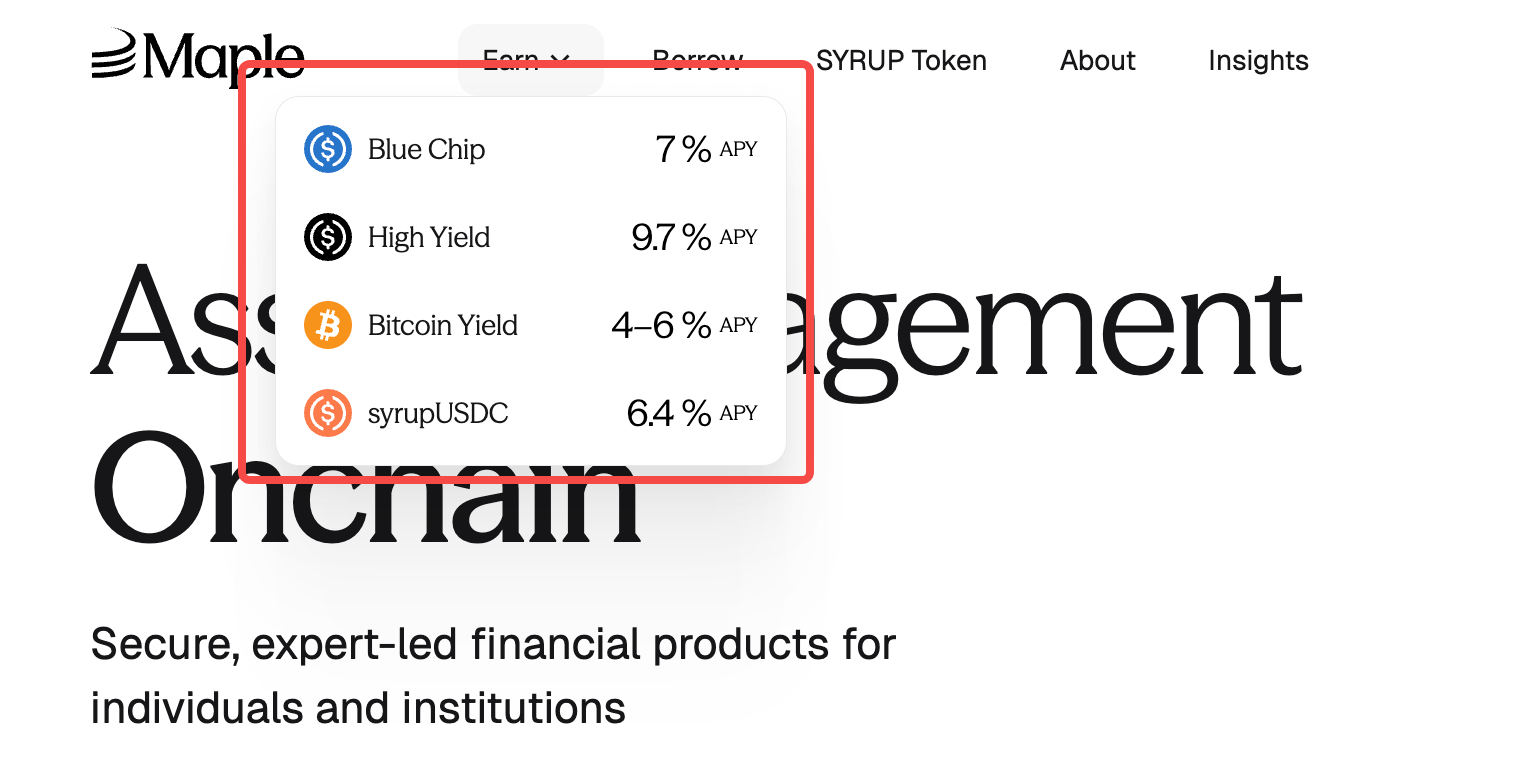

Open access includes SyrupUSDC, which offers an annualized yield of 6.4% (APY), suitable for individual and small institutional investors. SyrupUSDC is a yield product based on USDC, where funds enter the liquidity pool and invest in overcollateralized loans (borrowers need to provide assets exceeding 50% of the loan value), with no minimum amount and emphasis on liquidity and stability.

