Crypto's Distribution Playbook: Or, the DeFi Mullet

Compiled by: Luiza, ChainCatcher

Every few years, cryptocurrencies experience their moments of glory. For most of their lives, these moments followed a predictable four-year cycle: Prices soar (often dramatically), people flock in, most lose everything, and a few hold on. This is how cryptocurrencies grow through cycles of boom and bust, with true believers remaining after each shock.

Traditional institutions appear to be playing the same game—allocating Bitcoin to their balance sheets, launching exchange-traded funds, or allowing clients to trade cryptocurrencies. Each time such a move occurs, people haile it as a turning point. However, institutional entry often signals a market top, not the beginning of a new growth cycle. "Institutional arrival" has even become a meme. They never brought in a billion new users because they never truly embraced cryptocurrency; they only dipped their toes in the water.

But this time is different because institutions aren't just testing the waters anymore. They want crypto. For the first time in history, they're going all in because it's in their best interest.

This is quite ironic, considering that cryptocurrency was originally conceived as a rebellion against traditional institutions. Its core purpose was to create a new system, a new system, independent of the existing financial system. Yet, since I entered the cryptocurrency world, I've consistently witnessed a desire for recognition from established authorities—even those they are meant to "revolt" against. Where does this desire come from? Perhaps it stems from a growing realization that replacing the entire financial system is unrealistic. The current system is built on decades of accumulated trust, and for better or for worse, most people still believe it will serve them well.

Therefore, a more realistic goal is not replacement but penetration, allowing traditional institutions to gradually abandon those outdated models—those inefficient black-box operations that are incompatible with the highly interconnected, internet-native global world.

Until recently, this seemed like wishful thinking. But in this cycle, change is no longer coming from startups on the fringe, but from top-level design.

The US government's current rhetoric coincides with what the cryptocurrency industry has advocated for years. Maintaining the dollar's status as the world's reserve currency requires leveraging every lever, and cryptocurrency is one of the most powerful. Dollar-pegged stablecoins (such as USDT and USDC) have become dominant on-chain. Rather than resisting this trend, the US government has embraced it. Stablecoins have evolved from a "novelty" to a policy tool, becoming a core economic strategy during the Trump administration.

The GENIUS Act (full name: the Crypto-Asset Transparency and Regulatory Certainty Act, aimed at regulating stablecoin issuance) requires stablecoin issuers to purchase U.S. Treasury bonds, creating a new category of buyers for U.S. debt financing. Why is this important? Because purchasing Treasury bonds not only "funds the government" but also serves as the foundation of the entire financial system. U.S. Treasuries are considered the safest asset in the world: for governments, stable demand for them maintains low interest rates and a strong dollar; for institutions, they provide predictable returns backed by the credit of the U.S. government—undoubtedly the most reliable lender in modern history.

This creates a win-win-win situation: stablecoin issuers gain scalable, interest-earning, and highly liquid assets to back their tokens; institutions gain access to a secure and large market; and the US government gains new capital channels to finance its spending without driving up interest rates. This has now become a national strategy.

The incentives here are even more striking: large banks holding trillions of dollars in customer deposits now have reason to convert their reserves into stablecoins, as the latter are inherently more efficient. Arthur Hayes (Note: former CEO of BitMEX) estimates that this will add over $10 trillion in new purchasing power to US government debt.

Where will this liquidity go? It won't all be stuck in the Treasury market. Some of it will spill over into risky assets and into cryptocurrencies, creating a cycle: stablecoin growth → Treasury bonds receive funding → liquidity spillover → crypto markets rise → stablecoins grow again.

Because of this, the institutions are no longer just dipping their toes in the water this time, but are deeply involved.

This is why this moment in time could truly be a turning point: not because crypto convinces the world to betray traditional institutions, but because traditional institutions begin to turn to crypto.

