Author: Gate Research Institute

summary

•Stablecoins are divided into three types based on their price anchoring method: fiat-collateralized stablecoins, cryptocurrency-collateralized stablecoins, and algorithmic stablecoins.

•Currently, the global stablecoin market value has reached US$260.728 billion, accounting for approximately 1% of the US nominal GDP in 2024. The number of stablecoin holders has exceeded 170 million, accounting for approximately 2% of the world's total population, and is widely distributed in more than 80 countries and regions.

Governments around the world are increasingly prioritizing stablecoin regulation, with core legislative drivers encompassing financial stability, monetary sovereignty, and cross-border capital oversight. Economies such as the United States and Hong Kong have already introduced systemic regulations, ushering in an era of strong regulation for global stablecoins and reshaping the international financial order and monetary power landscape.

Behind the rise of stablecoins lies a hidden competition between monetary sovereignty and financial hegemony. As a strategic core resource at the intersection of financial sovereignty, financial infrastructure, and capital market pricing power, stablecoins have become a focal point of financial governance.

•Although stablecoins improve financial efficiency, they still face challenges such as anchoring mechanism risks, decentralization conflicts and cross-border regulatory coordination.

introduction

On July 18, 2025, the U.S. House of Representatives passed the GENIUS Act with 308 votes in favor and 122 votes against. The CLARITY Act, which regulates the structure of the encryption market, has been submitted to the Senate, and another bill opposing CBDC (central bank digital currency) passed the House vote.

Beyond the United States, countries around the world are rolling out stablecoin policies: Hong Kong will implement its Stablecoin Ordinance on August 1st, Russian banks are offering crypto custody services, and Thailand has launched a cryptocurrency sandbox. These developments signal the entry of stablecoins into the regulatory era, and the great power competition over stablecoins has officially begun.

Given that stablecoin legislation has become a focal point in financial governance, this article aims to analyze the reasons behind stablecoin legislation by various governments, compare the similarities and differences in bills, and analyze the impact of stablecoin compliance on the existing financial order, providing insights for industry builders and investors. Investors are advised to closely monitor regulatory trends, prioritize participation in fiat-collateralized stablecoins, and mitigate the compliance risks of algorithmic stablecoins. Traditional financial institutions should embrace the trend of asset tokenization and explore new opportunities, while crypto institutions should continuously advance their compliance efforts.

1.1 Definition and Classification of Stablecoins

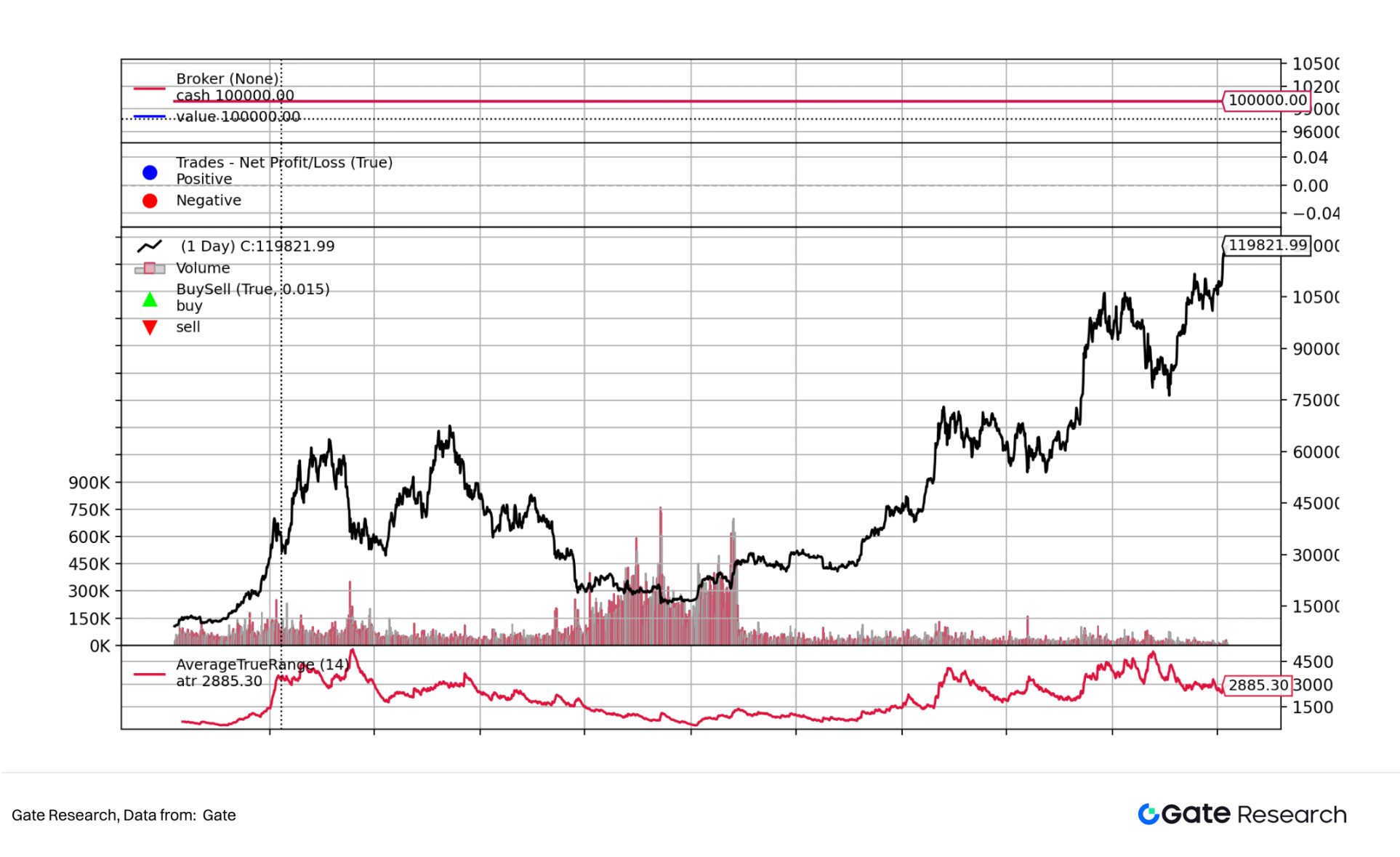

The figure below shows the BTC price curve and 14-day ATR curve. It can be seen that the price volatility of traditional cryptocurrencies, mainly BTC, is too high, which is not conducive to the promotion and application of cryptocurrencies. Stablecoins were first applied in 2014. Stablecoins are cryptocurrencies designed to maintain price stability.

Stablecoins are typically pegged to assets such as fiat currencies, commodities, and other cryptocurrencies, or leverage algorithmic regulation mechanisms to maintain their value. They are widely used in the financial sector as a core medium for digital asset trading, DeFi applications, and cross-border payments.

