Preface

On May 21, 2025, the Legislative Council of Hong Kong, China formally passed the Stablecoin Bill in the third reading, and then it was officially promulgated on May 30, marking that the Stablecoin Bill has officially become law and is expected to come into effect this year.

The Ordinance defines stablecoins as "legal currency-collateralized stablecoins", which are tokens that use legal tender (such as Hong Kong dollars and US dollars) as anchor assets to maintain stable value. After the implementation of the Ordinance, three types of activities related to stablecoins must obtain licenses: first, issuing stablecoins in Hong Kong; second, issuing stablecoins anchored to Hong Kong dollars in or outside Hong Kong; third, actively promoting the stablecoins issued by them to the Hong Kong public.

The regulations also stipulate that stablecoin issuers must apply for a license from the Hong Kong Monetary Authority (HKMA) with a minimum registered capital of HK$25 million. There are four requirements for licensees: First, in terms of reserves, licensees must maintain a robust stablecoin mechanism to ensure that the reserve assets of stablecoins are composed of high-quality and highly liquid assets, and are equal to the denomination of the circulating legal currency stablecoins at any time, and are properly separated and kept; second, stablecoin holders have the right to redeem stablecoins from the issuer at face value, and redemption requests must be free of charge and processed within a reasonable time. Third, a series of requirements for combating money laundering, risk management, disclosure, and auditing appropriate persons must be met; fourth, transactions must be conducted on licensed virtual asset trading platforms.

The entry into force of the Stablecoin Ordinance marks that Hong Kong has officially incorporated stablecoins into its financial regulatory system. Hong Kong has become the world's first jurisdiction to establish a comprehensive regulatory framework for "fiat-collateralized stablecoins". Compliant Hong Kong stablecoins are expected to be officially launched before the end of this year.

Hong Kong Stablecoin Issuer Sandbox

In addition to legislating on the stablecoin licensing system, HKMA also launched the Stablecoin Issuer Sandbox in March 2024 as one of HKMA's initiatives to promote the sustainable and responsible development of Hong Kong's stablecoin ecosystem. Through the "Sandbox", HKMA allows institutions that intend to issue stablecoins in Hong Kong to test their operational plans and conduct two-way communication on the proposed regulatory requirements to develop a regulatory system that is fit for purpose and risk-based. Therefore, it is highly likely that participants in the "Sandbox" will obtain the first batch of stablecoin licenses.

On July 18, 2024, HKMA announced three groups of participants in the stablecoin issuer sandbox, namely JD CoinChain Technology (Hong Kong), Yuanbi Innovation Technology, and a group consisting of Standard Chartered Hong Kong, Animoca Brands, and Hong Kong Telecom (HKT).

JD CoinChain Technology (Hong Kong) is a subsidiary of JD Technology Group. Its main business includes digital currency payment system and blockchain infrastructure construction. JD Technology Group is a business sub-group of JD Group that focuses on technology-based industry services. Relying on cutting-edge technology capabilities such as artificial intelligence, big data, cloud computing, and the Internet of Things, JD Technology has created products and solutions for different industries to help enterprises in all industries in the whole society reduce supply chain costs, improve operational efficiency, and become a digital partner worthy of industry trust. Liu Peng, CEO of JD CoinChain Technology, talked about the current status of JD Stablecoin: JD Stablecoin is a stablecoin based on the public chain and pegged 1:1 to legal currencies such as Hong Kong Dollar (HKD) or US Dollar (USD). It has entered the second phase of sandbox testing and will provide mobile and PC application products for retail and institutions. The test scenarios mainly include cross-border payments, investment transactions, retail payments, etc.; it is cooperating with leading compliant exchanges; in retail payment scenarios, it is docking and testing with acquiring scenarios such as JD Hong Kong and Macau Station.

