Stablecoins have now become the hottest topic, not only in the fields of technology, finance, and economy, but also in major social news, communities, and social platforms, where related content can be seen making headlines.

There are a lot of popular science content, various interpretations and opinions about stablecoins, which are quite lively. This article attempts to bring you some knowledge and opinions that may be more advanced and in-depth from a higher dimension.

1. International experts, celebrities, and executives’ comments on stablecoins

Here are some of the latest comments or opinions on stablecoins from international experts, celebrities, and executives:

1. On the growth and potential of the stablecoin market

• Gautam Chhugani (Bernstein analyst): “We expect major global financial and consumer platforms to issue co-branded stablecoins to enable value exchange on their platforms.” According to a Bernstein research report, the stablecoin market is expected to grow from $125 billion today to $2.8 trillion in the next five years.

• Noelle Acheson (corresponding author of Crypto Is Macro Now): "Demand growth is trending upward, which is bullish for crypto assets as it suggests increasing investor interest." She also noted that although the total market capitalization of stablecoins is still below levels from earlier this year, the growth trend suggests that the market is recovering.

2. Regulatory challenges and compliance of stablecoins

• Lael Brainard (Federal Reserve Governor): “Widespread adoption of stablecoins could pose risks to financial stability, and regulators need to ensure that their issuance and use are consistent with existing financial regulatory frameworks.” She stressed the importance of proper regulation of stablecoins to prevent them from being used for illicit financial activities.

• Anneke Kosse (BIS Economist): "The regulatory framework for stablecoins needs to be coordinated globally to avoid regulatory arbitrage and financial instability." She pointed out that the cross-border use of stablecoins requires regulators in various countries to strengthen cooperation and jointly develop regulatory standards.

3. Technology and innovation of stablecoins

• Nick Cafaro (CEO of Polymesh): "The development of stablecoins will promote the widespread application of blockchain technology in the financial field, especially in cross-border payments and supply chain finance." He believes that the combination of the stablecoin's stability mechanism and the decentralized nature of blockchain will bring higher efficiency and transparency to the global financial market.

• Mark Connors (CEO of 3iQ): “Innovations in algorithmic stablecoins provide new ideas for addressing the limitations of traditional stablecoins, but also bring new risks and challenges.” He emphasized the need for in-depth research and testing of algorithmic stablecoins to ensure their stability in market fluctuations.

4. Market dynamics and competition of stablecoins

• Garth Baughman (Federal Reserve economist): "The competitive landscape in the stablecoin market is changing, with some large stablecoins such as USDT increasing their market share while some other stablecoins are facing challenges." He pointed out that competition in the stablecoin market will affect its future development and market acceptance.

• Krisztian Sandor (markets reporter, CoinDesk): “The supply of Tether (USDT) continues to grow in 2023, showing an increase in demand for it. However, other stablecoins such as USDC and BUSD have seen a decline in market share, suggesting that the stablecoin market is still evolving.”

5. International influence and cooperation on stablecoins

• Facklmann, Juliana (Professor at the University of São Paulo, Brazil): "The emergence of stablecoins provides emerging market countries with a new cross-border payment solution, helping to reduce transaction costs and improve the efficiency of capital flows." She also pointed out that the international use of stablecoins requires countries to strengthen monetary policy coordination and regulatory cooperation.

• Camila Villard Duran (Professor at the University of São Paulo, Brazil): "The development of stablecoins will have a profound impact on the global financial system, especially in cross-border payments and international settlements. Central banks and regulators need to work together to explore how to use stablecoins to promote financial stability and economic development."

6. Risks and challenges of stablecoins

• Briola, Antonio (Professor at University College London): “The failure of stablecoins such as the Terra-Luna incident reminds us that the design and operation of stablecoins need to carefully consider risk control and market stability.” He emphasized the importance of stress testing and risk assessment of stablecoins to prevent similar incidents from happening again.

• Jacob Gerszten (Federal Reserve economist): "The widespread use of stablecoins may pose competitive pressure on the traditional banking system, and regulators need to pay close attention to their impact on financial stability." He also pointed out that the decentralized nature of stablecoins may bring new regulatory challenges and corresponding regulatory policies need to be formulated.

