Article written by: Lesley, MetaEra

Princess Christine

On June 17, crypto startup Infini announced the closure of all card services. The news attracted a lot of industry attention and the regret of loyal users.

"How to renew ChatGPT and Twitter Blue Label?"

“Is it possible to restart this business in the future?”

…

The more satisfied the users are, the more losses the company suffers - this is the cruel paradox faced by U-card startups.

Infini's closure of its U card business is not an isolated case. In the past two years, at least two well-known U card service providers have withdrawn from the market, first OneKey and now Infini. They have all tried to build a bridge between stablecoin payments and real consumption, but ultimately stopped due to high compliance costs and unsustainable business models.

A rational strategic retreat

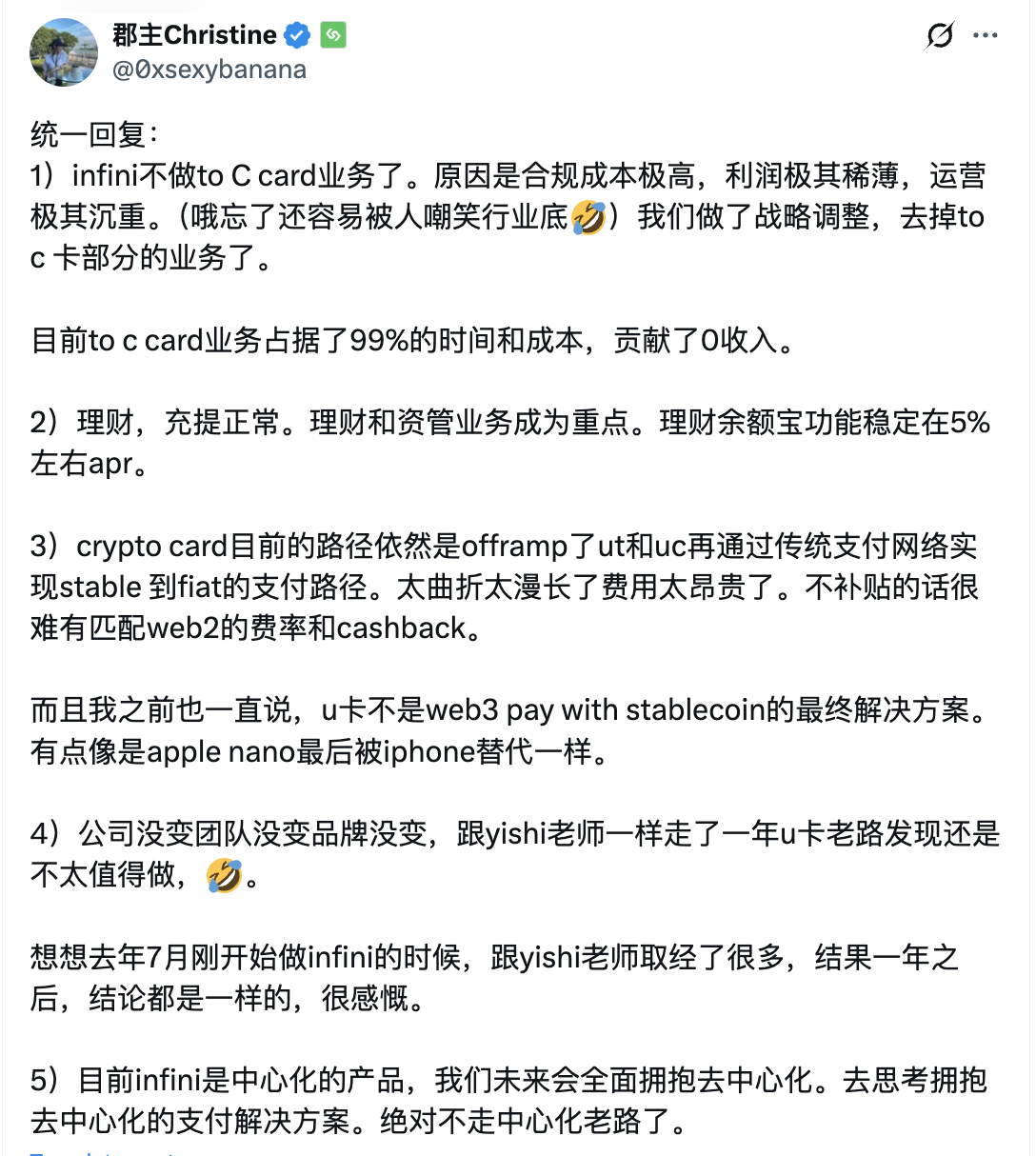

One hour after Infini officially announced the closure of the U card business, co-founder Christine further explained the reasons for this decision through the X platform. She pointed out that the decision to shut down the U card business was mainly due to high compliance costs, meager profits and high operating pressure. At present, the company will shift its focus to financial management and asset management. Christine also emphasized that the company will fully embrace decentralization, explore decentralized payment solutions, and resolutely no longer follow the old path of centralization.

Source: X (Princess Christine @0xsexybanana)

In an interview with MetaEra, Infini co-founder Christine talked about the mental journey of making this decision.

"I definitely hesitated in my heart," Christine said to the reporter. This team, which grew from an unknown small company, has accumulated a considerable user base in the Chinese-speaking region. Many community users on Twitter expressed their hope that Infini would stay, which deeply touched the team - "Everyone wants a good U card, not that we refund or close the card business."

But the decision was not made hastily. Christine revealed that the team had an in-depth discussion on whether to continue the card business early on, "This is a process of repeated thinking." The company has carefully considered future strategic adjustments to ensure that every step is in line with the direction of long-term development.

In the official announcement of the closure, Infini detailed the compensation plan for users: automatically refunding the card opening fee, ensuring the safe arrival of funds in transit, and promising to complete all refunds within 21 working days. This "start well and end well" attitude not only reflects the team's sense of responsibility, but also reflects the rare business ethics in this industry.

Two core obstacles: cost out of control and model failure

Infini U Card

