Key points:

The problem with the digital yuan has never been that it "chose the wrong path," but rather that its application space was limited by its M0 (money supply) positioning. While adhering to the fundamental principle of central bank issuance and sovereign backing, DC/EP (Digital Currency/Electronic Payment) has in the past been more like a project with a "correct system but restrained product development."

The shift from M0 to M1 is not a negation of the past, but a necessary paradigm shift: allowing the digital yuan to truly enter high-frequency scenarios, asset selection, and market mechanisms for the first time.

More importantly, the real challenge lies not in technology or compliance, but in whether we dare to leave enough room for market exploration under controllable conditions. If the digital yuan can only rely on subsidies and administrative promotion, it will never be able to form a network effect; only by learning to coexist with the market can it "run" like a real currency.

This is the most noteworthy underlying story behind the M1.

This article was written by Spinach's good friend, Beilong, who was involved in early CBDC-related work.

1. Don't rush to take sides: This isn't a debate about which path to take, but rather a difference in stage of development.

If we only look at the results, many people will draw a simple and crude conclusion: stablecoins have achieved scale and product-market fit (PMF), while the digital yuan is still lukewarm—does that mean that China chose the wrong path from the beginning?

This judgment was made too early and too hastily.

First, we must acknowledge a premise: China and the West have never been competing on the same track when it comes to digital currencies. The capitalist system, represented by the United States, tends to leave monetary innovation to the market—stablecoins are issued by commercial institutions, circulate freely on-chain, and are continuously tested and refined through DeFi, exchanges, and payment scenarios to first generate demand, and then regulators manage the risks.

China, however, chose a different path: the central bank directly promoted CBDC. Under this path, sovereign credit, financial stability, and systemic security are given top priority, with innovation itself taking a backseat to stability.

These two paths address different problems and are destined to present completely different development paces.

Looking back today, stablecoins have indeed succeeded, but their success is essentially a success of market mechanisms. The slow progress of the digital yuan, however, does not equate to failure; it is more like a result of deliberately slowing down the process under institutional constraints. Allowing a digital currency backed by a central bank and possessing the highest credit rating to expand entirely in a market-driven manner on-chain from the outset would obviously create systemic risks that no financial regulator could easily bear.

Therefore, there is no simple comparison of "which is more advanced" here, but rather the order of development is determined by the choice of system.

For ordinary users and entrepreneurs, here is a conclusion that is often overlooked but extremely crucial: Don't get hung up on "which path is right," because that's not something you can choose. The "path" is given by the system; what you can really do is use the "method"—within the established framework, make the product more user-friendly, uncover real needs, and allow money to truly enter high-frequency scenarios.

It is in this sense that today's discussion on the digital yuan moving from M0 to M1 is not about overturning the original path, but about acknowledging a reality: if we only focus on the "correctness of the path" but fail to implement it in practice, even the most correct approach will not yield results.

This round of changes does not indicate a change in direction, but rather a phase shift: the route has not changed, but the gameplay has begun to change.

2. Why it must have been M0 back then: Theoretically correct, but it locked the product into low-frequency demand.

If we were to evaluate the biggest "original sin" of DC/EP (Digital Currency Electronic Payment, specifically referring to China's CBDC) in its early stages, many would point the finger at the technology selection, the pace of implementation, or even conspiratorially attribute it to "conservatism." But the real answer is actually quite the opposite: the reason why DC/EP was strictly positioned as M0 from the beginning was not because of conservatism, but because the theoretical judgment at the time was too rigorous.

