By Arthur Hayes, Founder of BitMEX

Compiled by AIMan, Golden Finance

U.S. Treasury Secretary Scott Bessent deserves a new nickname. I previously called him BBC, short for Big Bessent Cock. Yes, his destructive penis is destroying the status quo of the global financial ecosystem, but that nickname doesn't do him justice. I believe he needs a more apt name to describe the pain he will inflict on two crucial components of the fiat (fugazi) financial system: the Eurodollar banking system and foreign central banks.

Like the serial killer in The Silence of the Lambs (a damn near classic worthy of a Netflix and Chill night for any uninitiated young person), Scott "Buffalo Bill" Bessant is about to eliminate the Eurodollar banking system and seize control of foreign non-dollar deposits. Just as slaves and trained legions maintained the Pax Romana, slaves and dollar hegemony maintain the Pax Americana. The slavery aspect of the Pax Americana isn't just about the historical importation of Africans to pick cotton; the modern whip is the monthly mortgage, with generations of young people willingly taking on life-crushing debt to earn worthless credentials in the hopes of landing a job at Goldman Sachs, Sullivan & Cromwell, or McKinsey. It's a far more widespread, insidious, and ultimately more effective form of control. Unfortunately, now that America has artificial intelligence (AI), these debt-ridden oxen are about to be out of work... put on your blue-collar work clothes, man.

I'm getting off topic.

This article discusses Pax Americana's control over the global reserve currency, the US dollar. Successive US Treasury Secretaries have wielded the dollar with varying degrees of success. Their most notable failure was allowing the Eurodollar system to emerge.

The Eurodollar system emerged in the 1950s and 1960s as a means of circumventing US capital controls (such as Regulation Q), circumventing economic sanctions (the Soviet Union needed a place to store its dollars), and providing banking services for non-US trade flows during the post-World War II global economic recovery. Monetary authorities at the time could have recognized the need to supply dollars to foreigners and allowed domestic money center banks to control this business, but domestic political and economic concerns demanded a firm stance. Consequently, the Eurodollar system grew to untold proportions over the ensuing decades, becoming a force to be reckoned with. An estimated $10 to $13 trillion in Eurodollars flowed through various non-US bank branches. The ebb and flow of this capital contributed to the various financial crises of the post-World War II era, which invariably required the printing of money to resolve. This phenomenon was discussed in an August 2024 paper by the Atlanta Federal Reserve titled "Offshore Dollars and US Policy."

For Bessant, the problems with the Eurodollar system were twofold. The first was that he had no idea how many Eurodollars existed or what they were financing. The second, and most important, problem was that these Eurodollar deposits weren't being used to buy his junk Treasury bonds. Could Bessant solve these two problems? With this in mind, let me quickly discuss the foreign currency holdings of non-US retail depositors.

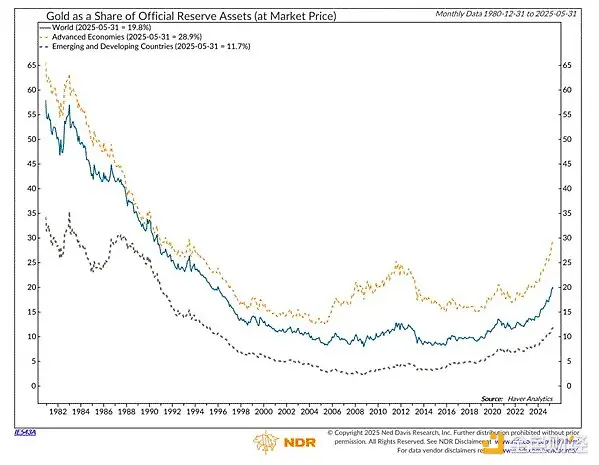

De-dollarization is real. It truly began in 2008, when America's monetary masters decided not to let banks and financial institutions fail due to their poor bets but to rescue them by launching quantitative easing (QE Infinity). A useful indicator of the reaction of global central banks, which hold trillions of dollars in assets, is the percentage of gold held in their reserves. The higher the percentage of gold held in a person's reserves, the less trust they have in the US government.

As you can see in the chart above, after 2008 the percentage of gold in central bank reserves bottomed out and began a long-term rise.

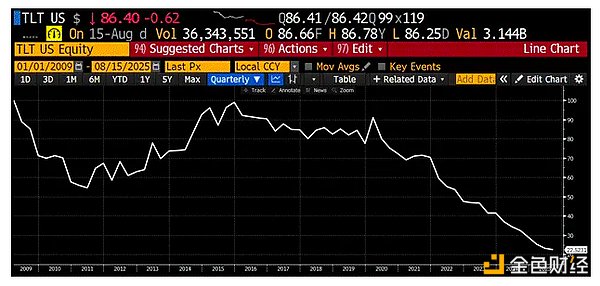

This is the TLT US ETF, which tracks the performance of U.S. Treasury bonds with maturities of 20 years or longer, divided by the price of gold. I've set its index at 100 since 2009. Since 2009, Treasury bonds have lost nearly 80% of their value relative to gold. The U.S. government's monetary policy has been to bail out its banking system while simultaneously penalizing foreign and domestic debt holders. No wonder foreign central banks are beginning to emulate Scrooge McDuck (the gold-hoarding cartoon character). U.S. President Trump intends to follow a similar strategy, but in addition to penalizing bondholders, he believes he can make America great again by taxing foreign capital and trade flows through tariffs.

