Author: seed.eth

On the last trading day of January 2026, the global financial markets witnessed a moment of terror that will go down in history.

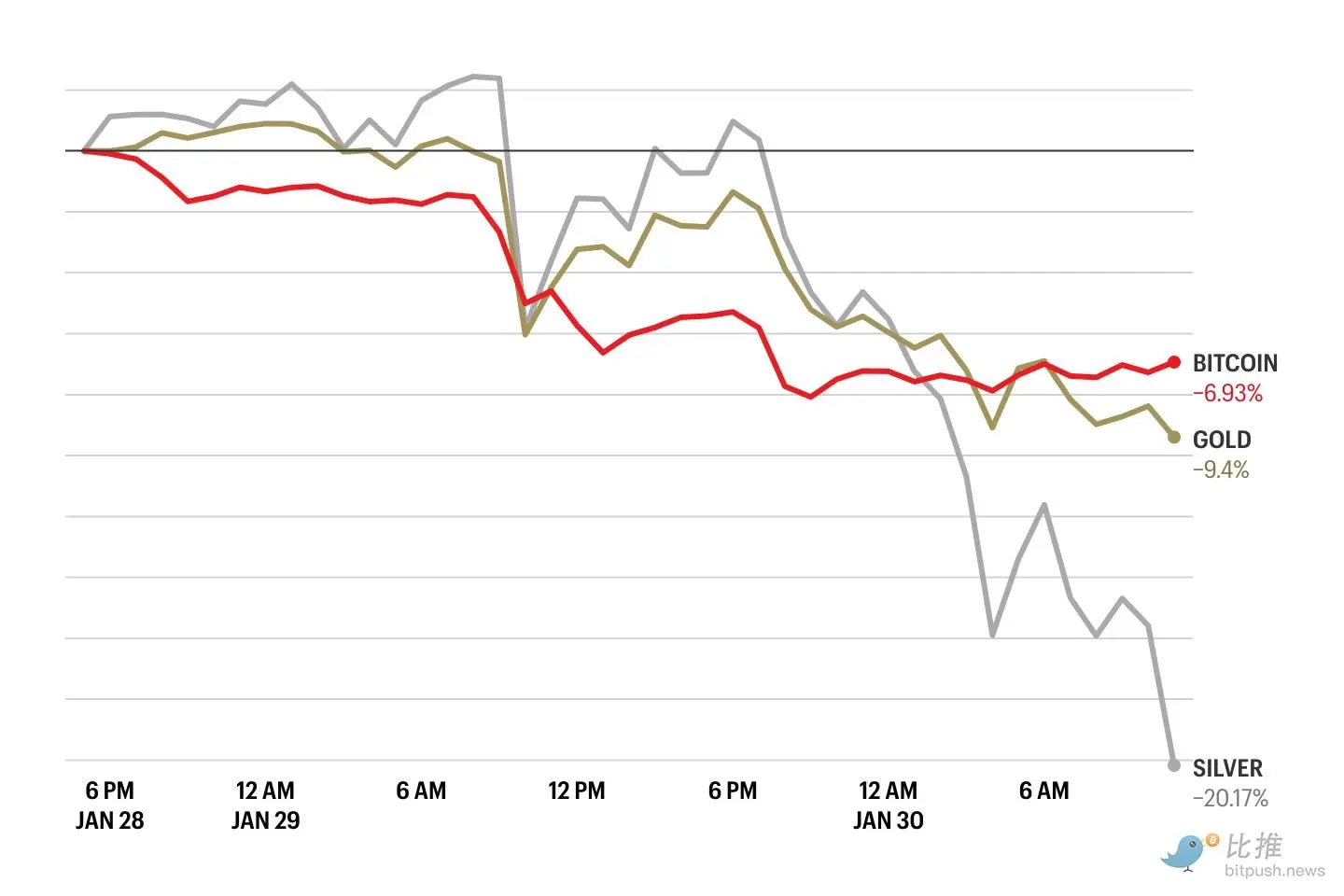

On Friday, January 30th (Eastern Time), the precious metals market, which had been surging and constantly breaking historical highs, was suddenly hit by a "cold wave".

Spot silver suffered its biggest single-day drop in history, plunging more than 30% at one point during the session; spot gold was not spared either, falling more than 9% in a single day, marking its worst loss since the early 1980s. Meanwhile, the previously weak US dollar index (DXY) suddenly surged, posting its biggest single-day gain since July of last year, rebounding by about 0.9%.

In the US stock market, the S&P 500 fell 0.4%, the Dow Jones Industrial Average fell 0.4%, while the Nasdaq, dominated by technology stocks, plunged 0.9%.

The cryptocurrency market was not spared either. Bitcoin (BTC) plunged as much as 4% to $81,045, hitting a two-month low since November of last year. Although it subsequently rebounded, it remained weak under pressure from continued outflows from ETFs.