We've never encountered a situation like this: a warming government stance, active institutional involvement, a clear regulatory framework, robust infrastructure, and cross-chain interoperability solutions. Now that this long-awaited breakthrough has arrived, how can crypto teams seize the opportunity? The answer lies in: the DeFi Mullet Model.

The Mullet of DeFi

All successful new technologies achieve widespread adoption by hiding complexity. The internet was a prime example: its early days required dial-up modems, obscure commands, and the patience to endure slow connections. Even in the 1990s and early 2000s, accessing the internet meant expensive computers, clunky browsers, or trips to internet cafes. For people like me living in developing countries, these remained luxuries until the early 2010s. For nearly three decades, the internet, despite its practicality, struggled to reach widespread adoption, fundamentally due to the limitations of its distribution channels.

Until the smartphone arrived. The internet went from being a place you had to "go" to a portable tool—from full-keyboard BlackBerrys and shatter-resistant Nokias to smooth touchscreen iPhones and Android phones. The web became always online and available. This shift not only broke down barriers to access but also created a whole new demand: billions of people who had never imagined needing the internet suddenly became dependent on it. Without smartphones, the internet might have remained limited to just a few million users.

Artificial intelligence similarly experienced its "ChatGPT moment" a few years ago. Previously, AI existed primarily in research papers, GitHub repositories, and developer APIs. But with the advent of accessible chat interfaces, generative AI quickly reached millions of users, who began using it to write emails, code, and conduct daily tasks. This was AI's mainstream transition: from a niche tool to a global phenomenon.

Two data are enough to explain everything:

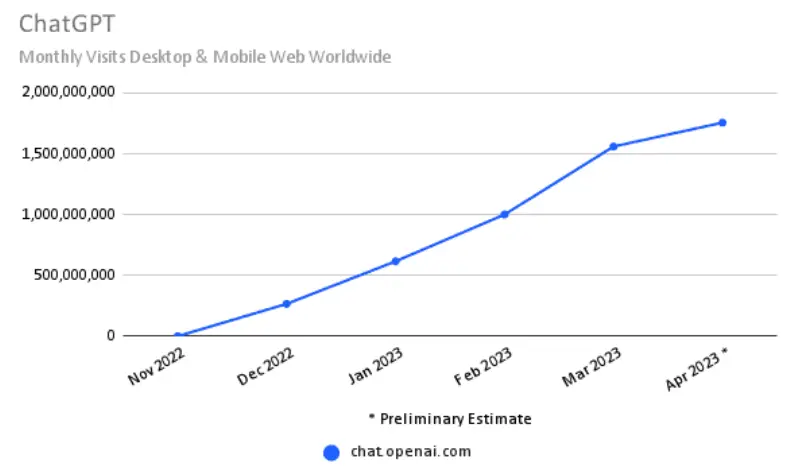

1. Record-breaking user adoption. ChatGPT surpassed 100 million monthly active users just two months after its launch at the end of 2022, a feat achieved by TikTok in nine months and Instagram in over two years.

2. Viral expansion of user engagement: OpenAI website visits soared from 152.7 million in November 2022 to 1.6 billion in March 2023, an increase of more than tenfold in four months.

Image source: similarweb Blog

Cryptocurrency is also awaiting its own "ChatGPT moment." The technology is mature, the infrastructure is in place, but the only thing missing is a channel for widespread adoption. Just as the internet needed smartphones, AI needed ChatGPT, and cryptocurrency needs its own interface revolution.

You can't expect billions of people to use decentralized exchanges or manage self-hosted wallets—my parents never learned that. But if their banking apps suddenly offered stablecoin payments or crypto yields, they'd try it. That's the most realistic path to a billion users.

I call this the "grandmother test." Cryptocurrency has yet to pass this test: you can't have your grandmother navigate a DeFi interface and deal with wallets, gas fees, or slippage. But if PayPal uses an on-chain yield mechanism in the backend, and the frontend simply presents her with a "5% yield savings account," she can simply click to participate—an approach she's perfectly fine with.