2. Three major theories related to stablecoins

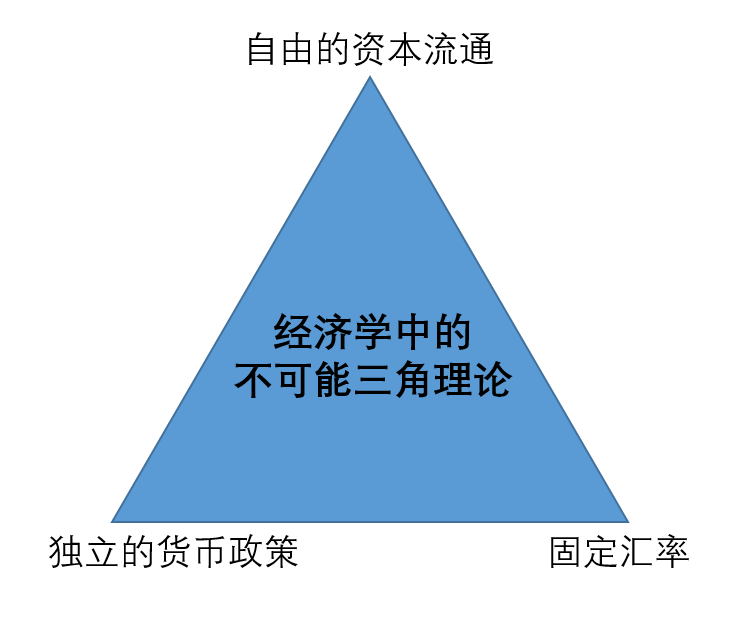

1. The “Impossible Trinity Theory” in Economics

Paul Robin Krugman, a famous American Jewish economist and Nobel Prize winner in economics, once proposed the theory of the "impossible triangle", that is, a country cannot simultaneously achieve free capital flows, independence of monetary policy and stability of exchange rates. In other words, a country can only have two of them, but not all three at the same time. If a country wants to allow capital flows and requires an independent monetary policy, it will be difficult to maintain a stable exchange rate. If a stable exchange rate and capital flows are required, an independent monetary policy must be abandoned.

A key question is whether stablecoins (cryptocurrencies) can form a currency/capital market, currency/capital tool, or currency/capital application that is useful to the government. If stablecoins (cryptocurrencies) can break this impossible triangle or be useful to sovereign states, they may be accepted.

