Written by: Will Awang

By 2025, spending stablecoins on daily consumption will no longer be a romantic notion of "global financial equality and financial inclusion," but a tangible reality.

While the broader crypto market continues to fluctuate between bull market cycles and regulatory readjustments, with most activity still focused on key infrastructure such as capital flows, remittances, and decentralized finance (DeFi), stablecoins have carved out a lasting niche market: they are being used for payments and consumption, not just for storage or trading.

However, closer observation reveals that less than 10% of these activities are linked to actual spending—that is, the purchase of goods and services.

However, this seemingly insignificant 10% is expanding at a visible pace, quietly rewriting the rules in the cracks of daily life: from street stalls to cross-border remittances, stablecoins are no longer just toys for "crypto geeks," but real payment options in consumers' pockets. Businesses are following suit, and capital and products are beginning to strategize around this small spark.

Consumers using stablecoins for daily expenses are like sparks igniting from the bottom up. Whether these sparks can spread depends on who seizes the initial flame and ignites a chain of subsequent demands. To this end, we have compiled "Where are stablecoins being spent?" and incorporated firsthand observations, attempting to pinpoint that initial glimmer of light and trace its trajectory.

I. Overview of the Consumer Market

Stablecoins have gained significant traction in the B2B enterprise payments sector. Companies in logistics, software, and financial services are using stablecoins for cross-border supplier payments, contractor payroll, and treasury operations. The stablecoin B2B economy is estimated to be operating at $36 billion annually, and its growth is accelerating as regulatory transparency increases in major markets such as the US (GENIUS Act), the EU (MiCA), and Hong Kong.

In the B2C consumer spending sector, growth has been relatively slow, but the trend is positive. Globally, over 25,000 merchants already accept stablecoins for e-commerce transactions, and point-of-sale (POS) pilot programs are underway in parts of Southeast Asia and Latin America.

Early adopters of stablecoin spending include digital commerce, travel, hospitality, and gaming.

Payment infrastructure providers are driving the use of stablecoins in everyday environments, enabling users to spend USDC, USDT, and other tokens without relying on native crypto applications. In 2025, Blue Origin began accepting stablecoin-pegged debit cards, which users could use to pay for spaceflight bookings. Uber is reportedly piloting cryptocurrency payments to drivers in Latin America. Web3 native gaming platforms are using stablecoins for in-game purchases, supporting chargeback-free microtransactions, and enabling fast settlements between global users.

Despite these advances, retail transactions still account for less than 5% of global stablecoin usage, highlighting a significant gap between infrastructure availability and consumer behavior.

For institutions, the conclusion is obvious: stablecoins have become a reality for daily consumption, but their distribution is extremely uneven.

Geographically, emerging markets are leading the way in practical applications. In Latin America, stablecoins are increasingly being used in pharmacies, cafes, and local merchants, often as a hedge against inflation or as an alternative to traditional banking services. In sub-Saharan Africa and Southeast Asia, stablecoins are being used to access global goods and services that are otherwise inaccessible due to fragmented payment channels.

B2B funding flows are growing the fastest, representing the most readily available opportunity for stablecoin infrastructure providers, exchanges, and fintech platforms. While retail and consumer adoption is smaller in scale, it is strategically significant, especially in regions where stablecoins are effectively addressing financial pain points.

The infrastructure is in place, and regulation is catching up. Now, the key to competition lies in distribution capabilities, user experience, and corporate partnerships. Stablecoins are no longer just "payment gateways"; they are entering the checkout process and officially appearing on balance sheets.

II. The Consumer Economy of Stablecoins

The data above paints a clear picture: despite increasingly mature infrastructure and expanding real-world use, the vast majority of stablecoin activity remains at the financial application level—trading, liquidity provision, and remittance channels. Only a small, but increasingly meaningful, segment of activity truly impacts the consumer economy, and businesses are shifting their focus accordingly.

2.1 Use Cases for Stablecoins

Despite their growing popularity, stablecoins remain primarily financial instruments. Globally, approximately 67% of usage is still dominated by decentralized finance (DeFi), liquidity management, and speculative exchanges; these are not "daily consumption" activities, but rather capital flows aimed at efficiency and arbitrage. Another 15% of stablecoin transactions involve "payment-like" cross-border remittances, rarely entering formal commercial channels such as sales terminals or invoice settlements.

