Author: Zuo Ye

Within a month, the crypto market experienced two shocks, October 11th and November 3rd. Whether DeFi still has a future has become a common question. At this time, it is a good time to observe the current DeFi market structure and the direction of change.

From a macro perspective, DeFi is rapidly shedding the "second system effect," and the impact of stablecoins on traditional banks and the payment industry is becoming increasingly real, as evidenced by the Federal Reserve's attempt to provide streamlined master accounts. Institutional DeFi represented by Aave, Morpho, and Anchorage is changing the operating model of traditional finance, while Uniswap's plan to open its fee switch and the ongoing battle of Perp DEX represented by Hyperliquid continue.

The immaturity of DeFi lies in choosing a noble death for the sake of ideals. We are far from declaring DeFi fully mature and only needing large-scale adoption. Two dark clouds still linger in the sky of DeFi:

- Who is the ultimate lender in the entire on-chain economic system? Morgan created the Federal Reserve, so what mechanism should assume a similar role in DeFi?

- Beyond the endless repackaging of existing DEX/Lending/Stable products, how can truly original DeFi tracks or mechanisms be developed?

Price is the result of a game.

But, as long as you're connected to the internet, I'll be right beside you.

We are often blinded by the omnipresent nature of things. In the DeFi universe, all innovations to date have revolved around DEX, Lending, and Stablecoin. This is not to say that BTC/ETH are not mechanism innovations, nor that RWA/DAT/crypto-equity/insurance are not asset innovations.

Referring to the six pillars of on-chain protocols, BTC and Bitcoin do not inherently require any other assets or protocols. The DeFi we are talking about refers to projects that occur on public chains such as Ethereum/Solana/L2. Referring to the leverage cycle of crypto, stocks and bonds, the cost of selling innovative assets is getting higher and higher, and the entire industry is pursuing products with real profitability, such as Hyperliquid.