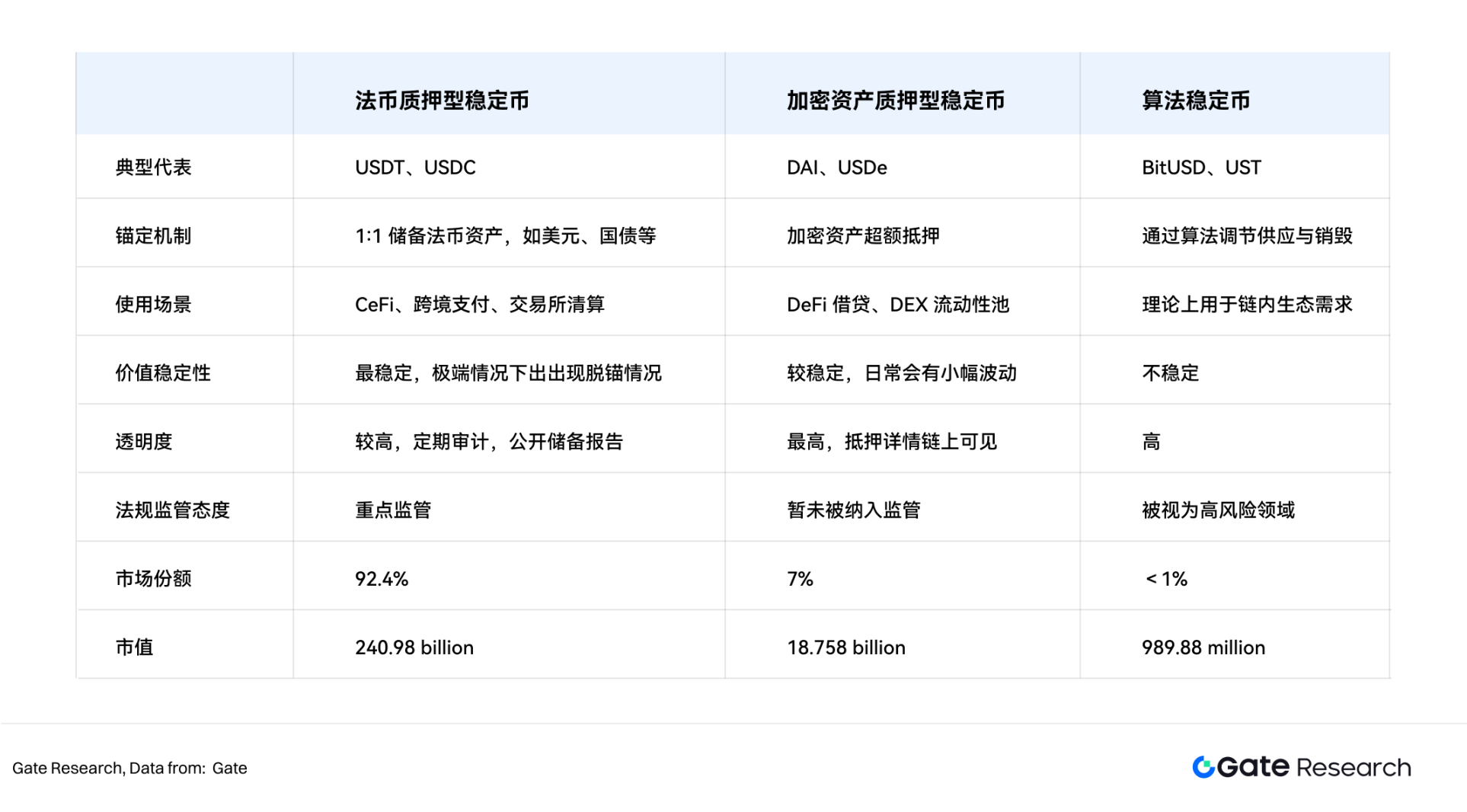

Stablecoins can be divided into three types based on the price at which they maintain their value:

•Fiat-collateralized stablecoins

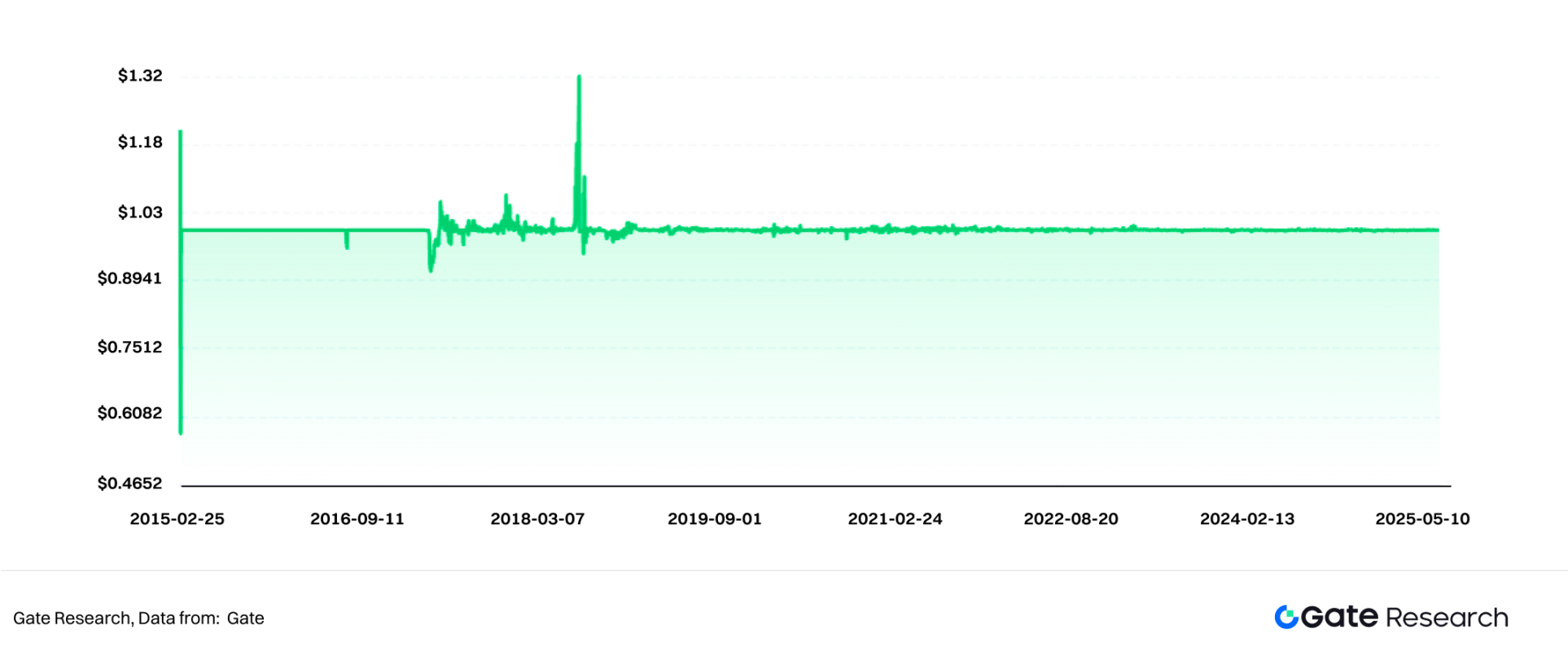

Fiat-collateralized stablecoins are the most common stablecoins, accounting for 92.4% of the market share. They achieve price stability by pegging tokens to fiat currencies such as the US dollar. The issuing institution pledges fiat currency or highly liquid assets (such as government bonds) in a bank or custodial account, then mints and issues tokens at a 1:1 ratio. Examples include USDT and USDC. The figure below shows the USDT price curve.