During the interview, Christine deeply analyzed the two major reasons for shutting down the U card business, each of which directly pointed out the core pain points of the U card industry.

Heavy cost structure

When the reporter asked which link in the card-issuing industry chain grabbed most of the profits, Christine's answer was unexpected: "In fact, we shouldn't ask about profits, we should talk about costs first. We don't have any profits in the U card business, only costs." This statement reveals the fundamental problems of the U card industry.

Christine analyzed the cost chain of the card issuance business in detail through the actual case of Infini.

KYT and KYC costs

KYT (Know Your Transaction) and KYC (Know Your Customer) are crucial in the crypto payment industry.

KYT protects funds and ensures compliance and financial integrity by identifying and monitoring transaction risks, preventing money laundering and fraud. To prevent illegal capital inflows, Infini cooperates with Cobo, and every recharge transaction must go through KYT.

KYC is an effective means to prevent identity theft, money laundering and other illegal financial activities, and ensure the transparency and security of the financial system. Infini also introduced Sumsub's services in the KYC process.

This also means that every time KYT and KYC are performed, Infini needs to pay the corresponding fees regardless of the results.

Card and bank fees

The upstream card group fees for card issuance services cannot be ignored either. "Card group" usually refers to organizations or networks that provide card payment solutions, such as Visa, Mastercard, etc., which manage the issuance, payment, transaction settlement and other processes of bank cards. The API provided by the card group requires a fixed monthly fee, and other fees such as exchange rate conversion fees and recharge fees will also affect the cost of the business.

"We chose a people-friendly route, and many of the costs are borne by ourselves. For example, there is a fixed fee of $0.1 per card per month, and we do not charge users separately." Despite this, the cost is still high and the profit is almost zero. Christine revealed, "Generally speaking, the exchange rate conversion fee is about 1% to 1.5%, which is not charged by us, but by upstream banks and card groups. But users will feel unhappy and feel that they are at a disadvantage in the exchange rate."

Operating costs

Infini's U card business is also facing huge operational pressure. Christine pointed out that "the operational complexity of U cards is comparable to that of cryptocurrency exchanges." The operation of U cards needs to ensure the security of each transaction and provide real-time customer support, but it does not bring the same level of profitability to the project as exchanges. In order to maintain a good user experience and efficient customer service, the Infini team bears huge operating costs.