There's really not much Bessant can do to convince central bank reserve managers to buy more Treasuries. However, from a dollar perspective, there's a large, underbanked segment of the Global South who crave a positive-yielding dollar account. As you know, all fiat currencies are garbage compared to Bitcoin and gold. That being said, if you're in a fiat currency system, the best fiat currency is the dollar. Domestic regulators who rule most of the world's population force their citizens to hold low-quality currencies plagued by hyperinflation and restrict their access to the dollar financial system. These citizens will buy T-bills at any yield Bessant offers, simply to escape their struggling government bond market. Is there any way Bessant can provide banking services to these people?

I first traveled to Argentina in 2018 and have been going regularly since. This is a chart of ARSUSD indexed to 100 starting in September 2018. The Argentine peso has depreciated 97% against the US dollar in seven years. Currently, when I go skiing there, I pay all my service fees in USDT.

Bessant has discovered a new tool that solves his problem. It's called a stablecoin. Dollar-pegged stablecoins are now being promoted by the US Treasury. The Empire will support selected issuers as they siphon off Eurodollars and retail deposits from the Global South. To understand why, I'll quickly outline the structure of an "acceptable" dollar-pegged stablecoin. Then, I'll discuss the implications for the traditional financial (TradFi) banking system. Finally, and this is what all you degenerates are here for, I'll explain why global adoption of a dollar-pegged stablecoin backed by Pax Americana will drive long-term growth in DeFi applications, particularly Ethena, Ether.fi, and Hyperliquid.

As you know, Maelstrom doesn't do this for free. We hold massive, massive, massive positions.

If you’re still new to stablecoins, I’d like to share a preview of a new stablecoin infrastructure project we’re advising on — Codex — which I believe will be the top performing token from its upcoming Token Generation Event (TGE) until the end of this cycle.

What are acceptable stablecoins?

A stablecoin pegged to the US dollar is similar to a narrow bank. Stablecoin issuers accept US dollars and invest these dollars in risk-free debt instruments. The only nominally risk-free debt instrument for the US dollar is a Treasury bond. Specifically, because issuers must be able to provide physical US dollars on demand when holders redeem them, stablecoin issuers will only invest in short-term Treasury bills (T-bills). T-bills have maturities of less than one year. Because they carry little or no duration risk, they trade like cash.

Let's look at the process.

Create a stablecoin with one unit. I’ll use Tether USD (code: USDT) as an example:

1. The Authorized Participant (AP) wires USD to Tether’s bank account.

2. Tether creates 1 USDT for every 1 USD deposited.

3. In order to earn US dollar returns, Tether purchases government bonds.

If the AP wires $1,000,000 USD, they will receive 1,000,000 USDT.

Tether purchases $1,000,000 worth of Treasury bonds.

USDT does not pay interest.

but

The interest rate paid on Treasury bonds is essentially the Fed Funds rate, which is currently 4.25% to 4.50%.

Tether’s net interest margin (NIM) is 4.25% to 4.50%.

To attract deposits, Tether or affiliated financial institutions (such as cryptocurrency exchanges) will pay a portion of the net interest margin when depositors stake their USDT. Staking simply means locking up your USDT for a period of time.

To redeem one unit of stablecoin:

1. AP sends USDT to Tether’s crypto wallet

2. Tether sells Treasury bonds equivalent to the USDT amount.

3. Tether sends 1 USD to the AP’s bank account for every 1 USDT.

4. Tether destroys USDT and removes it from circulation.

Tether's business model is straightforward. Accept US dollars, issue digital tokens running on a public blockchain, invest those dollars in Treasury bonds, and earn a net interest margin. Besant will ensure that issuers, tacitly endorsed by the Empire State through legal means, can only deposit US dollars in chartered US banks and/or hold Treasury bonds. No fancy tricks allowed.

Impact on Eurodollars

Before the advent of stablecoins, when Eurodollar banking institutions ran into trouble, the Federal Reserve and the U.S. Treasury always stepped in to bail them out. A well-functioning Eurodollar market was essential to the health of the empire. But now, there's a new tool that allows Besant to absorb these flows. At the macro level, Besant must provide a reason to move Eurodollar deposits on-chain.

