Authors: Iris, Bai Qin, Huang Wenying

On February 19, 2025, the Hong Kong Securities and Futures Commission (SFC) released the latest regulatory roadmap "ASPI-Re" for the virtual asset market, aiming to further improve the supervision of the virtual asset market, introduce more types of virtual asset products and functions, and balance innovation and risk management in Hong Kong's Web3 industry.

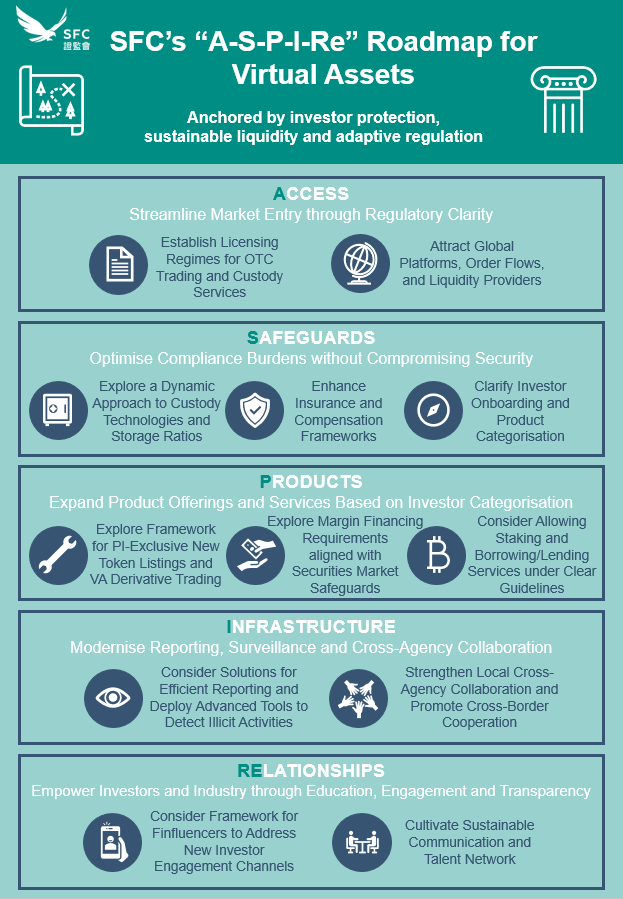

The roadmap proposes that the Hong Kong Securities and Futures Commission will adopt five major pillars, namely market access (Access), safety (Safeguards), product innovation (Products), infrastructure construction (Infrastructure) and relationship management (Relationships), as well as 12 actions, including but not limited to optimizing the licensing system, promoting OTC and custody service supervision, studying allowing professional investors to trade derivatives and staking, and building Hong Kong into a compliant and trustworthy virtual asset liquidity center.

For Mankiw, the release of the regulatory roadmap also means that the compliance direction and path for Web3 project startups in Hong Kong are becoming clearer. Therefore, in this article, Mankiw first summarizes the roadmap, extracts the key regulatory directions and relevant compliance matters for Web3 projects to enter Hong Kong, so that practitioners can understand.

Pillar A: Expanding Access

In 2024, the Hong Kong Securities and Futures Commission officially implemented the Virtual Asset Trading Platform (VATP) licensing system, and multiple virtual asset trading platforms in the Hong Kong virtual asset market have been approved to operate.

However, there are still barriers to entry in the market, especially over-the-counter ( OTC ) and custody services have not yet been included in the regulatory framework, which not only affects the integrity of the market structure, but also limits investors' trading options. To this end, the SFC proposed to establish an independent licensing system for OTC transactions and custody services under Pillar A, so that non-VATP businesses can operate under a compliance framework. OTC transactions are crucial for large transactions, and custodians are the key link in ensuring the safety of assets. The new licensing system will fill the gap in the market and enhance the security and transparency of the Hong Kong market.

At the same time, Hong Kong's virtual asset market cannot rely solely on local virtual asset trading platforms. Liquidity providers (LPs) and global virtual asset trading platforms can also bring fresh blood to Hong Kong's virtual asset market. Therefore, the Hong Kong Securities Regulatory Commission also plans to appropriately lower the threshold in 2025 and introduce this type of provider in compliance, so that local investors can access a wider range of global trading order books, while reducing transaction costs and improving market liquidity.