This is the "Mullet Head Model": traditional fintech on the front end, decentralized finance on the back end. Just as smartphones enabled this transformation for the internet, and ChatGPT enabled this breakthrough for AI, the Mullet Head strategy is poised to revolutionize cryptocurrency as well.

To the user, all they see is a loan or yield product offered by a bank, PayPal, or Coinbase; underneath, the transaction is being executed on-chain via a censorship-resistant protocol. Users don’t need to see or understand the complexity.

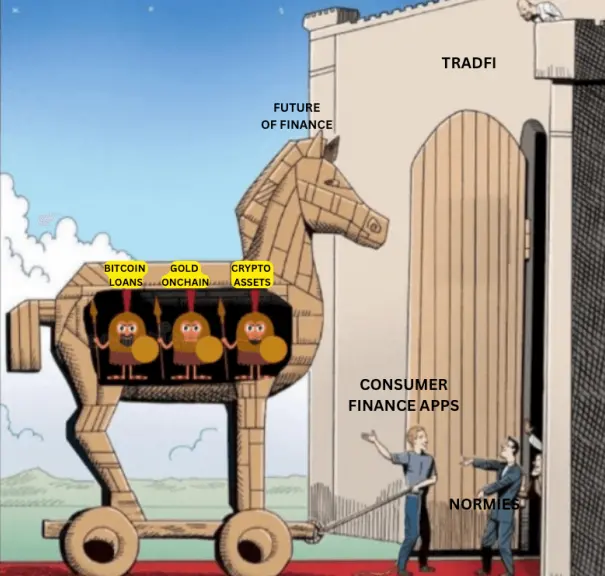

The Trojan Horse in the Castle of Traditional Finance

The DeFi mullet strategy is no longer a theory; it has become a Trojan horse for attacking the castle of traditional finance.

A prime example is the collaboration between Coinbase and Morpho. From a user's perspective, it's just a standard Coinbase feature: a clear button offering Bitcoin mortgage loans. However, after clicking the button, the loan actually comes from Morpho's on-chain lending market. Users don't see DeFi, only the word "loan."

This completely upends the traditional cryptocurrency business model. In the past, we always expected users to proactively adapt to the crypto world—learning how to use wallets, cross-chain transactions, pay gas fees, bridge assets, and operate decentralized exchanges. We stubbornly assumed that if "the product was good enough," "the returns were attractive enough," and "self-custody was essential," savvy users would naturally embrace DeFi! While this philosophy demonstrates a commitment to the cypherpunk spirit, it naively assumes that the world is willing to play by the same rules. Claiming "we don't need those users" may seem principled, but in reality it's a form of self-imposed imprisonment—like allowing business opportunities to slip away by refusing to improve packaging.

The DeFi mullet model completely shifts the narrative, putting us back on track: providing services within existing user scenarios (exchanges, bank portals, consumer finance apps). We offer consistent core products—lending, redemption, and yield—but hide the technical details that users don't care about, removing the cognitive barriers we once forced them to overcome.

For example, Coinbase and Morpho ultimately present users with only the core action: staking Bitcoin to receive USD. All other complexities are pushed to the background, returning to their proper place.

