Author: Bootly

The US government shutdown has officially ended, but the capital markets have not seen a rebound.

On Thursday local time, all three major U.S. stock indexes fell, with the Nasdaq down more than 2% and the S&P 500 closing down 1.3%; gold broke through a key support level.

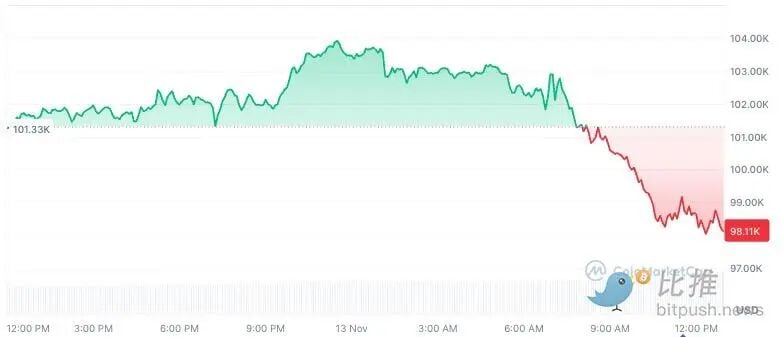

Bitcoin suffered a severe blow, falling to a low of $98,244 by the close of trading on the same day, the lowest point since early May. This was the third time this month that Bitcoin had fallen below the $100,000 mark.

Market sentiment has slipped from its highs and returned to the "extreme fear" zone.

This long-awaited "government resumption of operations" has failed to alleviate structural pressures in the market:

Tightening liquidity, concentrated selling by long-term holders, continuous outflows from ETFs, and a rapid cooling of expectations for interest rate cuts.

US trading session becomes the main driver of Bitcoin sell-offs: risk appetite plummets + liquidity tightens.

Bitcoin rebounded to around $104,000 during Asian trading hours, but weakened rapidly after entering the US trading session, and was quickly dumped below $100,000 in the afternoon, hitting a low of $98,000.

This trend is highly consistent with the simultaneous decline in US tech stocks:

- Nasdaq plunges

- Crypto-related stocks such as Coinbase and Robinhood declined.

- Mining stocks led the decline, with Bitdeer plunging 19%, Bitfarms falling 13%, and several other mining companies experiencing drops exceeding 10%.

The root cause is:

Expectations of interest rate cuts cooled rapidly → Risk assets were sold off across the board.

Last week, the market still believed that the probability of a rate cut in December was as high as 85%;

FedWatch now shows only 66.9%.

With future "cheap money" uncertain, Bitcoin's valuation is naturally difficult to sustain.

At the same time, the US Treasury is also withdrawing liquidity.

During the government shutdown, the federal budget recorded a surplus of approximately $19.8 billion, and the October surplus is likely to be even higher due to the large-scale shutdown. This means that the government has reduced its "injection" of funds into the market in the short term.

Analyst Mel Mattison described it as:

"This is the driest fiscal liquidity environment in months or even years."

With fiscal constraints and a cooling monetary policy, the US market has become the dominant force driving the recent Bitcoin plunge.

However, Mattison also pointed out that fiscal austerity is only a short-term phenomenon:

"With the fiscal floodgates about to reopen, the Trump administration must ramp up stimulus before the midterm elections."

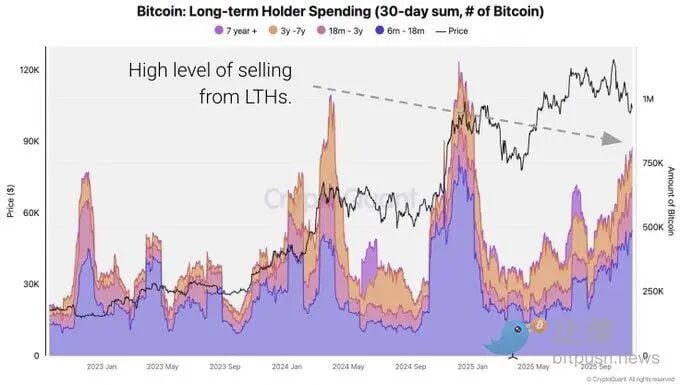

On-chain selling pressure was concentrated: LTH profit-taking combined with whale selling.