For Web3 companies, the launch of Pillar A means a change in the market entry threshold . Companies that plan to provide OTC trading or custody services in Hong Kong need to pay close attention to the new licensing requirements, and licensed trading platforms will also face greater competition from international platforms. At the same time, the opening of global liquidity will make Hong Kong a more attractive virtual asset center, but it also places higher demands on the compliance capabilities of companies.

Pillar S: Optimizing compliance requirements

At the end of 2024, the Hong Kong Securities and Futures Commission summarized the licensing process and results of the year and believed that it was necessary to optimize the compliance process and increase the licensing rate while ensuring market safety. At the same time, the global regulatory environment is constantly evolving, and overly strict compliance requirements may reduce the attractiveness of the Hong Kong market and hinder the entry of global liquidity.

Therefore, under Pillar S , the SFC proposed a series of adjustment plans to optimize custody, storage ratios, insurance compensation mechanisms and investor access rules to ensure that while maintaining market security, unnecessary compliance costs are reduced and market competitiveness is improved.

For example, Hong Kong's current custody requirements and cold storage ratios are too rigid, which may cause VASPs to face liquidity management difficulties during periods of high trading volume. The SFC plans to allow trading platforms to choose custody methods and optimize the ratio of hot and cold storage according to their own risk management strategies in the next adjustment, while supplemented by independent audits, real-time monitoring and other mechanisms to ensure the safety of funds while improving operational efficiency. In addition, the mandatory insurance and compensation mechanisms will also be more flexible. In the future, VASPs will be able to choose appropriate insurance plans based on their own business models, rather than a one-size-fits-all unified standard.

In terms of investor access, the SFC plans to enable Web3 companies to clarify their compliance paths when issuing products and entering the market through a clearer product classification framework. For example, different types of virtual assets such as security tokens, stablecoins, and RWA (real-world asset tokenization) may be subject to different regulatory requirements to reduce compliance uncertainty and ensure market transparency for investors.

For Web3 companies, the adjustment of Pillar S means a reduction in compliance costs, but it also raises higher technical and risk control requirements. Trading platforms and custodians need to adjust their storage and security strategies according to the new regulatory framework, while project parties planning to enter the Hong Kong market need to more clearly identify the regulatory attributes of their products to ensure compliance operations.

Pillar P: Expanding the product range

At present, the virtual asset trading market in Hong Kong mainly revolves around the spot market. At the same time, taking HashKey Exchange, the largest licensed exchange in Hong Kong, as an example, it currently only provides a few mainstream currencies (such as BTC and ETH), and the overall product diversity of the market is low. Compared with the global market, Hong Kong's trading ecology still has a lot of room for expansion, especially in financial instruments such as derivatives, staking, lending, and structured products .

Therefore, the introduction of Pillar P means that the Hong Kong Securities Regulatory Commission plans to expand the scope of tradable products under the compliance framework to meet the needs of professional investors for risk management tools and market depth. The core idea of the regulatory authorities is not to fully liberalize, but to open some high-risk products to professional investors (PI) under the Investor Suitability Principle , while strengthening transparency and market supervision.

First, the SFC plans to allow professional investors to trade new tokens and virtual asset derivatives. The listing of new tokens will be based on stricter due diligence and information disclosure requirements to ensure that only tokens that meet the standards can enter the market for trading. At the same time, the Hong Kong Securities and Futures Commission will also study the regulatory framework for virtual asset derivatives to support professional investors in hedging, arbitrage and risk management.

In addition to the expansion of trading products, the Hong Kong Securities and Futures Commission has also proposed exploring a compliance framework for pledge and lending businesses under Pillar P. At present, pledge and lending businesses have become mainstream virtual asset investment strategies in the global market, but the regulation of these services in Hong Kong is still in a gray area. In the future, it is expected that the SFC will allow regulated trading platforms to provide pledge and lending businesses, but they may be required to meet specific custody, risk management and information disclosure standards.

The implementation of this series of measures means that the product types in the Hong Kong market will be closer to international standards, but it also requires Web3 companies to invest more resources in compliance and risk control. For project parties planning to provide mortgage or lending services in Hong Kong, establishing a secure asset custody mechanism and a transparent profit distribution model may become key elements of compliance.