Only about 5% of the global stablecoin market capitalization is directly used by merchants—whether in brick-and-mortar retail, e-commerce, or service industries such as hotels and gaming. This figure, derived from merchant processing data and on-chain analytics, highlights that stablecoins are still in their infancy in consumer scenarios, although this is a significant increase compared to previous years and continues to rise quarter-on-quarter. The remaining 10% is used for hedging against inflation and as a stable value store.

2.2 Consumption Patterns: Behavior, Timing, and Incentives

Where stablecoin payments do actually occur at the retail level, the data reveals several clear patterns.

- Transaction amounts are often slightly higher than local fiat currency payments, partly due to consumers’ perception that stablecoins are “more valuable and more stable than local currency”; large-scale one-time purchases or stockpiling are common in grocery stores and pharmacies.

- There is also a unique rhythm in terms of time: in urban areas, more stablecoin transactions occur in the morning and evening of the weekday, coinciding with the commuting and lunch break windows; while they drop slightly on weekends, possibly because leisure spending relies more on cash or mobile banking.

- Incentive programs are becoming key to user retention. Many merchants in Latin America and Eastern Europe are offering around 1% cashback on stablecoin purchases, combined with gamified points within wallets. This is particularly popular among young people who already hold crypto assets, as they value the instant rewards.

Interestingly, some merchants reported that stablecoin users are more willing to tip, especially in the service industry, such as food and beauty. This may reflect a psychological disconnect from the consumption context, or it may reflect consumers' desire to "support" merchants who support crypto consumption.

Another characteristic of cryptocurrency payments is higher consumer spending. The American Automobile Association (AAA) predicts that by 2024, the average amount paid with cryptocurrency will be 30% higher than traditional payment methods. The travel and hospitality industry accounts for 14% of these cryptocurrency transactions. Airlines accepting cryptocurrency payments have seen a 40% increase in bookings.

Travala processed over $100 million in booking revenue last year, of which $80 million was in cryptocurrency, representing an 80% year-over-year increase. It noted that cryptocurrency users spent 2.5 times more per booking than non-crypto users and had three times the lifetime value. Accepting cryptocurrency allows travel providers to attract both a growing mass-market clientele and ultra-high-end consumers, creating a kind of "crypto wealth effect"—users who profit from cryptocurrency gains are more willing to spend.

In this regard, cryptocurrencies are booming in two ways: first, with severe inflation in developing markets, many unbanked consumers are starting to book budget travel; and second, elite cryptocurrency holders are starting to book luxury experiences.

2.3 How can stablecoins be widely adopted in daily consumption?

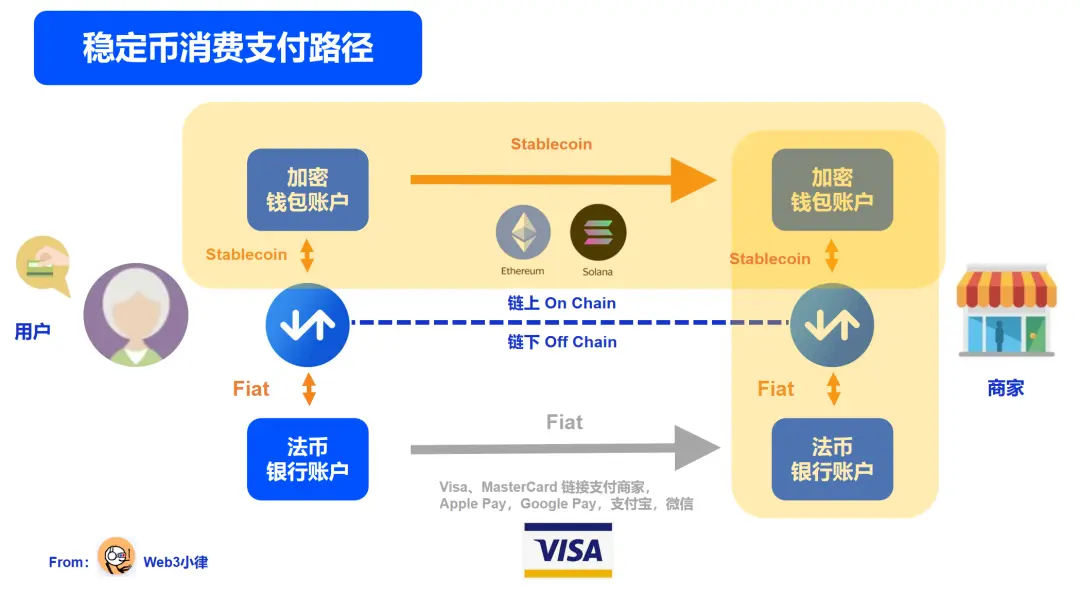

The integration of stablecoin payments into retail POS systems remains fragmented. Although all are called stablecoin acquiring, the implementation paths in the market currently fall into two main categories:

A. Independent Wallet Integration – Directly connect to USDC, USDT, or regional stablecoin wallets via QR code payment systems. This type of solution typically requires no new hardware purchase and can be launched within days, making it highly attractive to small businesses.