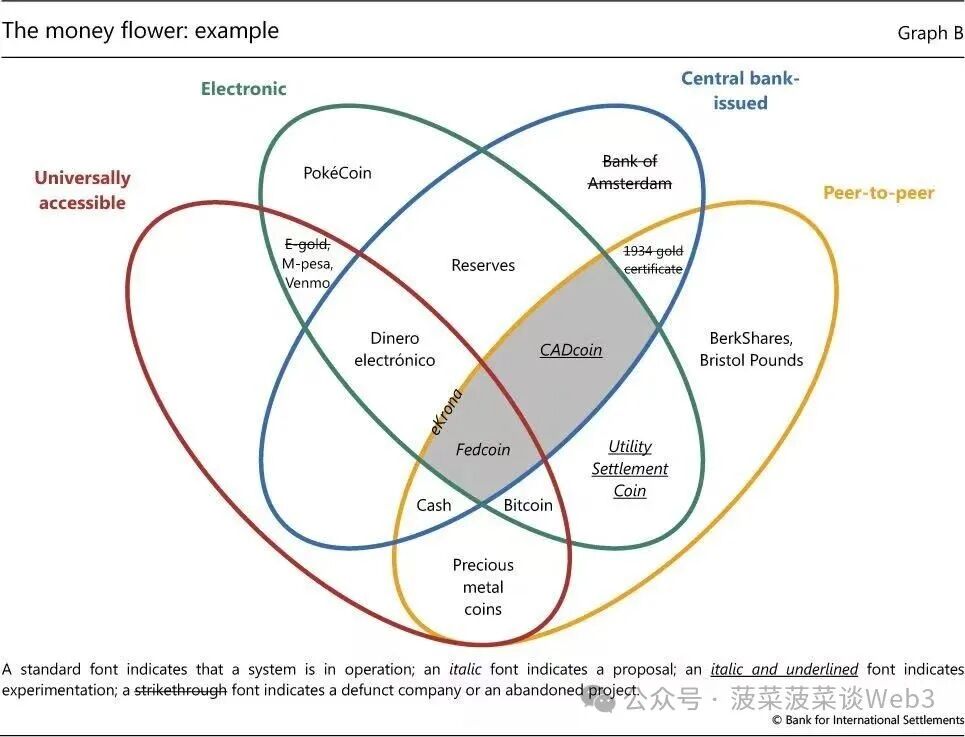

During the project initiation and design phases of the digital yuan, the core theoretical framework referenced by the People's Bank of China was the "Money Flower" analytical framework proposed by the BIS (Bank for International Settlements) in several of its studies. In articles such as Quarterly Review, the BIS points out that currencies can be systematically classified from dimensions such as the issuing entity, whether they are digitalized, whether they are account-based, and whether they are open to the public. A highly convincing conclusion is that among all mainstream forms of currency, only cash has not yet been truly digitized.

Deposits, transfers, and payment accounts have already been digitized within the banking system and internet platforms; the balances in Alipay and WeChat are essentially a technological extension of commercial bank deposits. Against this backdrop, the central bank's judgment is very clear: there is no need to reinvent the wheel. The mission of the digital yuan should be to fill the last gap in the supply chain—cash—rather than to replace the already highly mature electronic payment system.

Guided by this M0 positioning, the product design logic of DC/EP naturally points to "digital cash." Its focus is not on "how to better manage finances" or "how to participate in the financial market more efficiently," but rather on ensuring the continued usability of a digital currency backed by the central bank under various complex and even extreme environments.

Therefore, we see that DC/EP in practice emphasizes capabilities such as "dual offline payment"—that is, the ability to complete peer-to-peer value transfer even without network access or real-time account verification. This type of design is technically complex, but it does indeed solve some scenarios that traditional electronic payments cannot cover, such as those with limited network access, weak infrastructure, or special emergency environments.

The problem is that these scenarios are inherently low-frequency scenarios.

When internet payments can be completed with minimal friction in most places and at most times, a digital currency product that prioritizes "safety net" and "resilient design" is unlikely to naturally become a part of ordinary users' daily lives. Users won't voluntarily change their established payment habits just because it "works in extreme situations."

In other words, the theory of M0 is valid, and the design is self-consistent, but it inherently locks DC/EP into an "important but not high-frequency" position. This is not a product failure, but rather a positioning that makes it difficult to quickly achieve product-to-market fit (PMF).

Here's a little anecdote from back then.

In the early stages of the DC/EP rollout, I chatted with a friend from Tencent about the digital yuan. His assessment was very direct, even a bit playful: "They (referring to DC/EP) pose no threat to us whatsoever."

This statement is not a dismissive one, but rather an extremely calm assessment. From the perspective of an internet payment platform, a product strictly positioned as M0, primarily addressing the issue of cash digitization, would not directly touch upon the "core battlegrounds" of high-frequency payments, account systems, and user stickiness.

