By: Chilla, Analyst at Castle Labs

Compiled by: Tim , PANews

Stablecoins are dominating the market and gradually penetrating into the traditional financial sector and retail market. For example, supermarkets in some South American countries have begun to directly mark commodity prices with USDT. Its application scenarios are real, and in order to support this expansion trend, it may be necessary to seek support from new infrastructure.

Recently we have seen news about stablecoin-related chains, such as Plasma and Stable.

- What projects are they?

- What is the difference between them?

- Are they indispensable?

The rise of stablecoin-specific chains

The design goal of Plasma and Stable is to achieve faster, cheaper, and more scalable stablecoin transfers. The core idea is to attract liquidity and absorb funds from old networks that are less efficient but still have a large number of stablecoins.

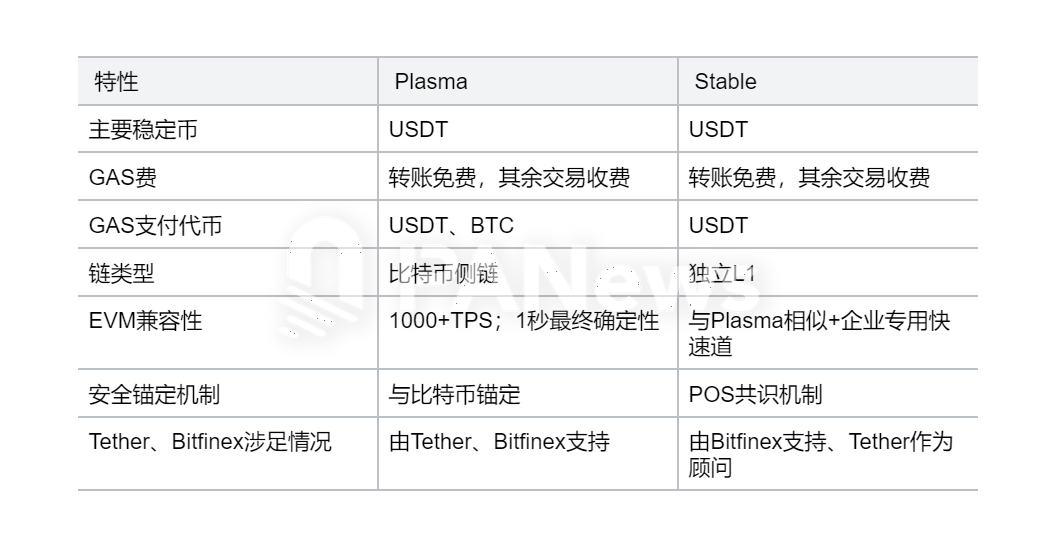

While there are some fundamental differences between the two networks, there are probably more similarities between them than not. In particular, the strongest commonality is USDT, which is the core hub shared by both.

More specifically, both integrate USDT0. This is an anti-fragmentation version of USDT that can be natively exchanged between different blockchain networks through LayerZero. It is currently mainly based on the Arbitrum network and is continuously expanding to emerging public chains. For end users, its usage experience is no different from regular USDT.

Plasma

Plasma is built as a Bitcoin sidechain, which means it inherits the security of Bitcoin through the anchoring mechanism, but maintains its own independent consensus mechanism. In short, malicious attackers need to break Bitcoin to tamper with Plasma history, but Bitcoin itself does not verify Plasma's blocks.

This system is designed for thousands of transactions per second and final confirmation in about 1 second, which is very suitable for the fast transfer of USDT, the stable currency of the US dollar. But the most outstanding feature compared to ordinary blockchains is that basic USDT transfers do not require GAS fees at all. So what is its profit model? The answer is: GAS fees are charged for all other operations in the network. After attracting users through free transfers to form a scale effect, the surge in users will drive the increase in the amount of on-chain operations that require payment. This is its operational strategy of using the second-order effect to create revenue.

Another special feature is that when it comes to handling fees, users can choose to pay with USDT or Bitcoin. The platform is fully compatible with EVM, and developers can easily deploy Ethereum applications. Since the platform has dual support from Bitfinex Exchange and Tether, it is not difficult to understand why it focuses on supporting USDT and Bitcoin.

Stable

Stable uses a different implementation. It is an independent first-layer network, not a sidechain, and uses a self-developed Proof of Stake consensus mechanism. Similar to Plasma, Stable is also compatible with EVM. The transfer gas fee of USDT stablecoin is zero, while the fees of all other on-chain operations still need to be paid. The key feature of the gas fee is that only USDT is accepted as payment currency.