This model doesn't change the merchant's QR code payment system; merchants still receive fiat currency, while stablecoin exchange is moved to the wallet's acquiring side. Its advantages are clear: it seamlessly integrates into the existing global fiat currency QR code system, eliminating barriers to the promotion and adoption of stablecoin acquiring on the merchant side. This is why we see seamless integration of encrypted wallets in regions with unified QR codes (such as Vietnam and Brazil).

Funding flow: Users pay with stablecoins, wallets/service providers redeem them for fiat currency, and then settle accounts with merchants using fiat currency.

B. Gateways and POS systems directly integrate stablecoin payments. Gateway and POS systems integrate stablecoins into platforms like Shopify, WooCommerce, and Magento via plugins and APIs, allowing merchants to accept token payments without restructuring their checkout processes. This approach requires strong bargaining power and market relations capabilities, and is typically led by large companies that directly integrate stablecoins into their gateway and POS systems. It offers clear advantages, securing merchant-side resources.

Large retailers, especially those with existing payment infrastructure, are beginning to partner with native cryptocurrency payment processors. Companies like BitPay, Flexa, Coingate, Circle Pay, and NowPayments offer APIs and merchant back-end systems that integrate stablecoin payments with fiat currency settlements. For example, a merchant can accept USDC at the checkout and receive payment in USD or EUR after closing time, completely mitigating volatility risk. Furthermore, several next-generation POS providers are launching hybrid terminals that support both traditional card payments and digital assets, with early deployments in markets including Brazil, Turkey, and Kenya.

Funding flow: Users pay with stablecoins, and merchants can choose to receive either stablecoins or fiat currency through a payment service provider (dual wallet account).

Examples of some POS providers are shown below:

- Brazil: Cielo (integrated with Binance Pay)

- Türkiye: PayTR (supported by NOWPayments); Paribu (local cryptocurrency exchange)

- Kenya: M-Pesa (integrated with BitPay); Kopo Kopo (integrated with CoinPayments)

The key to driving widespread adoption lies in customer experience and, more importantly, user guidance, especially for those unfamiliar with crypto wallets. Some merchants have begun posting educational notices in their stores or training their employees, while others are trying to attract customers through reward mechanisms. From a backend perspective, merchants still face obstacles in areas such as receipt generation, accounting system integration, and tax documentation. These often become bottlenecks for more established businesses to further adopt stablecoin payments.

2.4 Payment Infrastructure and Routing Mechanism

Supporting this shift is an increasingly mature stablecoin payment infrastructure. Currently, two main technological paths are emerging:

Stablecoin settlement mode: Stablecoins such as USDC are directly credited to your crypto wallet;

Hybrid routing mode: Stablecoins are automatically converted into fiat currency at the moment of payment, ensuring predictable returns and shielding merchants from volatility risks.

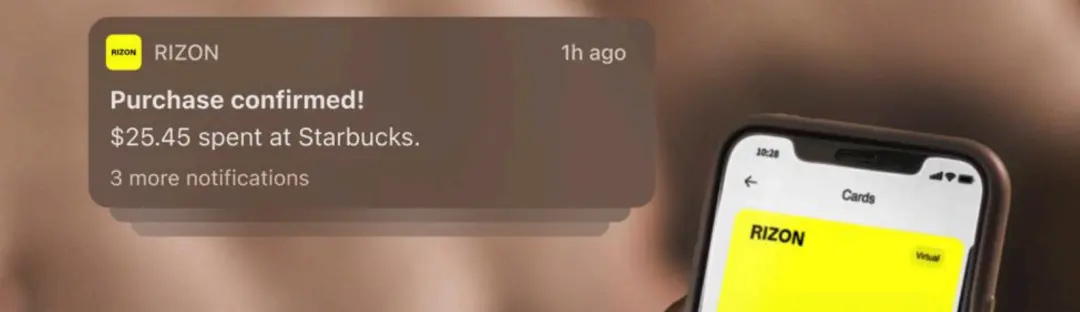

Fintech providers focused on crypto payments are expanding rapidly; card issuer Rizon has launched a stablecoin-backed Visa card, usable at over 150 million merchants in more than 90 countries, and supporting Apple Pay, Google Pay, and the Visa acceptance network. Meanwhile, Fiserv has partnered with Mastercard to issue the FIUSD stablecoin, aiming to allow smaller banks and their merchants to quickly access the stablecoin market.