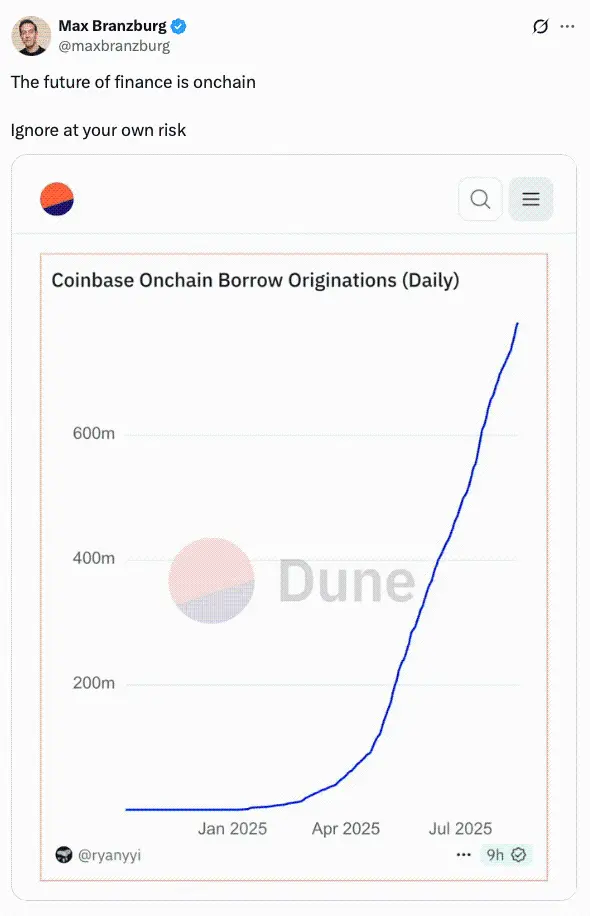

Early data strongly proves that the mullet strategy is feasible.

The path to scale for cryptocurrency is clear: encounter it in familiar scenarios. Today, the use cases of the “mullet model” are growing.

• Kraken x Ink x Aave: Institutional-grade on-chain DeFi lending distributed through retail channels

•Coinbase x Velodrome: On-chain liquidity behind the consumer interface

•ZeroHash x Mastercard x Chainlink: Credit card-backed tokens + DEX crypto payments

•SharpLinkGaming x Ethereum: Nasdaq-listed company gains DeFi benefits through digital asset tokens (DAT)

If the DeFi mullet model continues to be effective, the next billion users will use DeFi without realizing it.

Skeptics dismiss this as an "empty narrative," but that's precisely its power—narratives are how humans understand new technologies. "Bitcoin as a store of value" is also a narrative. No one on Wall Street cares about the Bitcoin network or blockchain technology; they simply want to buy BTC as an inflation hedge and store of value. The mullet model follows the same logic: compressing difficult-to-explain technical details into simple, palpable concepts.

More importantly, the Mullet model represents a paradigm shift in how products are built and distributed. Building products for crypto-savvy DeFi users is one thing, but the vast majority of people outside the industry only care about the results: dollars, returns, credit, tokens.

The mullet model provides entrepreneurs, investors, and regulators with a new approach to product development and promotion: you don’t need to drag a billion users into DeFi; you just need to quietly embed DeFi into the applications they already use.

Now is a historic moment

Traditional finance is no longer just dabbling in the cryptocurrency space. Pilot projects and tentative partnerships have been replaced by a full-scale embrace. Institutions like Robinhood, Stripe, Coinbase, and Circle are building blockchains, acquiring companies, and integrating crypto into their core architectures. Trillion-dollar asset management giants like Franklin Templeton and BlackRock are migrating their core currency markets on-chain. These traditional financial giants are investing real money in their cryptocurrency businesses, developing dedicated strategies, and establishing distribution channels. More notably, even the "Project Crypto" initiative launched by the U.S. Securities and Exchange Commission (SEC) hints at opening up on-chain access for the entire financial industry.

For banks and fintech companies, the "mullet model" is the optimal solution. Building DeFi infrastructure in-house is time-consuming and expensive, requiring a mature team versed in crypto markets and technologies. Rather than spending years developing in-house infrastructure, it's better to integrate into an existing ecosystem—in a fast-paced market, time is the most significant cost. Embracing the DeFi mullet model is clearly more economical, agile, and sensible.

Simply saying, "Institutions should use our technology" is insufficient. This is like telling people in 1995, "Businesses should run on the internet because TCP/IP is mature"—technical maturity doesn't guarantee user adoption. DeFi teams must proactively reach out to institutions. This doesn't mean abandoning decentralization or self-custody, but rather packaging existing technology into a form that institutions can directly use.