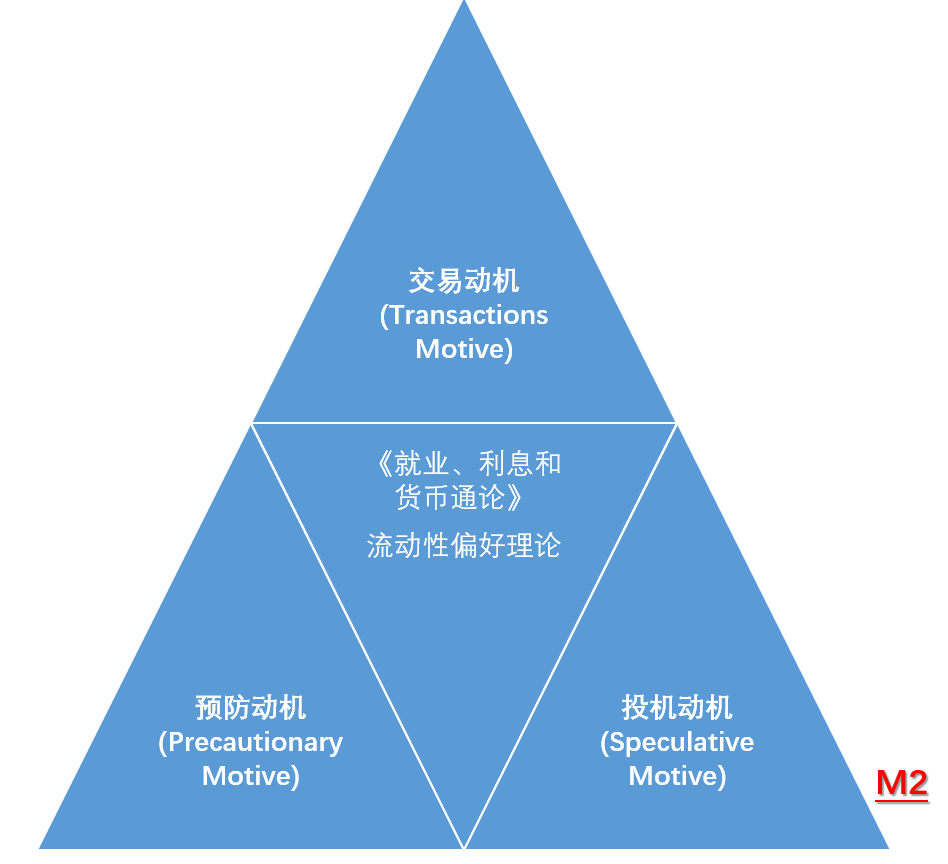

2. Keynesian theory of money demand

Keynes believed that the total money demand (M) of society is the sum of the money demand to meet the three motivations on the right, that is, M=M1+M2=L1(Y)+L2(R). This formula clearly shows that money demand is not only a function of income, but also a function of interest rates. In particular, interest rates regulate total money demand by affecting speculative demand.

It can be seen that in addition to transaction motives, stablecoins are now (or already have) speculative motives and precautionary motives.

3. Stablecoin: The first killer application of encrypted digital currency is finally born

Stablecoins were originally intended to facilitate buying, selling and trading in the encrypted digital world, but now they are growing secretly and becoming the "preferred" tool and means for cross-border payments.

The high volatility of cryptocurrencies makes it difficult to implement daily applications of "payment and transactions" - merchants who accept Bitcoin may wake up to find that the payment has shrunk by 10%; investors who want to hedge risks in the short term also lack a "safe corner". Stablecoins came into being, and the crypto world has a "stable unit of account" to facilitate transactions and transfers, allowing crypto finance to take the first step towards "practicalization".

Stablecoins have now triggered a "catfish effect" that central banks must face up to and seek innovation.

3. Five common sense about stablecoins

Regarding stablecoins, most articles will explain USDT and USDC. I didn’t want to introduce them, but since this may be the first time for readers to pay attention to stablecoins, we will only give the simplest introduction.

USDT was launched by Tether in 2014 to provide a stable value storage and transaction medium for the cryptocurrency market, solving the problem of excessive price fluctuations of cryptocurrencies such as Bitcoin. It is one of the earliest stablecoins and has quickly become the most commonly used stablecoin in cryptocurrency transactions due to its first-mover advantage and wide market acceptance.

USDC was jointly launched by Circle and Coinbase in 2018, aiming to provide a more transparent and compliant stablecoin to solve the reserve transparency problem of USDT. Circle has made many efforts in compliance, such as obtaining relevant licenses in many countries and regions, and USDC has also become the first stablecoin issuer in Europe that meets the MiCA standard.

1. Birth: To solve the pain points of cryptocurrency

The high volatility of cryptocurrencies makes it difficult to implement daily applications of "payment and transaction" - merchants who accept Bitcoin may wake up to find that the payment has shrunk by 10%; investors who want to hedge in the short term also lack a "stable corner". Stablecoins came into being: anchored to legal currencies (such as the US dollar, the euro) or other assets (gold, cryptocurrencies), using algorithms, mortgages and other means to "press" price fluctuations within a controllable range. For example, USDT and USDC were originally designed to give the crypto world a "stable unit of account" to facilitate transactions and transfers, so that crypto finance can take the first step towards "practicalization".

2. Definition of Stablecoin

Definition of Stablecoins Stablecoins are digital currencies designed to maintain a stable value. Unlike cryptocurrencies such as Bitcoin, the value of stablecoins is usually pegged to a fiat currency (such as the U.S. dollar) or other stable assets. This peg mechanism makes stablecoins relatively less volatile in price, making them more suitable for daily transactions and payments.

3. The core purpose of stablecoins: not just for hedging

The original core function of stablecoins was simply to make the trading of encrypted digital currencies more convenient, but today, their uses have become very wide.

The "stable anchor" of crypto trading pairs: the base currency pair of the trading venue (BTC/USDT, ETH/USDC).

Volatility avoidance: A safe haven during market fluctuations.

DeFi cornerstone: collateral/debt unit for lending protocols, trading pair basis for decentralized exchanges, and primary target asset for yield farming.

Cross-border payments and remittances: Faster and cheaper than traditional channels.

Daily settlement/salary payment: Application in supporting the crypto payment ecosystem (but unclear regulation is an obstacle).