Yuanbi Innovation Technology is a subsidiary of Yuanbi Technology. Yuanbi Technology uses innovative financial technology to build a business world of mutual trust and interconnection. Yuanbi Technology is based in Hong Kong and its mission is to make cross-border payments and financial services easier and cheaper for businesses. Yuanbi Technology has a background in DeFi, digital payments and financial technology. Its board members include former Hong Kong Monetary Authority CEO Norman Chan, HashKey Group Chairman Xiao Feng, ZhongAn International President Xu Wei, Sequoia China Managing Director Wang Hao, senior investor Zheng Tuo, HashKey Group CCO Zhang Dayong and Yuanbi CEO Liu Yu. Yuanbi Technology received US$7.8 million in Series A1 financing on September 30, 2024, including strategic investments from well-known industry companies such as Sequoia China, Hivemind Capital, Aptos Labs, Hash Global, SNZ Capital, Solana Foundation, Anagram and Upward Capital. Circle Coin Innovation Technology is testing its Hong Kong dollar stablecoin operation plan in the HKMA sandbox. At the same time, Circle Coin Wallet Technology, another subsidiary of Circle Coin Technology, has obtained a stored value facility (SVF) license issued by the HKMA and will officially operate by the end of 2023. With the platforms and capabilities of each subsidiary, Circle Coin Technology is actively building a trusted and compliant financial platform network.

Standard Chartered Bank is a leading international banking group headquartered in London, UK. It is one of the international banks with the longest history in China. Standard Chartered Bank has been operating in Hong Kong since 1859 and is now one of the three note-issuing banks in Hong Kong. Headquartered in Hong Kong, Anshin Group focuses on blockchain games and digital entertainment and is the parent company of the metaverse game platform The Sandbox. Founded in 1925, Hong Kong Telecom Limited is one of the largest integrated telecommunications service providers in Hong Kong. Regarding the cooperation on stablecoins, Anshin Group said: Hong Kong Telecom will strive to explore how stablecoin innovations can support local and cross-border payments through the sandbox to bring greater benefits to consumers and merchants; Standard Chartered Bank will actively participate in the stablecoin issuer sandbox to explore how to support the flourishing of Hong Kong's digital asset ecosystem in the most effective way, and have a deep understanding of the opportunities and risks brought by the evolution of the stablecoin market to this ecosystem; and Anshin Group is committed to promoting the popularization and application of digital assets and applying blockchain-related technology solutions to physical assets and traditional economy.

Why Hong Kong is obsessed with stablecoins

It is better to unblock than to block

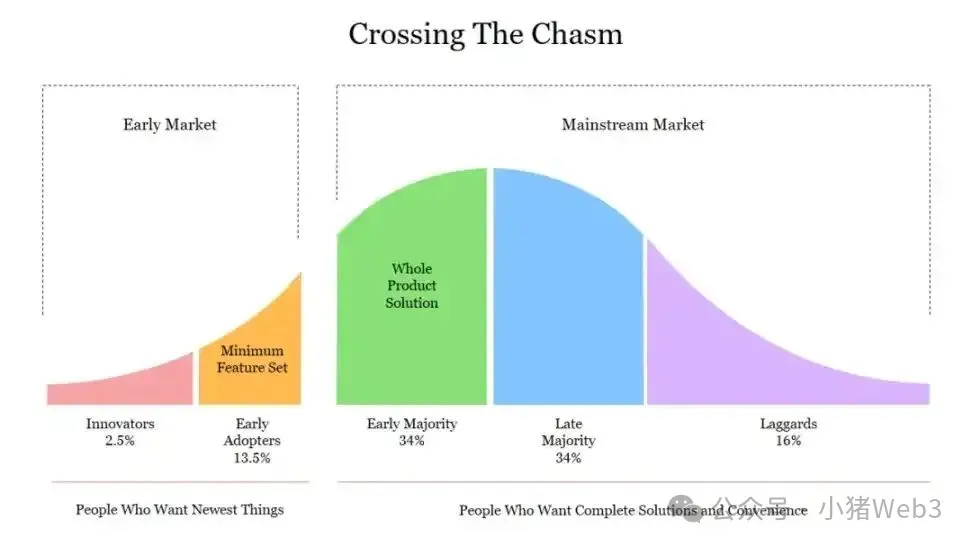

As of May 31, 2025, the total market value of cryptocurrencies is about 3.25 trillion US dollars, of which Bitcoin is about 2.07 trillion US dollars, and Bitcoin's market share is 63.7%. The high market share of Bitcoin shows the silence of the altcoin market. Geoffrey A. Moore's "Chasm Theory" may explain this phenomenon: there is a huge "chasm" between the early market and the mainstream market for high-tech products. Whether they can successfully cross the chasm and enter the mainstream market becomes the key to corporate growth.