For example, during the 2008 global financial crisis, the Federal Reserve secretly lent billions of dollars to foreign banks that were short on dollars due to the chain reaction of the collapse of subprime mortgages and related derivatives. As a result, Eurodollar depositors believed the US government implicitly guaranteed their funds, even though they were technically outside the US-regulated financial system. Declaring that non-US bank branches would receive no assistance from the Fed or Treasury in the event of another financial crisis would redirect Eurodollar deposits into the arms of stablecoin issuers. If you think this is far-fetched, a Deutsche Bank strategist wrote an article openly questioning whether the US would weaponize dollar swap lines to force Europeans to do what the Trump administration demands. You better believe Trump would love nothing more than to emasculate the Eurodollar market by effectively eliminating its banking services. These institutions eliminated his family's banking services after his first term; now it's payback time. Karma.

Without guarantees, Eurodollar depositors will act in their best interest and move their funds into dollar-pegged stablecoins like USDT. Tether holds all of its assets as US bank deposits and/or Treasury bonds. By law, the US government guarantees all deposits at eight "too big to fail" (TBTF) banks; following the 2023 regional banking crisis, the Federal Reserve and the Treasury effectively guaranteed all deposits at any US bank or branch. The default risk on Treasury bonds is also zero, as the US government will never voluntarily go bankrupt, as it can always print money to repay Treasury bond holders. Therefore, stablecoin deposits are risk-free in nominal dollars, but Eurodollar deposits are now not.

Soon, the issuers of stablecoins pegged to the US dollar will see $10-13 trillion in inflows and subsequent purchases of Treasury bonds. Stablecoin issuers become a large, price-insensitive buyer of Bessant’s dogshit paper!

Even if Fed Chairman Powell continues to obstruct Trump's monetary agenda by refusing to cut interest rates, end quantitative tightening (QT), and restart quantitative easing (QE), Bessant can issue Treasury bonds at interest rates below the federal funds rate. He can do this because stablecoin issuers, in order to profit, must buy whatever he sells at the yield offered. With a few moves, Bessant has gained control of the front end of the yield curve. The Fed's continued existence has become meaningless. Perhaps a Bernini-style statue of Bessant, in the style of "Perseus with the Head of Medusa," will stand in a plaza in Washington, D.C., titled "Bessant with the Head of the Jekyll Island Monster (i.e., the Federal Reserve)."

Impact on the Global South

American social media companies will become Trojan horses, destroying the ability of foreign central banks to control the money supply of their citizens. In the Global South, the penetration of Western social media platforms (Facebook, Instagram, WhatsApp, and X) is comprehensive.

I have spent half my life in the Asia-Pacific region. Converting depositors’ local currencies into US dollars or US dollar equivalents (such as the Hong Kong dollar) so that capital can access US dollar returns and US stocks makes up a large part of investment banking business in the region.

Local monetary authorities are playing whack-a-mole with traditional financial institutions, shutting down programs that allow capital to flow out. The government needs the capital of ordinary people and, to some extent, is isolating the capital of wealthy, non-politically connected individuals so that it can impose inflation taxes, prop up underperforming national champions, and provide cheap loans to heavy industry. Even if Bessant wanted to use large US money-center banks as a vanguard to provide banking services to these desperate people, local regulators would prohibit it. But there is another, more efficient way to access this capital.

Except in mainland China. Everyone uses Western social media companies. What if WhatsApp launched a crypto wallet for every user? Within the app, users could seamlessly send and receive approved stablecoins like USDT. With this WhatsApp stablecoin wallet, users could send money to any other wallet on various public blockchains.

Let’s use a fictional example to illustrate how WhatsApp could provide digital dollar bank accounts to billions of members of the Global South.

Fernando, a Filipino, ran a click farm in rural Philippines. Essentially, he created fake followers and impressions for social media influencers. Because all his clients were outside the Philippines, he found receiving payments difficult and expensive. WhatsApp became his primary payment method because it provided a wallet that could send and receive USDT. His clients, who also had WhatsApp, were happy to stop using their crappy banks. Both parties were happy with this arrangement, but it involved intermediary work in the local Philippine banking system.

After a while, the Bangko Sentral ng Pilipinas noticed that a large and growing portion of bank funds had vanished. They realized that WhatsApp had spread its dollar-pegged stablecoin throughout the economy. The central bank had effectively lost control of the money supply. Yet, there was nothing they could do. The most effective way to prevent Filipinos from using WhatsApp would be to shut down the internet. Beyond that, even putting pressure on local Facebook executives (if any) would be futile. Mark Zuckerberg ruled from his bunker in Hawaii. And he had the Trump administration's blessing to roll out the stablecoin feature globally to Meta users. Any internet laws that disadvantaged American tech companies would result in hefty tariffs from the Trump administration. Trump had already threatened the European Union with higher tariffs unless they abandoned their "discriminatory" internet legislation.

Even if the Philippine government could remove WhatsApp from the Android and iOS app stores, motivated users could easily circumvent the blockade by using a VPN. Of course, any form of friction will inhibit the use of internet platforms, but social media is essentially an addictive drug. After more than a decade of constant dopamine rushes, civilians will find any workaround to continue destroying their brains.

