Author: arndxt

Compiled by: Tim, PANews

I know this is not what you want to say, but I will say it anyway.

Solana is becoming the Bloomberg Terminal of the crypto world, built for high-speed trading, on-chain composability, and massive yield throughput.

Three data support my view:

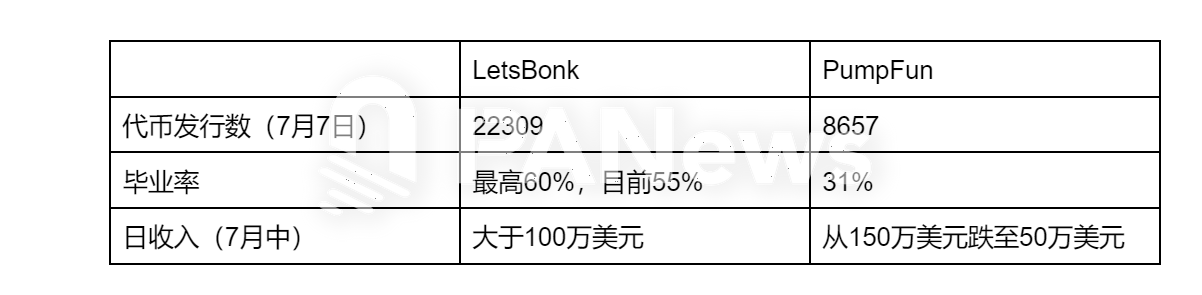

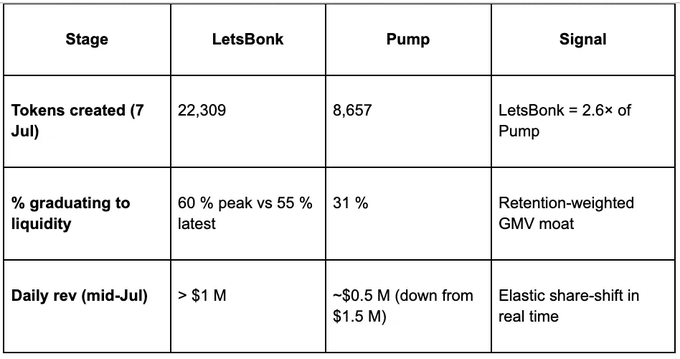

- The launch platform is now SaaS-based: LetsBonk surpasses Pumpfun, with a 60% graduation rate and entry into the liquidity pool, and daily revenue exceeds one million US dollars. Creator loyalty is lost, and retention-weighted GMV becomes a new moat.

- Tokenized shares are core collateral: they enable 24/7 liquidity, modular margin, and capital unlocking for private markets. The real market potential lies in the circulation of re-IPO equity.

- Solana has a diverse revenue structure: Q2 revenue was $570 million, accounting for 46% of all public chains. Its revenue mainly comes from decentralized applications, robot services, Launchpads, and production tools.

1. PMF from the launch platform competition to the actual combat test

LetsBonk’s highlight moments are more than just digital competitions:

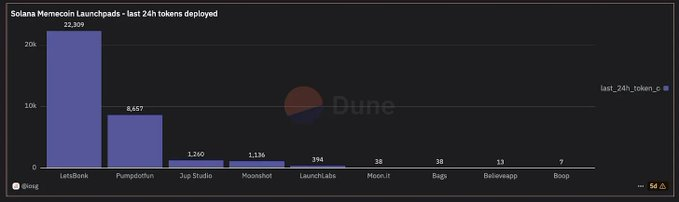

The market share has reversed: on July 5, its new token launches accounted for 66% of the total market, while the Pumpfun platform accounted for only 26%.

The quality of funds is more important than the size of the fund: the LetsBonk platform has a graduation rate of about 60%, while Pumpfun's graduation rate is only 31%.

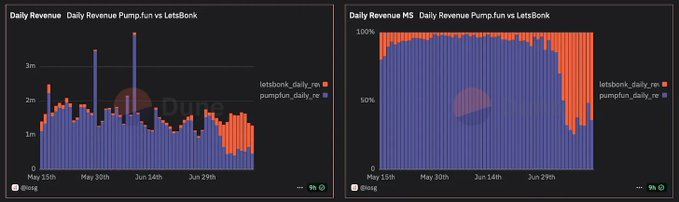

Monetization: Daily revenue increased from about $0 to over $1 million, while Pump’s fell to $500,000.

