After the previous article on the covert battle in the wallet sector regarding the underlying infrastructure of Tee, many viewers have been urging for an update. So, let's have another round of action in 2025.

Hyperliquid is undoubtedly the hottest topic of the year. This time, let's take an inside look and connect the dots to see how wallets, exchanges, DEXs, and AI trading are all vying for dominance here!

1. Background

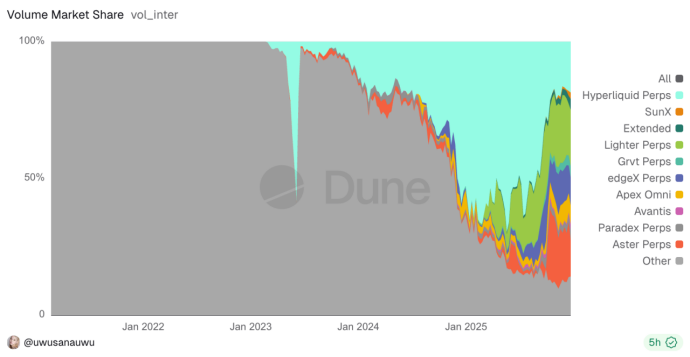

Over the past 25 years, I have basically researched all the perpetual trading platforms on the market, witnessing the five-fold growth and peak halving (9->50+->25) of the hypermarket. In the midst of these ups and downs, was it really overtaken by its competitors? Or was it due to concerns that the development of its HIP3 and builder fees reduced the platform's revenue?

The Perps field itself is also full of competitors. Recently, Aster, Lighter, and even Sun Perps have entered the fray, making the field shake up. Their Twitter space even set a new record for the number of online viewers at a Web3 industry conference.

The image below also shows the chaotic state of the market, and interestingly, it is also a rare process of dividing up an established market.

Recalling the competition among all DEXs during the DeFi Summer, including Uniswap, Balancer, Curve, and numerous Uniswap forks such as Pancakeswap, etc.

Perps at this moment is just like DeFi Summe at that moment. Some want to build platforms, some want to aggregate others, some want to become leaders, and some want to get a piece of the pie.

Throughout the year, various wallets have been vying to launch perpetual trading capabilities on DEX gateways. Metamask and Phantom were the first to do so, and last week Bitget also announced its integration. Other startups such as Axiom, BasedApp, XYZ (which operates on HIP3), and several AI trading platforms have also been trying to gain a share of the market by integrating with these platforms.

Thus, a new round of covert battles is underway in the wallet industry.

Everyone is vying to integrate Hyperliquid's perpetual trading capabilities. Is this driven by the benefits of open technology, the allure of rebates, or simply a reflection of genuine market demand? Why haven't some leading platforms taken action? Have the early adopters seized market share?

2. Ecological origins, builder fee and referral mechanism

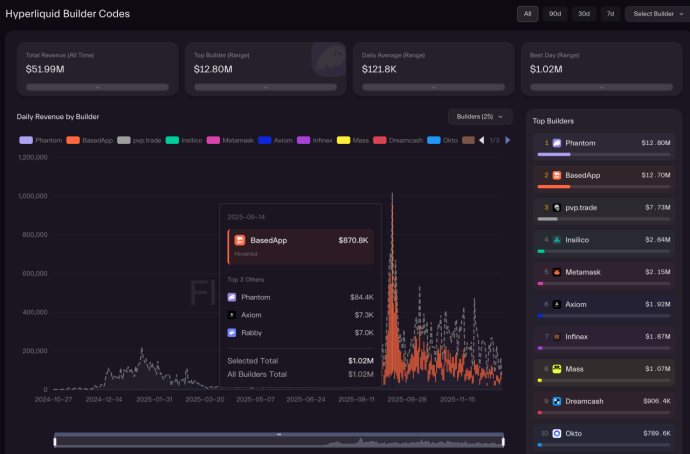

Hyperliquid's rebate mechanism mainly includes Builder Fee combined with Referral (rebate).

I've always believed this is a groundbreaking mechanism. It allows DeFi builders (developers, quantitative teams, aggregators) to charge an additional fee as service revenue when placing orders on behalf of users. The total transaction fee remains unchanged for users when placing orders on these platforms versus the official website.