For e-commerce merchants, they are reaping tangible benefits from stablecoin integration, with key highlights including:

- Recurring deductions and subscriptions: Eliminate card network chargebacks and delays with instant, programmable payments;

- Cross-border shopping is smoother: stablecoins bypass foreign exchange fees, exchange delays, and counterparty risks associated with traditional channels;

- Payment is final and irrevocable: significantly reduces the burden of fraud and operations due to chargebacks and disputes.

Data confirms this trend. A Fireblocks survey shows that 48% of enterprises cite "settlement efficiency" as their primary motivation for adopting stablecoins, 30% value "cost savings," and over 86% believe that "the infrastructure is ready and can be implemented immediately." The result is faster customer experience, lower operational risk, wider global payment reach, and all transactions are transparent and traceable at the ledger level.

III. Stablecoin Adoption Across Industries

In 2024, according to data from Visa's Allium, stablecoins facilitated $27.6 trillion in transaction value across 5.6 billion on-chain transactions. However, after excluding speculative and DeFi flows, only 5% (approximately $1.3 trillion) were real-world payments, with P2P accounting for 2%, B2C retail for 2%, and B2B commerce for 2%.

A McKinsey report states that stablecoin annual transaction volume has exceeded $27 trillion, with daily payment-related throughput estimated at between $20 billion and $30 billion, still less than 1% of global money transfers. While B2B flows have a significant operational impact, they only average around $400-500 billion annually, on par with broader merchant and institutional usage.

3.1 Retail stores were the first industry vertical to show signs of emerging trends.

Currently, stablecoin usage in brick-and-mortar retail remains limited, but early adopters have demonstrated its real-world usability and increasing practicality. While lagging behind e-commerce and B2B sectors, a significant increase in stablecoin acceptance among small and medium-sized merchants—particularly in emerging markets and crypto-friendly urban centers—is expected by 2025.

In the realm of brick-and-mortar stores daring to innovate, several categories stand out. Supermarkets and grocery chains are among the most pragmatic scenarios, especially in economies experiencing significant currency fluctuations. In Argentina and Venezuela, where inflation continues to erode purchasing power, many grocery stores now accept USDC and USDT directly at their checkouts, with customers frequently using mobile wallets or QR codes for payment. Specific examples include:

- Buenos Aires Central Market: Tether has partnered with KriptonMarket to enable merchants at this large wholesale and retail fruit and vegetable market to settle transactions in USDT.

- Several grocery stores in Buenos Aires' Villa Crespo district are accepting USDT via QR code payments through Binance Pay, a response to a shortage of US dollars in cash.

Restaurants are also embracing stablecoins, especially cafes, fast-casual eateries, and food trucks. In El Salvador, while Bitcoin initially made headlines, stablecoins are now quietly becoming a preferred digital payment method for city dwellers. Some examples:

- McDonald's supports USDT and USDC (via Strike and Bitfinex).

- Starbucks – Supports USDT and USDC (via Chivo and Strike)

- Wendy's Burgers - Supports USDT and USDC (via payment processors)

- Subway – Supports USDT and USDC (via Strike and CoinGate)

- Local restaurants in Elzont (“Bitcoin Beach”)

- Juice bars and street vendors in San Salvador and La Libertad

3.2 Current Status of Retail and E-commerce Adoption

Merchant acceptance of stablecoins is increasing, but the distribution is extremely uneven. As of mid-2025, more than 25,000 merchants worldwide supported stablecoins, primarily online, with a small number also penetrating physical stores. The most common mainstream assets are USDC, USDT, and PYUSD, typically integrated through native crypto checkout processors or stablecoin-linked Visa and Mastercard channels.

In terms of merchant and user penetration, institutional adoption continues to climb. NOWPayments points out that stablecoins now account for 57% of all merchant crypto payments, significantly higher than 7% in 2020. With over 25,000 merchants globally in retail channels, B2C penetration on e-commerce and digital platforms is deepening. User engagement is also expanding: over 150 million blockchain addresses hold stablecoins, and approximately 10 million addresses conduct stablecoin transactions daily, indicating widespread and active use. Notably, consumer demand is strongest in emerging markets such as Latin America and Africa, where institutional stablecoin payments have increased by over 200% year-on-year.