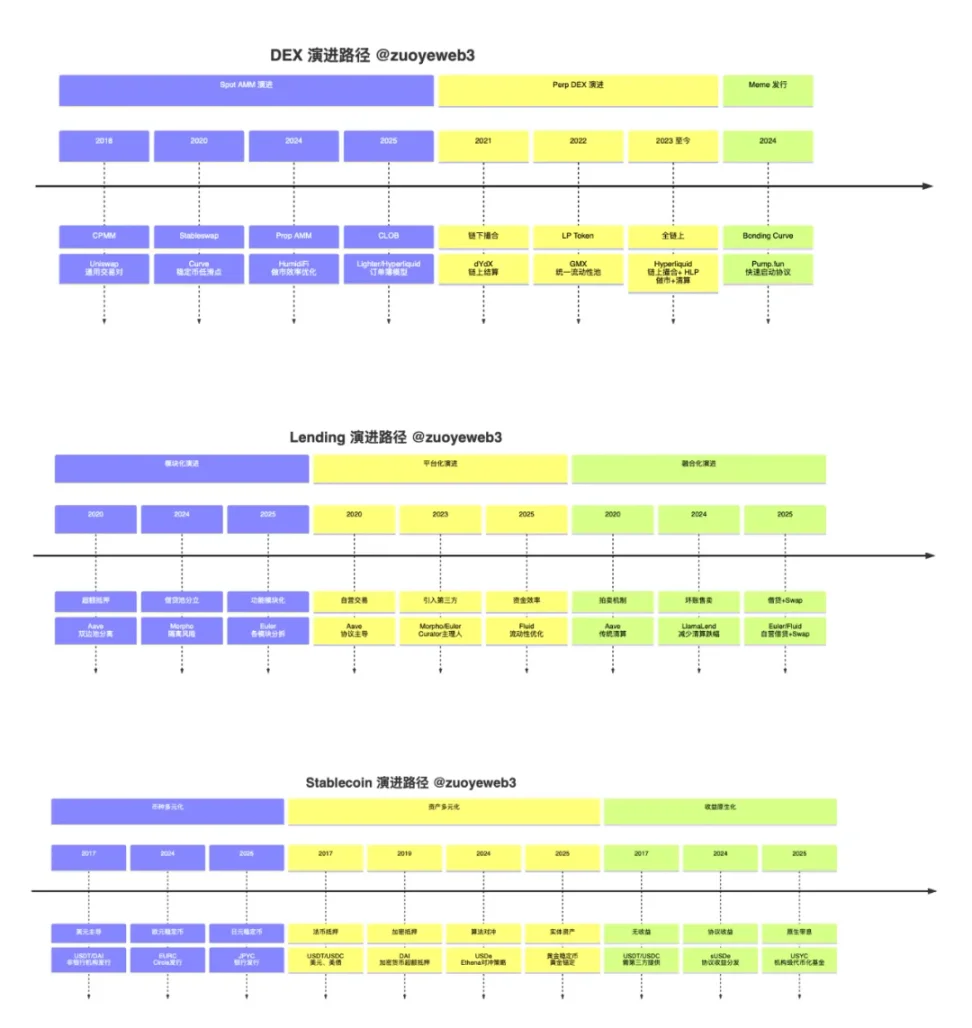

Image caption: The evolution of the DeFi paradigm. Image source: @zuoyeweb3

Since the end of DeFi Summer, DeFi innovations have been continuous improvements on existing products, assets, and established facts. For example, trading is divided into three types: spot, Perp, and Meme, which correspond to AMM/CLOB/Bonding Curve during DeFi Summer. Even the most innovative Hyperliquid has many traces of Serum.

From the most micro perspective, Pendle started with the earliest fixed-income products, then embraced yield-generating stablecoins such as LST/LRT and Ethena, and Euler and Fluid both chose to build their own lending + swap products. If users set yield strategies using YBS such as Ethena, it is theoretically possible to use DEX/Lending/Stablecoin simultaneously on any chain, any protocol, and any Vault.

While this synergistic effect amplifies profits, it also "creates" numerous liquidation tragedies and trust crises. Beyond this, there are no-go zones everywhere. Blockchain is born free, yet it is shackled everywhere.

Decentralization is a wonderful vision, but centralization is more efficient and less competitive. Centralization of protocols is even more problematic. Aave is certainly large and secure, but this also means that you have very few more and newer options, while newcomers like Morpho/Euler can only embrace insecure administrators and "inferior" assets.

Unbanked sparked a rush for stablecoins in the Third World. While it cannot be said that Aave's prudence caused Morpho's crisis, unAaved did trigger a rush among on-chain users and the younger generation for subordinated bonds, subordinated protocols, and subordinated managers.

Innovation can only happen among marginalized groups, where the cost of trial and error is too low. Those who survive will repeatedly disrupt the established order, and Aave V4 will become more like its own competitor than its own past success.

The protocols and their tokens we see now, their market prices and trading volumes are merely a direct reflection of the current environment; in other words, they are already an acknowledgment of the results of repeated games.

Whether it will be effective in the future, or even have any reference value, is hard to say. Stablecoin chains Plasma and Stablechain are extremely popular, but it is almost impossible for them to challenge the adoption rate of Tron and Ethereum. Even xUSD's challenge of USDe, which is much smaller than USDT, has already failed.

Pricing systems favor time; protocols that survive longer tend to survive even longer. The success of Hyperliquid and USDe is an outlier and a maverick. It's debatable how much market share Euler/Morpho/Fluid can take from Aave, but it's almost impossible for them to replace Aave.

Image caption: Crypto Gravity Wells: Timescales and Income, Image credit: @zuoyeweb3

Crypto Gravity Well: Time and App Rev [Continuous] From left to right is the token issuance time, from top to bottom is the Rev.

- Time: Balancer (stolen), Compound (silent), Aave (thriving) capture our time.

- Rev: Earning power is the only commercial value. One is the value of its own token BTC (USDT issuance, yield stablecoins want to take this shortcut), and the other is the ability to capture value (Pump's mining, withdrawal and selling).

Competition is becoming increasingly fierce, with companies burning through cash to achieve growth.

As shown in the figure above, the x-axis represents the duration of the protocol to date, and the y-axis represents the protocol's ability to capture value. Compared to metrics such as token price, trading volume, and TVL, profitability is the most objective indicator (Polymarket theoretically does not generate profits).

