Author: @bonnazhu, Bonna | U Butter

This rapid decline in the STRC index is, in my opinion, perhaps the best educational case study in finance.

It was still a lengthy warning, and it carried a strong personal tone.

TL;DR

- If MSTR were to die, it would still die from reflexivity, but not this time.

- The STRC returning to its par value anchor is only a matter of time; this is the nature of floating-rate bonds.

- Selling cryptocurrency for money is like drinking poison to quench thirst; it solves the short-term problem but has endless consequences.

A detailed explanation is as follows:

First, how should we understand this wave of BTC decline?

I personally believe that this rapid drop in BTC was a targeted attack by funds targeting MSTR. The cause was that MSTR used its already insufficient cash reserves (which the market generally believes were a safety cushion for preferred stock dividends) to repurchase some convertible bonds, causing the cash reserve coverage ratio for preferred stock dividends to plummet from more than two years to about six months. Then, it sold 32 BTC.

The market instantly sensed a "cash flow crisis" and quickly launched an attack. The already suppressed concerns about large IPOs draining liquidity, the World Cup diverting funds, and rising inflation and cooling interest rate expectations further facilitated the attackers in solidifying these expectations on the market. This allowed them to quickly force funds with information asymmetry to surrender or hesitate to make any rash moves to buy at the bottom.

This is actually a typical example of reflexivity in traditional financial markets:

Market prices do not passively reflect reality; rather, they can change reality.

in other words:

The expectation is contagious, and this contagiousness can alter reality.

The same scenario played out when Soros attacked the pound. The Bank of England's foreign exchange reserves might have been sufficient initially, but market participants suffered from information asymmetry. Once everyone believed it wasn't enough and collectively shorted the market, the reserves actually became insufficient. The same applies to bank runs. When everyone simultaneously believes the bank is about to collapse and rushes to withdraw their money, the expectation of failure can become a reality!

Applying this to MSTR, the attacker's playbook would be:

Declining cash reserves → Market anticipates liquidity crisis, forcing forced selling of cryptocurrencies → Panic selling depresses BTC → BTC price drop further compresses mNAV and worsens balance sheets → The expectation of "it can't hold on any longer" is increasingly being realized by the price, reducing available options → More people join short selling → Expectations become increasingly likely to materialize.

The fact that BTC itself cannot generate sustainable cash flow to cover dividend payments for MSTR, and that the flywheel's continued operation must rely on financing, is also why it is easier for attackers to seize opportunities.

Second, the logic behind STRC's decline and return to par value anchor.

The relationship between STRC and MSTR common stock is that of preferred and subordinated:

Common stock, as the subordinated tranche, absorbs most of the risk from Bitcoin price fluctuations.

STRC, as a priority, can maintain relative stability in most cases.

