Preface

On April 7, 2025, during the Hong Kong Web3 Carnival, the Hong Kong Securities and Futures Commission issued a circular on virtual asset trading platforms providing staking services. The regulator said it “recognizes the potential benefits of staking in enhancing the security of blockchain networks and the possibility of investors making profits.”

After the circular was issued, China Asset Management and Bosera Asset Management, which have already issued Ethereum spot ETFs, responded quickly. On April 11, Bosera Asset Management announced that the Bosera Hashkey Virtual Asset Ethereum ETF has obtained regulatory approval and can pledge up to 30% of Ethereum holdings from April 25, 2025. On April 18, China Asset Management will launch a pledge service for its Ethereum spot ETF, becoming the second fund in Hong Kong to provide such services.

The biggest difference between PoS and PoW public chains is the staking service. Investors can stake their PoS public chain governance tokens to blockchain nodes or liquidity staking platforms to obtain the same income distribution as PoW public chain network nodes. Investors can not only obtain passive value-added income from tokens, but also active income.

In contrast, although many public funds in Hong Kong have also jointly launched Bitcoin ETF products with exchanges, the PoW public chain has not designed a pledge mechanism. The so-called BTC pledge concept on the chain is actually a lending service provided after bridging the EVM public chain. As a custodian, the Bitcoin spot ETF fund has no right to lend out customer assets. Therefore, investors in the Bitcoin ETF cannot obtain active returns through pledge.

Compared with the US Securities and Exchange Commission, the Hong Kong Securities and Futures Commission approved the staking service of the Ethereum spot ETF earlier. This is a milestone event for Hong Kong, which aims to become the Asian Web3 center. This not only reflects the in-depth research of the Hong Kong cryptocurrency regulatory authorities on the on-chain income distribution mechanism, but also shows the Hong Kong government's aggressive and open-minded policies on the crypto industry. For traditional financial investors, they should be more concerned about how much actual benefits the ETF staking service can bring to investors. The following will specifically analyze the benefits that ETH staking brings to investors and its impact on Hong Kong's Web3 industry.

1. What is the return on ETH staking?

China Asset Management and Bosera Asset Management launched staking services for their Ethereum spot ETFs in April, with their staking nodes provided by OSL Exchange and Hashkey Exchange respectively. Since the two companies have not yet disclosed the specific amount allocated to investors after staking, this article will provide a reference for investors based on the income from staking ETH on the chain.

1.1 ETH staking mechanism and on-chain staking income

Here we can briefly describe the pledge mechanism of the Ethereum public chain. The public chain is a "pipeline" that provides a network for on-chain address transactions. As a decentralized infrastructure, the public chain is composed of server nodes distributed all over the world. When the trader's transaction is confirmed by the node, the trader needs to pay the gas fee to the node. However, it is not enough to buy a server to become an Ethereum node. In addition to hardware equipment, 32 ETH need to be pledged to the official contract address to become a qualified node. In addition to the income from block rewards, nodes can also obtain MEV (maximum extractable value) income and tips paid by investors who preemptively trade to obtain income. For ETH holders, if they do not have sufficient financial strength to operate nodes, they can indirectly obtain a share of the node's revenue by pledging ETH to ETH pledge service providers such as Lido.

The yield obtained from ETH staking is determined by a formula: staking yield = (block reward income + MEV fee + Tips fee) / total value of staked ETH.

