Author: Arthur Hayes

Original title: Snow Forecast

Release date: November 17, 2025

It's time for me to play the amateur meteorologist again. Concepts like La Niña and El Niño are entering my vocabulary.

Predicting storm wind direction is just as important as snowfall, as it determines which slopes are suitable for skiing. I used my rudimentary knowledge of weather patterns to predict when autumn will end and winter will begin in Hokkaido, Japan.

I discussed with other local skiers the possibility of my dream powder season starting earlier. I no longer refresh my favorite crypto trading app as frequently; now, I check Snow-Forecast the most.

As data points started coming in, I had to decide when to go on the slopes with incomplete information. Sometimes I wouldn't know what the weather pattern would be until the day before I put on my skis.

Several ski seasons ago, when I arrived in mid-December, I found the mountains covered in mud. Only one chairlift was open, serving a few thousand excited skiers. Queues could take hours to get a flat, sparsely covered beginner to intermediate slope. The next day, it snowed heavily, and I had one of my epic powder days at my favorite forest-covered ski resort.

Bitcoin serves as a free-market indicator of global fiat currency liquidity. Its trading depends on expectations of future fiat currency supply. Sometimes reality aligns with these expectations, and sometimes it does not.

Money is politics. And ever-changing political rhetoric influences market expectations regarding the future supply of fiat currency.

One day, the US president called for pumping up the assets of his favorite supporters with larger-scale, lower-cost funding, and the next day he called for the opposite approach to combat the destruction of ordinary people and inflation.

Just like in science, in trading, it's worthwhile to have firm convictions, but also to maintain a flexible attitude.

Following the disastrous defeat of the US on "Day of Massive Tariffs" (April 2, 2025), I called for prices to only rise and never fall.

I believe that US President Trump and his Treasury Secretary, Buffalo Bill Bessent, have learned their lesson and are no longer trying to change the world’s financial and trade operating system too quickly.

In an effort to regain popularity, they will offer benefits to their supporters (who own substantial amounts of real estate, stocks, and cryptocurrencies), funded by printed money.

On April 9th, Trump "taco'd," announcing a tariff truce, turning what appeared to be the beginning of a Great Depression into the best buying opportunity of the year. Bitcoin rose 21%, with some altcoins (mainly Ethereum) also rising, as evidenced by Bitcoin's dominance dropping from 63% to 59%.

However, recently, the implied dollar liquidity forecast for Bitcoin has deteriorated. Since hitting an all-time high in early October, Bitcoin has fallen by 25%, and many altcoins have been hit harder than capitalists were in the New York City mayoral election.

What has changed?

The Trump administration's rhetoric remains unchanged. Trump continues to criticize the Federal Reserve for keeping interest rates too high. He and his deputies continue to talk about pumping up the housing market through various means.

Most importantly, at every turning point, Trump made concessions to China, postponing the forced reversal of the trade and financial imbalance between the two economic giants because such financial and political pain would be unbearable for politicians who have to face voters every two to four years.

What hasn't changed, but which the market now gives more weight to than politicians' rhetoric, is the contraction of dollar liquidity.

The US Dollar Liquidity Index (white line) has fallen 10% since April 9, 2025, while Bitcoin (gold line) has risen 12%. This divergence is partly due to the Trump administration's positive liquidity rhetoric. Part of the reason is that retail investors see inflows into Bitcoin ETFs and the DAT mNAV premium as evidence that institutional investors are seeking exposure to Bitcoin.

The narrative goes like this: institutional investors have flocked to Bitcoin ETFs. As you can see, net inflows between April and October provided sustained buying support for Bitcoin, despite a decline in dollar liquidity. I must add a caveat to this chart. The largest holders of the largest ETF (BlackRock IBIT US) are using the ETF as part of a basis trade; they are not bullish on Bitcoin.

They profited from the price difference by shorting CME-listed Bitcoin futures contracts while simultaneously buying ETFs.

This approach is capital efficient because their brokers typically allow them to use ETFs as collateral to pledge their short futures positions.

These are the five largest holders of IBIT US. They are large hedge funds or investment banks focused on proprietary trading, such as Goldman Sachs.

The chart above shows the annualized basis returns these funds earned by buying IBIT US and selling CME futures contracts.

Although the exchange mentioned above is Binance, the annualized basis on the CME is essentially the same. When the basis is significantly higher than the federal funds rate, hedge funds will flock to trade, creating a large and sustained net inflow into ETFs.

This creates a misconception among those unfamiliar with market microstructures that institutional investors have a huge interest in holding Bitcoin exposure, when in reality they don't care about Bitcoin at all; they're simply playing in our sandbox to earn a few percentage points above the federal funds rate. When the basis falls, they quickly sell off their positions. Recently, the ETF complex has recorded massive net outflows as the basis has declined.

Retail investors now believe that these institutional investors dislike Bitcoin, creating a negative feedback loop that prompts them to sell, which in turn lowers the basis, ultimately leading to more institutional investors selling off ETFs.