In essence, it is similar to the hook mechanism of Uniswap V4. Both use their own order book (or liquidity pool) as infrastructure to provide access to various upstream platforms. In this way, it is easier to attract user groups from different platforms, and different wallet platforms also have more comprehensive ecosystem products to serve the different needs of their users.

This mechanism has already brought in over ten million US dollars in dividends for some projects since its initial launch, showing significant initial results, but its effectiveness has continued to decline since then.

From the diagram, we can also see many things that are worth pondering.

•Why is Metamask's user base no less than 5 times the revenue difference of Phantom access?

• Why is there such a large difference in revenue between based apps and axioms here? Where is Jupiter?

Is a dividend yield of 12M considered high or low? Is it short-term or long-term?

• Are platforms that only offer lightweight integration of HypeEVM or native cryptocurrencies at a disadvantage?

• Why are Bn, okx, etc. not included?

3. PerpDex's Opening Strategy

To answer these questions, we must first understand how various platforms are connected.

3.1 Open API Access Method

In fact, each PERPS provider has opened up its API, which is very comprehensive. Almost each provider has its own definition method, but the modules provided are roughly as follows: query class (account status, holdings, orders, market data, candlestick charts, etc.), trading class (order placement, cancellation, modification, leverage adjustment, withdrawal, etc.), and subscription class (WS real-time push of prices, order book, and changes in holdings).

This system itself requires these APIs to be provided to market makers for market making, while the user side only needs to change the direction of the transaction. However, the user side cannot be contacted like the market makers, so it is necessary to increase the degree of control.

Therefore, a rate limiting mechanism is necessary. Hype uses a dual rate limiting mechanism based on both address and IP address, which can dynamically adjust the rate limiting threshold according to transaction volume. However, it may face rate limiting challenges during high concurrency.

The advantages of this official API solution are rapid integration, no need to build your own nodes, low data latency, and good state consistency.

However, the disadvantages are also obvious: it may face IP/region restrictions and is easily affected by traffic limiting. Traffic limiting is less of a problem for a single user, but it is difficult for the platform to implement, since the number of users may increase at any time, and dynamic expansion is difficult to manage.

There's also the issue of updates. You have to know that there are restrictions on the release of apps when modifying code. If the official API is upgraded or changed, or if traffic is limited, the app developer has no control over it. In addition to becoming a traffic provider, they also have to bear the additional burden of customer complaints and risks.

3.2 Read-only Node Access Method

Hyperliquid has a dual-chain structure with EVM and core chains integrated into a single program and encapsulated in a closed-source environment. It is very difficult for external parties to crack and read the specific content. The official support is only for project teams to deploy such read-only nodes (which can obtain order, candlestick chart, and transaction data, but do not support sending transactions).

Moreover, not all historical data is made available. The amount of data here is enormous: more than 1TB of data can be added in just 2 days. If the historical data is not archived, the cost alone will hardly cover the revenue.

If the project team uses read-only nodes to reduce the frequency of reading the official API and thus reduce rate limiting issues, this is also the currently recommended approach.

Adopting this solution presents numerous technical challenges: intermittent block drops, massive storage requirements, and missing historical data. Furthermore, the data processing methods for nodes must be modified.

In my opinion, the biggest problem is the consistency issue brought about by this half-open mechanism.

For example, if I place an order using candlestick data from a read-only node, but the node itself is delayed (this is a matter of probability), but I can only place an order using the official API, which has no delay, this might indicate a data inconsistency. In this case, my market order could very well be executed at a price I don't want.

Whose responsibility is it? Does the platform earn enough to cover the compensation here? How much would it cost the platform to improve stability? Is it appropriate to simply shirk responsibility?

3.3 Market Selection

This is where the differences arise, with each side having its own approach.

• Metamask, as a typical example of a tool-oriented platform, directly adopts the approach of integrating open APIs through the front end, and even directly open-sources the integration code. This simple and straightforward approach brings rapid deployment efficiency. It is rare to see such a conservative leading wallet platform making such rapid market moves.

• Rabby, Axiom, and BasedApp also use this approach.

• Trust Wallet also integrates with Perps, but it connects to the BN-affiliated Aster platform, clearly indicating that it's being given the green light by its own product. However, how the commission is distributed internally is uncertain.

• Phantom originated from the meme wave on Solana, and here it emphasizes the pursuit of user experience, employing...