The recent drop in Bitcoin below $100,000 was not caused by panic among retail investors, but rather by a typical structural adjustment resulting from the simultaneous reduction of holdings by medium- and long-term funds on the blockchain.

CryptoQuant data shows that long-term holders (LTH) sold a total of approximately 815,000 BTC in the past 30 days, marking the largest sell-off since January 2024. On November 7th, approximately $3 billion worth of Bitcoin was sold for profit, indicating that a large number of low-cost Bitcoins chose to realize gains at that price level.

Similar profit-taking pressure occurred in the middle of the bull markets of 2020 and 2021, often corresponding to a period of adjustment.

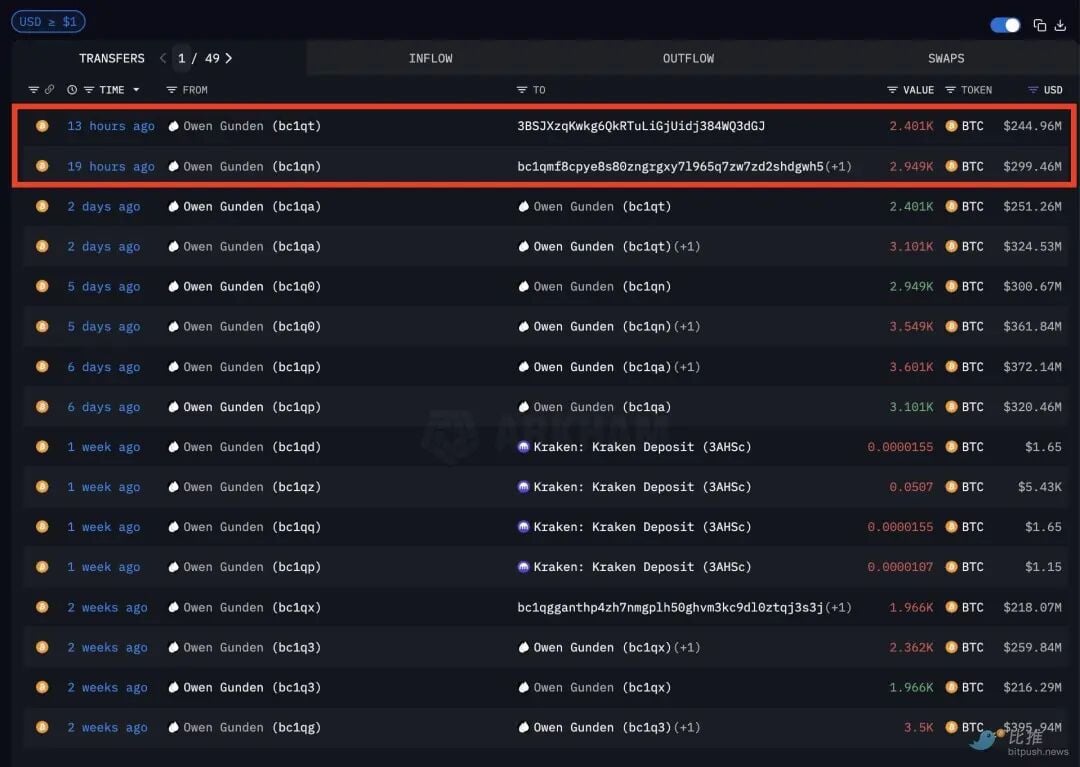

At the same time, whale behavior increased significantly, accelerating the downward pressure.

Arkham tracked down:

- Early Bitcoin whale Owen Gunden sold approximately $290 million worth of Bitcoin in a single day, but still holds $250 million in assets;

- A Satoshi-era whale who had held cryptocurrency for nearly 15 years sold off approximately $1.5 billion worth of its holdings last week.

- In October, the large address 195DJ also sold a total of 13,004 BTC and continued to transfer tokens to exchanges.

This means:

LTH profit-taking + whales concentrating their holdings → creating extremely strong selling pressure in the short term.