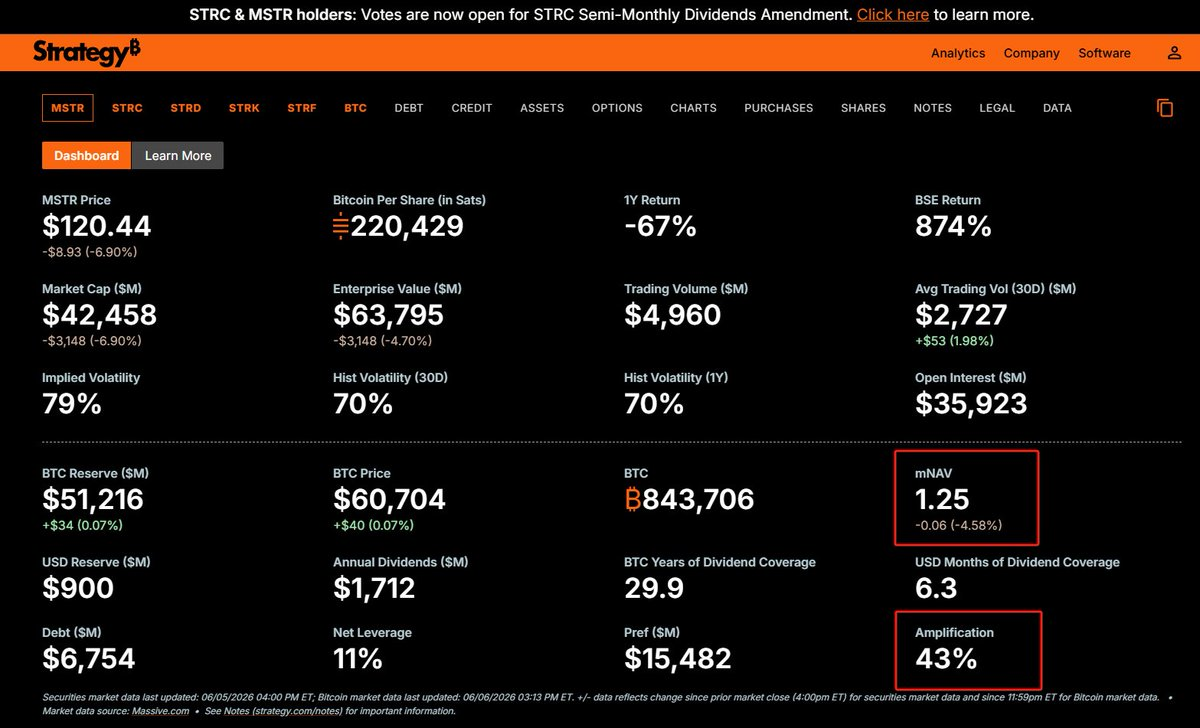

According to MSTR's target overall debt ratio of approximately 33-35% (currently, due to the drop in BTC price to 61k, the overall debt ratio has increased to 43%), theoretically, only when the BTC price falls below 26k, and common stock becomes worthless, will preferred stock be truly affected.

Why did STRC also fall?

This involves some fundamentals of bond pricing.

STRC is nominally preferred stock, but it is essentially debt in nature, with floating interest rates and no maturity date.

The price of a bond is essentially the sum of the present values of all future cash flows (interest per period, calculated based on the coupon rate + principal at maturity, equaling face value 100) discounted at a given discount rate. This discount rate is the required rate of return demanded by the market at that moment.

If the coupon rate is exactly equal to the required rate of return, then the discounted price will be exactly equal to the face value of 100. This often happens when bonds are issued, meaning that investment banks usually refer to the market conditions at the time and investors' required rate of return to set the coupon rate.

However, bonds have a long lifespan. Throughout their life, external interest rate conditions and issuer credit may change, all of which will affect the discount rate (denominator) corresponding to the required rate of return. If the required rate of return in the market rises while the coupon rate (numerator) remains unchanged, the present value will be lower than the face value, and the bond will trade at a discount; conversely, if the required rate of return falls, the bond will trade at a premium.

Therefore, the price of a bond is never a static number; on the contrary, it reflects how much return the market demands at that moment in order to be willing to hold it.

A price falling below par value implies that "the market demands a higher interest rate than the coupon rate." If you actually buy at this discount and hold to maturity, your final yield will indeed be higher than the coupon rate. This means that the less principal you paid when buying a bond with a face value of $100 makes up for the insufficient return provided by the coupon rate. In other words, the market is using the discount to claim compensation for the risk it believes it deserves, which the coupon rate failed to provide.

The STRC is similar. Market concerns about MSTR's cash flow have led to a repricing of STRC's solvency. As the narrative of a "cash flow crisis" intensifies, the required rate of return for holding STRC jumps, making the 11.5% coupon insufficient to cover the risk.

Of course, from the perspective of external attackers, this is also a complete charade: only by causing STRC to fall along with it can the "cash flow crisis" be made real under conditions of information asymmetry, making you unable to help but suspect:

Is there really some information I don't know?

For fixed-rate bonds, the story essentially ends here: the increase in the required rate of return can only be matched by a price decline, thus the discount can persist in the long term and never revert to the par value anchor. However, STRCs are not fixed-rate bonds; they have floating rates, allowing for adjustments to the numerator.

For example, if the market requires a necessary rate of return of 12% to be willing to hold STRC, MSTR management would therefore raise the coupon dividend from 11.5%. In this case, the price cannot remain below par value of 100 for an extended period. This is because, under such circumstances, STRC purchased at a discount would actually yield a return higher than 12%, and buying would naturally surge in, pushing the price back to the level where the implied return equals 12%, i.e., par value.

This is why medium- and long-term floating-rate bonds are always anchored to a face value of 100; it is an inherent characteristic of floating-rate bonds.

For MSTR, the STRC price reverting to par value at $100 is a prerequisite for its continued ability to raise funds. If it issues shares at a discount, the company nominally issues them at a face value of $100, but the buyer only pays $90. This is equivalent to the company using the dividend obligation stipulated by the $100 face value to pay interest on only $90 of the actual funds received, artificially inflating its true financing costs. Every time it raises funds, it loses money—is that even possible?

Third, when mNAV > 1, you can sell stocks, but never sell cryptocurrencies.

So what is the key to breaking this deadlock?

As mentioned earlier, this entire downturn is a reflexive scenario of a self-fulfilling prophecy, built on the expectation of information asymmetry and a cash flow crisis. To break this deadlock, all that's needed is to prove that the liquidity crisis doesn't exist, replenish reserves, and the attack will lose its foothold, causing the reflexive spiral to collapse on its own.

So how do we replenish our reserves?

Like many people on X are saying, should Saylor just jump out and say, "We sold more coins during this crash, and now we have enough funds to last for several years"? That would certainly work, and the panic would end.

However, the cost of this is another layer of implicit uncertainty.

Because this is tantamount to telling the market: you need to reprice me.