For this reason, for a long time, there was no truly direct competition between the digital yuan and the mainstream internet payment system.

This is precisely the starting point for subsequent reflection: when the digital yuan is only allowed to "work like cash," it has indeed fulfilled its mission; but if it is hoped that it will "be used like money," then simply defining it as M0 is clearly not enough.

3. It must be clarified that CBDCs and stablecoins are not the same type of currency.

Let's start with the conclusion: regardless of technological changes, the issuer of DC/EP can only be the central bank itself. This is not a strategic choice, but a fundamental institutional premise. Precisely because of this, CBDC and stablecoins are never "competitive in their own right," but rather different forms of currency under two different credit systems.

Many discussions about why the digital yuan is not as flexible as stablecoins actually confuse the issue from the outset. The reason why stablecoins can expand rapidly and frequently experiment is that they are essentially commercial currencies issued by commercial institutions: backed by enterprises, bearing commercial credit risk, and competing in the market to gain usage scenarios and liquidity.

In contrast, CBDC remains a credit money issued by the central bank, incurred by the central bank, and backed by sovereign credit. From a monetary perspective, this implies greater security and certainty; however, from a product perspective, it also means it must be subject to stricter boundary constraints. Any "overly aggressive" design could be amplified into systemic financial risk.

This is why stablecoins can be freely combined on-chain, embedded in DeFi, and participate in leverage and market making; while CBDCs have chosen caution and restraint for a considerable period. This is not a difference in technological capabilities, but an inevitable result of different credit responsibilities.

This is where things really start to get interesting: what happens when the highest-credit-rating form of currency begins to try to learn from market mechanisms?

From this perspective, the significance of M1 is not just whether it can accrue interest, but whether it provides a new possible path for CBDC—introducing an incentive structure that is closer to market demand without changing the issuing entity or sacrificing legal tender status.

In other words, the real question is not whether CBDC will replace stablecoins, but whether, while maintaining the sovereign credit base, CBDC can catch up with or even partially surpass stablecoins in terms of flexibility and usability.

This is the most noteworthy underlying trend behind the shift from M0 to M1.

4. From M0 to M1: The Digital Yuan Enters the "Asset Selection" Stage for the First Time

To summarize: Only when the digital yuan is allowed to enter M1 will it have its first opportunity to transform from a "payment instrument" into a currency that users will actively hold.

Under the M0 framework, DC/EP is more like a digital alternative to cash. The core value of cash lies in settlement and payment, not in "holding". You won't take more cash because of the cash itself; cash is merely a medium for completing transactions. Therefore, when the digital yuan is strictly limited to M0, it is inherently difficult to change user behavior—users will only use it when they are "needed", not when they have a "choice".

The introduction of M1 changed this premise for the first time.

M1 represents demand money: it can be held, participate in a wider range of financial activities, and has basic yield attributes. Even if this yield is very limited, it still has a decisive impact on user behavior. Because for the vast majority of users, what is truly unacceptable is not "low yield," but "no yield at all."

It is precisely at this point that the digital yuan begins to have a potential crowding-out effect on existing forms of electronic currency. Alipay or WeChat balances are essentially efficient payment tools, but the balance itself does not bear "asset attributes"; however, once the digital yuan enters M1, even with meager returns, it will begin to have a reason to be held long-term.

It is important to note that this does not mean the digital yuan will replace money market funds or other wealth management products. On the contrary, the digital yuan in M1 is more likely to serve as a "foundation": high-frequency liquidity remains in M1, while enhanced returns are achieved through products such as MMFs. This tiered structure is not contradictory; rather, it better aligns with the fund management habits of real users.

From this perspective, the M1 is not a simple technological upgrade, but a fundamental change in product positioning:

- From "Do we have the capability to digitize cash?"

- Moving towards "whether or not we can participate in users' asset allocation decisions".

This step doesn't determine whether the digital yuan "can be used," but rather whether it's worth keeping.

5. Failure to report to the State Council: A severely underestimated signal

Conclusion first: The fact that no longer requiring special approval at the State Council level means that the digital yuan is shifting from a "major engineering project" to a more normalized financial infrastructure.