Finally, Bessent could wield his sanctions weapon. Asian elites keep their money in US dollars in offshore banking centers. They clearly don't want their wealth eroded by inflation through their monetary policies. Do as I say, not as I do. Suppose Philippine President Bongbong Marcos threatens Meta. Bessent could immediately strike back with sanctions against him and his cronies, freezing their billions of dollars in offshore wealth unless they capitulate and allow stablecoins to proliferate domestically. His mother, Imelda, knew all too well the reach of US law, having defeated RICO charges stemming from allegations that she and her late husband, former dictator Ferdinand Marcos, embezzled Philippine government funds to purchase New York City real estate. I doubt Marcos would be eager for a second round.

If my argument is correct, and stablecoins are part of the US hegemon's monetary policy to expand the use of the dollar, then the empire will protect US tech giants from retaliation from local regulators for providing dollar banking services to civilians. These governments are powerless to do anything about it. Assuming I'm right, what is the total addressable market for potential stablecoin deposits from the Global South? The most advanced group of countries in the Global South is the BRICS. We exclude China, as it's ineffective against Western social media companies. The question is, what is the best estimate of local currency bank deposits? I asked Perplexity, and its answer is $4 trillion. I know this might be controversial, but let's add the Euro-poor-eans to this group. I believe the euro is a dead end, as Germany-first, then France-first, economic policies will fragment the monetary union. With the arrival of capital controls, by the end of this century, the euro's only use will be to pay for admission to Berghain, the renowned electronic music club in Berlin, Germany, and the minimum stay at Shellona, a beach club on the French Caribbean island of St. Barths. When we add the $16.74 trillion in European bank deposits, the total is close to around $34 trillion up for grabs.

Go big or go home

Bessant has a choice: go big or become a Democrat. Does he want Team Red to win the 2026 midterms and, most importantly, the 2028 presidential election? I believe he does. If so, the only way to win is to fund Trump so he can give away more free stuff to the people than the Mamdans and AOCs (referring to the radical left). Therefore, Bessant needs to find a buyer for Treasury bonds that is not price-sensitive. Clearly, given his public support for the technology, he believes stablecoins are part of the solution. But he needs to go all in.

If Eurodollars and the deposits of the poor in the Global South and Europe do not flow into stablecoins, he must Bismarck them with his star-studded “members” (referring to sanctions and other means). Either he rubs dollars on his skin (referring to accepting dollarization) or he will be sanctioned again.

$10 to $13 trillion in purchasing power for national debt comes from the collapse of the Eurodollar system.

$21 trillion in purchasing power for national debt comes from retail deposits of poor people in the Global South and Europe.

Total = $34 trillion

Obviously, not all of this capital will flow into USD-pegged stablecoins, but at least we have a huge total addressable market (TAM).

The real question is, how will the rise of $34 trillion in stablecoin deposits drive DeFi usage to new heights? If there’s a credible argument that DeFi usage will increase, which shitcoins will skyrocket?

Stablecoins flow into DeFi

The first concept readers must understand is staking. Let's imagine that some of that $34 trillion is now held in stablecoins. For simplicity, let's assume that Tether's USDT receives all inflows. Faced with intense competition from other issuers like Circle and large TBTF banks, Tether must pass on some of its net interest margin to holders. It does this by partnering with exchanges, where USDT staked in connected exchange wallets earns some interest in the form of newly minted USDT units.

Let's look at a simple example.

Fernando from the Philippines has 1,000 USDT. PDAX, a Philippines-based cryptocurrency exchange, offers a 2% yield on staked USDT. PDAX has created a staking smart contract on Ethereum. Fernando stakes his 1,000 USDT by sending it to the smart contract address. Several things happen:

1. His 1,000 USDT becomes 1,000 psUSDT (PDAX Staked USDT; PDAX's liabilities). Initially, 1 USDT = 1 psUSDT, but each day psUSDT becomes more valuable than USDT due to accrued interest. For example, using a 2% annual interest rate and ACT/365 simple interest accounting, psUSDT gains approximately 0.00005 per day. After one year, 1 psUSDT = 1.02 USDT.

2. Fernando receives 1000 psUSDT to his exchange wallet.

Something powerful just happened. Fernando locked his USDT in PDAX and received an interest-bearing asset in return. psUSDT is now collateralized within the DeFi ecosystem. This means he can trade it for another cryptocurrency; he can borrow against it; he can use it as leverage to trade derivatives on DEXs, and so much more.

What happens when Fernando wants to redeem his psUSDT for USDT a year later?

1. Fernando goes to the PDAX platform and unstakes 1,000 psUSDT by sending it to his exchange wallet and/or connecting a third-party DeFi wallet (such as Metamask) to the PDAX dApp.

2. psUSDT is destroyed and he receives 1020 USDT.