According to data from Visa's blockchain analytics division, the vast majority of on-chain stablecoin flows remain high-value B2B transfers, rather than low-value purchases in shopping carts or restaurant receipts. For stablecoins to achieve substantial adoption at checkout, the infrastructure must continue to improve, particularly in key areas such as user experience, instant fiat currency exchange, tax reporting, and merchant incentives.

New use cases continue to emerge, with some platforms offering cashback rewards to encourage customers to choose stablecoins at checkout, where fees are lower than traditional bank cards. In certain markets, merchants directly benefit from receiving stablecoins, as the processing costs are virtually zero compared to the 2%–4% fees charged by traditional payment networks.

3.3 Travel and Hospitality Industry: Early Trials, Initial Momentum Emerging

Consumer spending on travel, hotels, and digital entertainment remains limited, but the industry as a whole is actively experimenting with stablecoin payments at a strategic level. However, these use cases are still considered fringe scenarios, driven more by crypto-native users than by mass market demand.

A recent travel industry analysis, "The Rise of Cryptocurrency in Travel," points out that although cryptocurrencies currently account for less than 1% of leisure travel spending, this proportion is expected to climb to 3%–5% by 2030. Stablecoins are seen as a leading force driving this shift due to their predictable prices and efficient settlement.

Cryptorefills claims that in 2024, over 80% of its users made at least one cryptocurrency purchase per month. Travel is one of the company's fastest-growing sectors, primarily driven by digital nomads and conference travelers who also use the platform to purchase eSIM cards, book travel services, and top up their accounts. Cryptorefills is a B2C platform that offers cryptocurrency-based flight and hotel bookings.

Travala, an online travel agency (OTA) specializing in cryptocurrency, reports that "our largest customer base currently consists of digital nomads and conference travelers, with bookings typically targeting mid-range clients. In 2024, approximately 78% of bookings were completed using cryptocurrency, compared to less than 8% for credit and debit cards." Cryptocurrency is also attracting high-net-worth individuals. "The luxury market has enormous potential." Travala's concierge service targets this segment, providing personalized, high-end travel advisors.

More notably, in the UAE—a hub of luxury experiences and regulatory innovation—43% of five-star hotels now accept crypto payments. Travala, a purely digital travel platform, presents an even more aggressive usage curve: in September 2024, 77% of its orders were paid for with cryptocurrency, the vast majority of which were stablecoins.

These data mark a turning point: boutique resorts and forward-thinking chain brands are offering stablecoin options not as a gimmick, but out of consideration for competitive differentiation and global appeal. Within the broader travel ecosystem, stablecoins are becoming a tool for "end-to-end payment":

- From June 2024 to June 2025, crypto payments in the tourism industry surged by 38% year-on-year, with more than 40% of them being completed using stablecoins.

- Stablecoins were used to book rooms, flights, spas, and transfers, with the average transaction amount reaching 2.5 times the average transaction value of traditional legal tender, demonstrating a high average transaction value.

The figures above indicate that consumers are increasingly viewing stablecoins as a trusted medium of exchange, not only for simple bookings but also for carefully curated full-service travel experiences.

3.4 About the gaming industry

In contrast, the gaming industry is proving to be fertile ground for increasingly robust stablecoin spending. Many Web3 native games and virtual environments now accept stablecoins for in-game purchases, NFT transactions, and peer-to-peer settlements between players.

For example, Fortnite, developed by Epic Games, is a centralized, non-Web3 game, but certain third-party payment solutions have enabled stablecoin-based transactions, allowing players to purchase in-game currencies (such as V-Bucks) using stablecoins like USDC. For instance, payment platforms like TransFi have been integrated into the game's ecosystem, providing players with these stablecoin payment channels.

Globally, over 35% of players have used cryptocurrency for at least one purchase, whether for items, tournament entry fees, or subscriptions; of these, a staggering 70% of transactions utilize stablecoins. The blockchain gaming market is experiencing explosive growth: driven by a 52% compound annual growth rate (CAGR), the global blockchain gaming market is projected to reach $85 billion by the end of 2025.

"Play-to-Earn" (P2E) games, which use stablecoins to distribute rewards, contribute 62% of the market's revenue. At the platform level, 93% of blockchain games have integrated wallet support (such as MetaMask and Phantom), and 37% have introduced metaverse elements, creating more consumption scenarios for character skins, upgrade items, and social interactions.

Similarly, market valuations reflect scale: tokenized real estate on the Metaverse platform now exceeds $112 billion.