As a "bridge"/"transit station" for fiat currency to enter and exit the crypto world: the key entrance and exit of the exchange.

4. Classification of Stablecoins

A. Fiat-Collateralized: The mainstream choice, transparency is key

Mechanism: The issuer holds sufficient fiat currency reserves (such as US dollars, euros) or highly liquid cash equivalents (such as short-term US Treasury bonds) to support the value of the stablecoin in circulation (1:1 anchoring).

·Represents: USDT (Tether), USDC (Circle), BUSD (Paxos/Binance), TUSD (TrustToken).

· Core advantages: o Easy to understand: The principle is clear and the anchoring is intuitive. o High theoretical stability: With full collateral, the value support is strong.

· Core Challenges and Controversies: o Audit and Transparency: Top priority! Investors rely on the audit report (or on-chain proof) provided by the issuer to verify the authenticity, adequacy, and security of the reserve assets (such as whether they include risky assets such as commercial paper). USDT has been questioned for its lack of transparency. USDC has a good reputation for reserve transparency and asset allocation mainly based on US bonds and cash. o Centralization Risk: The issuer holds huge reserve assets and is a centralized trust node. There may be problems such as asset freezing, account banning, and operational risks. Regulatory pressure is concentrated on this type of stablecoin. o Banking system risk: Fiat currency reserves rely on the traditional banking system and custodians.

B. Crypto-Collateralized: Decentralized belief, complex but innovative

Mechanism: Users deposit excess digital assets (mainly ETH, WBTC, etc.) as collateral (the collateral ratio is usually >150%), and the system mints stablecoins (such as DAI) based on this.

Representative: DAI (MakerDAO) (most successful representative).

· Core advantages: o Decentralization: The rules of mortgage, minting, liquidation, etc. are determined by smart contracts and decentralized organizations (DAO) governance, which are free from the control of a single entity and more resistant to censorship. o Transparency: Mortgage assets are usually locked in public smart contracts and can be checked on the blockchain. o No need for traditional bank accounts: More suitable for a pure on-chain native environment.

· Core Challenges: o Complexity: Involving multiple factors such as collateral ratio, liquidation threshold, stability fee, governance token voting, oracle price feed, etc., the user experience threshold is high. o Volatility risk: The collateral assets themselves fluctuate violently. If the ETH price plummets too quickly, it may lead to insufficient collateral value (below the liquidation line), triggering large-scale liquidation and exacerbating the market decline (requiring a strong liquidation mechanism and oracle guarantee). o Collateral efficiency: It requires a large amount of "locked" high-value crypto assets as support, and the capital efficiency is lower than that of fiat currency collateral. There may still be pressure to decouple in extreme market conditions.

C. Algorithmic Stablecoin: Once the "Holy Grail", with both risks and opportunities

Mechanism: No real collateral. Rely on algorithms (on-chain smart contracts) and market supply and demand mechanisms (usually combined with the "dual currency model") to adjust the money supply to anchor the price.

Representatives: UST (collapsed) in the Terra ecosystem, the existing Frax (partial algorithm), USDD (partial reserve + partial algorithm). There are fewer pure algorithmic representatives.

Ideal goal: o Complete decentralization: no reliance on fiat currency, physical or crypto assets for collateral. o Higher capital efficiency: theoretically no need for large amounts of capital.

· Cruel reality and huge risks: o Death spiral risk: The most fatal weakness! When the price falls below the anchor price (such as $1), the algorithm design usually requires the destruction of stablecoins (shrinking supply) to boost the price, which is often achieved by incentivizing users to burn stablecoins in exchange for higher-value governance tokens (such as UST for LUNA). Once market confidence collapses, stablecoins are sold in large quantities, and the price of governance tokens may plummet due to additional issuance (users burning stablecoins will get more newly minted governance tokens). The plummeting governance tokens, in turn, completely destroy the value support of stablecoins, forming a "death spiral". The collapse of UST is a textbook example of this risk. o Over-reliance on market psychology: Price stability is entirely based on the premise that participants have continued confidence in the mechanism itself and are willing to participate in arbitrage. When confidence collapses, the mechanism is very likely to fail. o Design complexity: The model is difficult to perfectly design and maintain for a long time.

Current trend: Pure algorithmic stablecoins have basically lost market trust due to the collapse of UST. The mainstream is a hybrid model of partial collateral + partial algorithm (such as Frax) to increase the underlying credit support.