Where does the extra 20 USDT paid to Fernando come from? It comes from Tether's partnership with PDAX. Tether has a positive net interest margin, which is simply the interest income earned on its Treasury bond portfolio. Tether then uses these USDT to create additional USDT and sends a portion to PDAX to fulfill its contractual obligations.

Both USDT (the base currency) and psUSDT (the interest-bearing currency) have become acceptable collateral throughout the DeFi ecosystem. Consequently, a certain percentage of total stablecoin traffic will interact with DeFi dApps. Total Value Locked (TVL) measures this interaction. Every time a user interacts with a DeFi dApp, they must lock up their capital for a period of time, represented by TVL. TVL is at the top of the funnel, along with transaction volume or other revenue-generating activities. Therefore, TVL is a leading indicator of future cash flows for DeFi dApps.

Before we examine how TVL impacts the future earnings of several projects, I want to explain the key assumptions in the financial model we’ll be using.

Model assumptions

I will soon present three simple yet powerful financial models that estimate target prices for Ethena (token: ENA), Ether.fi (token: ETHFI), and Hyperliquid (token: HYPE) by the end of 2028. I predict the end of 2028 because that's when Trump leaves office. My underlying assumption is that Team Blue (the Democrats) is slightly more likely to win the presidency than Team Red (the Republicans). That's because Trump cannot successfully rectify the injustices inflicted on his base over a half-century of accumulated monetary, economic, and foreign policy within four years. The rat poison on the cake is that no politician will deliver on all their campaign promises. Consequently, voter turnout among the average Republican voter in Team Red will decline.

The rank-and-file members of the Red Team will be indifferent to any successor to Trump running for president, and won't turn out in sufficient numbers to outvote those childless cat ladies afflicted with Trump Derangement Syndrome (TDS). TDS will plague any Blue Team Democrat who ascends to the throne, leading them to adopt nose-splitting monetary policies simply to prove they're different from Trump. Ultimately, no politician can resist the temptation to print money, and dollar-pegged stablecoins are among the best price-insensitive buyers of short-term Treasuries. Therefore, they may not initially support stablecoins wholeheartedly, but the new emperor will realize they're practically naked without this capital and will ultimately continue the policies I discussed earlier. This policy swing will burst the crypto bubble and lead to an epic bear market.

Finally, the numbers mentioned in my model are enormous. This is a once-in-a-century shift in the global monetary architecture. Most of us, unless we're receiving intravenous stem cell injections for the rest of our lives...perhaps, will never witness such an event again in our investing careers. The upside potential I predict is greater than Sam Bankman-Fried's amphetamine habit. You will never again see a bull run like this in the DeFi mainstays that profit from the surge in dollar-pegged stablecoins.

Because I like to use decimal numbers ending in zero for my predictions, I estimate that by 2028, the total amount of USD stablecoins in circulation will be at least $10 trillion. This number is large because the deficit Bessant must finance is enormous and growing exponentially. The more Bessant uses Treasury bonds to finance his government, the faster the debt pile grows, as he must roll over the debt every year.

The next key assumption is the level of the federal funds rate chosen by Bessant and the incoming Fed Chair after May 2026. Bessant has publicly stated that the federal funds rate is 1.50% higher, while Trump has typically called for a 2.00% rate cut. Given that there tends to be overshoots, whether up or down, I believe the federal funds rate will quickly fall to around 2.00%. There's no real rigor to this number, just as there is no real rigor among all the establishment economists. We're all making it up, so my numbers are as good as theirs. The political and economic realities of a bankrupt empire demand cheaper money, and a 2% federal funds rate provides just that.

Finally, where do I think the 10-year Treasury yield will land? Bessant's goal is to generate 3% real growth. Adding a 2% federal funds rate (theoretically representing long-term inflation), we get a 10-year yield of 5%. I'll use this to calculate the present value of the terminal return.

Using these assumptions, we derive the terminal value of the cumulative cash flows. Because these cash flows can be provided as buybacks to token holders, we can use this as the fundamental value of a particular project. This is how I evaluate and project the fully diluted valuation (FDV). I then compare the future output of my model to the current value, and, bam, the upside potential becomes clear.

All model inputs are blue, and all outputs are black.

Stablecoin consumption

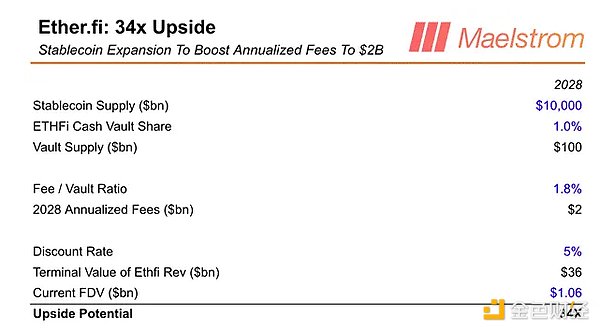

The most important action for new stablecoin users is spending on goods and services. By now, everyone is used to tapping their phone or debit/credit card on some sort of POS system to pay for things. Using stablecoins must be just as easy. Is there a project that allows users to deposit stablecoins into a dApp and spend them just like using a Visa debit/credit card? Of course there is, and it's called Ether.fi Cash.