Beyond gaming itself, stablecoins are at the heart of the high-value economy of virtual goods. In 2025, the total value of the metaverse market reached $316 billion, with $880 billion of digital goods transactions completed using stablecoins. Transactions of virtual real estate, virtual avatars, and tokenized assets are rapidly expanding: leading metaverse platform Decentraland earned over $275 million in 2025 solely from virtual land and digital asset transactions, with stablecoins being the primary settlement currency.

Behind this value is a surge in the user base: 70 million users utilize Metaverse Financial Services monthly, with $2.2 billion in transactions flowing daily through these virtual settlement systems. With their stable value and rapid settlement, stablecoins have become a natural choice for high-frequency trading in the immersive economy.

By 2025, the gaming and entertainment ecosystem had adopted stablecoins as the primary medium of exchange, significantly accelerating in-game economies, virtual experiences, and hybrid scenarios that blend with the real world.

3.5 Enterprise B2B Payment

A. Cost reduction and efficiency improvement

For businesses, efficiency, rather than cost, remains the primary consideration. Fireblocks research shows that 48% of businesses cite settlement efficiency as the biggest benefit of stablecoins, 30% mention cost savings, and 86% claim their existing infrastructure is ready for deployment. Improved operational efficiency is also noteworthy: a 2025 analysis shows that stablecoin settlement systems have reduced remittance and settlement fees to approximately 2.5%, while traditional bank channels can reach up to 5%.

Cryptocurrencies enable direct transactions without banks, thereby reducing costs and increasing profit margins. Travala estimates that the tourism industry processes over $11 trillion in transactions annually, and if blockchain-based solutions were adopted to reduce fees to 0.1%, $270 billion could be saved annually. “These advantages are significant: using stablecoins on high-speed networks, fees below one cent, near-instant confirmation, no chargebacks, and settlements available 24/7.”

B2B transactions can also benefit from this, enabling real-time settlement, eliminating currency exchange risks, and reducing the need for upfront payments. However, not all crypto solutions are created equal.

Future Adoption Trajectory: Accelerated Merchant Penetration – Over 57% of crypto merchant payments are now settled in stablecoins; Expanding User Activity – Millions of active wallets and transactions daily. Operational Benefits: Settlement speed takes precedence over cost savings; Infrastructure readiness and regulatory synergy are rapidly reducing friction; Decreasing costs and transparency make stablecoins an efficient alternative for cross-border and digital commerce.

B. Payment Application Scenarios

a. Stablecoins used for supplier, vendor, and payroll payments

According to PYMNTS data, the annual volume of B2B stablecoin transactions has reached $36 billion, constituting the largest segment in the practical application of stablecoins, surpassing P2P and card-linked payments. Artemis Analytics also supports this ranking, estimating that B2B stablecoin payments account for 50% of total payments. Demand is driven by global manufacturers, logistics providers, and service companies, who are increasingly using stablecoins to settle cross-border supplier invoices, pay overseas contractors, and streamline payroll.

b. Partnership and Hosting Solutions: Enterprise-Grade Infrastructure

Mastercard is integrating the FIUSD stablecoin into its payment ecosystem, making it available to merchants and businesses across its network of over 150 million merchants. Meanwhile, Fiserv plans to launch a stablecoin-powered digital asset banking platform, widely supported by Circle, Paxos, and Solana, bringing regional and community banks into the stablecoin payment system. Major banks such as Bank of America, JPMorgan Chase, Standard Chartered, PayPal, and Stripe are actively developing stablecoin issuance and integration strategies, targeting B2B and trade corridors. Corporate and fintech wallets, SAFE tools, and treasury management systems are now natively designed or upgraded to handle stablecoin flows, enabling businesses to allocate funds with programmable precision, built-in compliance, and integration with legacy systems.

The core value proposition focuses on instant settlement, avoiding exchange rate fluctuations, and near-frictionless channels, especially benefiting markets where traditional banking services are underserved.

c. Liquidity and Cash Management: Internal Fund Transfers

Large enterprises and treasury departments are using stablecoins as programmable liquidity tools. JPMorgan's digital dollar and euro token now handle over $1 billion in institutional transactions daily, demonstrating their deep integration into automated cash operations. This expanding scale uses stablecoins as real-time cash conduits, enabling instantaneous internal transfers, automated cash collection across jurisdictions, and seamless movement between fiat currency and on-chain digital assets through custody platforms.

"The new bank set the standard for what a digital bank should look like, but it never touched the core infrastructure. Stablecoins were that upgrade. The combination of the two unlocks everything a digital bank should have: instant transfers, low remittance costs, and access to global stablecoins."