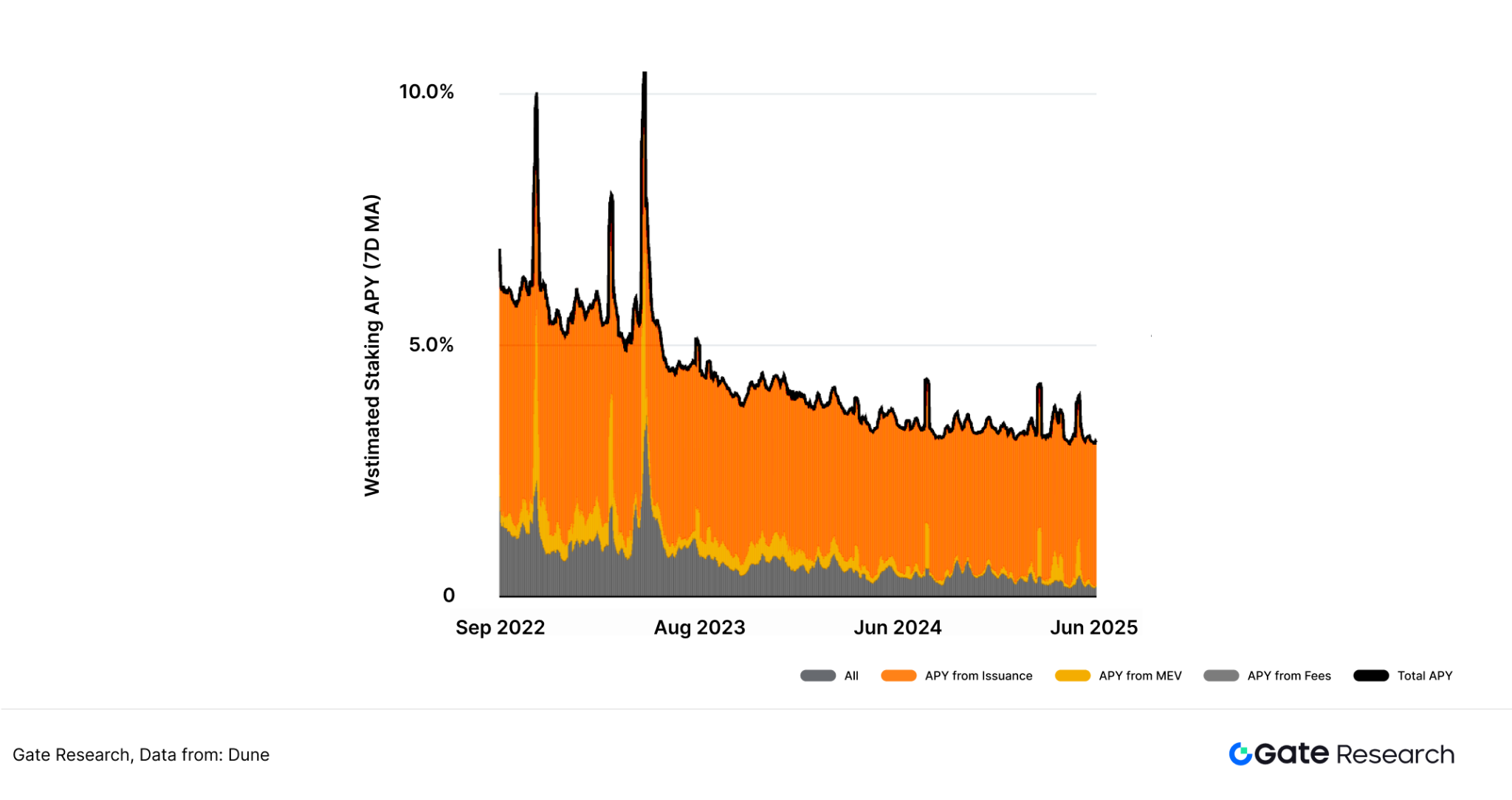

Figure 1: Annualized yield of Ethereum staking

According to statistics from the Dune Analytics platform, November 2022 is the end of the cryptocurrency bear market, but the APY (annual percentage yield) of ETH staking has remained stable at more than 5%, the highest in recent years. On the contrary, in December 2024, during the bull market of cryptocurrency, the APY of ETH staking was only about 3.3%. In May 2025, the APY of ETH staking was 3.07%. From the perspective of financial products, ETH staking cannot be considered a high-yield product [1].

In order to let more readers understand the changes in staking yields, this paragraph will break down the factors that affect the changes in staking yields in more detail. First of all, after the EIP-1599 proposal was passed, the block reward income obtained by the node was relatively stable and was only related to the consensus layer (Beacon Chain). The main factor for the rise in ETH staking APY is that MEV income and Tips income surged in a short period of time. Taking May 9, 2023 as an example, the APY of ETH staking on that day rose to 10.66%, of which the block reward yield obtained by the node was 3.81%, the MEV income of the node was 3.54%, and the Tips income of the node was 3.31%.

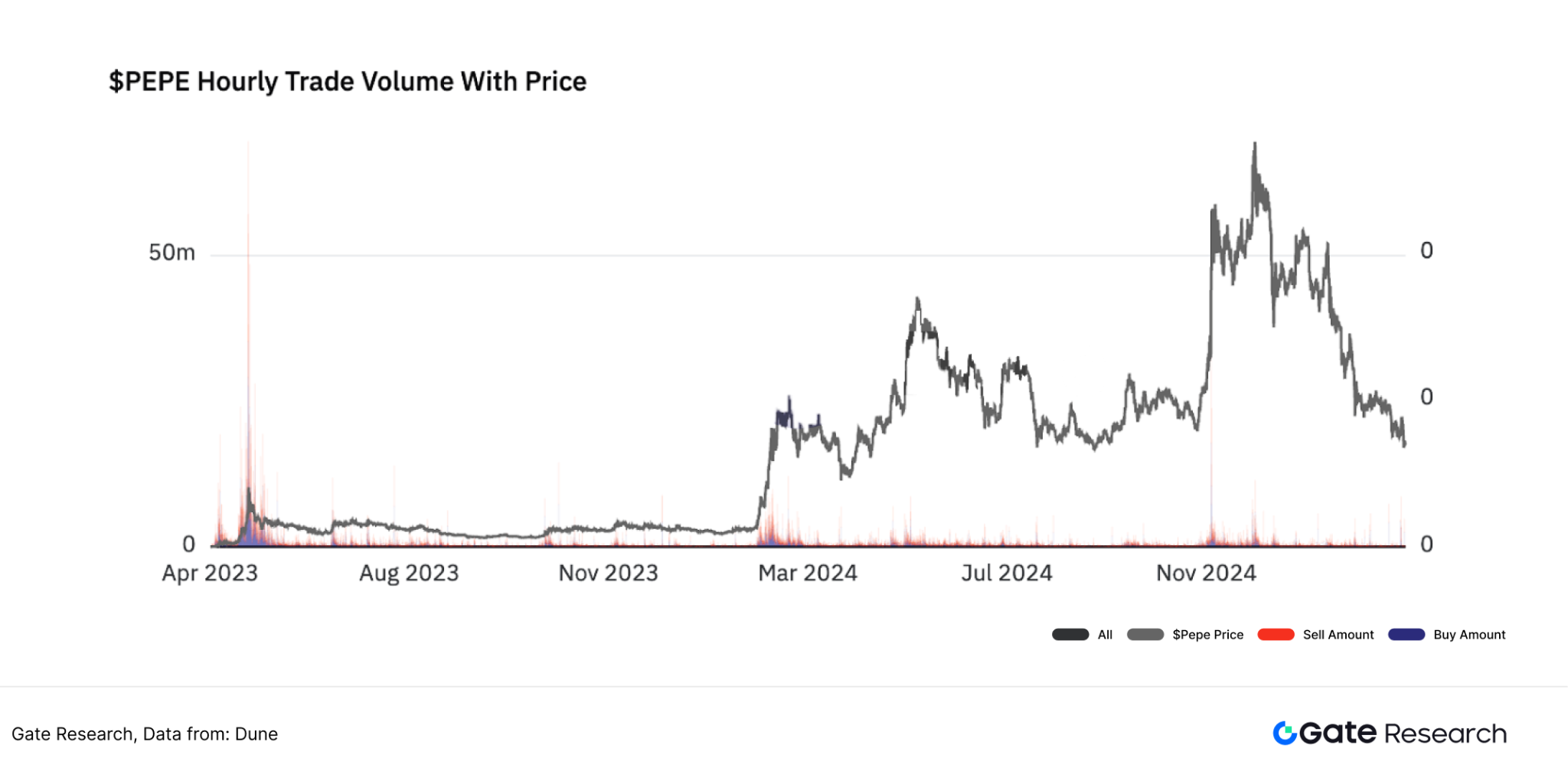

Back to early May 2023, the transaction volume of the Memecoin project PEPE soared during this period. Since the PEPE project was released on the Ethereum network in April 2023, its token market value has increased 70 times on May 5, reaching a stage peak. Investors were dominated by FOMO sentiment, and a large number of wallet addresses began to buy or sell PEPE. From May 6 to May 10, the market value of PEPE began to plunge, with a drop of more than 50%. In order to trade PEPE in advance, some users paid tips to the node to jump the queue. At the same time, the node can obtain the maximum on-chain value by manipulating the transaction order [2].