Users around the world can sign up in minutes, and once they complete the registration process, they'll have their own Visa-backed stablecoin spending card. You can use it on your phone and/or with a physical card. Once you've deposited your stablecoins into your Ether.fi wallet, you can spend them anywhere Visa is accepted. Ether.fi can even extend credit based on your stablecoin balance to turbocharge your spending.

I'm an advisor and investor in the Ether.fi project, so I'm obviously biased, but I've been waiting for a low-fee crypto solution for offline spending for over a decade. Whether I use an American Express card or an Ether.fi cash card, the customer experience is the same. This is important because for the first time, many people in the Global South will be able to pay for goods and services anywhere in the world using a payment method powered by stablecoins and Ether.fi.

The real profit lies in becoming a financial supermarket, offering many of the traditional products offered by banks. Ether.fi can then offer additional products to depositors. The key ratio I projected to calculate future cash flows is the Fee/Vault Ratio. How much revenue does Ether.fi earn for every dollar of stablecoin deposited? To come up with a reliable figure, I consulted the latest annual filings of JPMorgan Chase, the world's best-run commercial bank. On a base of $1.0604 trillion in deposits, they earned $18.8 billion in revenue, a fee/value ratio of 1.78%.

Ether.fi Cash Vault %: This represents the percentage of the stablecoin supply that is deposited into the Cash Vault. Currently, after only four months of existence, this percentage is 0.07%. Given that the product has just launched, I believe it is possible to increase this percentage to 1.00% by 2028.

I believe ETHFI can rise 34x from its current levels.

Now that civilians can spend their dollars, is there a way to earn a higher yield than the federal funds rate?

Stablecoin lending

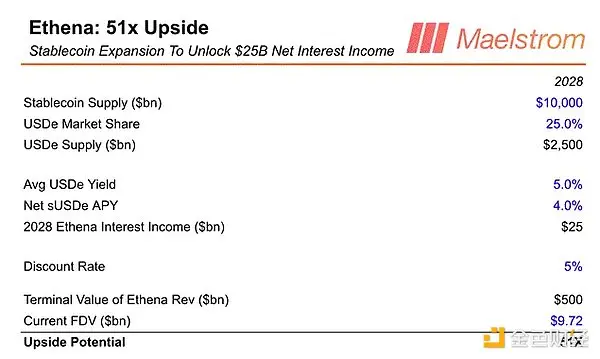

Once millions of people can go out and spend their stablecoins on coffee, they'll want to earn interest. I've already discussed my belief that issuers like Tether will pay out some of the net interest margin to holders. But it won't be a huge amount; many savers will seek higher yields without taking on excessive additional risk. Are there new endogenous yields within the crypto capital markets that stablecoin users can capture? Of course, there are, and Ethena offers the opportunity for higher returns.

There are only two ways to safely lend money in the crypto capital markets: to speculators through derivatives, or to crypto miners. Ethena focuses on lending to long crypto speculators by shorting cryptocurrency/USD futures and perpetual contracts. This is a strategy I called "cash and carry" when I popularized it at BitMEX. I subsequently wrote an article titled "Dust on Crust," in which I implored a brave entrepreneur to package this deal and offer it as a synthetic, high-yield stablecoin. Ethena founder Guy Young read the article and subsequently assembled an all-star team to take on this monumental task and make it a reality. When we heard what Guy was building, Maelstrom joined as a founding advisor. Ethena's USDe stablecoin became the fastest-growing stablecoin in history, accumulating approximately $13.5 billion in deposits in less than 18 months. USDe is now the third-largest stablecoin by circulating supply, behind Circle’s USDC and Tether’s USDT. Ethena’s growth has been so strong that by next St. Patrick’s Day, Circle CEO Jeremy Allaire will be drowning his sorrows in a pint of Guinness, as Ethena will become the second-largest stablecoin issuer after Tether.

Due to exchange counterparty risk, speculators typically pay higher interest rates than Treasury bond rates when borrowing US dollars to go long on crypto. When I created perpetual swaps with the BitMEX team in 2016, I set a 10% neutral rate. This means that if the perpetual swap price equals the spot price, longs will pay shorts a 10% annualized percentage yield (APY). Given that every perpetual swap exchange has copied BitMEX's design verbatim, they all have a 10% neutral rate. This is important because 10% is well above the current cap on the federal funds rate of 4.50%. Therefore, the yield on staked USDe should almost always be higher than the federal funds rate. This provides new stablecoin savers who are willing to take on a little extra risk with the opportunity to earn, on average, twice the yield offered by BitMEX.