Compliance costs

When asked which link in the cost of U Card is the most expensive, Christine responded without hesitation: "You must ask me which link is the most expensive? It must be the payment license." She further explained, "Payment business needs to obtain corresponding payment licenses in different regions, such as MSO (Money Service Operator) in Hong Kong and EMI (Electronic Money Instituion) in Europe. These licenses take a long time to apply for and are expensive." She added, "Especially in the KYC and Anti-Money Laundering (AML) links, each user verification is charged." The high cost of payment licenses and compliance services makes it difficult for start-ups to move forward in this industry.

Misaligned Crypto Vision and Reality

Compared to the ideal "bridge from the crypto world to real-world payments", the real U card is showing structural limitations. For Infini, this is not a path that can be taken in the long run.

"If you want to make a profit on U Card, you can only increase the handling fee." Christine admitted that U Card lacks a more effective profit model, and raising the handling fee is not a good solution. Raising the handling fee goes against the original intention of the team to be close to the people and have low fees, and may also arouse user dissatisfaction. In fact, in many regions, users can easily exchange stablecoins such as USDT for legal currency through exchange channels, and U Card does not provide a decisive value overflow.

The more realistic problem is that the user experience of U Card is far inferior to that of Web 2.0 products. "We often receive complaints from users that they will be charged exchange rate conversion fees when using cards in places like Hong Kong and Singapore." She explained that these fees are not set by Infini, but are charged by upstream bank card groups. However, from the user's perspective, these costs ultimately fall on them. "Users think we charge them and think we make a lot of money, but in fact we don't get a penny." While bearing the burden of complex compliance and customer service, Infini has not received a return commensurate with its efforts and the understanding of users, which makes Christine believe that this model is not a sustainable long-term development path.

Coinbase U Card

Currently, leading platforms such as Coinbase and Bybit are still actively promoting the U card business. Just this year, Coinbase announced that it will launch Coinbase One Card in the fall of 2025, and users can get up to 4% of Bitcoin back for each purchase.

However, the utility of this type of U card backed by a crypto exchange for enterprises may be different from that of Infini. Christine analyzed that these platforms are more likely to regard U cards as a "fund retention tool" rather than the main source of revenue. For example, Bybit users can enjoy fee reductions after depositing large amounts of funds. By providing benefits and fee reductions to users, U cards can effectively help exchanges improve the sedimentation of funds and the long-term retention of users. In this context, U cards are more like part of the platform ecosystem, used to improve user retention and fund sedimentation, rather than a direct profit tool. She explained that these platforms already have a complete customer service, KYC and compliance system, and their operating structure is naturally suitable for conducting U card business.

For Infini, without a huge trading business to back it up, the U card has become a high-burden, low-return energy-consuming device. The lack of long-term profit logic also makes the U card path unsustainable.

The future of crypto payments: U-card is unlikely to be the end of crypto payments

Infini has always adhered to the concept of Crypto Native and provided users with payment projects that provide services such as savings, financial management, and payment. Christine believes that the current encrypted payment field has not evolved along the trend of encryption.

When Bitcoin was first created, it was envisioned as an innovative payment tool. Stablecoins in particular have the advantages of being fast, low-cost, and censorship-resistant. U Card converts stablecoins (such as USDT and USDC) into legal tender, deposits them into bank accounts, and then users spend through traditional Visa or Mastercard networks. U Card actually bypasses these advantages, converts stablecoins into legal tender, and returns to traditional payment networks, which runs counter to the original intention of crypto payments. Christine believes that U Card's practice of converting stablecoins into legal tender has not only failed to tap the potential of crypto payments, but is a "setback" for the industry.

Christine emphasized: "The ultimate goal of crypto payments is to allow every user to pay directly with stablecoins rather than relying on fiat currency payment channels. What we want is 'Pay with crypto, pay with stablecoins', rather than returning to the traditional fiat currency payment system." She further added, I think the moment when an ordinary user can directly use USDT and USDC to pay and buy things without having to go through traditional Visa and Mastercard is the "iPhone" moment for crypto payments.