In the earlier stages, the digital yuan was promoted primarily through an engineering-based approach of "pilot-promotion-evaluation." This path was essential in the early stages, ensuring system security, controllable risks, and aligning with the central bank's consistent prudent principles. However, the costs were equally apparent: slow pace, limited application scenarios, and restricted room for innovation.

When the approval level changes, it essentially sends a signal: within the established institutional framework, more market players are allowed to participate, more application forms are allowed to emerge, and a certain degree of trial and error is also allowed.

Currency is never designed, but rather filtered through use. Only when the digital yuan gradually moves beyond the context of a "demonstration project" and enters the role of everyday financial infrastructure will it be able to truly thrive in high-frequency scenarios.

This change does not mean a relaxation of regulation, but rather a change in the way regulation is conducted: from strictly defining the path in advance to observing how the market self-organizes within the boundaries.

6. Chain Reaction: From Product Adjustment to Financial Structure Restructuring

The shift from M0 to M1 is not a single-point optimization, but a structural change that will continue to have an impact over the next few years.

6.1 The development path has been re-anchored: domestic CBDC, offshore stablecoins

A reality that is often overlooked but is gradually becoming clear is that China does not, and does not need to, choose between "CBDC or stablecoin".

Within the domestic system, promoting CBDC with the digital yuan at its core is the optimal solution for sovereign currency and financial stability; however, in offshore and cross-border scenarios, especially in highly market-oriented and international financial hubs like Hong Kong, preserving the issuance and application space for stablecoins is more practical.

This is not wavering, but rather a tiered governance approach:

- Domestically, CBDC will be used to solidify the digital foundation of sovereign currency;

- Offshore, using stablecoins and market mechanisms to connect with global liquidity.

6.2 Potential Squeeze on Traditional "Non-Interest-Generating Stablecoins"

Key takeaway: When sovereign credit currencies begin to possess M1 characteristics, the structural disadvantages of non-interest-bearing stablecoins will be gradually amplified.

The biggest advantages of stablecoins currently lie in their composability and liquidity, but on the "holding side," most stablecoins do not naturally generate interest. In contrast, once the digital yuan possesses basic yield attributes within the M1 framework, even with extremely low returns, it will create a significant difference in long-term capital allocation.

This doesn't mean stablecoins will be quickly replaced, but it does mean the competitive landscape has changed:

- In the past, the competition was about "whether it can be used";

- The future competition will be about "whether it's worth holding onto for the long term".

6.3 The relationship between the central bank and commercial banks has entered a more complex phase.

This is the most complex and the most difficult impact to avoid.

As the digital yuan becomes closer to M1, it essentially means that the central bank is beginning to confront public liabilities more directly. This change will inevitably touch upon the traditional division of labor between the central bank and commercial banks.

In the existing system, commercial banks play a core role in accounts, deposits, and customer relationships. However, as central bank digital currencies continue to strengthen their account and profit attributes, how to avoid creating a "siphoning effect" on the commercial banking system becomes a problem that must be addressed.

It is against this backdrop that the institutional framework surrounding the digital yuan will inevitably touch upon more fundamental legal issues—such as the definition of the central bank's functions, debt structure, and public relations in the Central Bank Law.

The "loose boundary" advantage of 6.4 USDT/USDC, and the reality that CBDC must face.

An undeniable fact is that the reason USDT and USDC are widely used globally is not simply because they are "pegged to the US dollar," but because they have chosen a path that is extremely market-oriented between anonymity and controllability.

In actual operation, USDT and USDC naturally possess strong "anonymity-like" characteristics at the on-chain level:

- The address serves as the account; binding to a real-world identity is not mandatory.

- Transferring funds has virtually no barriers to entry and can be embedded in various contracts and agreements;

- As long as the contract allows, it can be used in a wide variety of scenarios such as trading, staking, liquidation, and market making.

At the same time, they are not entirely out of control. Through smart contract permissions, freezing of issuer addresses, and cooperation with regulatory enforcement, stablecoins still possess the ability to intervene and recover assets "when necessary." However, it is important to emphasize that this level of control is deliberately extremely lenient, and occurs more after the fact than before.