Pillar I: Strengthening regulatory capacity

There were various airdrop phishing incidents before, and then the president recommended the MEME coin suspected of insider trading. The Web3 market has never been "lack" of market manipulation, fraudulent transactions, money laundering and other issues. However, at present, the SFC or the regulatory agencies of most countries and regions mainly rely on event triggers to regulate the virtual asset market, that is, they will take action only when a security incident occurs. This post-event regulatory model obviously has a significant lag and is difficult to effectively prevent market manipulation or fraudulent transactions.

Therefore, under Pillar I, the SFC plans to optimize regulatory reporting mechanisms and introduce data-driven monitoring tools through new technology tools and infrastructure construction to enhance market-wide regulatory capabilities. The SFC proposed that it will study ways to directly report digital asset information and explore various data-driven monitoring tools, including transaction monitoring, blockchain intelligence, wallet tracking, etc., to identify fraud, financial crimes and market misconduct earlier.

At the same time, the SFC plans to strengthen cross-institutional cooperation , including but not limited to cooperation with the Hong Kong Police, the Hong Kong Monetary Authority (HKMA), the International Organization of Securities Supervisors (IOSCO) and other institutions to jointly combat market manipulation and illegal transactions.

For Web3 companies, especially virtual asset trading platforms, Pillar I's regulatory upgrade means stricter data reporting obligations and higher transaction transparency requirements. Therefore, companies need to strengthen compliance management and risk control systems to ensure compliance with future regulatory standards, especially in terms of transaction data reporting, asset flow monitoring and anti-money laundering compliance.

Pillar Re: Market Education

The complexity and high risk of the virtual asset market make investor education and industry transparency issues that cannot be ignored. Pillar Re in the roadmap focuses on Web3 market education, industry exchanges and regulatory transparency , aiming to help investors better understand the market and promote interaction between Web3 companies and regulators.

One of the initiatives worth noting is that the Hong Kong Securities and Futures Commission plans to establish a regulatory framework for Finfluencers (financial bloggers) . In recent years, social media has been flooded with investment advice on virtual assets. Some KOLs (opinion leaders) have influenced investors' decisions through misleading propaganda, and even a few KOLs have become part of the scam. Therefore, the SFC plans to ensure that investors can better understand virtual asset investments and protect their interests by promoting responsible behavior and accountability of financial influencers. Once this initiative is implemented, for Web3 companies and KOLs, it may mean that the marketing compliance requirements in the Hong Kong market will be stricter, and KOLs and social media propaganda will be subject to higher standards of supervision.

In addition to the measures targeting KOLs, regulators also plan to launch investor education programs to enhance the level of awareness of market participants and reduce investment risks. In addition, Pillar Re also emphasized the establishment of an industry exchange platform to enhance policy transparency. The Hong Kong Securities and Futures Commission plans to strengthen communication with Web3 companies through the Virtual Asset Advisory Panel (VACP) , so that market participants can understand regulatory policies more directly and provide feedback during the policy-making process. In this way, Web3 companies will be able to use the official industry exchange platform to establish closer communication with regulators to ensure compliance and sustainability of their businesses.

Attorney Mankiw's Summary

The "ASPI-Re" roadmap released by the Hong Kong Securities and Futures Commission (SFC) is undoubtedly an important milestone in the compliance process of Hong Kong's virtual asset market. From the five pillars and 12 measures, the SFC is trying to find a balance between risk control and market development. For Web3 companies, the introduction of this series of new regulations not only means that the compliance threshold of the Hong Kong market is clearer, but also means that compliance costs, market competition and regulatory requirements will be comprehensively upgraded.

As a Web3 lawyer who has long been concerned about the regulation of the virtual asset market in Hong Kong, Mankiw has always maintained close communication with Hong Kong regulators and has been deeply involved in the license application, business compliance and regulatory adaptation of Web3 companies in Hong Kong. Facing the upcoming SFC regulatory upgrade, Mankiw will pay close attention and develop compliance solutions to optimize the business structure and improve market adaptability for virtual asset trading platforms, crypto funds, Web3 start-ups and cross-border business teams under the compliance framework.

As a Web3 lawyer who has long been concerned about the regulation of virtual assets in Hong Kong, Mankiw has always maintained close communication with the SFC and has been deeply involved in the license application and commercial compliance adaptation of Hong Kong Web3 companies. In the face of this regulatory upgrade, Mankiw has paid close attention to policy changes and helped trading platforms, crypto funds, start-ups and cross-border business teams to optimize their business structure within the compliance framework and improve market adaptability.