Figure 2: PEPE hourly trading volume and price

Once a token with a significant wealth-creating effect in a short period of time appears on the chain and forms a detonating flow, the Tips and MEV income obtained by the node will increase significantly. However, it should be noted that MEV income and Tips income are only related to the block-producing nodes, and are not evenly distributed. Therefore, in the future, the staking income of China Asset Management and Bosera Fund Ethereum ETF products will be closely related to the operation of OSL and Hashkey nodes respectively.

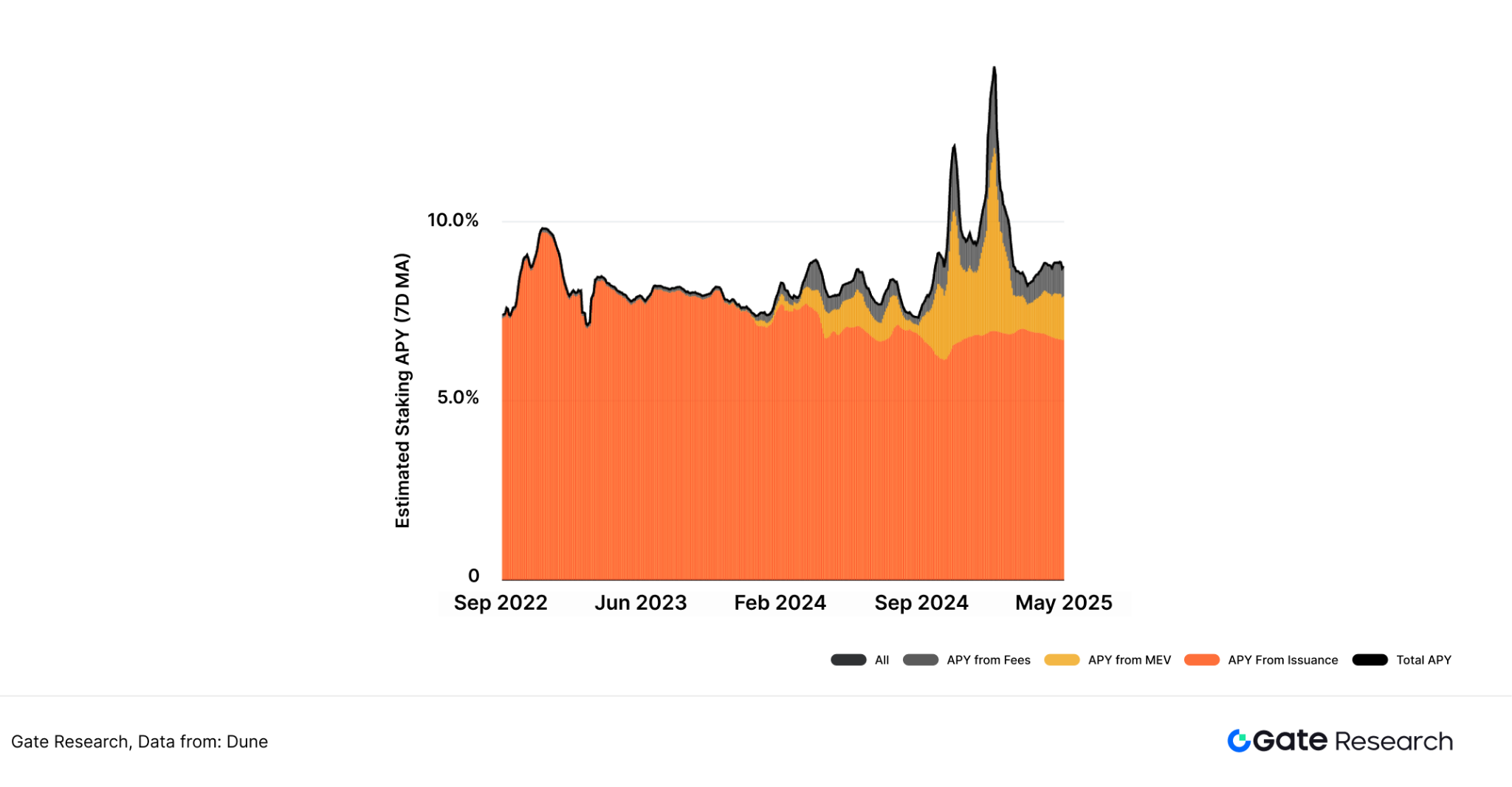

1.2 ETH staking yield vs. SOL staking yield

Compared with the staking yields of other public chains, the staking yield of ETH is actually not very competitive. Solana, as the main competitor of the Ethereum network, has a staking yield of 8.70% for SOL tokens in May 2025, which is 5% higher than the staking yield of ETH tokens. This also makes SOL holders more willing to stake. At present, the staking rate of SOL on the chain (total number of tokens staked/total number of tokens issued) is 67.97%, while the staking rate of ETH is only 28.56%.