Licensed access is for institutional clients, including Blue Chip (7% APY), High Yield (9.7% APY) and Bitcoin Yield (4-6% APY). KYC certification is required, with a minimum investment of US$100,000 and 24/7 white glove service.

The white glove service here is a high-end customized support, similar to the exclusive consultant of a private bank. Institutional clients can enjoy one-on-one assistance around the clock, including loan plan design, fund management advice and emergency problem solving.

Blue Chip invests in high credit rating loans, similar to traditional "blue chip stocks" with low risk; High Yield focuses on high-risk and high-return loan portfolios; Bitcoin Yield uses BTC collateral to allow holders to earn passive income.

From DeFi crisis to 2 billion asset management scale

The lending mechanism is the core highlight of Maple. But the lending business did not have such a smooth journey at the beginning.

In 2022, the DeFi industry encountered a "black storm": Terra collapsed and Three Arrows Capital went bankrupt, causing many DeFi platforms to fall into a liquidity crisis, and Maple was no exception.

In the early days, Maple adopted a partial collateral model, that is, no full collateral amount was required when applying for a loan, and the loan was assessed only based on the reputation of the borrower. This was a high-risk model and was even more vulnerable when facing black swan events. The scale of its asset management once shrank to US$200 million. At certain specific times, its partial collateral model caused the default rate to soar to more than 5%.

Faced with the crisis, Maple made a decisive transformation and introduced over-collateralization (150% collateral ratio) and a tri-party agreement in 2023. Borrowers use BTC to mortgage USDC, and third-party institutions monitor the value of the collateral. Maple executes smart contracts. If the BTC price falls beyond the threshold, the third party triggers liquidation to protect the interests of lenders.

Changes in product design not only restored trust but also provided a safer lending environment for institutional clients.

At the beginning of this year, as the mainstream narrative of the crypto market shifted from individual speculation to institutional dominance, and more funds were seeking low-risk and risk-free returns, you can more clearly feel that Maple Finance has shown a strong recovery momentum through the following data:

Maple’s flagship product, SyrupUSDC, a yield-generating stablecoin based on USDC, has seen its total value locked grow from $166 million to $775 million in 11 months, reflecting the surge in market demand for Maple’s products.