It uses a read-only node access method, and even the order placement process has to be relayed through the backend, rather than the client directly contacting the official API to place an order.

Actually, there are some amazing products on the market, and different perspectives to consider.

For example, Trade.xyz is currently the platform with the highest trading volume on Hip3. Instead of pursuing fierce competition in the existing market, it directly develops the ability to trade stocks.

VOOI Light is also quite capable (in terms of engineering). It's an intent-based cross-chain perpetual DEX, and its core strength lies in simultaneously integrating multiple perps DEXs. Essentially, it uses engineering effort to simultaneously implement multiple paths across various platforms. However, its drawback is the complexity of managing reserves across multiple integrations, resulting in a less smooth user experience.

Finally, I recently tested several AI trading platforms, almost all of which use open API access and backend integration with multiple perps. The experience was very cutting-edge; some used pure LLM large-scale model text interaction, while others used AI decision-making combined with following traders (the underlying layer can also link to tee hosting solutions like Privy), enabling AI-assisted perps trading without transmitting private keys to the project team.

Different options lead to different experiences, which can somewhat explain the differences in the final commission rebate data.

4. Reflection

The social login mentioned earlier can only solve the recovery problem, but it cannot solve the problem of automated trading.

4.1 Complexity of Reserves

This is actually the easiest part to overlook. Hyperliquid is far more complex than you might imagine; it's not a simple "plug and play" solution.

Various platforms initially viewed it optimistically as an integration of DEX aggregation, but they overlooked the fact that it's not a Lego model in essence. If it integrates with Hyperliquid, what happens when the market declines? Will that functionality still be retained? How many wallets are now discontinuing their former inscription protocols? And will users who uninstalled the platform have to go back to the official platform to find their accounts?

Furthermore, if Hyperliquid becomes less popular, and Aster or Lighter become popular, should we migrate to the new platform? The APIs of different platforms are not entirely consistent; how can we migrate and operate in parallel?

To smooth out these issues, it's inevitable to increase the complexity of the experience.

Ultimately, if users want a comprehensive entry point, why not use the official one?

Front-end integration brings a fast experience and coverage, but Metamask seems to have suffered a silent loss, not making much money, but providing its own user traffic for free.

The superior user experience brought by backend integration is currently the core reason why Phantom earns the most revenue, but it also brings huge costs. Ultimately, only they themselves may know the true ROI (return on investment).

4.2 Why can't the total return exceed its previous level?

Looking back at our own preferences (especially as advanced Perps users) regarding platforms like Hyperliquid, we still prefer the official, complete interface and operate primarily on PC. This is mainly because it offers more direct access to advanced features like stop-loss/take-profit settings, chart monitoring, and margin trading. After all, this market is dominated by high-end players.

The purpose of using mobile devices is to "monitor and respond to market changes anytime, anywhere, and manage position risk and prices, rather than to perform complex analysis."

Therefore, Phantom's advantage continues to decline after providing new users with an initial experience, because its focus is still on mobile devices.

BasedApps, which have both an app and a web entry point, cater to the needs of both. However, due to competition from the official web entry point, their potential is limited.

However, Hyperliquid's own app will be launched soon, so the market itself will become increasingly limited.

It can only be said that architectural differences determine the value of access, but the magnitude of the value depends on the depth of access. Ultimately, the ceiling of this model is still competition within the industry, and it is difficult for users contributed by the entry platform to remain on the original platform.

If a wallet can offer advanced mobile features (advanced charting, alerts and notification systems, auto trading), then it certainly has a differentiating value. We can see that Phantom updates quickly and introduced various advanced features, precisely to retain these users.

The solution lies in AI trading, auto trading (a trading model not officially recognized), and multi-perps aggregation—all approaches that DEXs have followed. However, issues remain, such as the difficulty in managing reserves across multiple platforms and the high rate of AI losses. Even with industry-standard private key escrow methods (PRvy, TurnKey), these solutions are still largely unavailable; those who know how will naturally learn, and those who don't can't be taught.

4.3 User Growth and Niche Complementation

Of course, many platforms are willing to accept not making money, since relying on commission sharing is already a pittance. However, if they can attract users who use Perps or meet the perpetual trading needs of existing users, it would be a good addition to their ecosystem.