•Crypto-collateralized stablecoins

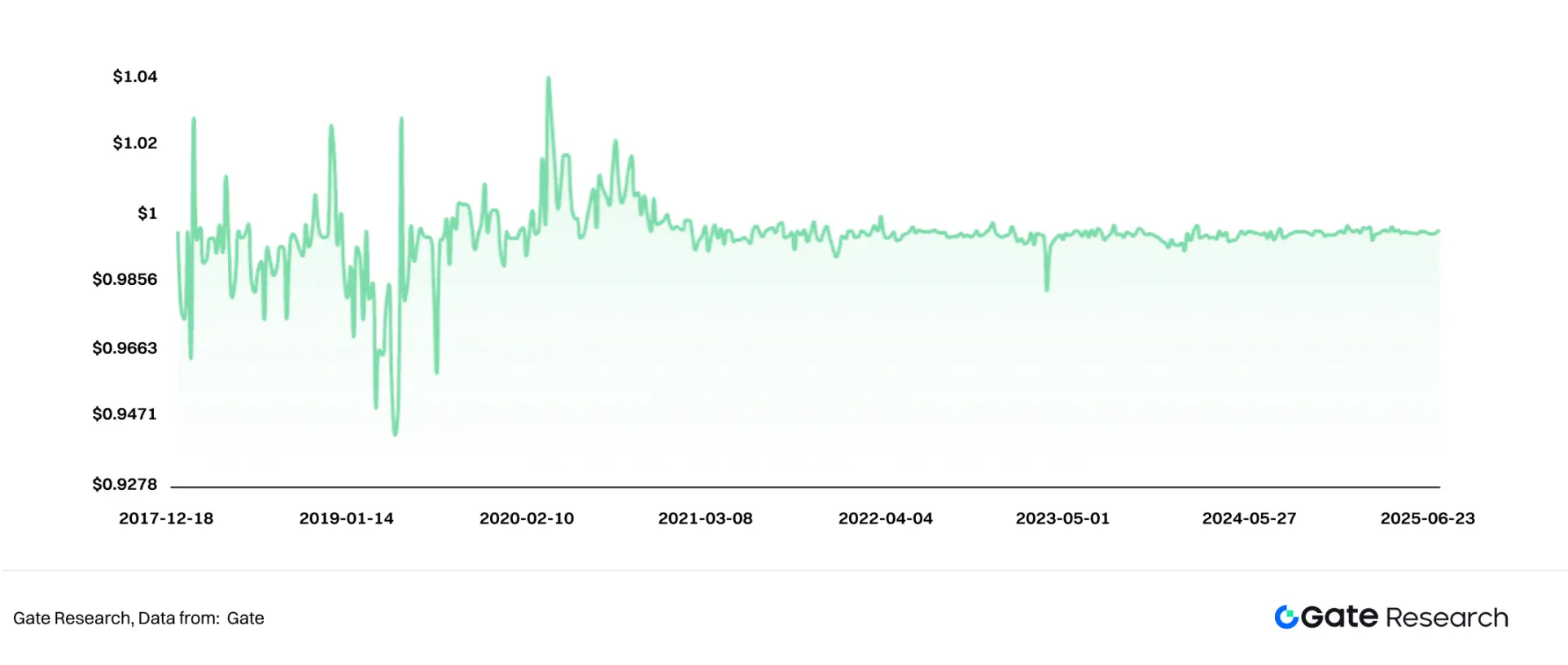

Unlike fiat-collateralized stablecoins, crypto-collateralized stablecoins are collateralized with cryptocurrencies. Due to the high volatility of cryptocurrencies, they often employ over-collateralization (typically around 150%) and incorporate on-chain liquidation mechanisms to maintain the value of the stablecoin. For example, in the case of DAI issued by MakerDAO (Sky), users over-collateralize ETH to mint DAI tokens. The chart below shows the DAI price curve.

•Algorithmic stablecoins

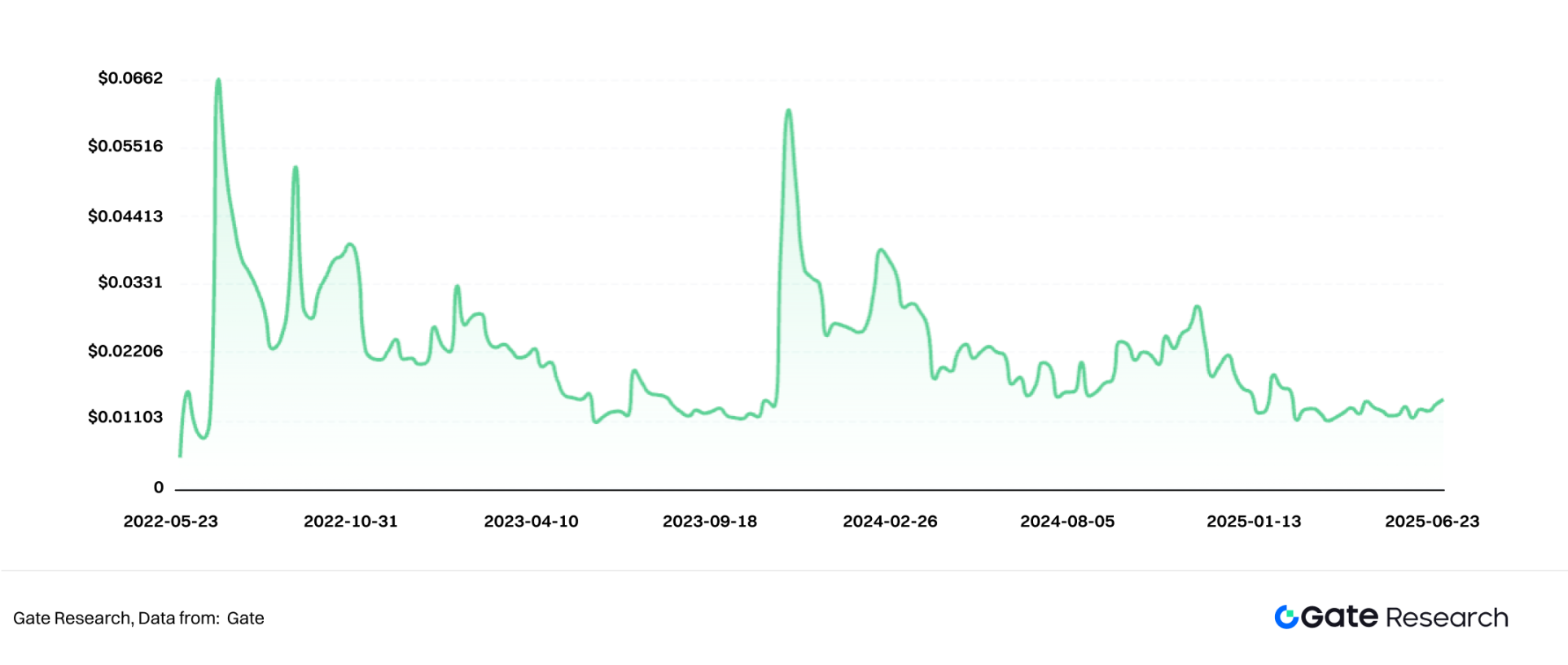

These stablecoins aren't backed by physical assets, but instead rely on algorithms and market supply and demand to maintain their price. When the token price is above $1, the system issues additional tokens, lowering the price. When the price falls below $1, the system buys back and burns tokens, raising the price. For example, UST (which has since collapsed) became an independent cryptocurrency in 2025, no longer pegged to the US dollar. The chart below shows the USTC price curve.

