Author: TaxDAO

introduction

On April 1, 2025, the Canadian federal government announced the formal elimination of the carbon tax on fuels, a move that caused a major stir in energy, manufacturing, and cryptocurrency mining—highly energy-intensive industries. On the surface, this seemed like a relief for businesses, and many cheered this tax benefit. However, a deeper analysis reveals that Canada not only did not relax carbon restrictions, but quietly tightened controls on the industrial side, applying more precise pressure to large-scale emission facilities. For cryptocurrency mining companies, which are heavily reliant on electricity, this marks the official start of a more complex cost game.

1. Policy Changes: The "fuel carbon tax" was abolished, but carbon prices did not cool down.

To understand the real impact of this change, it's essential to review the fundamental logic of Canada's carbon pricing. Under the Canada Greenhouse Gas Pollution Pricing Act, Canada's carbon tax system comprises two core components: a federal fuel charge for end consumers and small businesses, and an output-based pricing system (OBPS) for large industrial facilities. The latter was designed to protect energy-intensive industries from direct international competition while levying carbon costs.

The elimination of the fuel carbon tax only alleviates the tax burden at the retail level, while the industrial carbon price, which has a profound impact on large energy users such as mining companies, continues to rise. According to the federal plan, the price will increase by C$15 per tonne of CO₂e annually from 2023 to 2030, with a final target of C$170 per tonne. Canada's emissions reduction strategy remains unchanged, and the rising compliance costs under the carbon tax will inevitably be passed down through energy prices.

2. Carbon prices continue to rise: inflation in energy-intensive industries

From an economic structural perspective, the real impact of industrial carbon pricing is not a simple and crude "emissions tax," but rather an efficient transmission through the electricity price chain. It's important to note that power generation companies do not pay for all their emissions. Under Canada's mainstream "Output-Based Pricing System" (OBPS), the government sets a baseline for emissions intensity, and power plants only pay carbon costs for emissions exceeding that baseline.

In Ontario, for example, the industry benchmark for natural gas power generation is set at 310 t CO₂e/GWh, while the average unit emissions are around 390 t CO₂e/GWh. This means that the actual cost payable under carbon pricing is only the difference of 80 t/GWh. However, this excess cost (at a carbon price of CAD 95/tonne) translates to approximately CAD 7.6 per megawatt-hour of electricity; if the carbon price rises to CAD 170/tonne by 2030, this figure will climb to CAD 13.6/MWh. This mechanism then propagates to downstream industries such as mining and manufacturing, especially high-energy-consuming businesses like Bitcoin mining.

It's important to note that the impact of carbon prices is not evenly distributed across Canada, depending heavily on the power mix of each province. In regions like Ontario or Alberta, which rely on natural gas as a marginal power source (i.e., a pricing power source), carbon costs are more easily incorporated into wholesale electricity prices. However, in regions dominated by hydropower and nuclear power, this transmission effect is significantly weaker. This directly leads to cost differentiation in highly electricity-sensitive businesses like Bitcoin mining: in markets dominated by gas-fired power, rising carbon prices almost equate to a simultaneous increase in operating costs; while in regions rich in low-carbon electricity, this impact is relatively lower.

3. The dual pressures on mining companies: rising costs and policy uncertainty

For the Bitcoin mining industry, which is highly dependent on electricity, Canada's industrial carbon pricing system presents a dual challenge, profoundly impacting business operations and decision-making.

The first challenge is the direct increase in power generation costs driven by rising carbon prices. Canadian mining companies commonly use Power Purchase Agreements (PPAs). As industrial carbon prices continue to rise, the "carbon price adjustment" component in these contracts has a greater impact, leading to a year-on-year increase in the unit computing power cost of mining. Neither floating contracts linked to market electricity prices nor seemingly stable long-term fixed contracts can completely avoid this trend in the long run. The former will reflect cost increases more quickly, while the latter will face higher carbon tax premiums when renewing contracts in the future.