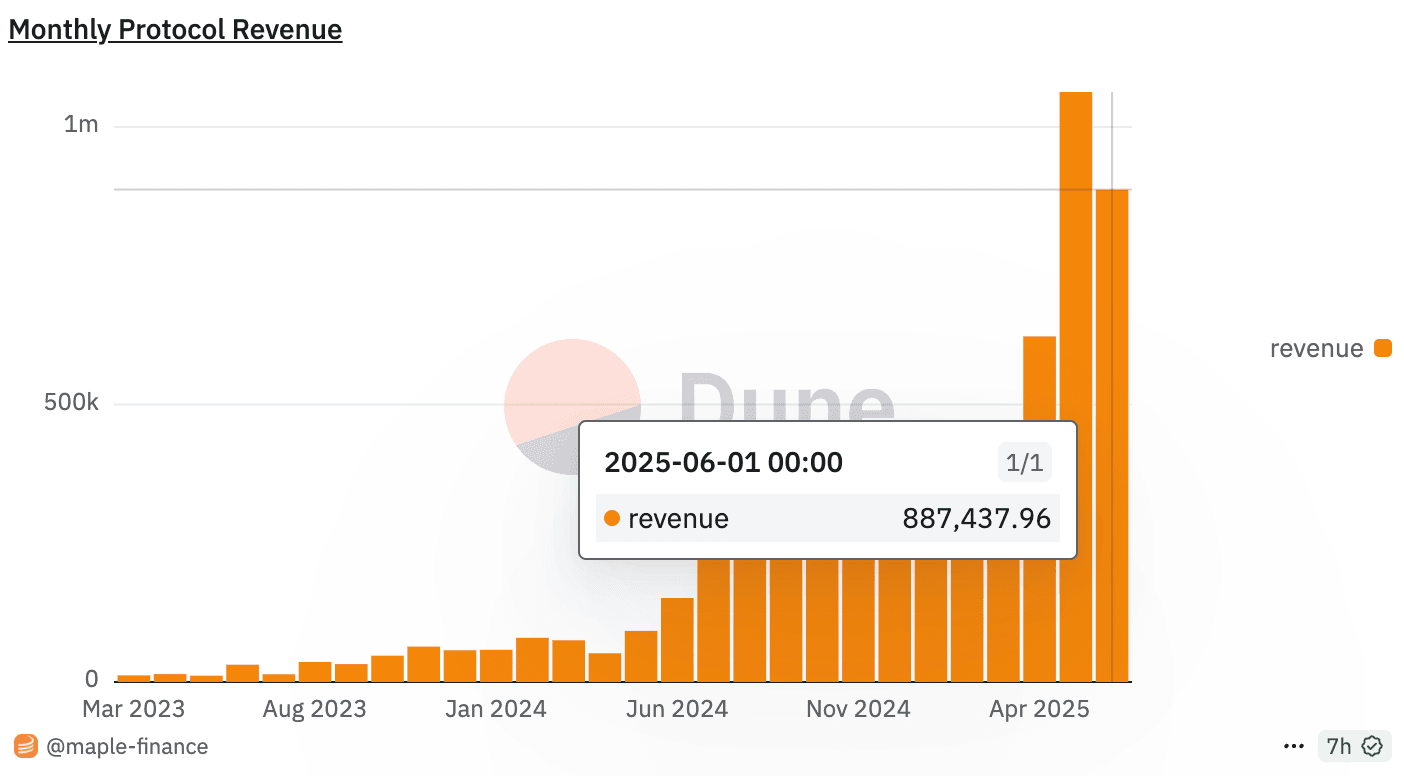

Additionally, assets under management (AUM) have surged nearly 10x since January 2025, and active loans outstanding within the protocol have increased to approximately $880 million, making Maple one of the largest crypto lenders.

At the same time, the increase in lending demand also makes it profitable. Since Maple charges a 0.5-2% handling fee for each loan, its monthly revenue exceeded US$1 million in May 2025, setting a record for revenue growth for three consecutive months.

Of these meaningful cash flows, 20% of the fees will be used to repurchase SYRUP tokens for stakers, which may also partially reveal why SYRUP tokens have risen against the trend since the beginning of this year.

In May of this year, Cantor Fitzgerald, a world-renowned financial services company, announced a $2 billion Bitcoin (BTC) loan program and selected Maple as its preferred partner.

As a long-established financial institution founded in 1945, Cantor’s business covers bond trading, real estate and financial technology, and it is a representative of traditional finance. Its joining also marks the recognition of on-chain credit by traditional giants.

Institutions often need flexible short-term financing, but traditional bank lending is inefficient, which makes Maple's customized services and more relaxed access mechanism an alternative for institutional lending.

Why can SYRUP rise when the general market falls?

Why can SYRUP rise against the trend?

The lending needs of institutions partially answer the question, but at a more micro level, SYRUP tokens are currently in a state of near full circulation, which also reduces the possibility of selling pressure to a certain extent.

If we analyze the reasons in a more structured way, "version bonus" is the simplest answer to this question. Specifically, this bonus can be broken down into:

Safe-haven asset characteristics:

When the crypto market falls, investors tend to choose low-risk, high-yield assets. Maple's RWA products (such as Treasury pools) and overcollateralized loans provide stable returns (5-20% APY), making them ideal safe-haven assets.

The Bitcoin Yield product provides BTC holders with a way to earn returns without having to sell their assets, attracting a large amount of institutional funds.