——RIZON

IV. The Rise of Emerging Banks

With its digital-first infrastructure, user-friendly interface, and global accessibility, the new bank has become a bridge between traditional finance and the crypto-native economy. Rizon's analysis highlights its potential: by 2025, with increased regulatory clarity and growing user demand for borderless currencies, the new bank is uniquely positioned to integrate stablecoins into the everyday banking experience—from payroll to payments and savings.

In 2025, the number of new bank users worldwide will exceed 600 million, compared to only 394 million in 2023, representing a compound annual growth rate of over 30% in recent years.

Major players are making moves. Revolut and N26 are expanding their crypto services to include stablecoin transfers and payments; Monzo and Wise are exploring instant, zero-foreign-dollar cross-border remittances through regulated stablecoin channels. In emerging markets, new banks like Nubank (Brazil) and Maya (Philippines) have piloted stablecoin-linked wallets for merchant payments and payroll. By embedding stablecoins into their core products, these new banks are becoming gateways for millions of users to “spend digital dollars, not just transact digital dollars.”

4.1 Rizon's Stablecoin Emerging Bank Case Study

Rizon, launched in 2025, is a next-generation non-custodial stablecoin application designed to make the "digital dollar" truly usable. Operating in over 110 countries, it allows users to deposit, transfer, spend, invest, and receive stablecoins such as USDC and USDT at low cost and near real-time. Through virtual and physical Visa cards, users can use stablecoins at over 100 million merchants and ATMs worldwide, covering all traditional card-swiping scenarios.

The non-custodial architecture ensures users have complete control over their funds and private keys. Rizon now supports tokenized stock trading, 5% cashback on purchases, and the RizPoints loyalty program, redeemable for airline tickets, hotel stays, and gift cards. Rizon's mission is simple: to make stablecoins a viable alternative to the outdated banking system. Rizon is more than just a crypto wallet; it's a modern financial gateway, enabling users worldwide to access secure, stable, and intelligent cross-border financial tools anytime, anywhere.

As the first new bank to fully integrate stablecoin accounts, cards, and APIs into the financial stack, Rizon allows users and businesses to hold, spend, and settle stablecoins as easily as fiat currency. Through direct integration with Visa, Rizon enables stablecoin spending at over 150 million merchants worldwide, eliminating exchange friction and unlocking real-world utility. With its non-custodial model, it can be used globally by anyone with a smartphone and internet connection.

Rizon's analysis highlights its potential: global remittances are projected to reach $913 billion by 2025, and stablecoins could save $39 billion in remittance fees annually, becoming a key driver of everyday cross-border payments.

"The nature of money is changing. While the internet has transformed how we work, communicate, and shop, our financial system remains outdated: slow, expensive, and inaccessible to billions."

The emergence of stablecoins has been a breakthrough: they are digital dollars backed 1:1 by real reserves, enabling instant, borderless, 24/7 transactions without banks or intermediaries. This is not just another crypto trend, but a fundamental shift in how money flows. However, stablecoins remain too complex for the average user.

At Rizon, we're building the next layer of currency: a simple, secure, and intuitive interface that makes stablecoins easily accessible to everyone. Just as new banks have done for fiat currencies, we're doing the same for the digital dollar—creating financial instruments that are inherently global, inherently fair, and built for those who need them most.

——IgnasSurvila, CEO & Co-founder @ RIZON

4.2 CoinGate's Stablecoin Payment and Settlement Services

CoinGate, founded in 2014 and headquartered in Lithuania, is a fintech and crypto payments company specializing in cryptocurrency payment processing and gateway services. Its platform helps merchants accept Bitcoin, stablecoins, and other digital assets, and provides fiat currency exchange services to mitigate volatility risks. Businesses can integrate CoinGate via API and mainstream e-commerce plugins to seamlessly access crypto payments globally.

The company also supports crypto fund distribution, invoicing, and treasury management functions, along with KYC/AML compliance mechanisms. CoinGate serves thousands of merchants, processes hundreds of thousands of crypto transactions annually, and is committed to building a bridge between traditional commerce and blockchain payments.

Since 2025, stablecoins have remained a mainstay of crypto payments on the CoinGate platform, but their share has shifted due to regulatory influence. As of this quarter, 31.3% of processed payments were settled in stablecoins. USDT remains the second most frequently used coin, accounting for 19.8% of all transactions; however, this data primarily reflects activity in the first quarter (before the MiCA regulations took effect), after which the platform delisted USDT as required by regulations. Meanwhile, USDC's transaction share has risen to 11.5%, ranking fourth. In terms of transaction value, stablecoins have an even more pronounced advantage, accounting for almost half of the total transaction volume.