The second challenge stems from the complexity and uncertainty of the regulatory environment. Mining companies in different Canadian provinces do not follow the same set of rules, but rather differentiated regulatory systems. For example, some provinces (such as Alberta) maintain low local industrial carbon prices to preserve competitiveness, refraining from adjusting to federal policy. While this reduces compliance burdens in the short term, it also introduces significant policy risks. The federal government has the authority to assess local emissions reduction efforts based on the "equivalence principle": if local measures are deemed insufficient by the federal government, a higher-standard federal system may intervene. This potential policy shift means that companies' "low-cost" investment decisions may face forced adjustments in the future. This uncertainty is becoming a crucial factor that mining companies must consider when establishing operations in Canada.

4. Shifting Mining Strategies: From Cost Control to Compliance Planning

Faced with increasingly clear cost pass-through paths and a complex and ever-changing policy environment, the operating logic of Canada's cryptocurrency mining industry is undergoing a significant transformation. Companies are shifting from passive electricity price takers to proactive compliance planners and energy structure designers.

First, businesses are beginning to make structural adjustments to their energy procurement. One strategy is to sign long-term green power purchase agreements (Green PPAs) or directly invest in renewable energy projects. These adjustments no longer aim to simply lock in a predictable electricity price, but rather to fundamentally decouple from the existing pricing mechanism based on marginal natural gas pricing plus Canadian carbon costs. Under the OBPS framework, this verifiable low-carbon electricity structure may also generate additional carbon credits for businesses, thus translating compliance spending into potential revenue streams.

Secondly, the differentiated regulatory rules between provinces are giving rise to complex strategies for arbitrage using policy differences. For example, in British Columbia (BC), the accounting boundary of its OBPS system is primarily concentrated within the province's territory. This rule design means that imported electricity purchased from outside the province is not included in the carbon cost collection. Mining companies can strategically design their electricity procurement mix (e.g., using a small amount of electricity locally while purchasing large quantities from other provinces) to circumvent high local carbon electricity costs.

Furthermore, the incentive mechanism inherent in the OBPS system itself (i.e., exchanging efficiency improvements for exemptions) is becoming a new direction for corporate technology investment. This is mainly reflected in two aspects: First, the scale threshold, where facilities with annual emissions below a certain standard (e.g., 50,000 tons of CO₂e) are eligible for exemptions, prompting companies to take their total emissions into account when designing capacity; second, efficiency benchmarks, such as Alberta's (AB) TIER system, where if industrial companies' emissions intensity from fuel-powered electricity generation is better than the officially set "high-performance benchmark value," they can legally and significantly reduce or even completely eliminate their carbon costs—and in certain circumstances, even obtain additional revenue by selling carbon credits.

The aforementioned strategic shifts signify that carbon compliance is no longer simply a matter of financial deductions. With the US and Europe successively advancing their Carbon Border Adjustment Mechanisms (CBAMs), Canada's carbon pricing policy is rising from a domestic issue to a key cost point for international investment, and corporate compliance is rapidly evolving into a core competency for its financial and strategic planning.

5 From Strategy to Implementation: The Three Major Challenges of Enterprise Transformation

Based on the above analysis, Canada's elimination of the fuel carbon tax represents a profound policy adjustment. The relaxation of restrictions on the fuel sector while increasing pressure on the industrial sector reflects the federal government's decision to balance emissions reduction targets with economic resilience. For energy-intensive industries such as Bitcoin mining, this choice clearly points to three future trends:

- First, energy costs will continue to rise, but there is room for planning.

- Second, policy risks are increasing, but they can be controlled through scientific site selection and compliance arrangements;

- Third, green investment and carbon credit mechanisms will become new sources of profit.