Figure 3: SOL staking annualized rate of return

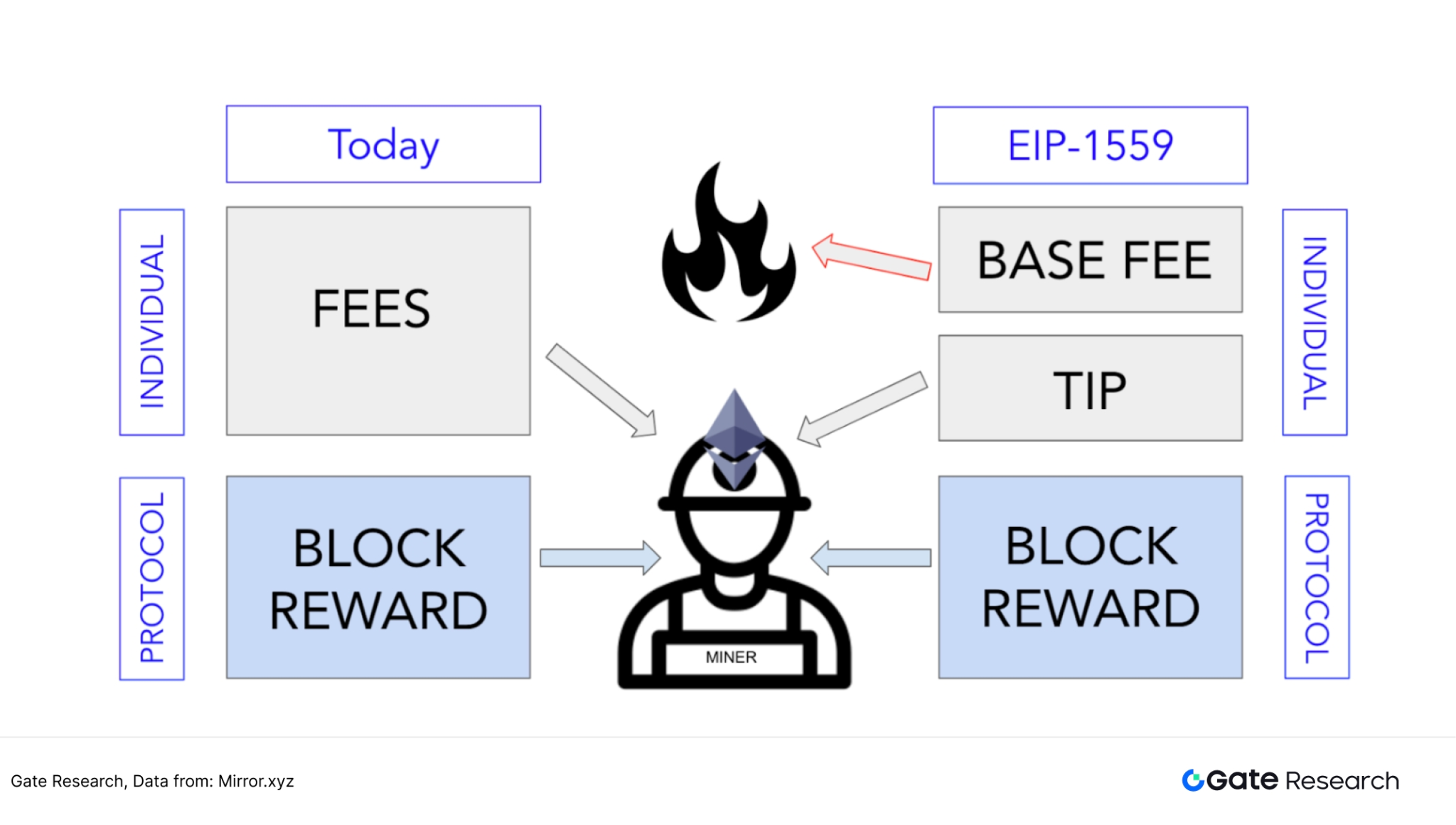

If we ask one more question, why does the yield of ETH staking continue to decline and lag far behind SOL? The author believes that the passage of EIP-1559 is a very important reason. The purpose of this proposal is to reduce the inflation rate of ETH, thereby further optimizing the economic model of Ethereum. Before the passage of EIP-1559, nodes had the basic fee + Tips fee of traders' on-chain transactions. After the passage of EIP-1599, nodes only receive the Tips fee paid by traders, and the basic Gas fee will be directly destroyed to ensure a stable deflation mechanism in the ETH economic model. Ethereum nodes and ETH stakers have lost an important income out of thin air. [3]

Figure 4: Changes in revenue for nodes before and after the EIP-1559 proposal was passed

In contrast, Solana's solution is a middle route, where 50% of the basic fee is burned, and the remaining 50% of the basic fee and Tips fee are rewarded to the node. SOL staking income has an additional 50% of the basic Gas fee share compared to ETH staking income. Solana's on-chain transaction Gas fee has been rising all year, and in the first quarter of 2025, it surpassed the Ethereum network for the first time, becoming the number one public chain Gas fee. Therefore, Solana nodes and token stakers also benefit from the increase in Gas fees. In terms of ensuring node income and token deflation mechanism, the core team of each public chain is looking for a balance point.

But in general, for traditional financial investors, staking SOL on the chain requires complex operations such as registering a Web3 wallet and selecting a public chain. Therefore, Ethereum ETF staking has increased investors' returns without increasing the operating threshold for investors, and is a milestone in the financial service progress in the process of Web2 moving towards Web3. Traditional financial investors can regard the staking service as providing an additional dividend of about 3% on the basis of token assets. [4]