D. Commodity mortgage type: niche but unique

Mechanism: Anchoring the value of physical commodities such as gold, silver, and oil.

· Representative: PAX Gold (PAXG) (pegged to 1 troy ounce of physical gold).

Value: Providing a way for the crypto market to access the price of real assets, an alternative to combating fiat currency inflation.

Challenges: The custody, auditing, and liquidity of physical assets are relatively large, and the market size is much smaller than that of fiat currency collateral.

E. Innovative stablecoins: combined with CBDC

Mechanism: It may be integrated with CBDC in the future and become a “supplement” to the central bank’s digital currency.

Representative: None at this time.

Principle: Central banks of various countries are working on CBDC (digital RMB, digital dollar, etc.), and stablecoins may work in conjunction with CBDCs - for example, using stablecoins as the "cross-border settlement layer" and CBDC as the "domestic legal layer". In other words, CBDC and stablecoins can be integrated, of course, this requires a lot of details.

5. Risks and controversies: hidden concerns in the shadows

The center of the regulatory storm: The object of most concern for global regulators. Concerns include: threats to fiat currency sovereignty, potential financial stability risks (especially when large-scale such as USDT), lack of adequate investor protection, anti-money laundering (AML)/counter-terrorist financing (CFT) compliance, insufficient reserve asset quality and transparency. Anti-money laundering/counter-terrorist financing (AML/CFT):

Anonymity can be abused. User Protection:

Risk of bankruptcy or absconding of the issuer. Monetary policy challenges:

Large-scale adoption could weaken the central bank's regulatory capacity (e.g., digital dollars replacing national currencies). Financial stability:

Potential impact on payment systems and capital markets. Countries are stepping up legislation (such as the EU MiCA framework and the US legislative proposal).

Operational risks (mainly for fiat-collateralized assets): bankruptcy of the issuer, fraud, hacker attacks on reserve accounts/custodian banks, and compliance errors leading to service interruptions or asset freezes.

Depegging risk (core challenge): Any type of risk can happen! Fiat currency (insufficient reserves/bank run), crypto asset (collateral price collapse/liquidation failure), algorithm (death spiral/confidence collapse) may temporarily or permanently depeg the $1 peg (such as UST collapse, USDC briefly fell to $0.87 due to Silicon Valley Bank risk).

Systemic risk: If a large stablecoin (such as USDT) collapses or has serious problems, it will have a catastrophic chain reaction on the entire cryptocurrency market (especially DeFi, which is highly dependent on it).

Transparency gap (especially for fiat-collateralized stablecoins): The authenticity, frequency, and depth of proof of reserves remain key pain points. Investors need to pay close attention to the transparency reports of leading stablecoin issuers.

4. Nine core viewpoints

The following are nine in-depth perspectives based on the latest development trends, regulatory dynamics and technological evolution of global stablecoins, which are comprehensively refined based on policy documents, market data and academic research. Each perspective is equipped with core evidence and forward-looking analysis:

1. Stablecoins have become a "digital weapon" in the financial game between major countries

Viewpoint: USD stablecoins (such as USDT and USDC) are essentially an on-chain extension of the USD hegemony, binding global liquidity through forced U.S. debt reserves.

Evidence: The US GENIUS Act requires that payment stablecoins be 100% allocated to cash, deposits or short-term US bonds, forming a closed loop of "global currency purchases → capital repatriation to US bonds";

Citi predicts that the scale of stablecoins will reach 3.7 trillion US dollars in 2030. If all of them are anchored to US Treasuries, it will become one of the largest holders of US Treasuries.

2. Offshore RMB stablecoin will reconstruct the cross-border payment system

Viewpoint: Hong Kong’s pilot RMB stablecoin (CNH) is China’s core strategy to break through the SWIFT blockade and open up a new path for RMB internationalization.

Evidence: Hong Kong's Stablecoin Ordinance came into effect, allowing licensed institutions to issue offshore RMB stablecoins. Standard Chartered and JD.com have entered the HKMA's sandbox test;

If the CNH stablecoin is implemented, it can build a cross-border payment channel independent of SWIFT, supplement the CIPS system, and reduce the exchange costs of the "Belt and Road" countries by 90%.