This massive global asset restructuring not only wiped out trillions of dollars in market value from the precious metals market, but also marked the first major correction to the trading logic of "weak dollar, strong gold and silver" since Trump returned to the White House.

Policy "hurricane": Warsh's nomination ignites the dollar's counterattack

The immediate trigger for this plunge in gold and silver prices was a major personnel appointment by the Trump administration. News on Friday indicated that Trump had selected Kevin Warsh as the next Federal Reserve Chairman.

This decision caused multiple shocks in the market:

- Defending the Fed's Independence: Previously, the market was highly concerned that Trump would choose a "proxy" who would completely submit to his will and favor aggressive interest rate cuts. This concern directly contributed to the continued decline of the dollar in January. Warsh, a former Fed governor, is known for his academic rigor and vigilance regarding inflation. His nomination greatly alleviated Wall Street's fears of the Fed's "politicization" and restored market confidence in the Fed's independence.

- Reshaping Interest Rate Expectations: Warsh historically exhibited a distinctly hawkish stance, showing near-zero tolerance for inflation. Compared to the potentially deep rate cuts that leading figures might have brought, the market quickly adjusted its expectations to a "more moderate and prudent" monetary policy. As assets that do not generate interest, gold and silver have become significantly less attractive under the expectation that "interest rates may remain high."

- Dollar short positions halted: The dollar index fell by about 1.4% in January, resulting in extremely crowded short positions. The news of Warsh's nomination prompted a large number of dollar short positions to be closed, causing the dollar index to rise rapidly above 96.74, which dealt a heavy blow to dollar-denominated precious metals.

Krishna Guha, vice chairman of Evercore ISI, said the market is trading in line with “Wash’s hawkish stance.” He added, “Wash’s nomination will help stabilize the dollar and reduce the one-sided risk of a continued weakening of the dollar, thus challenging the logic of the ‘currency devaluation trade’—which is also the reason for the sharp drop in gold and silver prices.”

Liquidity crisis in overbought territory

If Walsh's nomination is "Mars," then the extremely overbought state of the gold and silver markets is "dry tinder."

Before the crash on January 30, spot gold had approached the $5,600/ounce mark, while silver had peaked at $120/ounce. Since the beginning of the year, silver had risen by as much as 63%, and gold had risen by nearly 20% this month. A Wall Street quantitative strategist said, "This is no longer a rise that can be explained by fundamentals, but a typical speculative bubble driven by FOMO (fear of missing out).

Multiple technical factors led to Friday's "stampede" sell-off:

RSI indicator peaks: Gold's Relative Strength Index (RSI) reached a 40-year high (RSI close to 90) before the crash, indicating extreme overbought conditions.

Forced liquidation: Due to its high leverage, the silver market experienced massive programmed stop-loss orders after prices broke through key support levels. Estimates suggest that the market capitalization of gold and silver shrank by as much as $7.4 trillion on Friday. This scale of sell-off has evolved into a "liquidity contraction," forcing investors to sell the most liquid assets, gold and silver, to replenish margin for other assets.

Profit-taking: Early investors have a strong desire to cash out when faced with signals of a policy shift.

The combination of a stronger US dollar and a sharp drop in gold and silver prices has directly and severely damaged commodity currencies among the G10 currencies.

Australian Dollar (AUD): It plunged more than 2% at one point during the day. As a leading exporter of resources, the collapse of gold and silver directly damaged its trade foundation, making it the hardest-hit currency among the G10 currencies that day.

Swiss Franc (CHF): The price fell by about 1.5%. The sharp drop in gold prices completely severed the safe-haven premium of the Swiss franc, causing funds to flow into the US dollar, which was supported by hawkish expectations, amid panic.

Swedish krona (SEK): Plunges nearly 1.8% intraday.

Market Outlook: Is it a "Bull Market Correction" or a "Market End Signal"?

A research report from Citibank offers a sober perspective on the market outlook. Citibank points out that half of the risk factors supporting gold (such as geopolitical tensions, US debt concerns, and AI uncertainty) may subside later in 2026.

- Middle East and Russia-Ukraine Variables: As the Trump administration is committed to achieving "American-style stability" before the 2026 midterm elections, if the Russia-Ukraine conflict and the situation in Iran ease, the safe-haven premium for gold will further diminish.

- American-style gold stability: Citigroup's mention of "American-style gold stability" suggests that if Warsh successfully takes office and stabilizes the Fed's credibility, the dollar will regain favor with international capital, thus putting medium-term negative pressure on gold prices.

However, some analysts hold a different opinion.

Nanhua Futures points out that despite the significant short-term volatility, demand for silver in the new energy and industrial sectors remains strong, and a supply gap has long existed. This sharp drop is more of a result of deleveraging and bubble deflation than a complete deterioration of fundamentals.

JPMorgan analysts are bullish on gold's long-term prospects. In a recent report, they stated that both private investors and central banks are consistently increasing their gold allocations.

