Author: Ching Tseng, AppWorks Investor

Compiled by: Deep Tide TechFlow

Deep Dive: Investor Ching Tseng categorizes crypto companies into four quadrants: crypto-native/traditional finance-oriented, traction-driven/non-traction-driven. Of the 118 token launches in 2025, 84.7% failed to break even. Crypto-native but non-traction-driven projects are massively destroying capital, while traditional finance-oriented and traction-driven companies are capturing the $18 billion RWA market. This article clarifies where the money is flowing and what kind of token economics has failed.

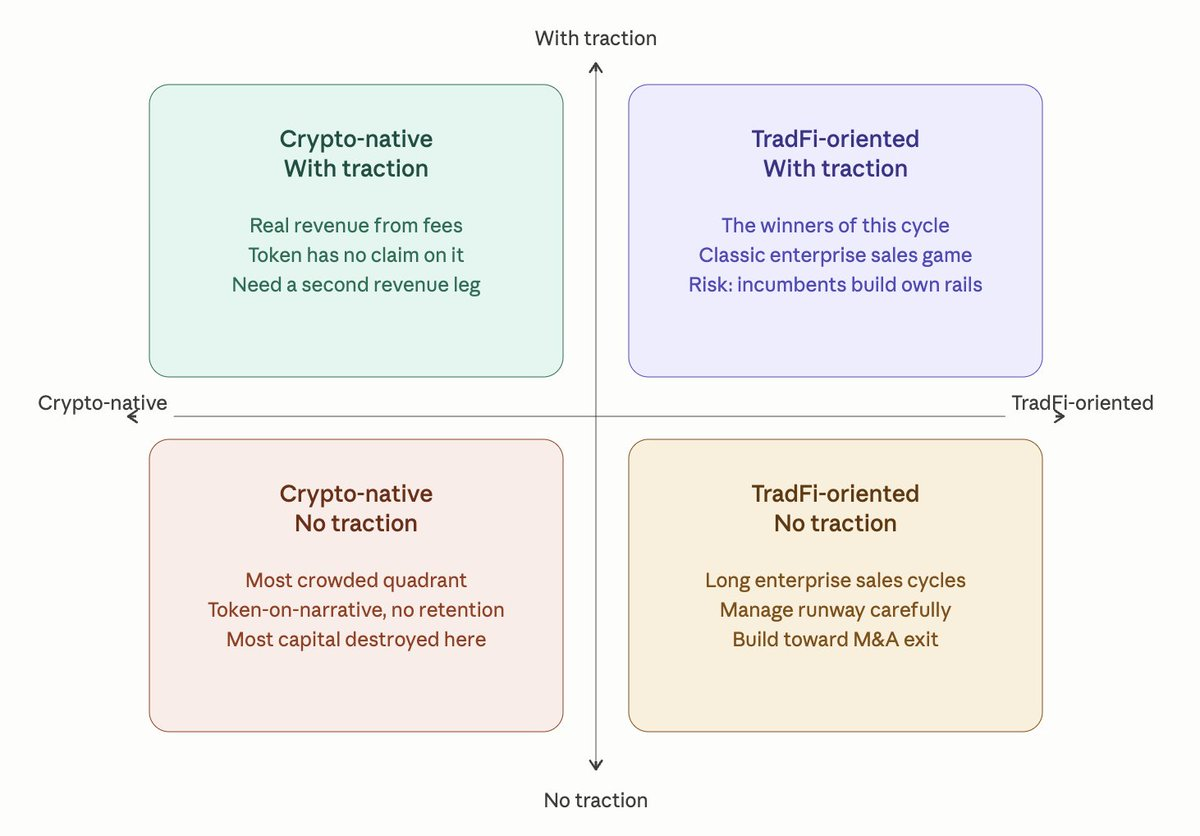

Sitting on the investor's side this year, I found that almost every crypto founder I met could be categorized into one of four types. The two axes are simple: crypto-native vs. traditional finance-oriented, with traction vs. without traction. These four quadrants cover approximately 75% of the market.

Each quadrant presents entirely different challenges. Here is my breakdown.

Encryption native, no traction

This is the most crowded quadrant, and also the place where capital has caused the most damage.

These teams are still showcasing TVL figures that were inflated in the previous cycle, without explaining why they were effective back then. They're asking for valuations of $20 million, $30 million, and sometimes even $200 million, with just a utility token and a roadmap, claiming the token has "clear use cases" because of paying transaction fees or voting in governance.

The data is brutal. Of the 118 token offerings tracked in 2025, 84.7% fell below their offering price, with the median drop of 71% on a fully diluted valuation basis. Following the launch of some of the most anticipated "native DeFi L1" tokens in this cycle, TVL (total value) plummeted by over 90% in the first year, mirroring the overall token price movement. AI-related tokens saw an average annual return of -50%, with several top performers from 2024 experiencing drawdowns exceeding 80% from their peaks.