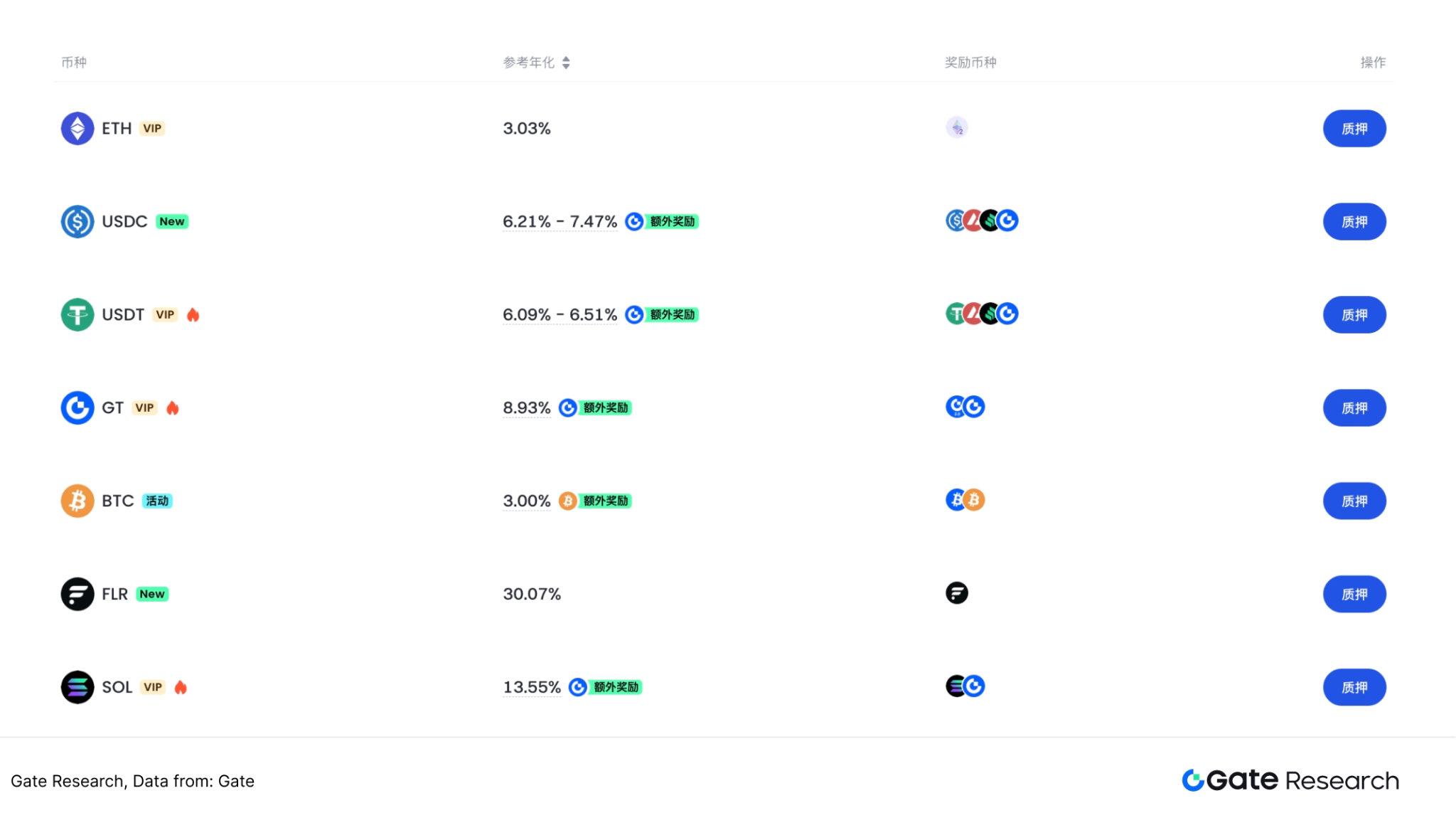

Figure 5: Gate Chain Coin Earning Page

As the world's next-generation super unicorn exchange, Gate Exchange provides investors with a convenient on-chain coin-earning service. In the on-chain coin-earning section, investors can earn excess returns without complicated on-chain operations. The ETH staking yield is 3.03%, and the SOL staking yield can be as high as 13.55%. [5]

2. Hong Kong Ethereum Spot ETF Pledge is a favorable policy for the long tail

Comparing the attitudes of cryptocurrency ETFs in Hong Kong and the United States, it can be seen that the United States launched the Bitcoin ETF earlier, and the Bitcoin ETF launched by the United States is the world's first cryptocurrency ETF fund, which has a demonstration effect. However, in terms of Ethereum ETF, the Hong Kong Securities Regulatory Commission is one step ahead and approved the establishment of the Ethereum ETF fund on April 15, 2024. The products of China Asset Management, Harvest Fund, and Bosera Fund were quickly launched on April 30.

The approval speed of Ethereum spot ETF in the United States is slower than that in Hong Kong. Four months after the Bitcoin ETF was approved, the US Securities and Exchange Commission approved the Ethereum ETF in May 2024, while the Ethereum ETF fund products of BlackRock and Fidelity were not officially launched until the end of July 2024. From the perspective of policy implementation and implementation, the Hong Kong Securities and Futures Commission has taken the lead in Ethereum ETF. However, as a global financial center, the United States still has an unparalleled advantage in liquidity. As of December 31, 2024, the management scale of BlackRock iShares Ethereum Trust ETF reached US$3.584 billion. [6]

In contrast, the scale of ETF funds under management in Hong Kong is relatively small. As of December 31, 2024, the scale of China Asset Management's Ethereum ETF was US$34.34 million [7], the scale of Bosera Fund's Ethereum ETF was US$19.55 million [8], and the scale of Harvest Fund's Ethereum ETF was US$9.57 million [9]. The total scale of the three is US$63.46 million, which is about 1% of the total scale of US Ethereum ETF funds.

Based on the logic of financial products, Hong Kong's Ethereum ETF can share gas fees through pledge services, which has obvious competitive advantages over the US Ethereum ETF. If a rational user holds BlackRock's Ethereum ETF, he should redeem it and subscribe to China Asset Management's or Bosera's Ethereum ETF to pursue higher returns.

