At the end of December 2025, the EU's Markets in Crypto-Assets (MiCA) regulatory framework will celebrate its first anniversary of full implementation. This year marks not only the implementation of regulations but also the first year that crypto-native institutions and traditional financial institutions will formally clash at the same table.

Timeline

The launch of MiCA was not achieved overnight, but rather through meticulous planning over several years. Over the past year, we have witnessed the entire process of CASPs (crypto asset service providers) going from "observation" to "taking the lead."

Regulatory Focus

MiCA's regulatory focus is no longer on abstract principles, but rather on setting quantifiable and testable hard thresholds for CASP's actual operation, asset protection, and market transparency.

Here are the five core focuses of the MiCA regulatory framework:

License and "passport" mechanism

Core principle: Replace fragmented national registrations with a single authorization. Once a CASP obtains authorization from its home country's NCA (National Competent Authority), it can provide "passport" services to all 27 EU countries.

Purpose: The authorization and passport notification will be published in the ESMA (European Securities and Markets Authority) public register for easy verification by banks and partners.

Institutional "Substance" and Governance Requirements

Key point: Regulators require CASPs to have a real decision-making body within the EU and at least one director permanently residing in the EU—preventing the establishment of "mailbox companies".

Requirements: The ESMA/EBA (European Securities and Markets Authority/European Banking Authority) guidelines emphasize that management bodies and qualified shareholders must clearly define their roles, time commitments, and capabilities.

Customer Funds and Asset Protection

Core principle: Hard, testable controls. Upon receiving fiat currency from a customer, CASP must deposit it with an EU credit institution or central bank before the end of the next business day, and must never use customer assets for its own accounts.

Responsibilities: Require isolation, daily reconciliation, clear custody contracts, and bear liability for losses caused by their own negligence.

Trading platforms and brokers: monitoring, transparency, and record keeping

Core principle: Strengthen market monitoring and information disclosure. Trading platforms must monitor market abuse and maintain complete order/traceable records.

Data requirements: Pre-trade and post-trade data must be published (near real-time; free after a 15-minute delay) and remain available for two years. Order book data must be retained for several years for regulatory agencies, and best execution principles must be standardized.

Token Issuance: White Paper and Retail Protection

Key point: For tokens other than ARTs/EMTs, the issuer must be a legal entity and must draft, notify, and publish a crypto asset white paper before public offering or access.

Investor protection: Retail buyers who purchase tokens before trading begins have a 14-day right to withdraw their investment. For tokens without a clearly identified issuer (such as BTC), platforms seeking access are responsible for disclosure and warnings.

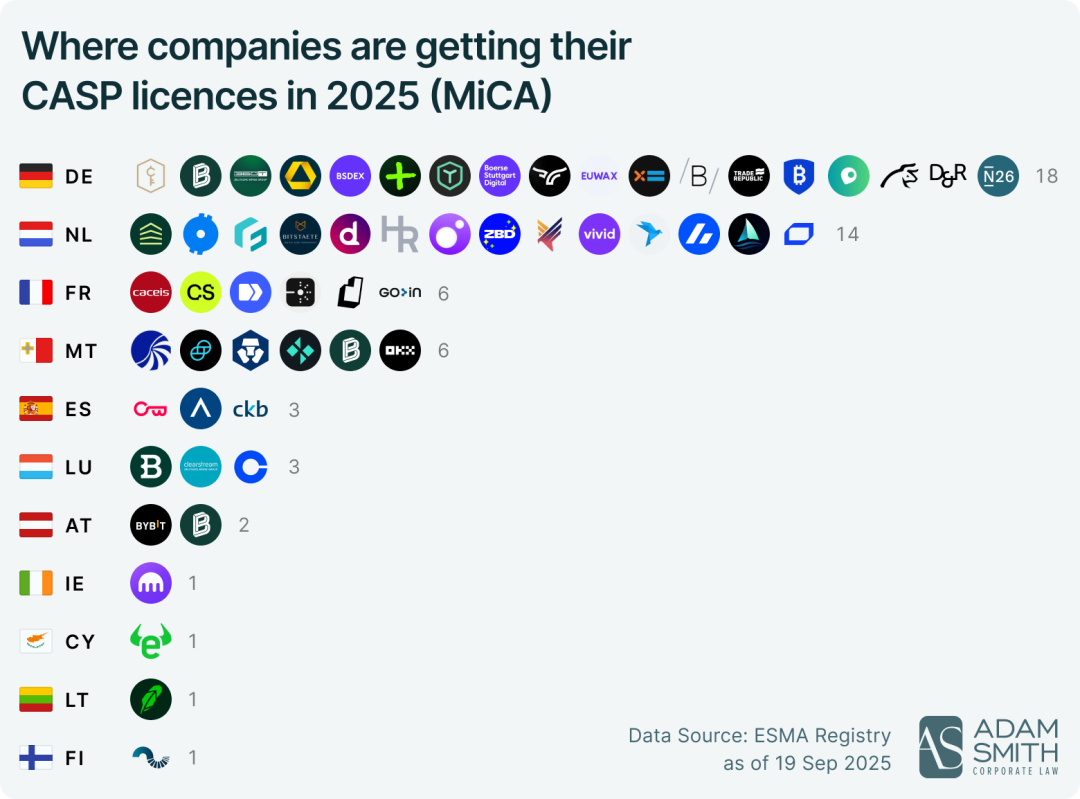

License Plate Panorama

MiCA's biggest advantage lies in its "passporting" mechanism. Previously, exchanges wanting to do business in Europe might have needed to apply for licenses in multiple countries, including Germany, France, and Italy. Now, obtaining a CASP license in just one EU member state allows them to operate legally in all 27 member states.

This has led to a fierce battle for "license plate dominance" over the past year. The current license plate landscape is as follows:

Total number of licenses issued: 57

Popular registration locations:

Germany: A Compliance Bastion for Banks and Custodians

It boasts the largest number of licenses and the highest value, making it a hub for the integration of traditional finance and crypto.

If an institution seeks a "bank-level compliance image" and wants to establish connections with deep capital markets, Germany is the preferred destination for such "regular" institutions.

Netherlands: The "artery" of payment and fiat currency channels

As the second largest market after Germany, it demonstrates a strong integration of Crypto native features with payment functionality.

The regulatory environment here is extremely well-suited to the brokerage model.

*The image and some of the above content are from Adam Smith.

Previously, fragmented regulations forced companies to scramble between countries, with compliance costs prohibitively high. Now, the "passport rights" granted by MiCA are no longer a privilege exclusive to giants, but a cornerstone benefiting every licensed institution. Whether it's a top centralized exchange or an innovative startup specializing in a niche market, obtaining a CASP license means opening a compliance highway to 27 EU member states, covering 450 million people. This is MiCA's most profound reshaping of the industry—it completely ends geographical arbitrage, making "compliance" the only passport to scalable expansion.

After reshaping

Looking back on the year MiCA came into full effect, the EU ended the "Westworld" era of the crypto market with "a set of rules".

For practitioners, the "arbitrage era" is over, and the "business expansion era" has arrived. Future competition will no longer be about who runs the fastest or who is the boldest, but about who has the best compliance costs and who can more smoothly enter the deep waters of traditional finance.

MiCA is just the beginning. With regulatory frameworks following suit in the UK, Singapore, and other regions, a global network of crypto compliance has essentially taken shape. For crypto, this may no longer be the chaotic world of outlaws, but it is a new continent poised to accommodate trillions of dollars due to established rules.