Author: Scof, ChainCatcher

Recently, Strategy (formerly known as MicroStrategy) officially submitted documents to the U.S. Securities and Exchange Commission, planning to issue up to $21 billion of 8% Series A perpetual preferred shares. This move has attracted market attention because it not only involves large-scale fund raising, but may also have a far-reaching impact on Strategy's Bitcoin purchase strategy.

According to official documents, these preferred shares have a par value of $100 per share, an annualized interest rate of 8%, and quarterly dividends, which can be paid in cash, common stock, or a combination of the two. In addition, preferred shares can be converted into common stock at a ratio of 10:1, that is, every 10 preferred shares can be converted into 1 common share.

The preferred stock issuance will adopt the "market issuance plan" model, that is, the company can sell preferred stock directly in the market, similar to the ATM issuance of common stock. This means that Strategy now has ATM financing channels for both common stock and preferred stock.

So what is the difference between this issuance of preferred shares and previous ones? Will this innovative financing method bring new variables to the Bitcoin market? This article will provide an in-depth analysis of this.

Strategy The evolution of financing methods

Before analyzing Strategy’s latest financing method, let’s briefly review its past methods of purchasing Bitcoin.

In the early stages, Strategy, as a software company, used idle cash on its books to purchase Bitcoin. The first three investments in this stage bought 40,700 Bitcoins.

As companies invest more in Bitcoin, they begin to use convertible preferred bonds (convertible bonds) for financing. Convertible bonds allow investors to convert bonds into company stocks under certain conditions, providing both downside protection (the principal and interest can be recovered when the bonds mature) and potential gains from stock price increases. 119,481 Bitcoins were purchased in this way.

In addition to convertible bonds, Strategy has also issued senior secured bonds, which are secured debt instruments with lower risk than convertible bonds but a more fixed income model. Using this model to raise funds, the company bought 13,005 bitcoins.

As MSTR's stock price rises, the company has increasingly adopted at-the-market (ATM) financing since 2021. ATM is a widely used financing method in the United States, which allows listed companies to issue new shares directly on the open market at current market prices to raise funds.

On February 20 of this year, Strategy issued $2 billion in convertible senior notes. The review process required for this financing method is more complicated and time-consuming than before, so the market speculated at the time that Strategy's purchase of BTC would slow down.

However, the $21 billion perpetual preferred shares submitted for review this time have once again raised the market's expectations that Strategy will return to the "buy, buy, buy" mode.