In fact, stablecoin payments have a potential that cannot be ignored. According to on-chain data, on May 31, the global stablecoin market value exceeded US$250 billion, showing the huge demand for stablecoins as a payment tool. Christine believes that the "crypto-payment" market still has huge room for development.

From trial and error to reconstruction: Infini's experience accumulation and future choices

Talking about the gains of the past year, Christine half-jokingly said, "Looking back on these things, I might not have started U Card in the first place." She recalled the experience of asking Yishi, the founder of OneKey, for advice last year. Yishi explained to Christine the difficulties and pressures of U Card very sincerely. At that time, OneKey had just shut down its U Card business due to regulatory pressure.

However, Christine initially did not fully understand the complexity of compliance. "I thought it would be OK as long as I didn't touch the 'gray industry'," she said with a smile, "but that's far from the truth." After a year of practice, she experienced firsthand that the compliance pressure faced by payment businesses far exceeds that of traditional pure crypto projects, which is a major challenge that cannot be avoided in crypto payment startups.

Although the road to entrepreneurship is full of challenges, her experiences over the past year have also allowed her to gain valuable experience.

She firmly believes: "If you want to succeed in starting a business, the right time, right location and right people are all essential, and 'right people' is the most important. A good team is crucial. If the team has enough vitality and combat effectiveness, many new businesses can be successful." In the past year, Christine and her team have continuously overcome technical difficulties and formed a more efficient collaborative model in management.

In addition to the team, Christine particularly emphasized the importance of reputation. In the crypto industry, both personal character and brand reputation are very important. "In this industry, reputation is the most core asset. If the reputation is bad, it will be difficult to continue future business." She gave an example, saying that although Infini suffered a theft in February this year, the team still decided to use its own funds to fully compensate users for losses and ensure that no user suffered losses. Such a move not only won the trust of users, but also laid the foundation for the long-term development of Infini.

Looking ahead, Infini has clearly focused its development on two directions: one is to support the company's daily operations with stable financial products and establish a sustainable income base; the other is to continue to explore truly decentralized encrypted payment paths and enhance their feasibility in real-world applications.

Infini Earn

First of all, Infini will continue to strengthen its financial management product line, which is an important source of income for the company. "Because many products that can generate income are on-chain, we will open some CeFi products in the future, so that we can provide stronger risk resistance." She said: "The market is volatile. If a bear market comes, the income from lending and financial management will often decline. Therefore, we need to provide users with more diversified and safer financial products to help them maintain their income in different market environments."

In order to meet the needs of different users, Infini also plans to segment financial products. For example, she mentioned that some arbitrage products or medium- and high-frequency quantitative products are suitable for users who are willing to accept a certain lock-up period; while for users who need to deposit and withdraw funds at any time, they can still choose more flexible Lending products. She emphasized that future financial products will be differentiated according to risk levels in order to better match users' needs for liquidity and returns.

On the other hand, Christine is still confident about the future of crypto payments and hopes to continue to explore the truly decentralized crypto payment path, especially in stablecoin payments. She made it clear that the traditional card payment solution is a temporary transitional solution, and the real solution should be decentralized stablecoin payments. Stablecoin payments can achieve extremely fast settlement and extremely low costs, which is the advantage of decentralized payments. "We have spent so much time and operating costs on a temporary transitional solution, why not think about a more long-term solution?" She revealed that Infini will increase its research and development efforts on decentralized payment solutions, and is committed to enabling users to pay directly with stablecoins and get rid of traditional fiat currency payment channels. "There are already some product ideas and ideas in this area, but we also need some time to develop and test."

Summary: Finding the landing point of long-termism in reality

Speaking of the future, Christine said that Infini will always move forward as a long-term entrepreneur and firmly believe in the development prospects of encrypted payments. Speaking of the future, she said that she hopes to see the company maintain steady revenue and make substantial progress in the field of encrypted payments.

From facing compliance challenges to exploring the grand vision of decentralized crypto payments, Infini is accumulating valuable experience and steadily advancing technological innovation and business expansion. As the team continues to grow, Infini is working tirelessly to create more efficient and convenient payment solutions. Although the future is full of uncertainty, the direction Infini insists on and the experience it has accumulated are gradually building a more sustainable innovation path, which may have a profound and lasting impact on the crypto payment industry.