The larger narrative lies in how MiCA is reshaping the market landscape. Due to its failure to meet MiCA's compliance requirements for stablecoins, USDT has been effectively delisted by numerous regulated platforms within the EU and EEA. Tether has explicitly stated that it will not cooperate in applying for compliance certification, significantly weakening its availability in regulated markets. Therefore, the decline in USDT usage on platforms is not due to reduced demand, but rather regulatory restrictions directly reducing its circulation. Conversely, USDC, having passed MiCA compliance certification and supporting multiple public chains, has experienced explosive growth: compared to the same period last year, USDC payments on CoinGate surged by 760%; usage increased more than sixfold from January to September 2025 alone. A clear "substitution effect" is observed—European merchants and consumers who previously used USDT are collectively migrating to USDC.

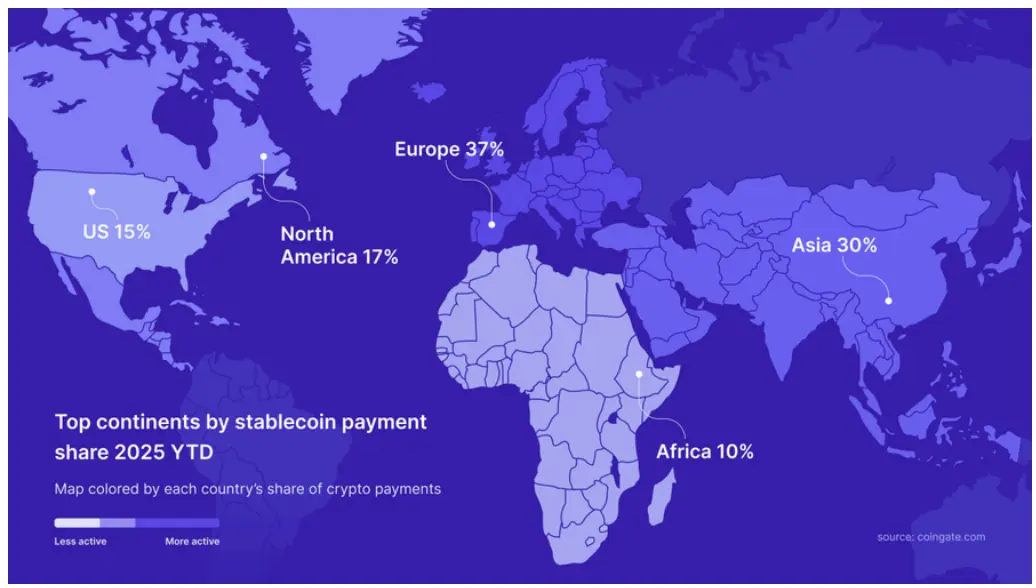

Regionally, the United States remains the largest single market for stablecoin payments with a 15% share. However, if Europe is considered as a whole, its order volume accounts for a staggering 37%, ranking first globally. Asia follows closely behind with 30%, primarily driven by India and Hong Kong. In Africa, Nigeria is the most prominent market.

In terms of use cases, stablecoins are most concentrated in digital-native industries, such as adult content, proxy services, and web hosting; at the same time, gaming, gift cards, and consumer e-commerce are also showing steady growth.

On the withdrawal side, the changes are even more significant: in 2025, 85% of merchant settlements on the CoinGate platform were paid in stablecoins. This indicates that for businesses, stablecoins are no longer just another payment option, but the preferred settlement layer for cross-border settlements, remittances, and B2B fund flows.

In summary, the data clearly shows that regulation has become one of the main forces influencing the adoption of stablecoins. The MiCA regulations in Europe have created a "natural experiment": in a regulated environment, USDT's market share is collapsing, while USDC is rapidly becoming the preferred stablecoin for both consumers and merchants.

V. Conclusion

By 2025, stablecoins will no longer be just theoretical tools; they are being used for spending, settlement, and large-scale applications in the real economy. From institutional liquidity pipelines to retail checkouts, stablecoins are quietly but decisively changing the way value flows. Although only about 5% of annual transaction volume (approximately $1.3 trillion) is linked to payments for actual goods and services, this small segment represents the fastest-growing category of on-chain value transfer. In areas such as B2B, e-commerce, hospitality, gaming, and P2P, stablecoin spending is moving from the periphery to mainstream functionality.