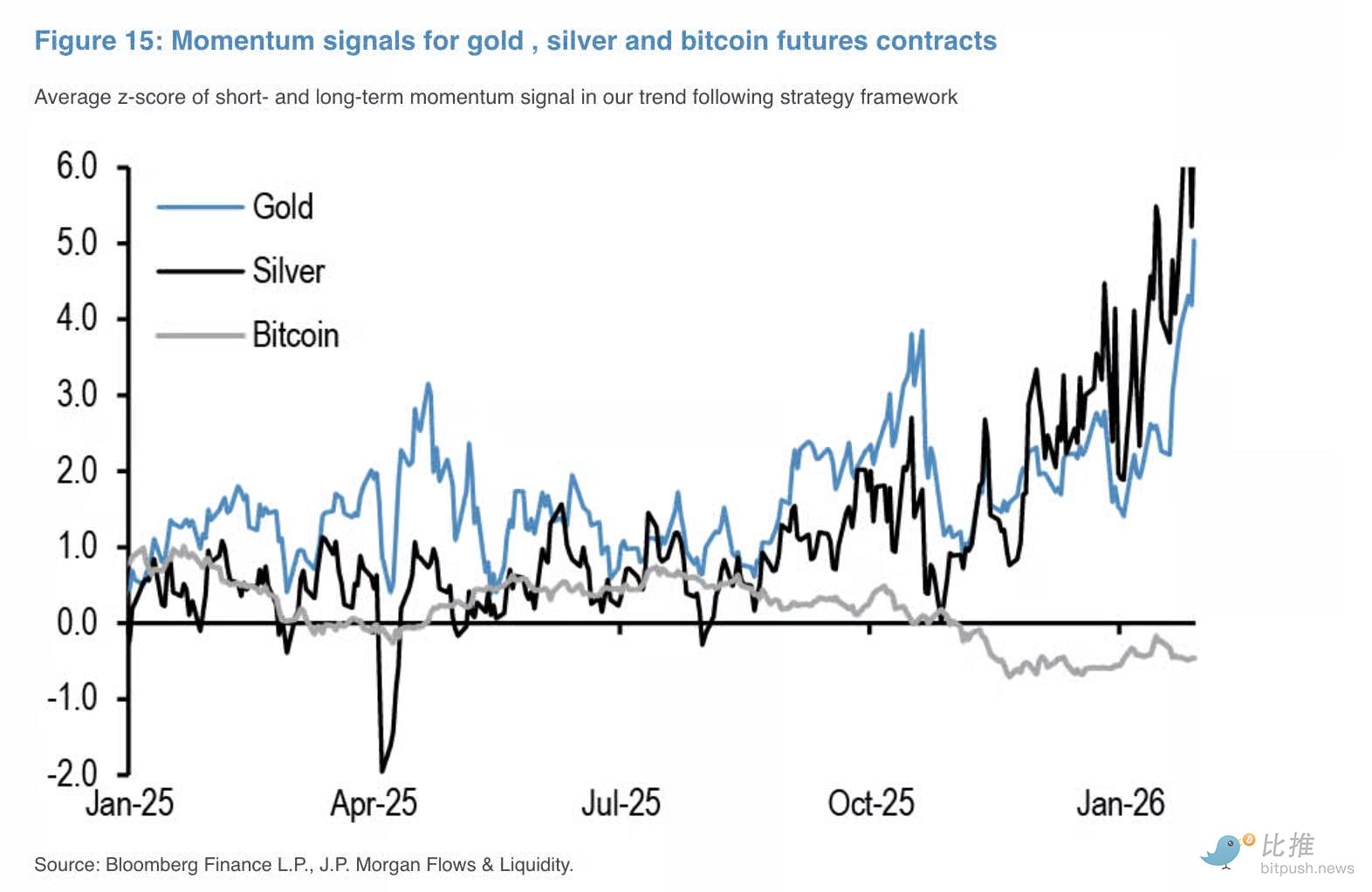

Analysts used the Hui-Heubel ratio (a metric for market breadth and liquidity) to highlight structural differences in liquidity across different assets. The chart shows that gold consistently has a lower Hui-Heubel ratio, indicating stronger liquidity and higher market participation. Silver, on the other hand, has a higher ratio, reflecting weaker liquidity. Assuming people continue to use gold as a substitute for long-term bonds as a stock hedge, private investor allocations to gold could rise from the current slightly over 3% to around 4.6% in the coming years. In this scenario, analysts believe the theoretical price range for gold could reach $8,000 to $8,500 per ounce.

For ordinary investors, the most crucial point to observe at present is:

If, after Warsh takes office, the Federal Reserve's policy focus truly shifts from "blindly supporting growth" to "returning to monetary discipline," then 2026 will be a turning point for the global financial environment.

This shift means that the US dollar index is poised to completely break free from its year-long slump and regain its dominance as the global reserve currency; while gold and silver, pushed to their peak by previous euphoria, may be forced into a long and painful period of consolidation to digest the premium bubble accumulated over the past few years. The future of Bitcoin will become even more uncertain.