Most mainstream altcoins actually represent the "innovative technology" of Web3. "Early adopters" are still a small circle of Web3 believers who agree more with the narrative of Web3. However, once they move towards "mainstream adopters" - a kind of pragmatists in the middle, the first problem they encounter is what specific problems the product can solve, and whether it can bring real value compared with the advantages of similar products (in Web2). Only when the product truly has more comprehensive advantages can it be adopted. However, it is difficult for altcoins to give an answer, because most of the scenarios described by altcoins do not exist at all, or exist under the premise of large-scale adoption of blockchain (this premise is not met at this stage), and naturally cannot bring real value.

However, the performance of stablecoins is completely opposite to that of altcoins, and the total market value has been hitting record highs. According to Coingecko data, the total market value of stablecoins has exceeded 250 billion US dollars, an increase of 70% compared with the same period last year. Among them, Tether (USDT) has a market value of more than 153 billion US dollars, accounting for about 61.2%, ranking first; USDC has a market value of more than 61 billion US dollars, ranking second.

Stablecoins are expected to be the first Web3 product to be accepted by "mainstream adopters". In the global payment field, stablecoins have become an important infrastructure. Although the current payment field is still dominated by intermediaries who control high fees, in fact, stablecoins have become the biggest disruptor in the payment field. In 2024, stablecoins processed $27.6 trillion in transaction volume, surpassing Visa and Mastercard. The number of active stablecoin wallet addresses increased from 22.8 million in February 2024 to more than 35 million in February 2025, an increase of 53%.

When this market has grown to a certain scale, from a regulatory perspective, it is better to "unblock than to block" - it is more effective to establish a clearer regulatory framework than to ban it completely.

The Arrow is on the String

Coincidentally, the U.S. Senate passed the procedural vote of the United States Stablecoin Innovation Guidance and Establishment Act of 2025 (GENIUS Act) by 66:32 on May 19.

The GENIUS Act is intended to establish a federal regulatory system, clarify the legal status of stablecoins, balance innovation and risk prevention, and strengthen the dominance of the U.S. dollar. Unlike the stablecoins defined in the Stablecoin Regulations, which can be anchored to any fiat currency (including Hong Kong dollars, U.S. dollars, etc.), the stablecoins defined in the GENIUS Act must be anchored to the U.S. dollar, emphasizing the dominant position of the U.S. dollar in global stablecoins. Here is a fact to add: in the crypto market, 99% of stablecoins are 1:1 anchored to the U.S. dollar, and the cryptocurrency trading ecosystem and decentralized finance (DeFi) platforms mainly use U.S. dollar stablecoins, which consolidates and expands the crypto hegemony of the U.S. dollar.

Although the GENIUS Act restricts the compliance of non-US dollar stablecoins in the United States, it does not restrict the compliance of US dollar stablecoins abroad, which in disguise stimulates the further reliance and use of US dollar stablecoins around the world. This undoubtedly poses a challenge to the legislation of stablecoins in other regions. If the anchoring degree with the US dollar stablecoin is too shallow, it will be out of touch with the actual market, but if the anchoring degree is too deep, it will quickly lose the financial market independence of its own stablecoin. Here is another fact to add: in some small and medium-sized countries with relatively weak sovereign currencies (such as Ghana and Nigeria), US dollar stablecoins have partially replaced the status of sovereign currencies among young people.

In summary, due to the overwhelming market advantage of the US dollar stablecoin, other fiat stablecoins will face higher transaction costs in actual applications, and the relatively relaxed regulatory policies reflected in the GENIUS Act will further impact the market of other fiat stablecoins.

Therefore, the rapid passage of the Stablecoin Bill in Hong Kong, China was also stimulated to a certain extent by the GENIUS Act. Regulatory agencies in countries such as Japan, Singapore and Dubai are also following up on relevant legislation. As the saying goes, "the arrow is on the string and has to be shot."

think

Does the crypto market need regulation?