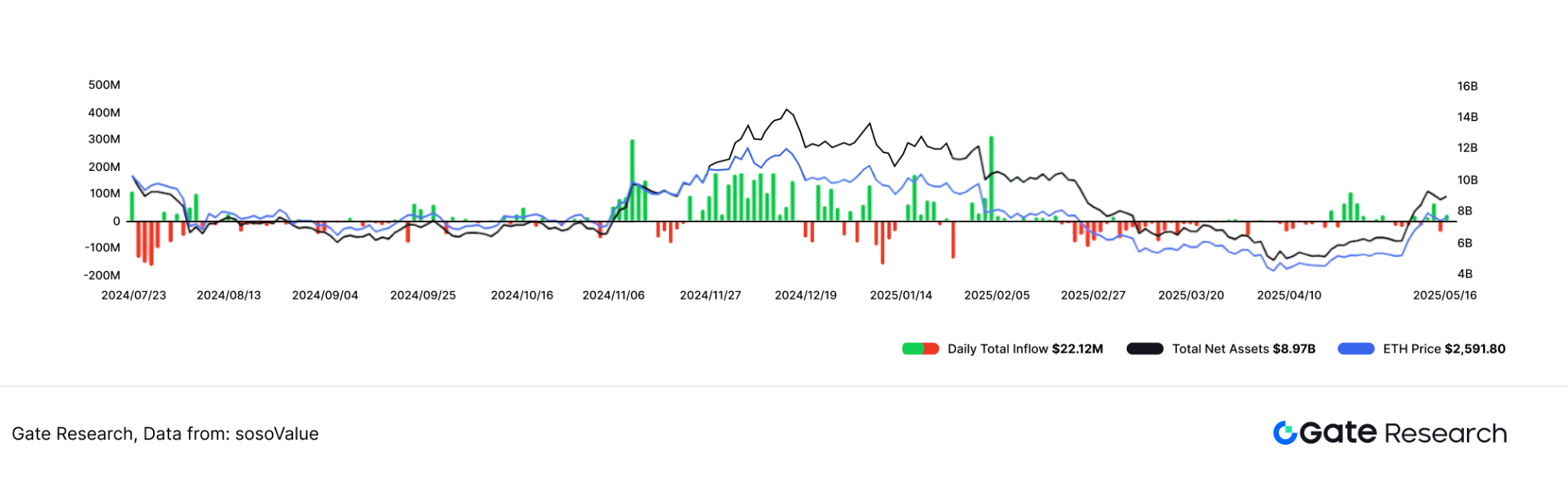

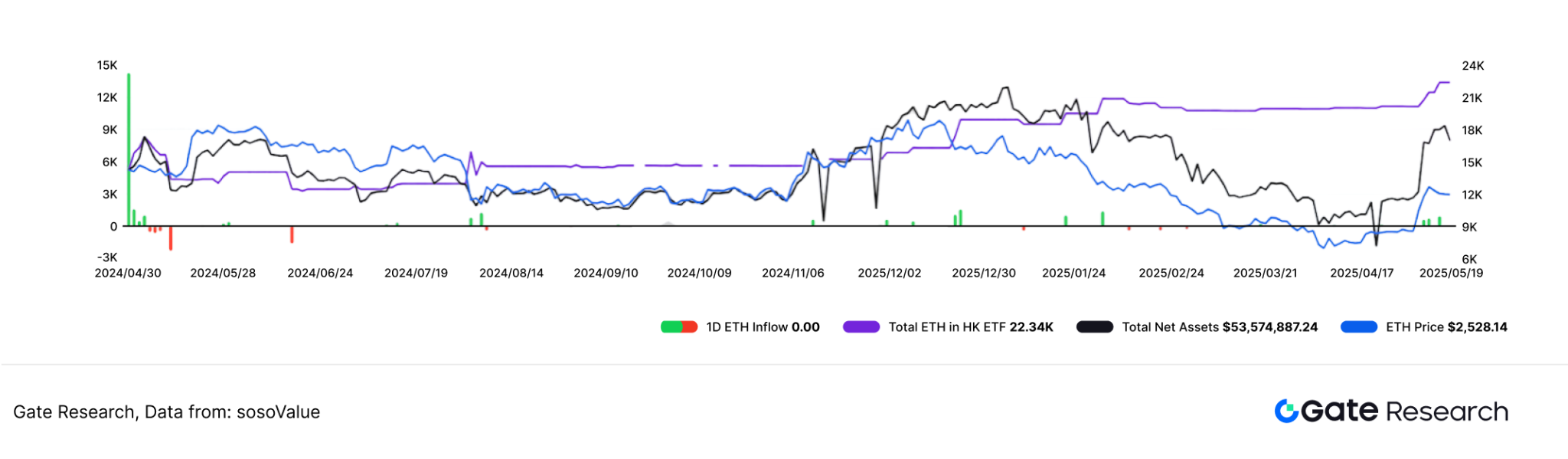

However, the facts are not as expected. After the launch of the pledge service in April 2025, the subscription of the Hong Kong Ethereum ETF Fund did not show a significant increase. In May, the price of ETH tokens rose from US$1,500 to US$2,500, and the Hong Kong Ethereum ETF Fund had a net inflow of US$610,000 and US$700,000 on May 12 and May 13, respectively. After the Hong Kong ETF Fund launched the pledge service, the US Ethereum ETF Fund did not experience a large outflow. On the contrary, it had a cumulative net inflow of US$230 million from April 24 to April 28, and the cumulative net inflow in April was greater than the net outflow.

Figure 6: Total size and net inflow of US Ethereum spot ETF

Figure 7: Hong Kong Ethereum Spot ETF Total Size and Net Inflow

This phenomenon can be explained from two perspectives. First, the liquidity of the Hong Kong market is not as abundant as that of the US market. Even if the pledge service is launched, there is not enough liquidity injection. Second, for holders of US Ethereum ETF funds, it is difficult to complete the registration of Hong Kong securities accounts in a short period of time. Finally, the main customers of ETFs are traditional financial investors, and there is still a threshold to understand the term "pledge". Although the current investor popularization has changed the impression of most investors on cryptocurrencies, traditional financial investors still need time to understand the deeper logic.

Hong Kong's approval of virtual asset ETFs to provide pledge services is a long-tail favorable policy, but it has failed to significantly increase the scale of management in the short term. This is mainly due to the lack of liquidity in the Hong Kong market, the difficulty of international investors to register, and the limited understanding of the concept of "pledge" by traditional investors. With the deepening of market education and the improvement of infrastructure, the long-tail effect of this policy is expected to gradually emerge in the future.