In theory, the earlier a protocol is established, the stronger its stable profitability. If a newcomer wants to enter the market, it can only continuously enhance its own token liquidity and trading volume flywheel, similar to Monad/Berachain/Story. Failure is the most likely outcome.

Value as a goal in balance

We should have faith in the power of the masses, but not in their wisdom.

DeFi is a movement, and compared to exchanges and TradeFi, it is indeed one of the best innovation cycles in history in the context of overall easing, and may give rise to a new paradigm that surpasses the DeFi Summer.

Exchanges are being hit hard, and Hyperliquid's transparency has for the first time demonstrated stronger antifragility than Binance. After 1103, the pace of lending and stablecoins has slowed but not been disproven. People do need subprime bonds, as well as simple funds/bonds/equity certificates—stablecoins.

While market makers were restricted from migrating liquidity from CEXs during 10.11, on-chain trading, spot/contract trading, and alternative assets are all actively expanding their scale. As long as the problems can be engineered and combined, there is a possibility that they can be completely solved.

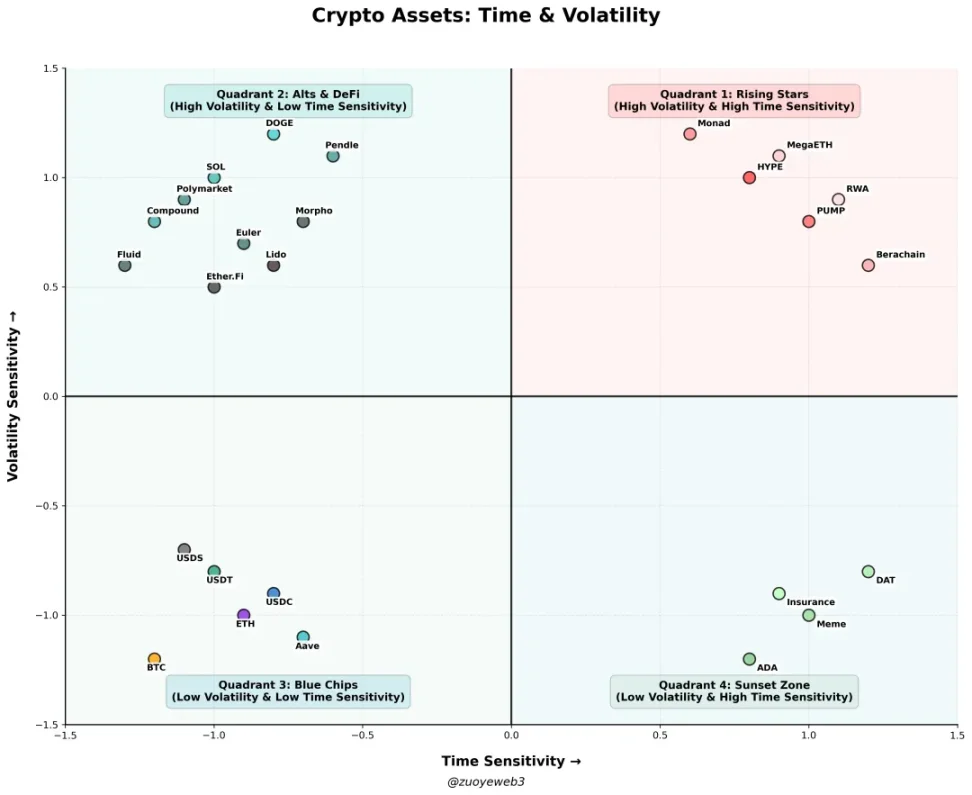

Image caption: Crypto assets: Time & volatility, Image source: @zuoyeweb3

- Quadrant 1 (Emerging Stars): HYPE, PUMP, Public Chains/L2/Alt L1 (Monad, Berachain, MegaETH), RWA (Bond, Gold, Real Estate)

- Second Quadrant (Altcoins): DOGE, SOL, Compound, Pendle, Polymarket, Euler, Fluid, Morpho, Ether.Fi, Lido, No-USD Stablecoin, Option

- Third Quadrant (Industry Leaders): BTC/ETH/USDT/USDC/USDS/Aave/

- Fourth Quadrant (Death Zone): ADA, Meme, DAT, Insurance

Many new assets are placed in the Rising Star Zone, which is more sensitive to time and volatility. They are essentially short-term speculative assets. Only by transcending simple game cycles and falling into stable holding groups and use cases can they enter the Altcoin Zone, which is not particularly sensitive to time, but whose liquidity cannot withstand drastic market changes. Most projects will stay in this zone.