Direct beneficiaries of RWA narrative:

The increased interest of traditional financial institutions in blockchain (such as BlackRock's BUIDL and JPMorgan's digital bonds) has driven the growth of the RWA market. As the "institutional-grade loan engine" of DeFi, Maple directly benefits from this trend. The funds of institutional investors are large and stable, offsetting the emotional fluctuations of the retail market.

Differentiated competition:

Compared to retail-oriented protocols such as Aave and Compound, Maple's institutional orientation and RWA focus give it an advantage in the market segment. Although its competitors (such as BlackRock's BUIDL and Ethena) are strong, Maple's on-chain transparency and flexibility are more suitable for crypto-native institutions.

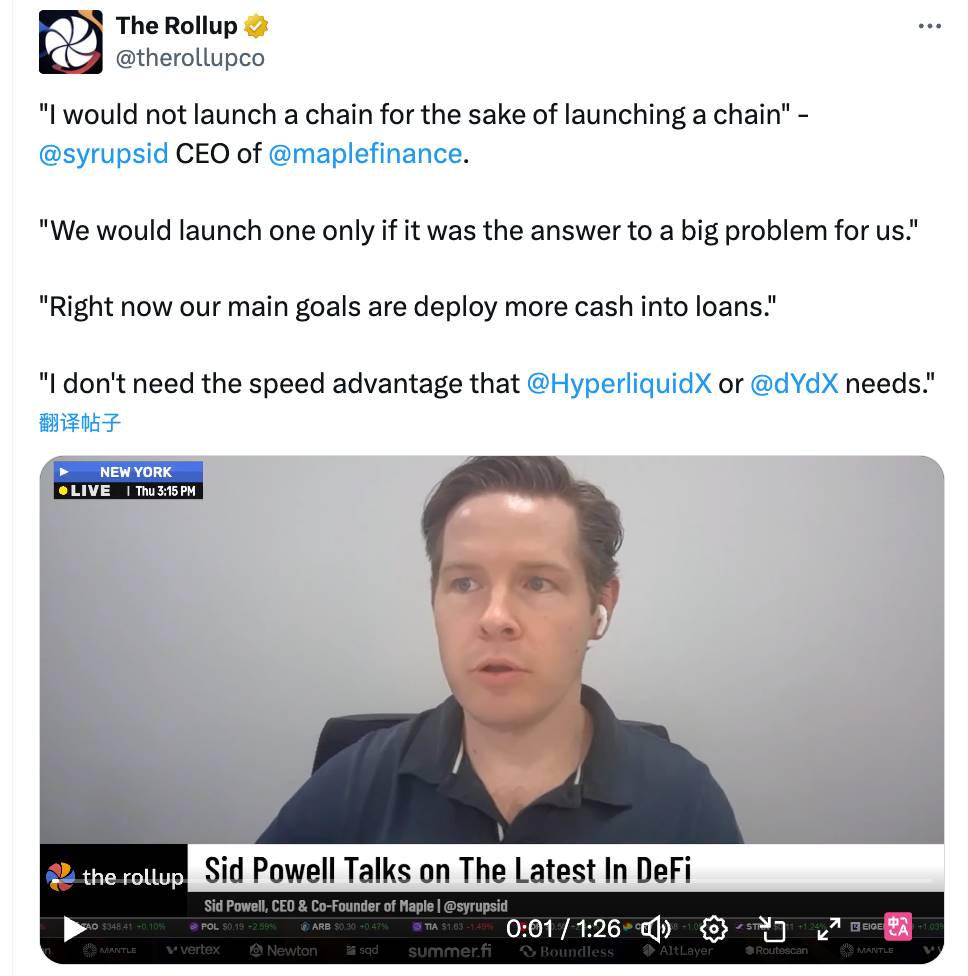

The team's product requirements positioning:

When some DeFi projects started to work on L1, infrastructure and performance, Sid Powell, the founder of Maple, revealed a view that infrastructure should not be built for the sake of infrastructure in an interview with a podcast:

“We will only launch it if it solves our big problem… Right now our main goal is to put more cash into lending, I don’t need the speed advantage of Hyperliquid and dydx.”