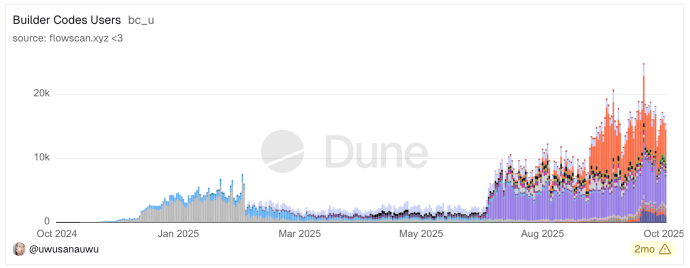

We can draw this conclusion by analyzing some HL data from the blockchain, because this group is actually very small.

As shown in the chart below, each provider's integration only translates to a few thousand daily active users, totaling less than 10,000 to 20,000.

Furthermore, considering Hyperliquid's monthly active users, its revenue is essentially based on a whale service model, which is a typical example of the Matthew effect and inverted pyramid funding structure in the contract trading market.

Currently, HL has around 1.1 million total wallet addresses, with 217,000 monthly active users and 50,000 daily active users. But the key is here – the top 5% of users contribute over 90% of the OI and Volume, forming a typical pyramid structure.

The top 0.23% of users (with funds ranging from $1M+, totaling over 500 people) control 70% of open contracts ($5.4B), with the top 100 users holding an average position of $33M each, and their open interest (OI) is 920 times that of the average user.

In contrast, the bottom-tier users (150,000 users), who make up 72.77%, contribute only 0.2% of the contract volume, with an average holding of only $75 per person.

This structure illustrates that the contract market is essentially a game between professional institutions and high-net-worth individuals. Although a large number of retail investors constitute the user base and activity level, their capital volume is almost negligible.

This structure actually reflects a very counterintuitive idea: that Hyperliquid itself is indeed very profitable, jumping into one of the most profitable exchanges in just one year.

However, his profits essentially come from high-end whales, whose motives may be to resist censorship, seek openness and transparency, or be driven by quantitative trading.

However, the significance of integration by various platforms is actually limited to bringing in regular users. Therefore, a long-term user education process is needed to potentially convert those already working on Perps within CEXs to the increasingly competitive Web3Perps platform.

5. In conclusion, is integrating Perps really a good business?

Most projects need to adapt to the market, but when a platform reaches its peak popularity, the market can adapt to it. HyperLiquid is currently receiving this treatment, but it may not be able to maintain it. Although it can be explained that the surge in trading volume of other competitors in the market is due to expectations of new airdrops, resulting in non-genuine trading outcomes.

Moreover, many of HL's measures are relatively correct. Compared to many other platforms in the past, which often thought they could do everything themselves and reap all the benefits, I would specifically criticize OpenSea for creating a mandatory royalty system that forces the market to follow the leader. Each instance incurs fixed high costs, interferes with the flow of goods, affects the true market pricing, and ultimately turns countless NFTs into heirlooms.

In HL, he opened up EVM and all the various DEX and PEPS APIs, so soon a bunch of derivatives appeared on the market.

RWA assets, particularly US stocks and gold, are becoming new traffic entry points and differentiated growth points in the current Perp DEX field. TradeXYZ's cumulative Perp volume of $19.1 billion, averaging $320 million per week and $45.7 million per day, is the best proof of this.

Hyperliquid's generosity is evident in its airdrops and buybacks; often, staking HYPE for ADL can yield substantial profits.

After all the twists and turns, the battle for market leadership is a problem for the few platforms to worry about. Returning to the covert war of wallet integration this year, integrating third-party Perps is mostly a low-ROI business. Whether in terms of user growth revenue, platform commission earnings, or stability investment, it is not a good business.

It's conceivable that after seeing the real benefits after integration, many platforms will still be reluctant to give up the Perps sector's advantages and will move towards self-developed technology and massive user acquisition and promotion. The battle for this sector is not over and will continue for another year. However, only new users acquired from non-Cex sectors will be truly effective users.

Disclaimer

This article is very information-dense because many architectural overviews are highly condensed, and the technologies are not fully open source, but rather based on analysis of published information.

Furthermore, this discussion is purely from a technical solution perspective and does not imply any positive or negative evaluation of the products from any company.