Moreover, the harder the project team works, such as through measures like ve(3,3), buyback, destruction, merger, and renaming, they may still remain at this point. This can be seen as a gradual ramp-up period. If you don't move forward, you fall behind; even if you try to move forward, you may still regress.

The rest of the story is simple: those that successfully pass through the tribulation enter the stable zone and become so-called assets that transcend cycles, such as BTC and ETH, and perhaps half of SOL and USDT. However, most assets will slowly die out, at which point they are neither sensitive to time nor have any volatility.

Memes and DATs will exist as a long-term market, but assets belonging to them are unlikely to have long-term opportunities. DOGE and XRP, among a very few representative assets of memes and clones, are outliers.

In fact, if we view protocols as asset innovation, many problems become clear: the goal of a startup is to sell itself once and for all, rather than to become a sustainable open system.

- Spot DEX: The trading itself focuses on mainstream assets (BTC/ETH) and whales swapping positions. Retail investors no longer trade altcoins. The core of the project is to seek specific customers rather than become a permissionless public infrastructure, such as dark pools to rationalize the information gap between whales and retail investors.

- Perp DEX: The news of Lighter's huge funding round is a prelude to its token launch, and the VCs are highly polarized. Big Name is more like a TGE financing party, while small VCs can only perish in the Perp track, and retail investors can only pick up trash from all kinds of launchpads.

- Meme: Emotions themselves have become a tradable asset, failing to become an industry-wide consensus. PumpFun shows no ability or indication of solving this problem.

- Platform-based & modular lending: a long-term trend. Lending agreements can sell their liquidity, brand, and technology in segments, essentially a B2B2C model.

- The integration of DEX and Lending is among the newest in this matryoshka doll-like development; a dedicated article will be published later to explain its mechanisms.

- Non-USD stablecoins/non-USD-pegged stablecoins: In the short term, the focus is on developed regions such as the Euro, Japanese Yen, and Korean Won, but in the long term, the market can only be found in the Third World.

This section focuses on the market situation of yield-based stablecoins. Overall, yield-based stablecoins are the most suitable asset form for linking DEX/Lending/Stable, but they require massive engineering and combination capabilities.

In contrast, there are innovative models outside of DEX/Lending/Stable, but the number of observed samples is currently small. For example, the stablecoin NeoBank is still a combination of the three, and the prediction market belongs to the broad DEX type. The better ideas may be Agentics and Robotics.

The internet has brought about replicable scalability, which is very different from the production model of the industrial era. However, there has been no corresponding economic model for a long time. Advertising economics requires sacrificing user experience. Compared with LLM on-chain, Agentics is at least more in line with the technical characteristics of blockchain, namely the all-weather transaction efficiency brought by extreme programmability.

With the gradual decrease in gas fees, and years of TPS improvements and ZK development, the large-scale adoption of blockchain has the potential to occur in a replication economy that does not require human intervention.

The combination of robotics and cryptocurrency is not very interesting in the short term. At least until Yushu has shed its gimmick and educational value, it will be difficult for robots to truly take root in Web3. As for the long term, only time will tell.

Conclusion

Make DeFi more DeFi.

Robotics has been around for too long; a reckoning must be done in a minute.

The combined liquidation mechanism of DEX+Lending was a proactive measure to address the DeFi crisis, but it couldn't stop the spread of the 11.03 crisis. The most effective measure was Aave's early rejection. However, looking at the entire industry, how to handle liquidation and restore the market has become the biggest challenge.

In 2022, after the 3AC incident, SBF took the initiative to acquire and restructure the agreement involved. Then, less than six months later, FTX was also taken over by a traditional law firm. After the collapse of Stream's xUSD, it was also handed over to a law firm immediately.

Code is Law; it's about to become Lawyer is Coder.

Before SBF and law firms, BTC has long served as the ultimate liquidator, but it will take a long time to rebuild people's trust in the on-chain economy. But at least, we still have BTC.