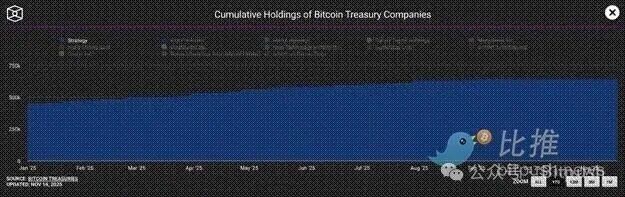

Digital asset trusts (DATs) offer institutional investors an alternative way to gain exposure to Bitcoin. Strategy (ticker symbol: MSTR US) is the largest DAT holder of Bitcoin. When its stock price is trading at a significant premium to its Bitcoin holdings (known as mNAV), the company can issue shares and use other financing methods to acquire Bitcoin at a lower price. As the premium decreases to a discount, Strategy's acquisition of Bitcoin slows down.

This is a chart of cumulative holdings, not the rate of change of that variable, but you can see that as Strategy's mNAV premium disappears, the growth rate of its holdings has slowed.

Despite the contraction in dollar liquidity since April 9, inflows into Bitcoin ETFs and purchases of DAT allowed Bitcoin to climb. But this situation has now ended.

The basis is no longer attractive enough to sustain institutional investor purchases of ETFs, and with most DATs trading at a discount to their mNAV, investors are now also avoiding these Bitcoin derivative securities. Without these flows to mask the negative liquidity conditions, Bitcoin must fall to reflect current short-term concerns that dollar liquidity will contract or grow less rapidly than politicians have promised.

Produce the evidence.

Now it's time for Trump and Bessett to produce evidence or shut up. Either they have the ability to put the Treasury above the Federal Reserve, create another housing bubble, and issue more stimulus checks, or they are a bunch of weak and incompetent liars.

To further complicate matters, Democratic Party members have found (unsurprisingly) that campaigning on affordability issues is a winning strategy. Whether the opposition delivers on promises like free transit cards, large numbers of rent-controlled apartments, and government-run grocery stores is irrelevant. The point is that American voters want to be heard and, at least, to have the self-deception that someone is thinking of them. People don't want Trump and his "Make America Great Again" (MAGA) supporters using fake news to mask the inflation they see and feel every day.

They want to be heard, just as Trump told them in 2016 and 2020 that he would crack down on and deport “people of color” so that their high-paying jobs would magically reappear.

For those with a multi-year outlook, these short-term stagnations in the rate of fiat currency creation are insignificant. If the red-camp Republicans cannot print enough money, the stock and bond markets will crash, forcing those dogmatic members of both parties back to the Satanic cult of money printing.

Trump is a shrewd politician, much like his predecessor Biden—who also faced similar discontent over inflation triggered by COVID-19 stimulus measures—he will publicly shift gears, attacking the Federal Reserve as the culprit behind the inflation plaguing ordinary voters. But don't worry, Trump won't forget the wealthy asset holders who finance his campaign. "Buffalo Bill" Bessant will be given strict orders to print money in creative ways incomprehensible to the average person.

Remember this 2022 photo? Our favorite "sycophant," Federal Reserve Chairman Jerome Powell, was being lectured by former President Joe Biden and Treasury Secretary Janet Yellen. Biden explained to his supporters that Powell would crush inflation. Then, because he needed to boost the financial assets of the wealthy who got him to power, he told Yellen to reverse all of Powell's rate hikes and balance sheet contraction at all costs.

Yellen issued more Treasury bills than notes or bonds from the third quarter of 2022 to the first quarter of 2025, which drained $2.5 trillion from the Fed’s reverse repurchase program, thus pumping up stocks, housing, gold and cryptocurrencies.

For ordinary voters—and some of you readers—what I just wrote may seem like gibberish, and that's precisely the crux of the matter. The inflation you are experiencing is the very thing that politician who claims to care about solving the burdens on ordinary people has created.

"Buffalo Bill" Bessant must work a similar magic trick. I'm 100% confident he'll devise a similar outcome. He's one of the greatest masters of currency market channels and currency trading in history.

What is the situation?

The market setups in the second half of 2023 and the second half of 2025 bear a striking resemblance. The debt ceiling battles ended in midsummer (June 3, 2023 and July 4, 2025), forcing the Treasury to rebuild the General Account (TGA), thereby drawing liquidity from the system.

2023:

2025:

"Bad Girl" Yellen has won over her boss. Can "Buffalo Bill" Bessant find his "BB" and reshape the market with Bismarck-like methods so that Republicans can win the votes of voters who hold financial assets in the 2026 midterm elections?

To dispel the notion that they should allow credit to contract, the market presents a Hobson's Choice. Once investors realize that printing money is prohibited in the short term, stock and bond prices will plummet. At this point, politicians must either print money to rescue the highly leveraged fiat currency financial system supporting the broader economy, but this would lead to renewed inflation, or allow credit to contract, which would destroy wealthy asset holders and cause mass unemployment as over-leveraged firms are forced to cut output and jobs.

The latter is generally more politically acceptable because 1930s-style unemployment and financial distress are always the losers in elections, while inflation is a silent killer that can be hidden through subsidies to the poor funded by printing money.