From the perspective of a legislator, the answer to this question is that regulation is necessary. From the perspective of a Web3 researcher, the author will also come to the conclusion that a certain form of regulation is needed. The crypto market has been developing for fifteen years since the establishment of the first Bitcoin exchange Mt.Gox. The decentralization of blockchain has not brought an open, transparent and fair market environment. On the contrary, you can see almost all "securities" crimes in this market: illegal fundraising, false information disclosure, market manipulation, insider trading, and fraudulent issuance.

Because of the lack of supervision, financial crime is permitted. If financial crime is permitted, then not committing a crime becomes a crime. After all, there are only so many leeks, and if you don't cut them, others will. History goes round and round, and human nature remains unchanged. The unmanned sea hides sinister undercurrents, and the free order brings false promises.

However, regulation will bring three problems: the first is the issue of degree, the second is the issue of centralized power constraints, and the third is the issue of decentralized conflicts. The latter two issues will not be discussed in this article, and the main focus will be on the issue of the degree of regulation.

Generally speaking, the higher the degree of regulation, the higher the compliance cost of enterprises. Due to the decentralization of the crypto market, it is relatively easy to circumvent regulation if the enterprise is not large, and local users are more likely to freely choose external enterprises, so non-compliant enterprises can also grow wildly. If the compliance means of traditional finance are often expensive, slow, and restrictive, then in a market where compliant and non-compliant enterprises coexist, compliant enterprises must be the ones to be expelled. Hashkey's recent rumored predicament is partly due to the high compliance costs in Hong Kong.

Therefore, the degree of supervision must be the first thing that legislators in Hong Kong, China must think about: how to reduce the compliance costs of enterprises, help them establish competitive advantages, and ensure that supporting the development of crypto assets in Hong Kong does not become a slogan.

Does the Hong Kong dollar stablecoin have a future?

As mentioned above, 99% of stablecoins in the crypto market are US dollar stablecoins, so does the Hong Kong dollar stablecoin still have a chance?

Yes, because the stablecoin itself serves as a price anchor and is the basis for transaction pricing and liquidity. Therefore, the focus is on creating a Hong Kong dollar stablecoin trading scenario. Here we have to mention Hong Kong’s RWA strategic layout.

The so-called RWA is to represent and trade real-world assets in a tokenized way. Hong Kong itself has many high-quality assets, such as blue-chip stocks in Hong Kong stocks, and backed by mainland China, it can help mainland assets issue RWA in Hong Kong or overseas. At present, there are three successful cases of domestic assets issuing RWA in Hong Kong, which were completed by Ant Digits in cooperation with Longsun Technology, GCL Energy and Patrol Eagle Group. The underlying assets of the three cases are all mainland new energy assets.

In my opinion, Hong Kong Stablecoin and RWA are two-in-one, representing the capital side and the asset side respectively. When the asset side is high-quality and strong enough, sufficient funds will naturally flow into the capital side to match it. This is actually an important direction for the crypto market to move from virtual to real. Of course, what is emphasized here is that the underlying assets of RWA must be high-quality and the pricing must be reasonable, because RWA is a means of asset tokenization, and it will not change the original attributes of the underlying assets, let alone become a bargaining chip for speculation.

Therefore, the simultaneous development of RWA is also something that Hong Kong legislators need to think about. They should embrace stablecoins and abandon CBDC, attract sufficiently high-quality assets to be converted into RWAs, and establish an open, real-world crypto market.

Summarize

In this round of crypto market cycle, we can clearly see the huge changes in the perception and use of cryptocurrencies. Bitcoin is extremely strong as a store of value, while altcoins are sluggish as technological innovations. However, stablecoins have quietly become the infrastructure of global payments and are the target of legislation and supervision in various countries and regions, with Hong Kong, China being the first to bear the brunt.

Hong Kong, China, has transitioned from a regulatory sandbox environment to formal regulations, and launched the Stablecoin Ordinance to attract global capital and multiple stablecoin projects with an open and innovative attitude, consolidating Hong Kong's position as an international financial center and crypto asset hub. While responding to the "dollar hegemony" of the US "GENIUS Act", it also provided a sample for other governments.

However, the regulation of stablecoins will also bring more compliance costs to enterprises. Legislators in Hong Kong should balance the policy pressure on enterprises and the competitive environment of the market to support the development of crypto assets in Hong Kong. At the same time, RWA, as an important trading target for promoting the development of stablecoins, should also be actively promoted to establish an open and real-based crypto market.