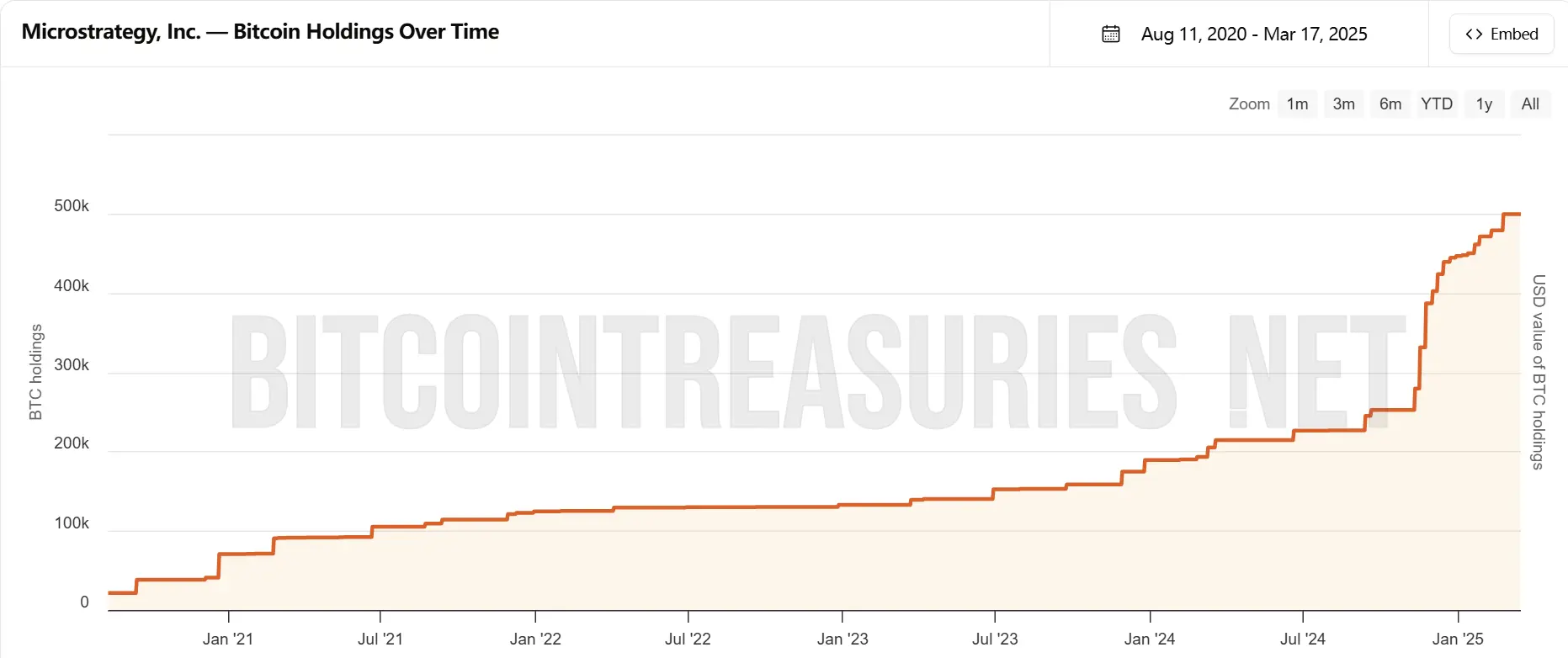

The number of BTC held by Strategy. Source: bitcointreasuries.net

How are preferred stocks different?

Compared with previous financing methods, the perpetual preferred stock that Strategy applied for this time is significantly different in structure. In the past, the company mainly relied on debt financing and stock issuance to obtain funds, while this issuance of preferred stocks has found a new balance between traditional equity financing and debt financing.

The biggest difference between preferred stock and common stock is that it is neither completely dependent on the company's performance nor has a fixed maturity date and repayment requirement. It is more like a financial instrument "in between the two", where the holder can receive fixed dividend income regularly and convert it into common stock under certain conditions.

For Strategy, this means that it can continue to raise funds by issuing additional preferred shares without having to bear the pressure of repayment due for traditional debt financing. Compared with the convertible bonds and senior secured bonds issued previously, this financing method provides greater flexibility and reduces short-term financial burden.

Of course, this model is not without cost. The annualized interest rate of the preferred stock is set at 8%, which is obviously higher than the 0%-0.75% convertible bonds and 6.125% priority secured bonds issued by Strategy in the past. The core question in the market is how the company can pay this considerable dividend cost.

Analysts speculate that Strategy may issue additional common stock through ATM to make up for the funding gap, or even directly use the additional shares to pay dividends. Although this model allows the company to raise funds in a short period of time, it may also lead to the problem of dilution of common shareholders' equity.

Is it a good time to place a bet?

If Strategy's perpetual preferred shares are approved, it will undoubtedly bring new impetus to the Bitcoin market.

Simply put, this type of preferred stock is equivalent to the company finding a more flexible and lasting way to raise funds, and the money will eventually be used to buy Bitcoin.

Compared with the past practice of issuing bonds or directly selling stocks to raise money, perpetual preferred stocks have no fixed maturity date, and companies can always use them to raise funds without having to repay the principal regularly like repaying debts. At the same time, since the preferred stocks this time adopt a model similar to the issuance of common stocks, Strategy can sell preferred stocks to raise funds at any time according to market conditions, without having to wait for approval or find specific investors like bond financing.

This means that Strategy may buy Bitcoin faster in the future, or even continue to buy more steadily.

But in the current sluggish market conditions, is it appropriate to initiate such a more aggressive financing method?

James Carter, a senior analyst at Goldman Sachs, said, "Strategy's $21 billion preferred stock issuance plan shows Saylor's extreme optimism about Bitcoin, but in the current market downturn, such high leverage operations may increase volatility risks."

Michael Evans, a fintech researcher at Citigroup, believes that "against the backdrop of overall pressure on the cryptocurrency market, Strategy's choice shows its judgment of future trends. If the market picks up, its returns may be astonishing, but at present, attention should be paid to capital flows and changes in market sentiment."

Due to the complex structure of perpetual preferred stock financing, SEC approval may take several months. ChainCatcher editorial department will continue to follow up on the progress.