Institutions are most concerned about three core areas:

• Compliance: Never cross regulatory red lines. If the DeFi team does not build a comprehensive KYC, reporting, and risk management interface, institutions will not even consider joining;

• Reliability: For seasoned cryptocurrency users who "go to Discord to find solutions when things go wrong," occasional protocol volatility may be acceptable; however, institutions require "deterministic guarantees." This includes service availability (uptime) protocols, penetration testing reports, and clear problem-handling processes. For DeFi developers, wrappers, software development kits (SDKs), and service agreements may not be "cool enough," but it is these tools that give institutions peace of mind.

Looking at the bigger picture, most obstacles lie not with the protocols themselves, but with the last mile. This may seem like tedious labor to some DeFi users and builders, but now is the time to let go of that obsession and develop tools that truly bring cryptocurrency to the masses.

The "DeFi Mullet" model is now widely known, but what is the "Interop Mullet" model? As you may know, the problem of "interoperability" in cryptocurrency has been solved, and the relevant tools are in place—meaning that fintech companies and institutions can smoothly enter the on-chain world and fully unleash the potential of the crypto internet capital market.

The core of the DeFi mullet model is to "abstract the application layer of cryptocurrency" (for example, hiding the Morpho protocol under a button on Coinbase);

The cross-chain interoperability mullet model focuses on abstracting the cryptocurrency infrastructure layer—for example, hiding the cross-chain bridges, blockchain networks, and decentralized exchanges that the LI.FI protocol relies on to execute transactions, or the stablecoin issuance technology supported by the cross-chain interoperability protocol and its proprietary token standard. It's like "another mullet under the mullet model," providing the underlying technical support.

Interoperability: The mullet beneath the mullet

Viewing DeFi as the ultimate solution to crypto's application challenges is like assuming that improving car comfort will solve traffic congestion. The real problem lies beneath the cars—the roads themselves.

The beauty of the crypto ecosystem is that it's not a unified internet of value, but a multiverse comprised of hundreds of chains, each embodying its builders' unique vision for scalable blockchains. This fragmentation is both a source of charm and a barrier to mass adoption, and interoperability is the key to breaking through.

Interoperability and DeFi can also accelerate the process of institutions launching crypto products. The following two cases are very representative:

•Stablecoin issuance: Today, everyone is eager to launch their own stablecoins, including cryptocurrency companies, fintech companies, banks, and even local governments. By 2025, the question of whether to issue a stablecoin will no longer be "whether to issue a stablecoin"; the key question will be "when to issue it." As countries like the United States "step up the accelerator to promote the popularization of cryptocurrencies so that their national currencies can circulate through cryptocurrency infrastructure," everyone is eager to join this "stablecoin gold rush." In the current cryptocurrency ecosystem, the best (or even the only legal) way to launch a "future-proof" stablecoin is to adopt a "cross-chain interoperable token standard." Such standards can not only significantly shorten the time it takes to issue a stablecoin, but also significantly reduce the technical and operational costs of the issuance process. At the same time, the issuer can still retain control of the token contract, ensure security, and collect related fees, achieving a "win-win for all parties."

• Asset exchange (same chain, cross-chain, cross-chain bridge exchange)

In the cryptocurrency space, the demand for asset exchange has never disappeared. This means that companies like exchanges, wallets, deposit channels, and custodians will always need to provide "asset exchange" services for themselves or their users.

Final Chapter

The core challenges of the crypto space have long been technological breakthroughs: scalability, consensus mechanisms, and interoperability. Top talent has largely solved these problems, and the infrastructure is already in place.

The central challenge now shifted: it was no longer about building an engine but about creating a car that people actually wanted to drive. The mullet model was the blueprint for that car.

The crypto industry has created a $4 trillion economy driven by idealistic optimism about building a better world; pragmatism will be the key to success in the next phase of its journey. The Mullet Model embodies this pragmatism—it recognizes that the traditional financial world possesses what crypto needs most: distribution channels. This is the most direct path to making cryptocurrency accessible to everyone. Builders who understand this will ultimately shape the future.