My thoughts

Retaining weighted GMV is the real moat. The graduation rate is essentially a net income retention indicator for the launch platform; whoever can institutionalize it first will win the enterprise-level API integration market (Telegram robots, "one-click coin issuance" SDK, etc.).

Pumpfun still occupies the majority of creators' mind share (cumulative revenue of about $700 million), but the LetsBonk platform has proven that the user conversion cost is close to zero. Pumpfun's next wave of user churn may not be natural, but artificially planned, imagining that top influencers provide "24-hour exchange listing" guarantee services.

Valuation of project scale: Even with a stable revenue flow of $1 million per day, annualized revenue can reach $100 million. With a profit margin of about 80% for Solana infrastructure, this protocol, which has only been online for a year, has already presented a SaaS-level economic model. Even if the drastic fluctuations are excluded, the valuation of $1-2 billion is still valid based on 10-15 times the forward sales.

Switching costs approach zero, so user minds are rented rather than truly owned.

Pumpfun platform reached cumulative revenue of US$700 million in just 18 months, but LetsBonk, which came from behind, took advantage of trading competitions and seized a large market share in less than three weeks.

A paradigm shift in incentives means:

- The loyalty of creators is like that of mercenaries. Airdrop activities and "24-hour listing on exchanges" internet celebrity promotion packages are enough to make a whole group of creators "jump ship" overnight.

- Defensive moat equals liquidity networking, not UI experience. Pumpfun is expected to achieve straight-line pull-ups through native decentralized exchanges and liquidity provider bribery mechanisms, thereby increasing exit costs.

Competitive strategy for newcomers: Overinvest in incentive strategies, promote visual effects of leaderboards centered on tokens and days, and realize monetization before the customer acquisition cost model is reset.

Funnel economics suggests that acquiring volume is easy, but graduation is king.