3. Stable currencyization in emerging markets accelerates the contradiction of de-dollarization

Viewpoint: People in countries with high inflation spontaneously adopt stablecoins as "digital dollars", but this exacerbates the local currency sovereignty crisis.

Evidence: Argentina’s annual inflation rate exceeded 200%, and 40% of savings were converted to USDT; Nigeria received more than $59 billion in cryptocurrencies annually, and 43% of African on-chain transactions involved stablecoins;

Although central banks in Türkiye, Lebanon and other countries have banned stablecoins, over-the-counter P2P transaction volumes have increased by 300% year-on-year.

4. RWA (real world assets) becomes a new anchoring paradigm for stablecoins

Viewpoint: As a value carrier, stablecoins are accelerating the tokenization of traditional assets (such as US bonds and funds). For example, BlackRock issued a tokenized US bond fund, and Circle's USDC was used for on-chain asset settlement, promoting the "programmability" of the financial market.

Evidence: The global tokenized asset size is expected to exceed $1 trillion in 2025, of which stablecoins account for more than 70%. The Hong Kong Stablecoin Ordinance allows commercial banks to issue stablecoins and supports the use of tokenized assets in cross-border payments. BlackRock and Fidelity issue tokenized funds (such as BUIDL) with U.S. Treasuries as underlying assets, allowing stablecoins as a subscription/redemption medium; MakerDAO allocates more than $3 billion in reserves to U.S. Treasuries and corporate bonds, and its issued DAI has become the benchmark for RWA settlement.

5. Regulatory arbitrage gives rise to competition for “stable currency offshore centers”

Viewpoint: Hong Kong, Singapore and the UAE are competing for stablecoin issuers with differentiated licensing systems, forming a new regulatory competition and cooperation landscape in Asia.

Evidence: Hong Kong requires issuers to have a paid-in capital of HK$25 million + 100% reserve segregated custody, while Singapore’s sandbox allows for a trial run of flexible capital;

JD.com plans to issue a HKD/USD stablecoin in Hong Kong, aiming to reduce cross-border payment costs by 90%, while Singapore has attracted Circle to set up its Asian headquarters.

6. Algorithmic stablecoins enter the 2.0 era of "partial reserve + enhanced token economics"

Viewpoint: After the collapse of UST, the new generation of algorithmic stablecoins integrate over-collateralization and gaming mechanisms to avoid a death spiral.

Evidence: Ethena Labs’ USDe adopts the dual model of “ETH staking income + perpetual contract hedging”, and its market value has increased from 146 million to 6.2 billion US dollars in one year (according to network data);

Frax Finance v3 introduces partial fiat reserve + protocol controlled value (PCV) mechanism, and the decoupling risk is reduced by 80% compared with UST.

7. CBDC and stablecoins move from confrontation to "regulatory complementarity"

Viewpoint: Sovereign digital currencies (such as the digital RMB) will be interconnected with compliant stablecoins to form a dual-track payment network.

Evidence: China’s central bank has set up an international digital RMB operations center to explore cross-chain exchange with Hong Kong’s stablecoins;

The EU MiCA framework requires stablecoin issuers to deposit a deposit with the central bank to reserve a channel for CBDC access.

8. Enterprise-level stablecoins reshape global supply chain finance

Viewpoint: Multinational corporations use stablecoin settlement to replace traditional letters of credit, achieving seconds-level payment and cost revolution.

evidence:

The global manufacturing leader uses stablecoins to pay suppliers, with settlement time reduced from 3 days to 5 minutes, saving 1.2% in fees per transaction;

Amazon and Shopify support merchants receiving USDC payments, and PayPal's PYUSD covers 2 million merchants.

9. Compliance with stablecoin licenses has become the "lifeline" of financial technology companies

Viewpoint: Whether or not a company can obtain a license from a major jurisdiction determines whether it can participate in the trillion-dollar stablecoin ecosystem.

Evidence: Only five institutions were selected in the first batch of Hong Kong sandbox list (including ZhongAn Bank and Standard Chartered), and JD.com, Small Commodity City and others competed for the second batch of licenses;

The US GENIUS Act requires that stablecoin issuers must hold a national banking license, and Goldman Sachs and JPMorgan Chase are accelerating their layout.