3. Hong Kong Ethereum Ecosystem Prospects and RWA Development

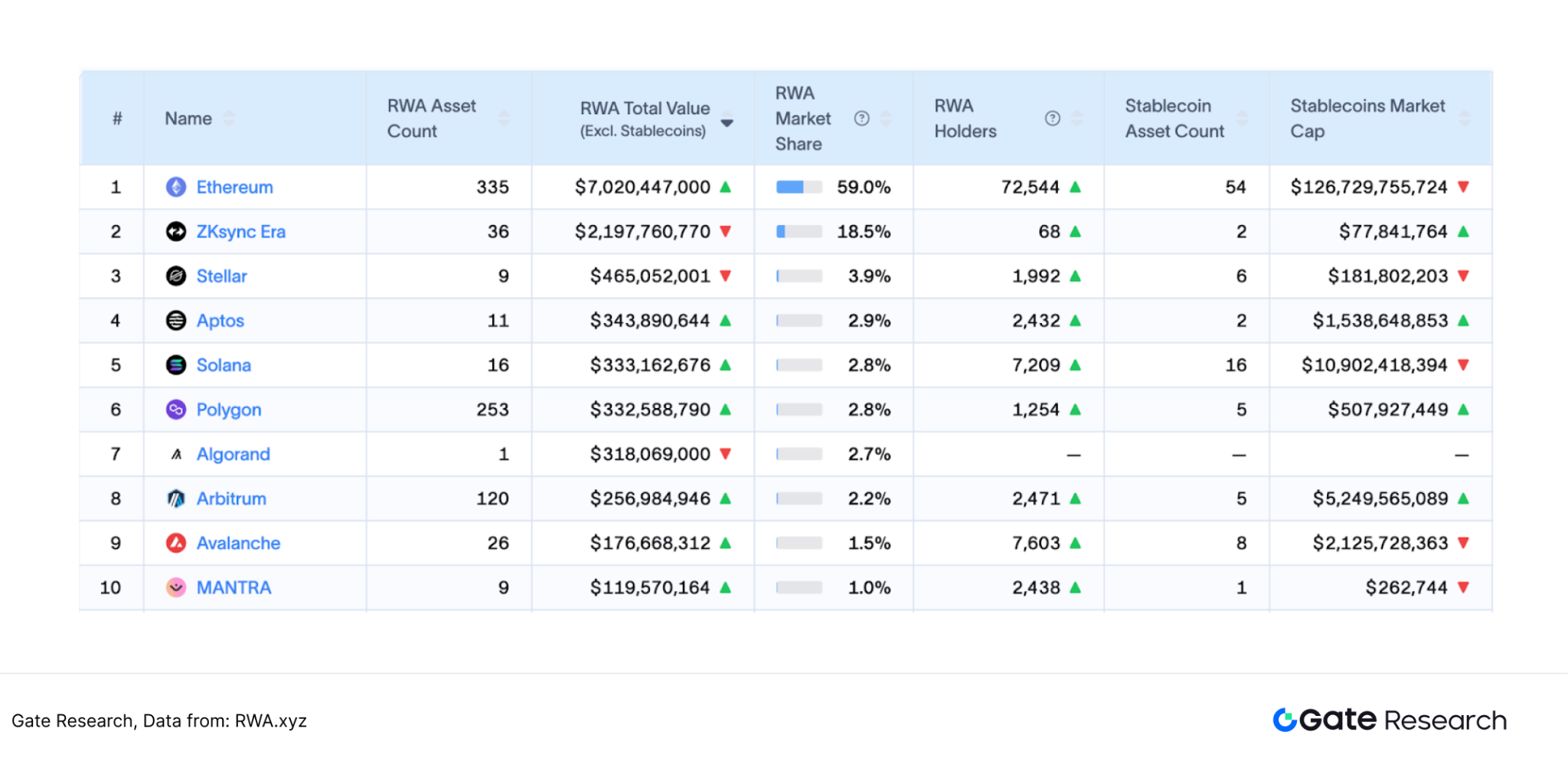

As mentioned above, Hong Kong is faster than the United States in landing Ethereum ETF spot ETFs, and SOL staking has better returns than ETH staking. Here readers may wonder why the Solana ETF fund is not passed as soon as possible and related staking services are provided? Here we need to discuss the relationship between cryptocurrency and traditional finance in a more macro way. The core reason for the approval of the Bitcoin ETF is that Bitcoin is the main value measurement currency among cryptocurrencies, and the consensus on Bitcoin standard has been deeply rooted in the hearts of the people. The approval of the Ethereum ETF is on the one hand because ETH has long occupied the second place in the cryptocurrency market value, and on the other hand, it is also because the Ethereum network is currently the public chain with the highest total value of RWA assets [10].

Figure 8: RWA total asset size ranking

RWA is the anchor point for cooperation between the traditional financial sector and the crypto world. In 2024, RWA gradually separated from DeFi and became an independent narrative. As the financial center of Asia, the Hong Kong Economic and Trade Authority officially launched the Ensemble Sandbox Project Group in August 2024 to promote tokenized applications. As of May 2025, the sandbox project has successively completed the RWA project of Langxin Technology Charging Pile, the RWA project of Xinxing Group Photovoltaic Power Station, and the RWA project of Patrol Eagle Group Two-wheeled Vehicle Battery Replacement. In addition, Ensemble team member China Asset Management (Hong Kong) Co., Ltd. launched the first retail tokenized fund in Asia Pacific in February 2025-China Hong Kong Dollar Digital Currency Fund. The underlying assets of the fund are short-term Hong Kong dollar deposits, and the tokens are issued on the Ethereum chain.

The policy support and the rapid implementation of the project demonstrate Hong Kong's high attention to the RWA field. As of May 2025, the total value of RWA assets on the Ethereum network chain exceeds US$7 billion, and the total value of stablecoin assets exceeds US$120 billion, both of which are the first in the public chain, and it is a huge asset pool. The implementation of Hong Kong's pledge service this time may have a bigger ambition. It may mean that Hong Kong will participate more in the governance and construction of the Ethereum network to develop RWA, a track that the policy focuses on.