Comparison of three types of stablecoins

1.2 Characteristics of Stablecoins

Stablecoins' unique value anchoring mechanism distinguishes them from the volatile fluctuations of traditional cryptocurrencies, and are therefore widely regarded as "digital cash" or "bridge assets" in the crypto asset ecosystem. They have the following main characteristics:

• Price stability

By being linked to stable assets such as the US dollar and gold, or adopting over-collateralization mechanisms and algorithmic adjustment mechanisms, stablecoins achieve lower price volatility and have stronger store of value and transaction medium attributes.

• Bridging traditional finance and decentralized finance (DeFi)

Stablecoins use traditional finance as underlying assets, are issued on the blockchain, and can interact with on-chain protocols and tools, especially playing an important role in core applications such as DeFi lending, liquidity mining, and derivatives trading.

•Lower payment costs and higher efficiency

Relying on blockchain technology, stablecoins can achieve near-real-time cross-border transfers with fees far lower than traditional banking systems, without geographical or time restrictions, significantly improving the efficiency of capital circulation.

• Anti-inflation and capital risk aversion

Most stablecoins are pegged to US dollar assets, meaning they are subject to the same inflation as the US dollar. In countries with severe inflation or currency devaluation (such as Argentina and Turkey), stablecoins have become a key means of hedging and preserving assets due to their stability. In parts of Africa and Latin America, stablecoins have become a means of daily payment.

1.3 Main Application Scenarios

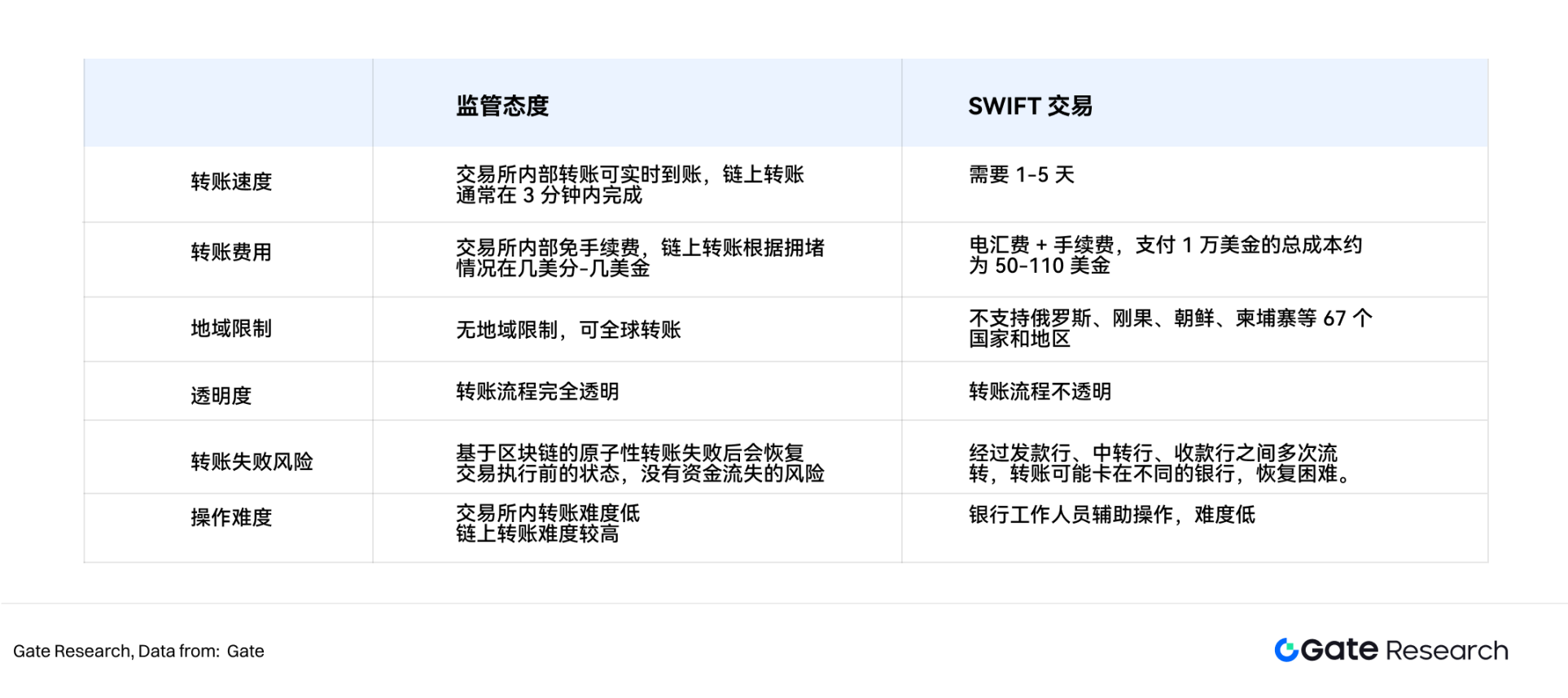

Based on the aforementioned characteristics, stablecoins are currently being used in a variety of scenarios, including decentralized finance, cryptocurrency trading, cross-border trade, daily payments, and capital hedging. Cross-border trade is a key area of focus in the recent US and Hong Kong legislation. Transactions using stablecoins not only effectively mitigate the currency inflation issues of individual countries, but also offer significantly higher payment costs and efficiency than the traditional SWIFT system.

Legislative background

2.1 The rise of stablecoins

Currently, the global stablecoin market capitalization has reached $260.728 billion, exceeding MasterCard's market capitalization and accounting for approximately 1% of the US nominal GDP in 2024. Stablecoins are a vital component of the international financial system. The global penetration of stablecoins continues to climb. As of now, stablecoin holders exceed 170 million, representing approximately 2% of the world's population, and are widely distributed in over 80 countries and regions.

2.2 Motivations for government intervention and regulation

Governments around the world are actively involved in the regulation of stablecoins. The motivation behind this is not only to prevent financial risks, but also to protect the core interests of monetary sovereignty, financial security, and cross-border capital control, as well as to alleviate the credit risks of fiat currencies.

•Prevent systemic financial risks: Avoid the loss of control of stablecoins and the resulting turmoil in the payment system and capital markets, and prevent risk spillovers similar to the 2008 shadow banking crisis.

•Maintain monetary sovereignty and financial order: Prevent private stablecoins from replacing legal tender in domestic circulation and weaken the central bank’s control over monetary policy and payment system.

•Combating illegal cross-border capital flows: Stablecoins can bypass regulatory systems such as SWIFT, and the government is concerned about their potential abuse in areas such as money laundering, tax evasion, and sanctions circumvention.

• Hedging against the impact of “US dollar stablecoin hegemony”: The United States promotes USDT/USDC and other currencies to become “on-chain dollars”, and other countries explore countermeasures through legislation to explore their own stablecoins (Hong Kong dollars, euros, and RMB).