5. Six possible development trends in the future

1. Stablecoins are reshaping the global payment system and becoming the core infrastructure in the digital economy era

Stablecoins use blockchain technology to achieve real-time cross-border payment (minutes) and disruptive cost reduction (the handling fee is only 1/10 to 1/100 of traditional wire transfers), and have become the core bridge connecting traditional finance and the crypto world. For example, USDT is widely used for import payments and savings in countries with high inflation such as Argentina and Nigeria, and the Hong Kong dollar stablecoin of JD.com has been connected to Southeast Asian e-commerce platforms to promote regional trade efficiency.

2. Under the wave of regulatory compliance, stablecoins will enter a new era of sovereign currency competition

Countries have strengthened regulation of stablecoins through legislation in order to maintain monetary sovereignty and financial stability. For example, the US GENIUS Act requires that stablecoins be 100% backed by highly liquid US dollar assets and prohibits the unauthorized circulation of overseas stablecoins; the EU has restricted the scale of non-euro stablecoin transactions through the MiCA framework; and Hong Kong, China, has balanced innovation and risk through a licensing system and explored offshore RMB stablecoin pilots.

3. Stablecoins will become a key tool for inclusive finance and bridge the global financial divide

In regions such as Africa and Southeast Asia where traditional financial services are insufficient, stablecoins have become an alternative for cross-border remittances and savings through their low threshold and low cost. For example, Nigeria receives more than $59 billion in cryptocurrencies each year, and 43% of African on-chain transactions involve stablecoins.

4. The geopolitical game of stablecoins will reshape the international monetary power structure

The dominance of the US dollar stablecoin (accounting for 85% of the market) has strengthened the hegemony of the US dollar, but China, the European Union and other countries are exploring the path of currency internationalization through stablecoin pilots. For example, Hong Kong's offshore RMB stablecoin may become a new tool for trade settlement in the "Belt and Road Initiative", challenging the monopoly of the US dollar.

5. Integration with CBDC: Becoming a "supplement" to the central bank's digital currency

Central banks of various countries are working on CBDC (digital RMB, digital dollar, etc.), and stablecoins may work in synergy with CBDC - for example, using stablecoins as the "cross-border settlement layer" and CBDC as the "domestic legal layer" to complement each other's strengths and weaknesses. While China is exploring the digital RMB, it is also studying the "stablecoin regulatory sandbox", which may form an ecosystem of "legal digital currency + compliant stablecoin" in the future.

6. Decentralization: A purer “crypto-native stablecoin”

The crypto community pursues "decentralization". In the future, there may be more complete algorithmic stablecoins and over-collateralized stablecoins to solve the loopholes of the existing model. For example, introducing multi-asset collateral, dynamically adjusting the collateral ratio, and even combining AI algorithms to predict market fluctuations, so that stablecoins can be truly "decentralized and stable."

VI. Conclusion

Stablecoins are a great attempt by the crypto world to achieve "value stability". They connect volatile crypto assets with real finance, support the prosperity of DeFi, and also expose the risks and regulatory difficulties of crypto finance. As a digital currency designed to maintain stable value, stablecoins have broad application prospects and important application value in cross-border payments, supply chain finance, and decentralized finance.

However, the development of stablecoins also faces regulatory challenges such as anti-money laundering, consumer protection and financial stability. In the future, will it become a "new tool" for compliant finance, or continue to "innovate" on the edge of regulation? In any case, every step of stablecoins is reshaping our imagination of "currency and finance" - this may be the most fascinating part of the crypto world: always looking for "stability" in the unknown and building order in chaos.

As a key bridge between the crypto world and traditional finance, the value and potential of stablecoins are unquestionable. It has spawned efficient global payments and open financial innovation (DeFi), demonstrating the momentum of technology to reshape finance. However, the trust crisis, regulatory challenges and potential systemic risks it has caused are like the sword of Damocles hanging high. The future of stablecoins must be a process of seeking a difficult balance between innovative vitality and financial stability. Only through transparent operations, solid reserves and effective supervision can this "stabilizing force" truly escort the digital economy on its voyage, rather than becoming the source of the next storm. For ordinary users, understanding its mechanism and recognizing its risks are the prerequisites for participating in this change.

The views in this article are merely academic exchanges and industry discussions and do not constitute investment advice. We should strictly abide by my country's laws and regulations, consciously stay away from illegal financial activities, jointly maintain a good economic and financial environment, and safeguard national financial security and social stability.