No FOMO

The fundamentals are solid and the price of the currency is rising. Does this make you feel FOMO?

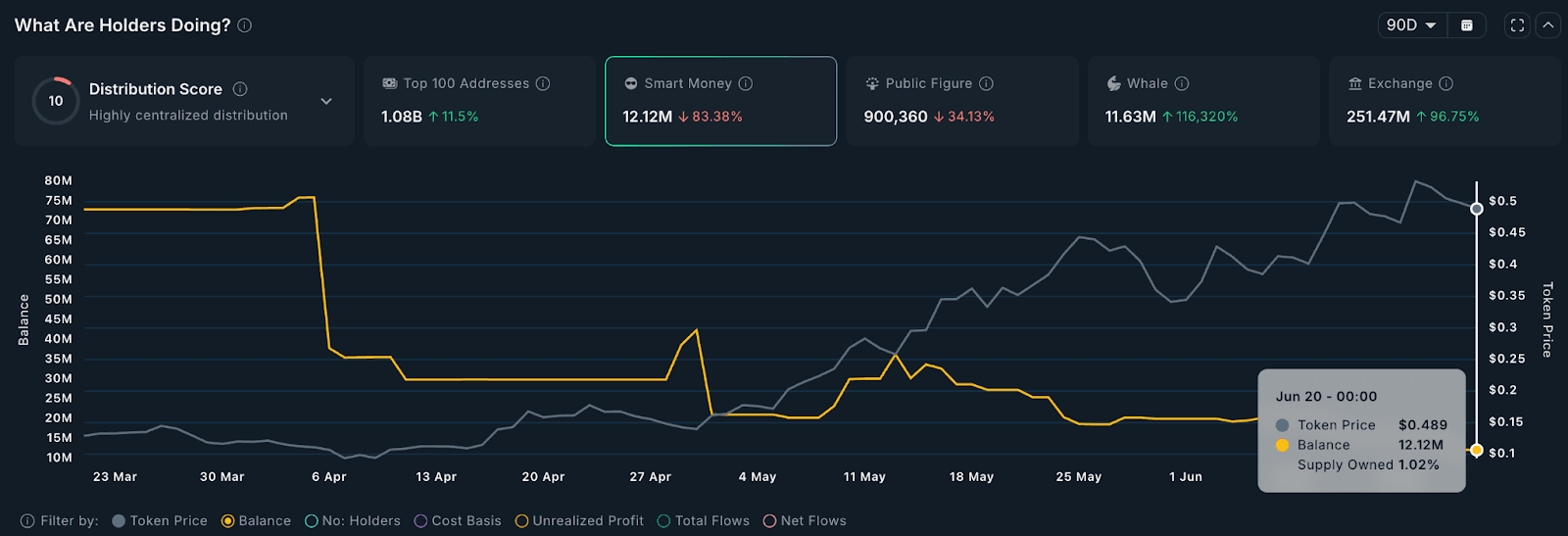

Don’t worry. There are already too many cases in the crypto market where good products do not mean continued good performance of tokens. Some movements of funds on the SYRUP chain also seem to show the exit of early profiteers.

Nansen's analysis shows that there have been signs of significant outflows from smart money and funds.

For example, Blocktower has deposited over $10.5m of SYRUP to Binance exchange wallets in the last 34 days, and Dragonfly has sent over $1.75m of SYRUP to a known FalconX wallet in the last few days. The same is true for Maven11, which sends SYRUP to an intermediary wallet and then to Binance.

On an aggregate level over the past 90 days, the amount of smart money holding SYRUP has fallen by over 83%, while exchange SYRUP balances have grown by 96%, a clear sign of an early capital withdrawal.

But at the same time, some whales are also starting to accumulate SYRUP, and whales' holdings have increased by 116,000% in the past 90 days.

Looking at these data together, the market may have reached a point of turnover and divergence, and following either side of the equation would involve investment risks.

In general, business methods that are more in line with the version give Maple greater room for growth; but at any given moment, watching more and doing less is a safer choice.