The pattern is consistent. Initial traction comes from users looking for quick profits rather than genuinely liking your product. Tokens based on narrative pricing, without revenue or user retention to support their valuations, will bleed in 2025. Massive emissions reveal that on-chain activity is primarily mercenary behavior.

What needs to be internalized in this quadrant is that the long-term value of a token comes from the team's ability to generate revenue and return capital to holders, rather than from the artificial utility of forcing users to spend it. Regulators still prevent anyone from publicly saying "tokens are equity," but empirically, that's the only valid model. Everything else is, at best, a cyclical transaction.

If you're here, the honest approach isn't to issue another coin. Instead, go back to the fundamentals: Who are your real users, what are they willing to pay for, and how do you capture a portion of them?

Encryption is native and has traction.

This quadrant is full of teams that built something substantial years ago, typically in the previous cycle, and have been quietly earning good income from trading, lending, or exchange fees. The teams are small, their cash flow covers salaries, and their products are effective.

Sounds good, right? But they also have challenges to overcome.

Most tokens launched early on are now facing structural problems: revenue exists, but the tokens have no mechanistic claim to it. Some of the largest products on the market have monthly trading volumes in the tens or even hundreds of millions of dollars, but the direct value captured by the tokens has been zero over the years. No matter how good the revenue/profits are, the market doesn't really trade tokens at a consistent multiple; the market prices based on expected growth, not current economic conditions.

The buyback debate is the other half of this quadrant story. Some protocols that pledged to fund weekly buybacks with transaction fees in early 2025 saw their prices surge by over 40% in the following month. Other protocols running automated, fee-funded buyback programs cumulatively bought back over $1 billion worth of tokens in seven months, with a single-day buyback reaching nearly $4 million. Total DeFi buybacks in 2024-2025 are estimated at approximately $2 billion.

Buybacks sound like the answer. Sometimes they are. But for teams without spillover revenue in this quadrant, buying back tokens is just burning through future runways to defend a price that might not hold. The harder, and better, question is whether you can grow a second revenue stream not tied to crypto volatility. Because if traditional finance-oriented competitors build better institutional distribution while you're still surviving on altcoin traders, your moat will quickly become infrastructure commodity pricing.

Traditional financial orientation, lacking traction

This group is expected to expand in 2024-2025. Custody tools, compliance middleware, tokenized tracks, on-chain FX, and institutional settlement are all genuinely useful. They are all expensive. They all have enterprise sales cycles measured in quarters, not weeks.

The problem isn't with the product. It's with the math. The founders raised $15 million to $30 million with the assumption that institutions would come to them, but even getting a Tier 1 bank client could take 12-18 months and require compliance infrastructure, meaning they'd burn through cash for a year before generating their first dollar of revenue.

The good news is that the exit environment in this quadrant is exceptionally healthy. Crypto M&A is projected to reach a record $8.6 billion in 2025, with over 140 VC-backed crypto companies being acquired, a 59% jump year-over-year. Some of the biggest deals involved existing giants paying hundreds of millions to billions of dollars for distribution, licenses, and corporate relationships across derivatives, trading infrastructure, and payment tracks.

If you're in this quadrant, the calm approach is to manage your valuation and cash runway like your lifeline to achieve meaningful M&A results, because they truly are. Don't price yourself out of the acquirer pool. Don't burn through 24 months chasing a company logo. Build complementary partnerships with larger players who might eventually want to acquire you.

Traditional financial orientation, with traction

The winners of the current system.

Tokenized real-world assets grew from $5.5 billion at the beginning of 2025 to $18.6 billion by the end of the year, a 3.4-fold increase in twelve months. The largest tokenization platforms now handle billions of dollars in institutional liquidity, with the market leader holding approximately 20% of the market share, underpinning one of the world's largest tokenized government bond funds with nearly $3 billion in assets under management (AUM).

These companies aren't trying to convince anyone that crypto is the future. Their institutional clients have already made their decision. The game now is straightforward enterprise sales: win over more banks, more asset managers, more issuers; build alliance structures so that when institutions buy one of your products, they naturally buy the other three from your partners; and squeeze unit economics on top of your already built compliance and custody stack.

If the team is a pure service provider, this becomes the classic enterprise software war: sales velocity, net retention, and integration depth.

The main risk in this quadrant doesn't come from competition native to crypto. Rather, it comes from existing giants, large asset managers, and global banks eventually building their own tracks, bypassing startups that help them adapt to on-chain environments. The window of opportunity exists, but it's not unlimited.

The four quadrants may seem different on the surface, but they all guide us toward the same underlying shift: the market is maturing.

This doesn't mean narratives are dead. Institutions still chase trending topics, as anyone who's looked at semiconductor and AI valuations over the past two years knows. But in mature markets, a simple narrative has a shorter half-life. It can still get you started, but it won't sustain you.