• Alleviate fiat currency credit risk and support government bonds: By 2025, the market capitalization of US dollar stablecoins will exceed $260 billion, with US Treasury bonds generally accounting for more than 60%-80% of reserve assets. Stablecoin reserve demand has become a significant buyer of US Treasury bonds, providing continued support for the creditworthiness of the US dollar.

In order to strengthen the international status of their own currencies, protect the safety of consumer assets, seize the right to speak in the field of digital assets, and solve the problem of lack of supervision of stablecoins, the United States, Hong Kong, Europe and other countries have successively introduced systematic regulatory laws and regulations. The stablecoin industry has officially entered the era of strong supervision and compliance.

Progress in Stablecoin Regulation in Major Global Economies

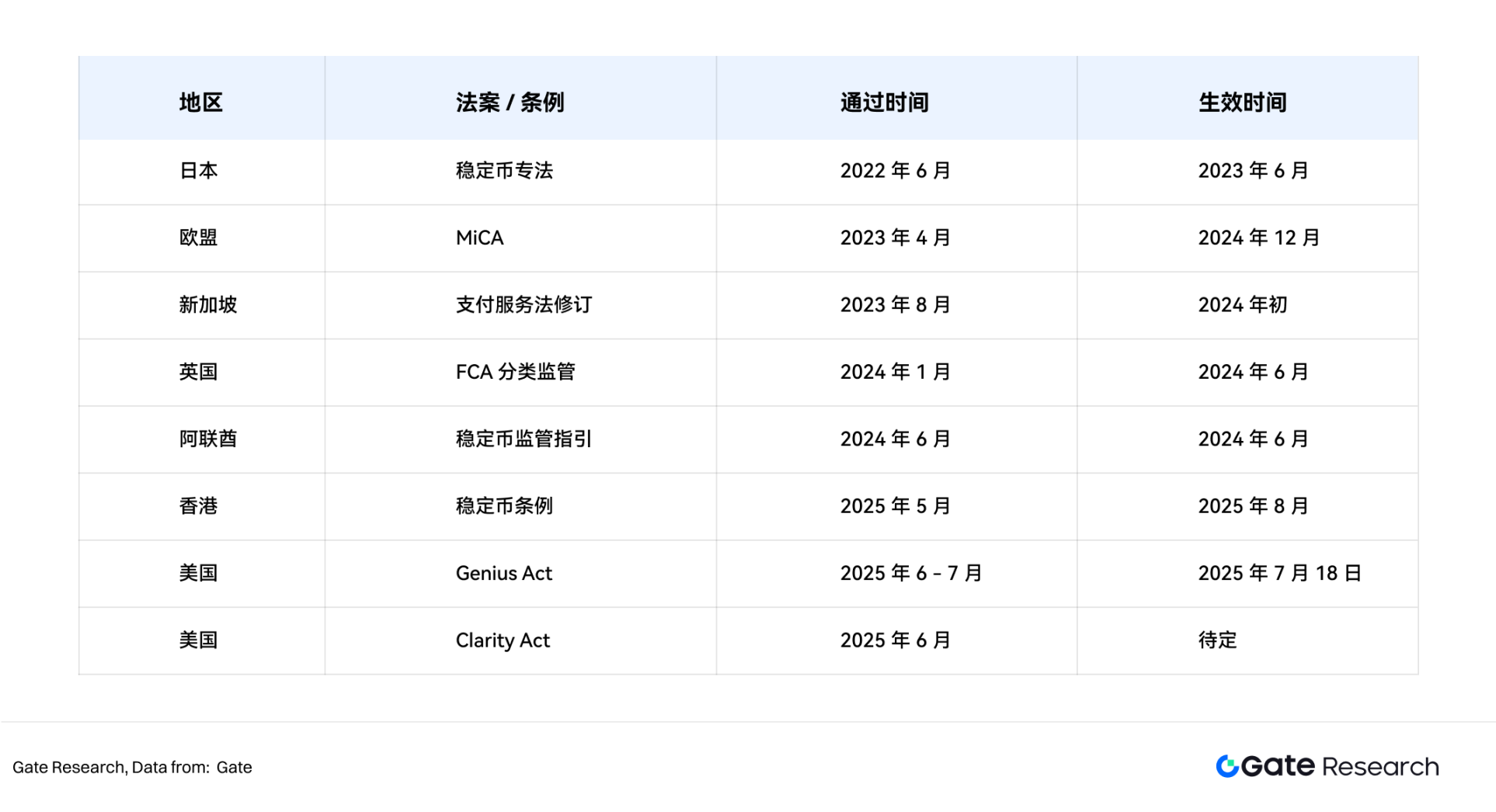

Since 2022, with the expansion of stablecoins in the global market, various countries have issued relevant regulations to regulate them. The following figure shows the timeline of the progress of stablecoin regulation in various countries:

3.1 The United States introduces the Genius Act and the Clarity Act

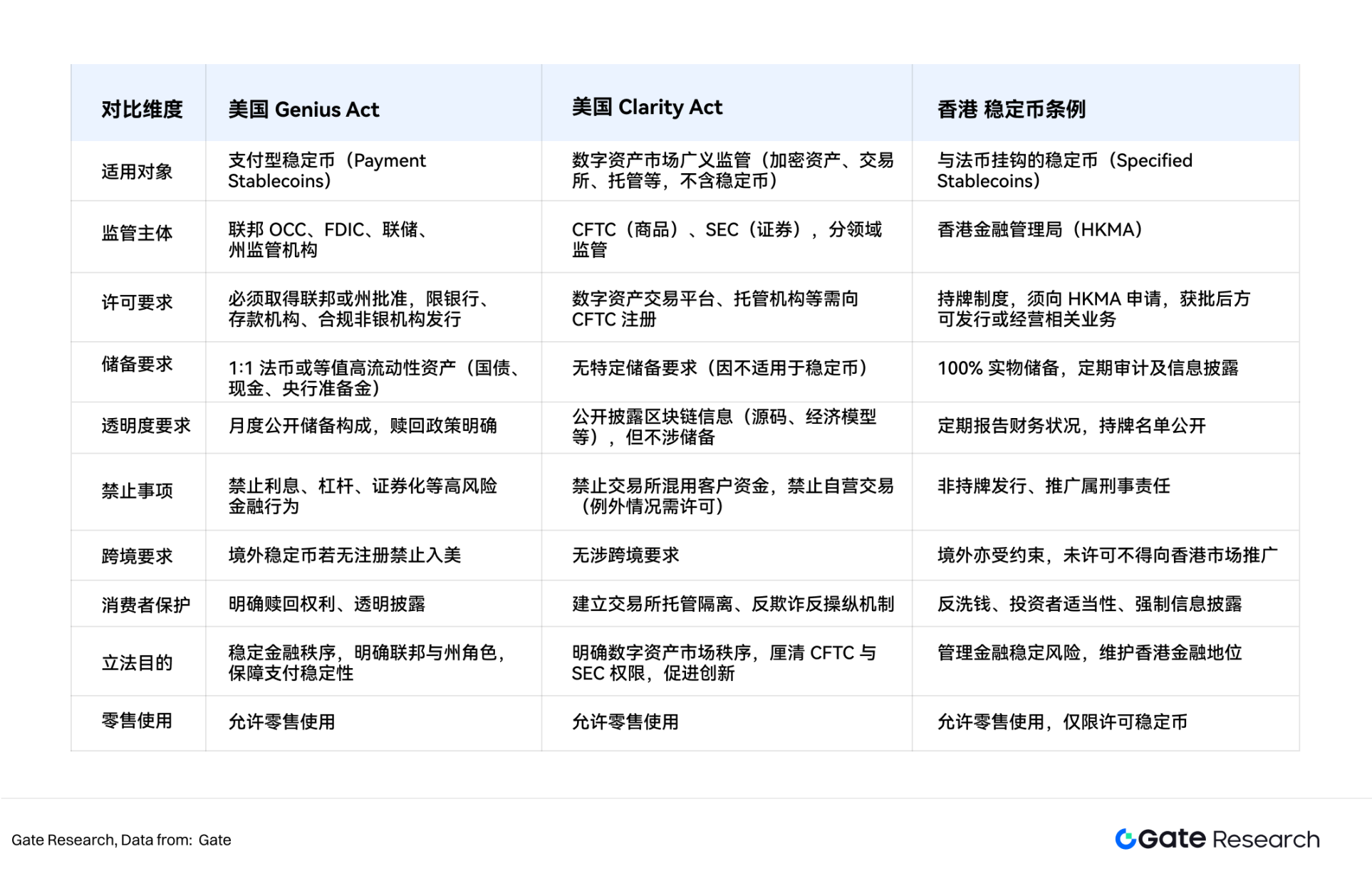

The renowned Genius Act (Guiding and Establshing National Innovation for US Stablecoins Act) was passed by the Senate on June 17, 2025, and by the House of Representatives on July 17, 2025, with a vote of 308–122. President Trump signed it into law on July 18, 2025. This marked the first time that the United States established a unified federal regulatory framework for stablecoin issuance. Its core provisions include:

•Regulatory model: A dual-track system of federal and state regulations is adopted, with unified authorization and licensing by the U.S. Office of the Comptroller of the Currency (OCC).

•Issuing entities: limited to banks, deposit institutions and approved specific non-bank financial institutions.

•Reserve requirements: 1:1 fiat currency reserves are required, and the reserve assets must be U.S. Treasury bonds or cash to ensure the stablecoin’s redemption ability.

• Transparency obligations: Issuers are subject to monthly audits, information disclosure and anti-money laundering reviews.

•Business restrictions: Issuers are prohibited from providing stored value interest or engaging in financial activities such as leverage and securitization to curb the accumulation of systemic risks.

•Cross-border restrictions: Prohibit unauthorized foreign stablecoins from circulating in the U.S. market and strengthen the capital market firewall.

On the same day, the Clarity Act (Digital Asset Market Clarity Act) passed the House of Representatives and was sent to the Senate for deliberation. Its primary purpose is to clarify the division of regulatory responsibilities between the SEC and the CFTC in the digital asset market, covering trading platforms, crypto derivatives, DeFi, and more.

3.2 Hong Kong launches the Stablecoin Ordinance

The Hong Kong Legislative Council passed the Stablecoin Ordinance on May 21, 2025, which will be officially implemented on August 1, 2025. The main contents include:

•Licensing system: All stablecoin issuance, sales, marketing and other activities must obtain permission from the Hong Kong Monetary Authority (HKMA).

•Scope of application: Focus on stablecoins pegged to fiat currencies, excluding products pegged to purely crypto assets.

• Capital requirements: The minimum capital requirement is HK$25 million, and effective risk management and internal control mechanisms must be in place.

•Reserve requirements: 100% reserves in physical or equivalent liquid assets, subject to regular audit and disclosure.

•Anti-Money Laundering and Consumer Protection: Strictly comply with AML/CFT regulations and investor suitability requirements.

•Liability for violations: Conducting relevant business without a license will constitute criminal liability, which may be punished by up to imprisonment and a fine.

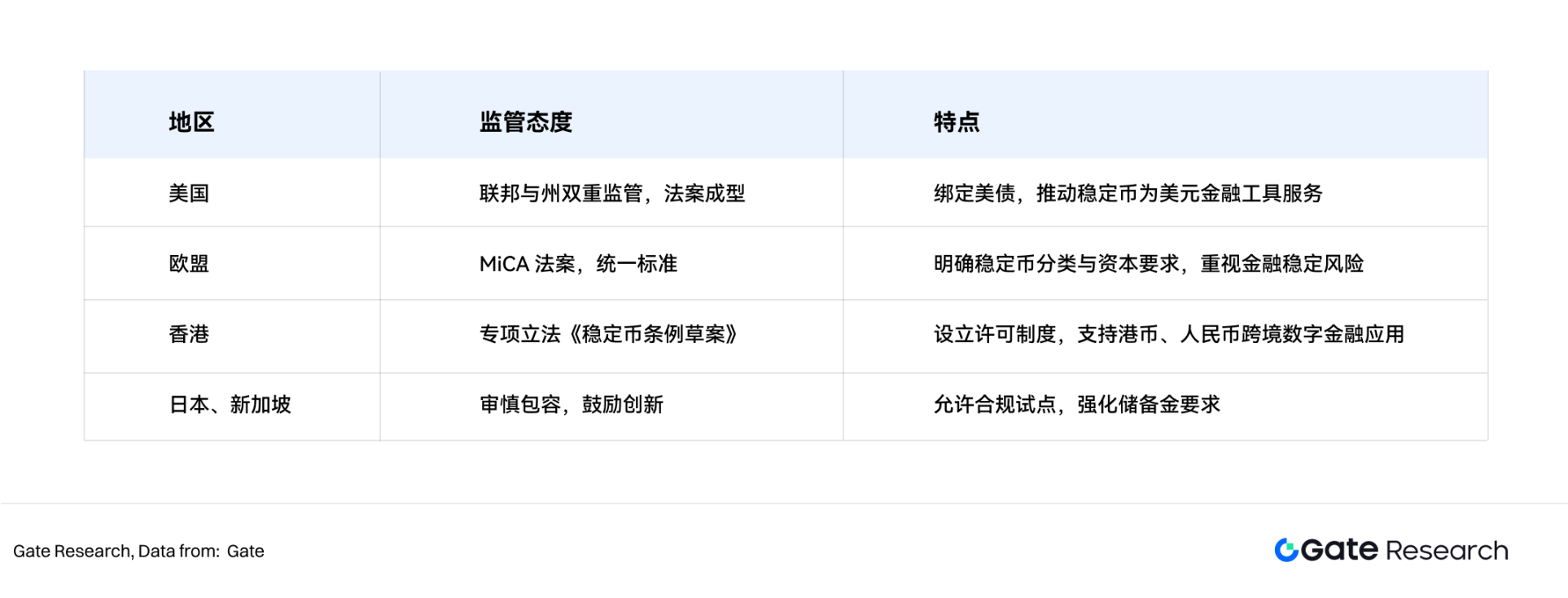

There are significant differences in the compliance requirements for stablecoins between Hong Kong and the United States:

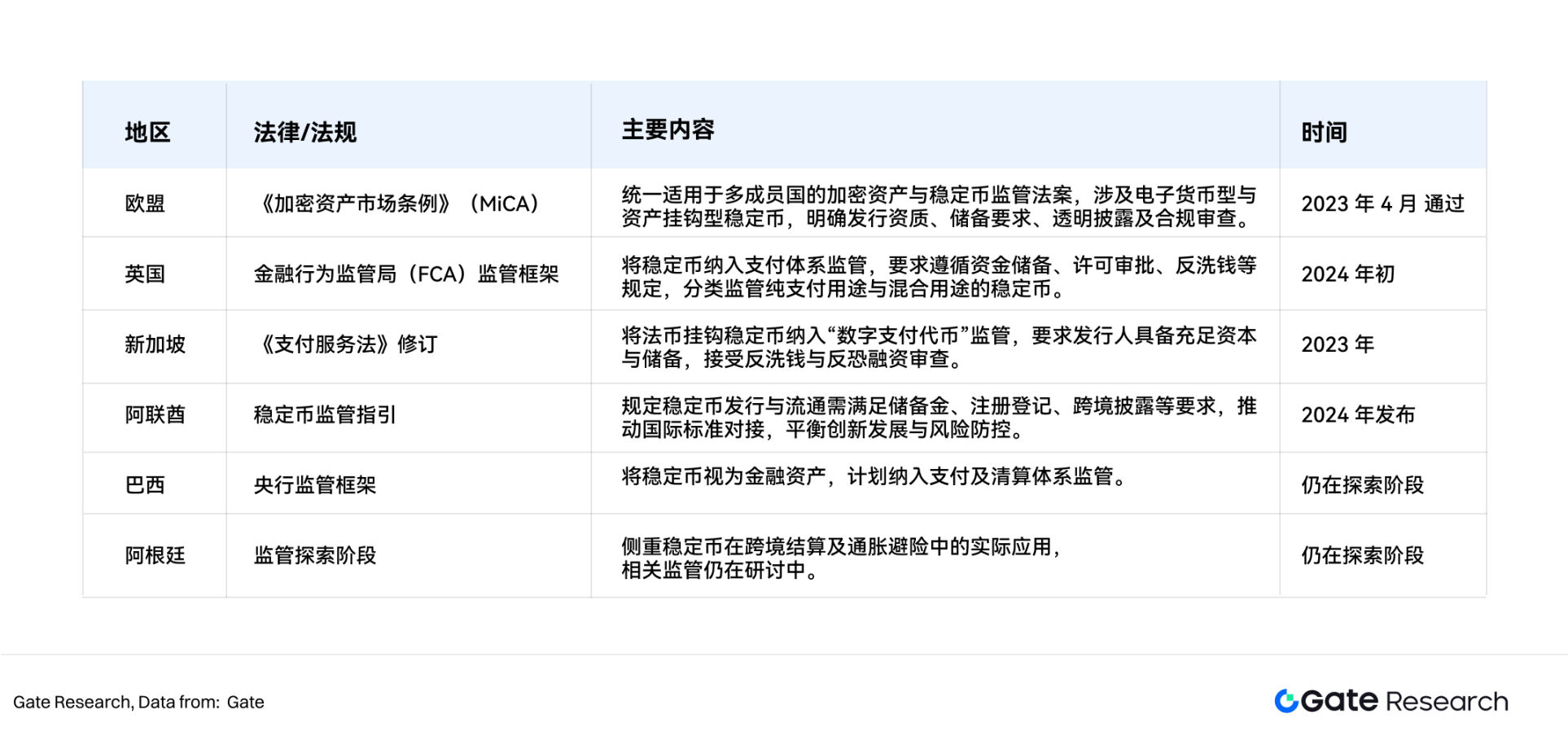

3.3 Dynamics of other economies

In addition to the United States and Hong Kong, other major economies are also actively promoting regulatory frameworks related to stablecoins, which are generally showing a trend of becoming more prudent and stricter and gradually taking shape.

Overall, regulatory oversight in various countries focuses primarily on collateralized stablecoins, excluding high-risk algorithmic stablecoins. This will further restrict the development of algorithmic stablecoins. Furthermore, Hong Kong only recognizes fiat-collateralized stablecoins, refusing to allow the issuance and circulation of crypto-collateralized stablecoins. This will further solidify the dominant position of fiat-collateralized stablecoins.

Although different countries have different regulatory attitudes and progress towards stablecoins, they generally build frameworks around core principles such as "reserve transparency, anti-money laundering review, consumer protection, and financial stability", and gradually align with their own digital asset or financial system regulations.

Reshaping the financial order under the leadership of stablecoins

4.1 The Competition for Financial Sovereignty Behind Stablecoins

In the current stablecoin market, USD-pegged stablecoins account for over 90% of market capitalization. Products like USDT and USDC have become de facto standards in global exchanges, DeFi, and cross-border payments. This not only maintains the dollar's dominance in traditional finance but also, through stablecoins, further deepens the dollar's influence in the emerging digital financial ecosystem.

Legislation such as the US Genius Act explicitly stipulates that US dollar stablecoins must be backed by high-quality assets such as US Treasury bonds and short-term notes, strengthening the link between stablecoins and core US dollar assets (Treasury bonds). This mechanism creates a dual anchor structure of "stablecoins and US Treasury bonds." By holding large amounts of US Treasury bonds, stablecoin issuers indirectly provide continuous buying power for the US Treasury, further solidifying the dollar's dominant position in the global financial system. This mechanism creates an "implicit buying relationship" between stablecoins and US dollar assets, solidifying the dollar's global financial hegemony.

The widespread global circulation of US dollar-denominated stablecoins has fostered a trend of "on-chain dollarization" in many emerging markets and high-inflation countries, eroding the use cases and financial sovereignty of local currencies. For example, in Argentina, Turkey, Russia, and other countries, USDT has become the default tool for asset preservation and cross-border payments. This phenomenon has been viewed in the literature as the US dollar's digital penetration of financially vulnerable countries through stablecoins, undermining their monetary policy independence.

At the same time, the progress of legal tender stablecoins such as the Euro and the Hong Kong Dollar in compliance reflects that countries are trying to hedge the spillover effects of the US dollar stablecoin through means such as the digitization of their own currencies and the legislation of stablecoins. A new round of currency competition in the digital age has begun, and the struggle for financial hegemony has shifted from the traditional system to the on-chain ecosystem.

4.2 Competition for the Next-Generation Financial Infrastructure

Stablecoins not only enable payments and transactions but are also becoming a core component of the next-generation cross-border payment and clearing infrastructure. Compared to the traditional SWIFT system, stablecoins offer advantages such as real-time settlement, low costs, and decentralization. The United States aims to replicate SWIFT's dominant infrastructure position in the on-chain financial world through its dollar-denominated stablecoins, incorporating global payment, settlement, and custody services into its rules and regulations. International financial centers such as Hong Kong and Singapore are using policy guidance to promote the deep integration of their local financial infrastructure with fiat stablecoins, aiming to establish themselves as hubs and nodes for cross-border digital finance.