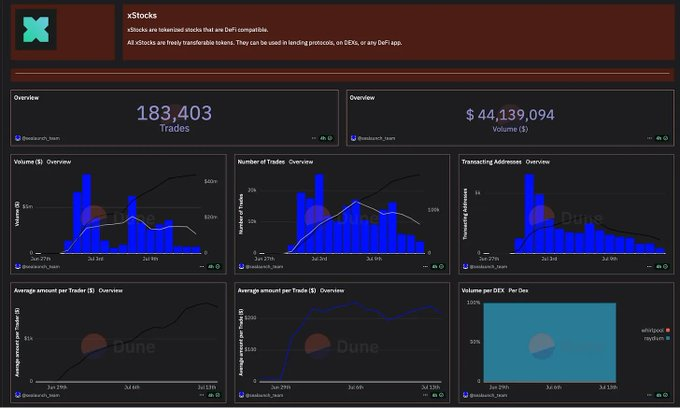

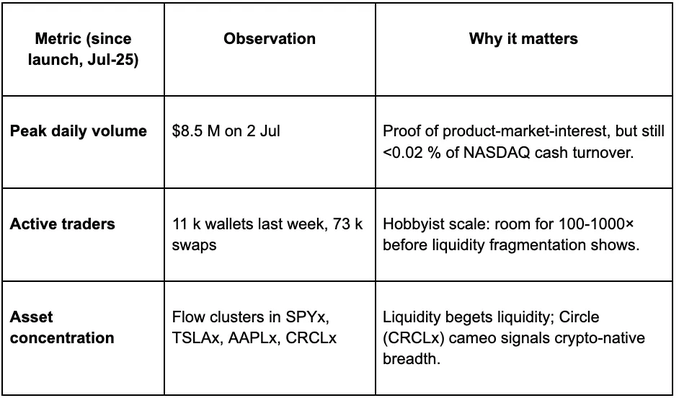

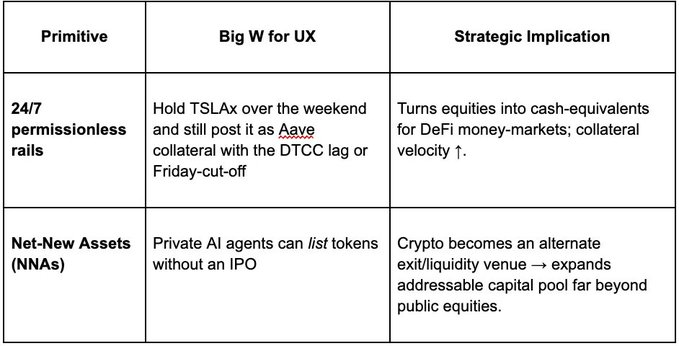

2. Tokenized stocks are a Trojan horse for introducing traditional financial liquidity

Tokenized stocks are more than just "Apple stocks on the blockchain," they:

- Compressing traditional financial settlement delays to minutes

- Opening up a new class of collateral assets

- Opening up financing channels for large private institutions

The winning blockchain ecosystem must meet three core elements: a regulated token issuance mechanism, a sound oracle system, and a highly liquid perpetual contract market. The winner will become the "Stripe Connect"-level infrastructure in the tokenized equity space, fully capturing the value upside dividend.

Where are we on the “S growth curve”?

xStocks and Robinhood whitelist synthetic put options on Apple ($AAPL) on-chain, while transforming illiquid assets or private equity into composable collateral.

Two basic structures that make tokenized stocks real value rather than gimmicks

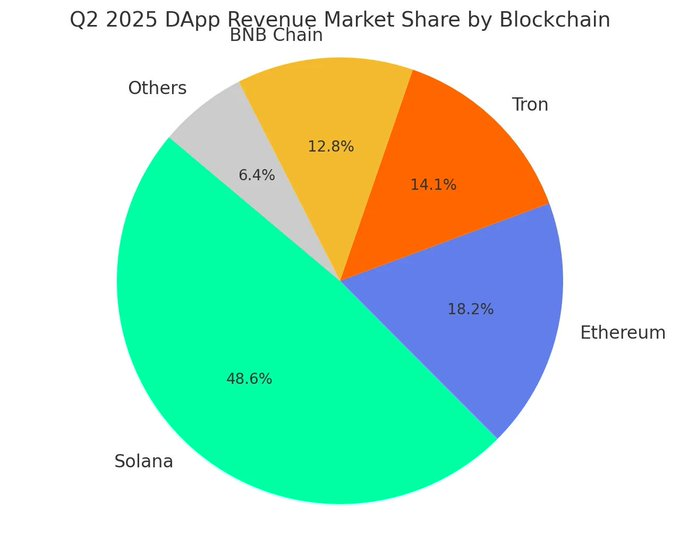

3. Solana as the “revenue mechanism” of the production and marketing chain

Solana's second-quarter revenue reached $570 million, accounting for 46% of the market share.

- Ethereum: $213 million

- TRON: $165 million

- Binance Chain: $150 million

- Other: Up to $75 million

Two facts can be seen:

- The main application scenario of cryptocurrency is still transaction as a service.

- Built for professional users: Professional users drive profits and losses; mainstream exchanges will subsequently lead the public to enter the market

Why do "professional users" beat "general public" in the field of encryption?

Solana optimizes the full life cycle value of professional users, while centralized exchanges need to bear the costs of KYC certification, fiat currency channels and new user support.

- Latency Arbitrage Loop: 400 millisecond trading sessions and near-zero fees allow bots to refresh orders dozens of times per second; every tiny advantage translates directly into protocol fees.

- Combinable leverage: launch tokens → instant AMM liquidity pool → perpetual contract mortgage, the whole process takes only a few minutes. The capital turnover speed is a full order of magnitude higher than Ethereum L2.

- The network incentive mechanism is highly consistent with the needs of whales: professional users are willing to pay more and have a lower churn rate, which can also lay a liquidity foundation for the platform, thereby continuously attracting a new generation of professional users to join.

Conclusion

Solana is committed to maximizing the life cycle value of professional users, while centralized exchanges bear the costs of KYC, fiat currency channel maintenance and novice support.

The fastest-growing companies in crypto see blockchain as a high-speed rail for capital markets.