The capital market premium flywheel narrative of "continuously increasing holdings, never selling coins, and constantly increasing the BTC content per share for shareholders" is definitely gone. Instead, it has become "may sell a large amount of coins to shrink the balance sheet when necessary, thereby diluting the BTC content per share," which is at least a discounted flywheel that takes three steps forward and one step back.

The result is that you don't know how common shareholders will react, or whether mNAV will disappear completely. Even if it doesn't disappear, narrowing is highly likely, since the premium for mNAV > 1 corresponds to an implicit call option in MSTR that "each share will contain more BTC in the future." If the rate of increase in BTC content slows down, the call option will naturally not be as valuable as before.

The importance of the mNAV premium to MSTR is self-evident. MSTR's expansion logic doesn't rely solely on common stock or leveraged debt financing like STRC (equity disguised as debt). Instead, it uses a "water to add flour, flour to add water" approach, maintaining its overall debt ratio within its ideal 33-35% range to prevent it from spiraling out of control. A narrowing mNAV premium directly impacts the size of the window for subsequent stock issuance and financing, a short-sighted approach.

In my opinion, a better approach would be to leverage the current situation where mNAV = 1.25x and the premium still exists significantly to raise funds by issuing new shares and selling them to replenish cash reserves. MSTR already has ample Shelf Offering quotas registered with the SEC. This is the only way to clearly please both the equity-debt holders and common shareholders of STRC at the same time, without the risk of repricing.

The specific mechanism is as follows:

When mNAV is significantly greater than 1, choosing to issue new shares and sell them first means that for every $1 of new shares you issue, if you use all of it to buy BTC, you can create more than $1 of shareholder value in the capital market. This is precisely why shareholders are willing to entrust their money to you. Because of this, in this situation, you don't actually need to use all the money raised to buy cryptocurrency: you can keep a portion as cash reserves for future principal and interest payments without negatively impacting shareholder value. At the same time, with more cash reserves, STRC holders feel safer, the alarm is eliminated, the risk premium decreases, and STRC will gradually return to its peg. Therefore, even if you want to raise STRC later, you can do so without any problems.

Conversely, choosing to sell cryptocurrency to raise funds is a short-sighted approach. Once the repricing causes mNAV to narrow or even disappear, the path of issuing new shares to buy cryptocurrency becomes impossible. This is because at this point, the fair value of your shares is equal to the BTC behind them. Why wouldn't I just buy cryptocurrency directly? Moreover, you have to retain a portion of the financing to pay interest, which is a naked negative shareholder value: it's like taking my money, using part of it to buy cryptocurrency (which creates value in the capital market to just break even), and using the other part directly to pay interest and losses.

This is a structure with net blood loss.

At that time, since issuing new shares will no longer be feasible, STRC's issuance will also be gradually affected. Not only will the overall expansion flywheel likely come to a standstill, but your financing window will also be closed, so you will have to rely on cash reserves. If the cash reserves are also used up, then you will really only have selling coins left, and that will be the end of the road.

Furthermore, selling shares has another advantage: it directly improves the debt ratio. Currently, due to the drop in BTC to 61k, MSTR's overall debt ratio has increased from the target of 33-35% to approximately 43%. The capital gained from issuing new shares and selling existing ones is equity capital: cash (asset side) increases, equity increases, and after deducting a small portion retained for interest payments, the overall debt ratio will further improve.

And what about selling cryptocurrency? Because the cash you get from selling cryptocurrency is immediately used as dividends, the asset side first sees a decrease in BTC, then a cash outflow, resulting in a net decrease in total assets, while liabilities remain the same, and the debt ratio actually worsens slightly.

Selling shares: Improves debt ratio ✓, preserves BTC content per share ✓, does not harm premium ✓

Selling cryptocurrency: worsens debt ratio, reduces the amount of BTC per share, and significantly hurts the premium.

The superiority or inferiority is obvious at a glance.

Finally, if, I mean if,

Is MSTR really selling a large amount of coins to replenish its reserves?

So, as many Twitter users, including Delphi and his group, have predicted, the short-term crisis will definitely be resolved, BTC will rebound, and STRC will revert to its previous level. This is precisely why I said that if MSTR is truly going to die, it won't die this time; selling stocks or cryptocurrencies will indeed solve the immediate crisis.

But personally, I've also lost my mystique towards MSTR and Saylor.

Furthermore, due to the repricing logic of common stock, the "BTC content per share" call option is no longer as valuable as before, causing the mNAV premium to gradually disappear. This leads to the strange phenomenon of BTC rebounding, STRC reverting to its anchor, while MSTR common stock falls.

The next time, when cash reserves run out again and the market anticipates selling coins again, the reflexive scenario will play out once more, and it's uncertain whether this will be the beginning of the end.

But to be honest, I would accept that kind of ending.

Perhaps "change" is itself part of this "situation".