4.3 Competition for Digital Asset Pricing Power

In the current digital asset market, stablecoins are not only a medium of exchange but also deeply involved in reshaping market pricing power. USDT and USDC virtually monopolize the major trading pairs in the crypto market, becoming the de facto standard for anchoring on-chain asset liquidity and pricing. Changes in their supply directly influence overall market risk appetite and volatility.

The United States has strengthened its control over digital asset market pricing and liquidity through stablecoin legislation and regulation, indirectly solidifying the dollar's central position in global capital markets. Meanwhile, Hong Kong and the European Union, through the promotion of regional stablecoins, hope to gain greater regional pricing power and influence in future digital financial competition.

Risks and Challenges

The risks of stablecoins come from the systemic risks brought about by their own price anchoring mechanism on the one hand, and the compliance risks brought about by external supervision on the other.

5.1 Preventing systemic risks

The core of stablecoin price stability lies in the value stability of the underlying assets. Therefore, the greatest systemic risk of stablecoins comes from the price fluctuations of their corresponding collateral, which can cause the stablecoin price to deviate from its anchor.

Looking back at the first stablecoin in history, BitUSD, it was released as early as 2014. Its price decoupled in 2018 and lost its 1:1 anchor relationship with the US dollar. This was because its collateral was an unknown, highly volatile asset without any guarantee - BitShares.

The same year, MakerDAO issued DAI, which employed over-collateralization and liquidation mechanisms to mitigate the risks associated with the high volatility of crypto assets. However, this inherently failed to improve capital efficiency and exposed the stablecoin to the price volatility of the collateralized assets. Similarly, stablecoins backed by fiat assets do not guarantee absolute security.

In March 2023, the collapse of three US banks—Silicon Valley Bank (SVB), Signature Bank, and Silvergate Bank—caused both USDC and DAI to decouple. According to Circle, the issuer of USDC, $3.3 billion in cash reserves used to collateralize the stablecoin were held at SVB. This caused USDC to drop by over 12% in a single day.

DAI's value also experienced volatility, primarily due to the fact that over half of its collateral reserves were pegged to USDC and related instruments. This situation stabilized after the Federal Reserve announced support for bank creditors, and USDC and DAI returned to their respective pegs. Since then, both stablecoins have adjusted their reserve structures, with USDC primarily holding its cash reserves at BNY Mellon and DAI diversifying its reserves across multiple stablecoins and increasing its holdings in real-world assets (RWAs).

This chain of depegging events reminds stablecoin issuers to diversify their assets to combat systemic risks.

5.2 Violation of the concept of decentralization

Although stablecoins once promoted the widespread use and compliant access of cryptocurrencies, their mainstream models (USDT, USDC, etc.) rely on centralized entity operations and fiat currency asset backing, which runs counter to the core concept of blockchain's native decentralization and censorship resistance.

Some scholars believe that fiat-collateralized stablecoins are essentially on-chain mirrors of fiat currencies such as the US dollar, which essentially strengthens dependence on the traditional financial system (the US dollar, the banking system), forming a "centralized core under the appearance of decentralization" and weakening the original ideal of decentralization of cryptocurrencies.

This centralized reliance not only subjects stablecoins to the credit risks of issuers and custodians, but is also likely to be frozen or tampered with in extreme circumstances (compliance policies, review pressure), violating the original intention of blockchain, which is "permissionless and tamper-proof."

5.3 Difficulties in cross-border regulatory coordination

Globally, stablecoins involve multiple jurisdictions, cross-border financial and data flows, but there are significant differences in regulatory stances, definitions, and compliance requirements for stablecoins across countries:

Due to the large differences in regulatory frameworks among countries, stablecoins face strong uncertainties and legal risks in cross-border use, settlement and compliance processes, which can easily lead to "regulatory arbitrage" and compliance gaps, hindering their global development.

5.4 Potential Financial Sanctions Risks

With the turbulent international situation, stablecoins also face the risk of being included in the financial sanctions toolchain. The United States, through its regulatory-led USD stablecoins, may leverage their global on-chain payment and settlement properties to strengthen scrutiny of capital flows and fund usage, and even impose sanctions such as freezes and blockades on specific entities and countries.

Alexander Baker noted that stablecoins have, to some extent, become an extension of the on-chain dollar and may, like traditional systems like SWIFT, become part of the US financial weaponization toolkit. This undoubtedly increases political and compliance risk exposure for some emerging markets, cross-border transactions, and on-chain financial projects, driving further global exploration of de-dollarization and regional stablecoins.

Conclusion

The rise of stablecoins epitomizes the reshaping of the monetary order in the digital financial era. Since their inception, stablecoins have steadily penetrated various sectors, including payments, transactions, and asset reserves. With their high efficiency, low cost, and programmability, they have gradually become a crucial bridge connecting traditional finance and the digital economy. Today, stablecoins are not only core infrastructure for the crypto market but also profoundly impact the evolution of the global financial landscape, and are increasingly being incorporated into the financial regulation and monetary strategies of a growing number of countries.

Behind the rise of stablecoins lies a hidden competition between monetary sovereignty and financial hegemony. The dominance of US dollar-denominated stablecoins in the global market further solidifies the dollar's dominance in the on-chain world. The deep ties between its reserve structure and US Treasury bonds also make stablecoins a crucial extension of US financial strategy. Emerging markets and other major economies, on the other hand, are attempting to gradually mitigate the pervasive influence of US dollar-denominated stablecoins through local stablecoins, digital currency regulation, and the development of cross-border payment systems, thereby promoting global currency diversification and the digitization of their own currencies. Stablecoin legislation has become a key variable in the future reshaping of the international financial order, reflecting deeper national interests and the redistribution of financial power.

However, the future development of stablecoins still faces numerous uncertainties. First, the systemic risks inherent in the anchoring mechanism and reserve structure are difficult to completely eliminate in the short term, and potential trust crises and market volatility remain. Second, a unified global regulatory framework has yet to emerge, and cross-border regulatory coordination and legal application face numerous obstacles. Stablecoins continue to operate in a gray area, facing ongoing compliance and policy risks. Third, issues such as centralized issuance and the weaponization of finance create inherent tensions between stablecoins and the inherent principles of blockchain decentralization and censorship resistance. Balancing regulatory compliance and technological autonomy remains a core issue that the industry must address.

In the future, stablecoins will play an increasingly important role in financial infrastructure, currency competition, and the international settlement system. Their development path is related not only to the deep integration of decentralized finance and real-world assets, but also to the construction of a new global financial order and the redistribution of discourse power.

References

•Gate, https://www.gate.com/zh/price

•Sky, https://sky.money/

•Deltec, https://www.deltecbank.com/news-and-insights/the-history-of-stablecoins/

•Tether, https://tether.to/en/

•DeFiLlama, https://defillama.com/stablecoin/dai

•CSPengyuan, https://www.cspengyuan.com/pengyuancmscn/credit-research/macro-research

•rwa.xyz, https://app.rwa.xyz/stablecoins?utm_source=substack&utm_medium=email

•Swift, https://www.swift.com/about-us/legal/document-centre

•Congress, https://www.congress.gov/bill/119th-congress/senate-bill/394/text

•Whitehouse, https://www.whitehouse.gov/fact-sheets/2025/07/fact-sheet-president-donald-j-trump-signs-genius-act-into-law/