Some (but certainly not all) of these new stablecoin deposits will be held in Ethena to earn higher returns. Ethena will receive a 20% commission on any interest earned. Here’s a simple model:

USDe Market Share: Currently, Circle's USDC holds a 25% market share of all stablecoins in circulation. I believe Ethena will surpass Circle, and over time, we see USDC losing deposits at the margin as USDe gains deposits. Therefore, my long-term assumption is that USDe will achieve a 25% market share, closely following Tether's USDT.

Average USDe Yield: Given a USDe supply of $2.5 trillion in my long-term scenario, this will put downward pressure on the basis spread between derivatives and spot. As Hyperliquid becomes the largest derivatives exchange, they will lower the neutral interest rate, increasing demand for leverage. This also means a significant increase in open interest (OI) in the crypto derivatives market. If millions of other DeFi users have trillions of dollars in stablecoin deposits at their disposal, they could reasonably drive open interest into the trillions.

I believe ENA can rise 51x from its current levels.

Since ordinary people can earn more interest income, how can they escape the poverty caused by inflation through trading?

Trading stablecoins

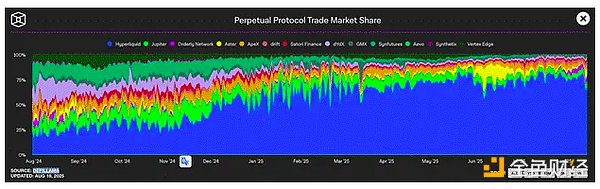

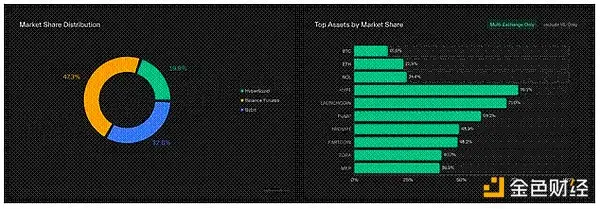

The most pernicious impact of global currency debasement is that it forces everyone, if they don't already own a plethora of financial assets, to become speculators in order to maintain their standard of living. As more of the world's population suffering from rampant fiat currency debasement now saves on-chain via stablecoins, they will trade the only asset class that allows them to speculate their way out of inevitable poverty—cryptocurrency. Currently, the preferred on-chain trading venue is Hyperliquid (token: HYPE), which holds 67% of the DEX market share. Hyperliquid is so transformative that it is rapidly countering the growth of decentralized exchanges like Binance. By the end of this cycle, Hyperliquid will be the largest cryptocurrency exchange of any type, and Jeff Yan (Hyperliquid founder) may be richer than Binance founder and former CEO CZ. The old king is dead. Long live the new king!

The theory that DEXs will eat all other types of exchanges isn’t new. What’s new in Hyperliquid’s case is the team’s ability to execute. Jeff Yan built a team of around ten people and delivered a better product faster than any other team in the space, centralized or decentralized.

The best way to understand Hyperliquid is to think of it as a decentralized version of Binance. Because Tether and other stablecoins primarily power Binance's banking channels, we can consider Binance a precursor to Hyperliquid. Hyperliquid also relies entirely on stablecoin infrastructure for deposits, but it offers an on-chain trading experience. With the introduction of HIP-3, Hyperliquid is rapidly transforming into a permissionless derivatives and spot trading powerhouse. Any application that desires a liquid central limit order book with real-time margining can integrate any derivatives market they desire through the HIP-3 infrastructure.

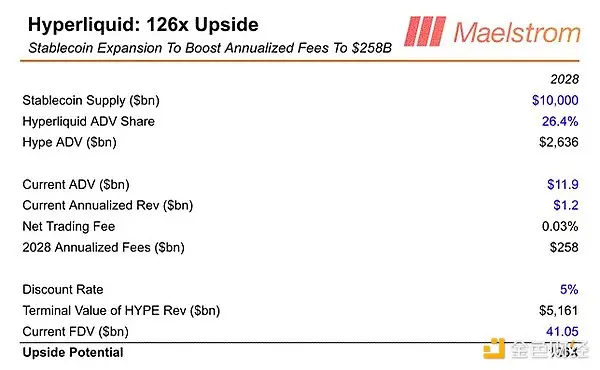

My prediction is that by the end of this cycle, Hyperliquid will be the largest cryptocurrency exchange of any type, and the growth of stablecoins to $10 trillion in circulation will supercharge this growth. Using Binance as an example, we can project Hyperliquid's average daily trading volume (ADV) for a given stablecoin supply level.

Currently, Binance’s perpetual swaps have an average daily trading volume of $73 billion, and the total stablecoin supply is $277 billion; this represents a 26.4% ratio. You’ll see this represented in the model as the Hyperliquid ADV Share.

I believe HYPE can rise 126x from its current levels.

Finally, I want to talk about the shitcoin stablecoin project I’m most excited about because of its upcoming token launch.