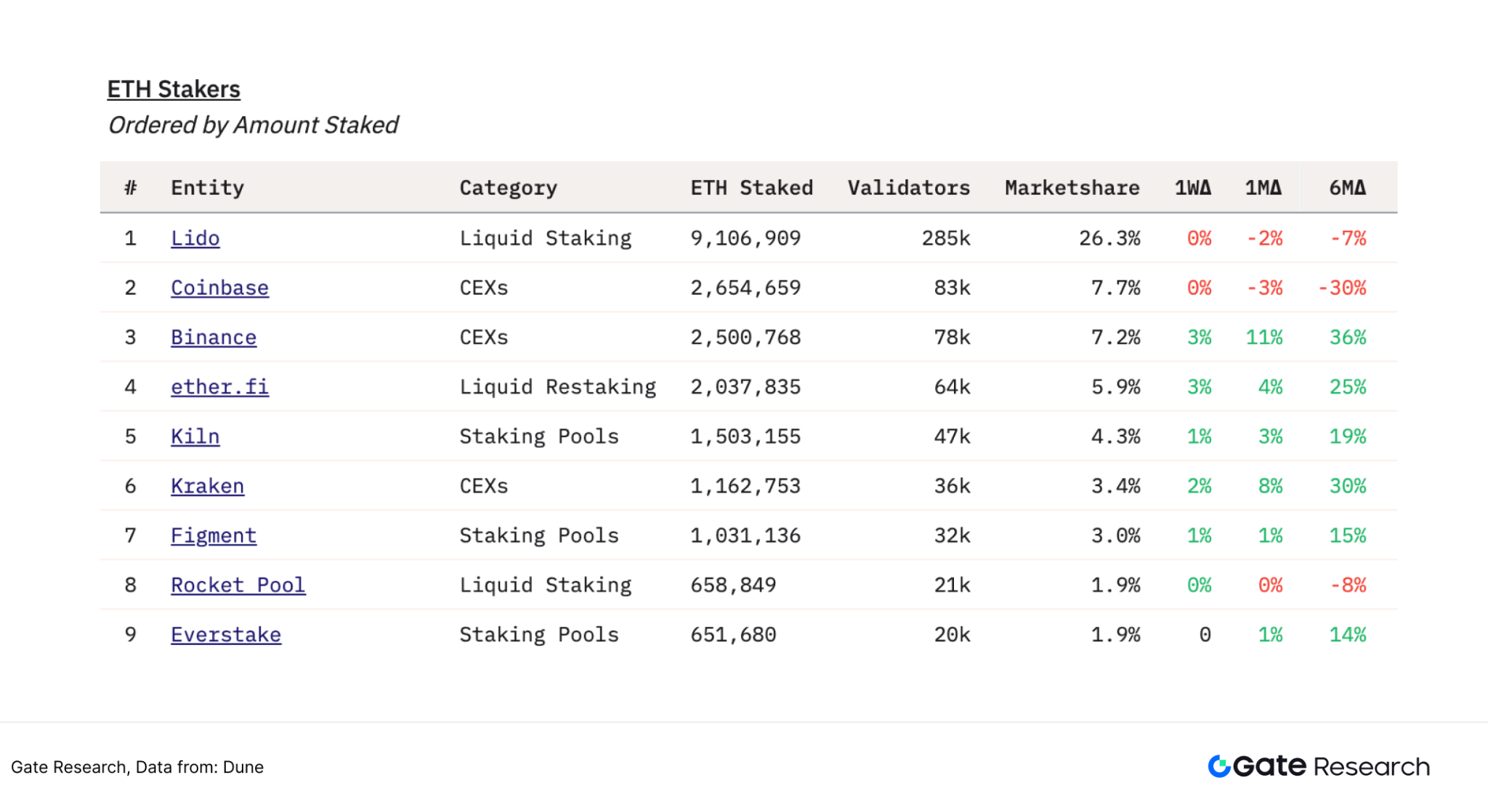

Figure 9: Ranking of total ETH pledged on the Ethereum network

ETH main nodes are regarded as important contributors to network security and have a greater say in the governance and development direction of the Ethereum ecosystem. For example, in the fourth quarter of 2024, DeSci became an emerging narrative in the industry, with its core promoters being Ethereum founder Vitalik, Coinbase founder Armstrong, and Binance founder CZ. Lido, which occupies 26.3% of the Ethereum staking market share, has a strong influence on the Ethereum community through its founder Lomashuk. It can be seen that staking services can not only increase user benefits, but also increase Hong Kong's voice in the Ethereum community, thereby further developing a compliant RWA ecosystem. [11][12].

4. Conclusion

Hong Kong's policy breakthroughs in the Ethereum ecosystem and its in-depth layout of the RWA track have laid an important foreshadowing for the next stage of development. By approving the Ethereum spot ETF pledge service, Hong Kong has not only strengthened its position as Asia's Web3 innovation hub, but also demonstrated strategic foresight in the RWA field. With the accumulation of over $7 billion in RWA assets and the advantages of stablecoin infrastructure, the Ethereum network has become the core bridge between traditional finance and the crypto world. With the implementation of physical asset tokenization projects such as charging piles and photovoltaic power stations promoted by the Ensemble sandbox of the Hong Kong Monetary Authority, and the issuance of on-chain funds anchored to Hong Kong dollar deposits by institutions such as China Asset Management, Hong Kong is attracting more RWA projects to take root with policy dividends and technical compatibility. In the future, with the improvement of Ethereum's governance voice and the optimization of the pledge income model, Hong Kong may become a key node for the issuance, trading and compliance of RWA assets in Asia, giving rise to more innovative practices in the real economy and blockchain technology.

Data Source

1. Dune Analytics

https://dune.com/21co/staking-dashboard

2. Dune Analytics

https://dune.com/queries/2502563/4117691

3. Mirror.xyz

https://mirror.xyz/looplove.eth/SOhMBCF_Z4vIWFHu4r8fpdBaLMhRTBCvNj6i5d4pNMU

4. Dune Analytics

https://dune.com/21co/staking-dashboard

5. Gate

6. Blackrock, https://www.blackrock.com/us/individual/products/337614/ishares-ethereum-trust-etf

7. China Asset Management

https://www.chinaamc.com.hk/wp-content/uploads/chinaamc/resources/Factsheet_3046_20241231_CHI.pdf

8. Bosera Fund

https://www.bosera.com.hk/api/infobase/downloadattfile.do?attachmentId=12647

9. Harvest Fund

https://www1.hkexnews.hk/listedco/listconews/sehk/2025/0430/2025043002910_e.pdf

10. RWA.XYZ

11.Dune Analytics

https://dune.com/hildobby/eth2-staking

12.99 Bitcoins