Stable is supported by Bitfinex and USDT0. The company hired Tether CEO Paolo Ardoino as an advisor from the beginning, which fully demonstrates its focus on USDT, the main stablecoin in circulation.

In addition, they seem to be more focused on corporate and institutional clients, which will be discussed in detail later.

Privacy Policy

Both networks are very concerned about privacy protection. Although the specific situation is still unclear, the Shielded transaction concept mentioned by Plasma and the confidential transfer technology used by Stable are designed to protect transaction privacy while maintaining compliance.

In general, there is not much information about the exact difference between these two types of infrastructure. In addition to the technical differences explained above, it is reported that the Stable platform will also add more institutional-friendly features, such as:

Dedicated block space service for enterprises: Dedicated block space is provided for enterprises. This means that regardless of network congestion, transaction speeds can be guaranteed to be stable and fees will not surge.

USDT transfer aggregator: consolidate multiple USDT0 transfers to increase processing speed and reduce transaction costs.

Do they have any real use cases so far?

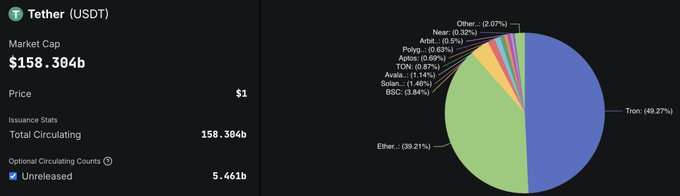

Of the USDT market value of $158.304 billion, 49.27% is circulated through the TRON network. Is anyone still using this chain? The ecosystem of the new public chain is much more developed than it.

However, it was the cheapest and most efficient option in the beginning. Therefore, Tether has always used this chain to mint and transfer funds. But the TRON public chain was not designed for this purpose. More importantly, Tether is not deeply involved in the chain ecosystem, but is just a user. If it loses its dominance over USDT, it will be the last straw that breaks the camel's back for TRON. Considering the lack of a sustainable ecosystem on the chain, this outcome is bound to happen.

The core strategy of chains like Plasma and Stable is to absorb liquidity from ecosystems with weak DeFi foundations. The purpose is not to eliminate competitors, but to surpass those inefficient chain ecosystems by building a hub centered on USDT payment and commercial settlement, especially with the advantage of free transfers. The liquidity attracted will naturally drive the influx of users and capital, giving rise to new DeFi protocols and ultimately building a truly vital ecosystem.

All this may give rise to a new SWIFT system that specifically serves stablecoins, where Tether not only issues stablecoins, but also becomes the dual cornerstone supporting currency value and underlying infrastructure. With the scale advantage of USDT, Tether can benefit from it, while Plasma and Stable can fully enjoy the dividends brought by the high-speed flow of funds on their networks.

It is undeniable that other blockchain ecosystems will not be forgotten. Solana, which focuses on core functions such as debit card payments and fiat currency exchange channels, Ethereum and its second-layer solutions focusing on the DeFi field, and emerging chains with specific application scenarios are likely to continue to flourish.

Recent Progress in Plasma

While this does not represent long-term sustainability, the short-term hype has been fully validated by the Plasma public token sale, which has seen a total of $1 billion in deposits within the subscription limit, meaning the chain will be ranked 12th in the stablecoin circulation rankings when it goes live.

In addition, Plasma has promoted a number of collaborations, such as:

- Yellow Card: Focuses on USDT transfer services in Africa.

- BiLira Kripto: Connecting Turkish Lira to Stablecoins to Enable Cross-Border Payments.

- Uranium Digital: Bringing commodity trading on-chain.

- Axis: Launching interest-bearing synthetic USD (xyUSD).

- Curve and Ethena

We will also wait for the subsequent development of Stable.

Conclusion

This is not to say that such projects will necessarily achieve product-market fit. In fact, the concept of a "stablecoin chain" may just be a sophisticated marketing strategy: creating a spotlight effect for USDT while using zero gas fees as a gimmick to create hype. This is essentially setting the stage for a vampire attack, except that it does not create token incentives out of thin air (such as the SushiSwap model), but rather achieves this by exempting users from transaction costs. To some extent, it can be called a free value-added model in the trading field.

Both chains are ready. But what will be more interesting in the future is how they will differentiate themselves, choose the best market channels, and most importantly, whether they can build a sustainable business ecosystem.