Collateralized stablecoins

Now that millions, perhaps even billions, of people use stablecoins, how will non-crypto businesses capitalize on this new form of payment? Most businesses around the world have a payments problem. They're overcharged by payment processors, and often banks simply won't deal with them. But with stablecoins in the hands of more users, businesses can free themselves from the clutches of greedy traditional financial institutions. While this is a noble aspiration, businesses need an easy-to-implement technology stack that allows them to accept stablecoin payments, pay suppliers and taxes in local currency, and properly account for cash flow.

Codex is a dedicated blockchain project for stablecoins. While not currently an issuer, it provides businesses with the ability to process stablecoin-to-stablecoin, stablecoin-to-fiat, and fiat-to-stablecoin payments. Remember Fernando and his click farm? He needed to pay some of his employees pesos into their local bank accounts. Using Codex, Fernando can receive stablecoins from his clients and convert some of them into pesos, depositing them directly into their local bank accounts. Codex has already launched this feature and achieved $100 million in transaction volume in its first month.

The reason I'm so excited about Codex has to do with disintermediating traditional global transaction banking. Yes, that's a huge total addressable market (TAM), but even more transformative and currently untapped is extending credit to small and medium-sized enterprises (SMEs) that otherwise lack access to working capital financing. Today, Codex only provides credit for less than a day to the most secure payment service providers (PSPs) and fintechs, but tomorrow, Codex could offer longer-term loans to SMEs. If an SME operates entirely on-chain and uses Codex for stablecoin payments, it can achieve triple-entry bookkeeping.

Triple-entry bookkeeping improves upon double-entry accounting in that, because all income and expense transactions are on-chain, Codex can calculate net income and cash flow statements for SMEs in real time, using unforgeable data. Based on this unforgeable data, Codex can confidently provide loans to SMEs, confident that the business's fundamentals will enable them to repay the principal and interest on time. Currently, in most developing countries, and to some extent in developed countries, SMEs find it difficult or impossible to obtain bank loans. Banks are understandably risk-averse, fearing that the retrospective accounting data they receive may be fraudulent. Consequently, banks limit lending to large corporations or politically connected elites.

I envision Codex becoming the largest and most influential financial institution first in the Global South, and then in developed countries outside the U.S., by using stablecoin infrastructure to lend to small and medium-sized enterprises. Codex will truly become the first true crypto bank.

Codex is still in its early stages, but if the founders succeed, they will make their users and token holders incredibly wealthy. Before Maelstrom took on this advisory role, I made sure the founders were ready to pursue a tokenomics strategy similar to Hyperliquid's. From day one, revenue earned will flow back to token holders. They may raise a funding round. But I wanted to make sure the world knew there was an actual stablecoin infrastructure project in place, processing real transaction volume today, and about to hold a token generation event (TGE). It was time to board a faster-than-light (FTL) ship.

Besant's Control

The extent to which Bessant will terrorize Eurodollar and non-dollar bank depositors around the world depends on the US government's spending trajectory. I'm confident that Bessant's boss, US President Trump, has no intention of balancing the budget, cutting taxes, or slashing spending. I know this because Trump has admonished his fellow Red Team Republicans for being too obsessed with spending cuts. He's more or less jokingly said they still have to win the 2026 election. Trump has no ideology other than winning. And in a late-stage capitalist democratic republic, political winners hand out favors in exchange for votes. Therefore, Bessant will run rampant, with no Officer Starling around to stop him.

As government deficits continue to expand and US hegemony declines, the substantial growth needed to raise tax revenues will become unfeasible. Therefore, Bessant will continue to cram more and more debt down the market's throat. However, when the clear policy of those in charge is to weaken a currency, the market doesn't want to hold debt denominated in that currency. Therefore, using stablecoins as a debt absorber, it's time to embrace the dollar or face sanctions again.

Bessant will wield his sanctions stick broadly and fiercely to ensure that dollar-pegged stablecoins bring home capital sequestered in Eurodollars and non-US retail bank deposits. He will commission tech bros like Zuckerberg and Musk to spread the gospel to distant, uncivilized tribes. And these broligarchs will happily drape themselves in the flag and push dollar-pegged stablecoins on their non-US users, whether local regulators like it or not, because they are patriots!

If I’m right, we’ll see headlines covering these topics:

1. The need to regulate the offshore US dollar market (i.e., Eurodollars)

2. Tie the use of central bank dollar swap lines with the Federal Reserve and/or the Treasury to certain aspects of opening digital markets to U.S. tech companies.

3. Propose regulations requiring stablecoin issuers to deposit US dollars in US bank branches and/or hold Treasury bonds.

4. Encourage stablecoin issuers to list on the U.S. stock market

5. Major US tech companies add crypto wallets to their social media apps

6. Members of the Trump administration have made generally positive statements about the use of stablecoins

Maelstrom continues to be very bullish on the stablecoin vertical, with positions in ENA, ETHFI, and HYPE. We are always looking to the future; therefore, you will hear more about Codex, as I believe it will become a major player in stablecoin infrastructure.

Pass me the dollar lotion (referring to the inflow of stablecoins), I'm a little dry (referring to the need for capital inflow).