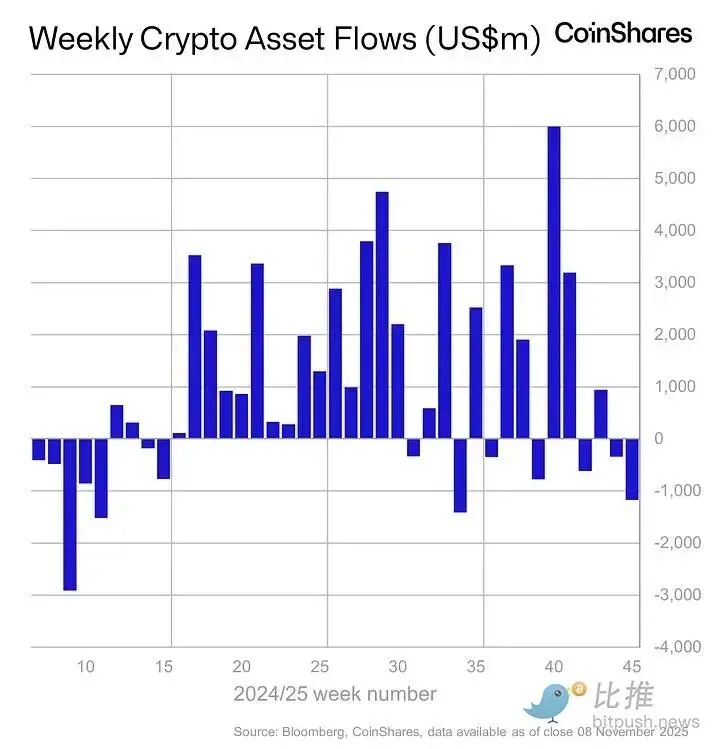

ETF/ETP funds continue to flow out, with the US market under the heaviest pressure.

According to a CoinShares report, global digital asset investment products have seen significant capital outflows for the second consecutive week, with a net outflow of $1.17 billion last week.

Most of the capital flight occurred in the US market, with outflows reaching $1.22 billion, while the European market (Germany and Switzerland) still recorded a net inflow of approximately $90 million, showing a clear divergence.

Bitcoin and Ethereum are the main battlegrounds for this round of capital withdrawal.

- Bitcoin products saw a net outflow of $932 million.

- Ethereum products saw a net outflow of $438 million.

- During the same period, shorting Bitcoin products recorded a net inflow of $11.8 million, the highest level since May 2025.

ETFs contributed significantly to Bitcoin's upward momentum in 2025, and when this buying activity stalled and turned into outflows, prices naturally came under pressure.

Can it reach a new high this year?

Bitcoin is currently hovering below its 365-day moving average. CryptoQuant views this as a key trend support level for the current bull market: once it returns above the moving average, the price is expected to strengthen again; if it continues to be under pressure, a mid-term pullback similar to that of September 2021 may occur.

The Fear & Greed Index has fallen to 15 (extreme fear), which is highly similar to the deep shakeout phases in the middle of past bull markets.

Based on a comprehensive analysis of macroeconomic, on-chain, ETF, and technical signals, the likelihood of breaking the $126,000 mark this year has significantly decreased.

Bitcoin is more likely to fluctuate between $95,000 and $110,000 before the end of the year.

To achieve a strong breakthrough, three conditions must be met:

- ETFs resume net inflows

- US fiscal stimulus has been clearly implemented.

- US Treasury yields fell and dollar liquidity improved.

However, judging from the policy pace, these three factors are more likely to appear simultaneously in early 2026, rather than at the end of 2025.

Looking ahead to 2026: Liquidity and cycles may resonate.

Despite short-term pressure, Bitcoin's medium- to long-term trend remains solid.

2026 may even become the core year of this cycle.

① Macro liquidity is expected to see a genuine shift.

With the economy slowing and employment weakening, the probability of the Federal Reserve entering a substantial rate-cutting cycle in 2026–2027 is increasing.

② The expansion of institutional participation in ETFs will bring about larger-scale buying.

The strength of institutional buying in ETFs in 2025 has been proven.

Against the backdrop of an interest rate cut cycle, long-term funds such as pension funds, global asset management firms, and RIAs will enter the market deeply through ETFs, reshaping the valuation system.

③2026 is the "second year after the halving": the strongest window of opportunity in history.

2013, 2017, 2021

All three cycles reached new highs in the "second year of the halving".

Based on this, we determine the range for 2026 as follows:

- Baseline target: $160,000 – $240,000

- Strong scenario: $260,000 – $320,000

This round of decline is more like a deep shakeout in the middle of a bull market than a trend reversal.

What will truly determine the next peak for Bitcoin will be the convergence of macroeconomic factors and institutional funding in 2026.