However, there is a gap between "knowing" and "doing" these strategic opportunities. In practice, enterprises are facing three core challenges from decision-making to implementation:

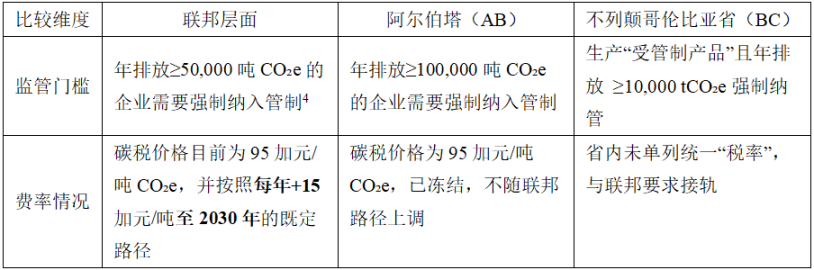

First, the two-tiered "federal-provincial" structure introduces regulatory complexity and hinders information input for decision-makers. While Canada has a federal carbon pricing benchmark, each province is allowed to design and implement its own equivalent industrial pricing system (such as OBPS or TIER). This results in businesses facing not a unified standard, but rather a situation of "one benchmark, multiple implementations." Significant differences exist between provinces in their definitions of "exemption thresholds," emission benchmarks for specific industries, rules for generating and using carbon credits, and even methods for calculating imported electricity. This localized implementation detail makes it impossible for businesses to simply apply a national standard. A carbon-saving strategy validated as effective in Province A may not qualify for exemptions in Province B due to different accounting methods, posing a significant challenge to businesses in developing optimal strategies.

Table: Comparison of Carbon Tax Rates at the Federal Level in Alberta (AB) and British Columbia (BC)

Secondly, traditional cost-making methods are no longer entirely applicable. Previously, the core consideration for mining companies' site selection was a single, immediate electricity price (/kWh). However, under the new regulations, companies must now consider risk-weighted factors. Decision-makers must now quantify those elusive variables: how much premium should be factored in for the hidden policy reversal risk behind a region's temporary low carbon price? Further complicating matters, investing in green energy (Trend 3) is a high capital expenditure (CAPEX) decision, while paying a carbon tax is a variable operating expenditure (OPEX)—assessing the future gains and losses from both in the decision-making process is not something traditional operations teams can accomplish.

Finally, the lack of a compliance system within the execution team hinders the implementation of strategies. Even if the decision-making level formulates a perfect strategy, it faces significant challenges at the execution level. The sole deliverable of all strategies is a compliance report submitted to regulatory agencies. This requires companies to establish a cross-validation system covering legal, financial, and engineering aspects. For example, does the data from the MRV (Monitoring, Reporting, and Verification) system meet the requirements of a tax audit? Are the sources and attributes of cross-provincial electricity consistent with legal contracts and financial accounting? Without this systematic compliance capability, even the most ingenious strategies cannot translate into real financial benefits.

6 From "Taxable" to "Responding", Where are Crypto Mining Companies Headed?

Currently, Canada's carbon pricing policy is entering a more refined phase. It is no longer simply a tax collection tool, but rather a consideration of both economic governance and industrial structure. Under this system, competition among energy-intensive companies will no longer depend solely on the cost of electricity, but also on the depth of their understanding of policy, the sophistication of their financial models, and the precision of their compliance implementation. For cryptocurrency mining companies, this presents both challenges and opportunities—those still relying on outdated single-cost models for site selection may be passively drained by future policy adjustments; while those that can systematically plan by combining energy markets, tax policies, and compliance structures will truly possess the ability to weather economic cycles.

However, as analyzed earlier, from strategy formulation to compliance implementation, enterprises are facing a triple challenge: insufficient information input, outdated decision-making models, and a lack of compliance execution. Under this trend, carbon tax planning, energy structure design, and policy risk assessment have become the core logic of the new round of competition among mining companies. Therefore, shifting from a passive "taxable" business model to a proactive "respond" strategic choice has become an unavoidable reality for mining companies.