Just as I have confidence in Hokkaido's "snowmaking machine," I am 100% certain that Trump and Bessant want their Red Camp Republicans to remain in power.

Therefore, they will find a way to be tough on inflation while printing the necessary money to continue supporting the Keynesian "fractional reserve bank" scam in the current state of the US and global economies.

On a mountain, arriving too early can sometimes lead to a slippery slope. In the financial markets, before we return to an "up-only" world, in Nelly's words, the market must first "Drop Down and Get Their Eagle On." (By the way, they don't make music videos like they used to.)

The Bull Case

The argument contrary to my negative dollar liquidity theory is that as the US government resumes operations after the shutdown, TGA will quickly decrease by $100 billion to $150 billion to reach the $850 billion target, which will increase liquidity in the system. Furthermore, the Federal Reserve will stop shrinking its balance sheet on December 1st and soon resume balance sheet expansion through quantitative easing (QE).

I was initially optimistic about risk assets after the shutdown. However, as I delved deeper into the data, I noticed that approximately $1 trillion in dollar liquidity has evaporated since July, according to my index. Adding $150 billion is great, but what's next?

Although several Federal Reserve governors have hinted at the need to resume quantitative easing to rebuild bank reserves and ensure the proper functioning of the money market, this has remained mere rhetoric. We'll only know they're serious when Nick Timiraos of the Wall Street Journal, a Fed "whisperer," announces that a resumption of quantitative easing has received the green light. But we're not there yet. Meanwhile, the Standing Repo Facility will be used to print tens of billions of dollars to ensure the money market can cope with the massive issuance of Treasury bonds.

In theory, Bessant could reduce TGA to zero. Unfortunately, because the Treasury must roll over hundreds of billions of dollars in Treasury bills weekly, they must maintain a large cash buffer in case of unforeseen circumstances. They cannot afford the risk of defaulting on maturing Treasury bills, which precludes the possibility of immediately injecting the remaining $850 billion into the financial markets.

The privatization of government-backed mortgage lenders Fannie Mae and Freddie Mac is certain to happen, but not in the next few weeks. Banks will also fulfill their "duties" by providing loans to those who manufacture bombs, nuclear reactors, semiconductors, etc., but this too will happen over a longer period, and this credit will not immediately flow into the veins of the dollar money market.

The bulls are right; as time goes on, the printing presses will inevitably start churning out.

But first, the market must pull back the gains since April in order to better align with liquidity fundamentals.

Finally, before I discuss Maelstrom's positioning, I don't endorse the "four-year cycle." Bitcoin and certain altcoins only reach new all-time highs after the market has released enough tokens to accelerate the money printing process.

Maelstrom's positions

Last weekend, I increased our USD stablecoin position, anticipating lower cryptocurrency prices. In the short term, I believe the only cryptocurrency that can outperform the negative USD liquidity environment is Zcash ($ZEC).

With the rise of artificial intelligence, large tech companies, and large governments, privacy has largely vanished across the internet. Zcash and other privacy-focused cryptocurrencies using zero-knowledge proof encryption represent humanity's only chance to combat this new reality. This is why Balaji and others believe the grand narrative of privacy will drive the crypto market for years to come.

As a follower of Satoshi Nakamoto, I am offended that the third, fourth, and fifth largest cryptocurrencies are dollar derivatives, a coin that does nothing on an idle chain, and CZ's centralized computer.

If these are the second largest cryptocurrencies after Bitcoin and Ethereum in 15 years, what exactly are we doing?

I have no personal opinion on Paolo, Garlinghouse, and CZ; they are masters at creating value for their token holders. Please take note, fellow founders. But Zcash, or similar privacy cryptocurrencies, should follow closely behind Ethereum.

I believe the grassroots crypto community is waking up to the fact that what we tacitly support by giving these types of coins or tokens such high market capitalization is at odds with a decentralized future in which we, as flesh-and-blood human beings, retain agency in the face of tech, government, and AI giants.

Therefore, while we wait for Bessant to find his rhythm in printing money, Zcash, or another privacy-focused cryptocurrency, will enjoy long-term price increases.

Maelstrom remains a long-term bullish pick. If I have to buy back at a higher price (as I did earlier this year), that's okay. I proudly accept my losses because I have spare fiat currency on hand, allowing me to bet boldly and make it truly valuable. Having liquidity when the April 2025 scenario recurs is more decisive for your overall profit and loss over the cycle than having to give back small profits to the market due to trading losses.

Bitcoin has fallen from $125,000 to a low of $90,000, while the S&P 500 and Nasdaq 100 are hovering near all-time highs, which tells me that a credit event is brewing.

I confirmed this view when I observed the decline in my dollar liquidity index since July.

If I am correct, a 10% to 20% correction in the stock market, coupled with 10-year Treasury yields approaching 5%, would be enough to create a sense of urgency and prompt the Federal Reserve, the Treasury, or another U.S. government agency to introduce some form of money printing program.

During this period of weakness, Bitcoin could absolutely fall to $80,000 to $85,000. However, if the broader risk markets implode and the Federal Reserve and Treasury accelerate their money-printing frenzy, then Bitcoin could surge to $200,000 or even $250,000 by the end of the year.