It is precisely this "extremely loose, but not zero" design that has given the market enormous room for exploration. A large number of DeFi, cross-border settlements, and gray-area but real demands have been discovered, validated, and amplified in this relaxed environment.

This, in turn, raises an unavoidable question: if CBDC remains in a state of highly upfront control, strong identity binding, and strong scenario limitations, then it will be difficult for it to truly compete with stablecoins in terms of application exploration.

Therefore, the real challenge in shifting from M0 to M1 lies not only in whether it generates interest, but also in whether the central bank digital currency is willing and able to break through overly conservative usage boundaries, provided that risks are controllable.

This is not about replicating the path of USDT or USDC, but about answering a more realistic question: while maintaining legal tender status and sovereign credit, can CBDC leave enough "room for exploration" for the market?

Only by taking a substantial step on this issue can the digital yuan truly enter those scenarios that are still dominated by stablecoins today.

6.5 Application scenarios are systematically opened up

When the digital yuan is no longer just a "payment demonstration" or "cash replacement," but enters the M1 system, its potential application scenarios will be systematically unlocked:

- Wages, subsidies and other public payments

- Cross-institutional and cross-system settlement

- Deep integration with financial products and contract-based payments

These scenarios will not emerge overnight, but they determine that the digital yuan is no longer just a "sample showcasing technological capabilities," but will truly enter the main process of financial operations.

7. A direction worth serious discussion: the "dual-track design" of onshore and offshore digital yuan.

Let's start by stating the core judgment: If we want the digital yuan to truly "take off" globally, it may be necessary to clearly distinguish between "onshore digital yuan" and "offshore digital yuan" in the institutional design.

This is not radical innovation, but a realistic choice.

The onshore digital yuan will continue to serve the domestic financial system, and its core objectives remain manageable, controllable, and traceable. Through a tiered account system, real-name registration requirements, and scenario limitations, it ensures that the fundamental premises of anti-money laundering, counter-terrorism financing, and financial stability are not shaken. This logic is necessary and reasonable in the domestic environment.

However, the problem is that if the same constraints are replicated unchanged in cross-border and offshore scenarios, it will be almost impossible for the digital yuan to generate real momentum for international use.

In contrast, a key reason why USDT and USDC have been able to spread rapidly in overseas markets is that they offer stronger anonymity by default: the address is the account, and identity is not pre-linked; regulation and intervention occur more after the fact than before. This design does not encourage violations, but rather leaves ample room for market exploration.

Following this logic, one proposal worth serious discussion is to introduce stronger, mathematically provable anonymity for the offshore digital yuan.

The anonymity mentioned here is not entirely uncontrollable, but rather achieves "selective disclosure" and "conditional traceability" through cryptographic means:

- In daily transactions, users do not need to reveal their full identity;

- Traceability can be restored through compliance procedures when specific legal conditions are triggered.

- The control logic has shifted from "comprehensive pre-emptive" to "limited pre-emptive + ex-post intervention".

This design will make the offshore digital yuan more functionally similar to a stablecoin, while maintaining the credit rating of a sovereign currency. This is precisely what no current commercial stablecoin can offer.

From a strategic perspective, this "dual-track design" will not weaken domestic regulation; on the contrary, it may lead to a clear division of labor.

- Onshore, the digital yuan continues to serve as a financial infrastructure and policy tool;

- Offshore, the digital yuan assumes the roles of "international settlement currency" and "export of digital form of yuan".

If this idea can be implemented, then the digital yuan will no longer be just an upgrade of the domestic payment system, but may become a key tool in the process of RMB internationalization.

This is not a risk at all; on the contrary, it could be a truly “great thing”.

8. The real challenge is not "whether or not," but "whether or not we dare to let the market run its course."

Let's state the conclusion clearly first: the biggest challenge facing the digital yuan is not in terms of technology or institutional legitimacy, but rather in whether it is willing to allow sufficient freedom to the market under controllable conditions.

Looking back at the development path of stablecoins, an often overlooked but extremely important fact is that the success of USDT and USDC was not "planned," but rather emerged gradually from a series of imperfect and even gray-area uses by the market. Cross-border transfers, on-chain transactions, DeFi staking, settlement intermediaries... almost none of these scenarios were "approved for use in this way" by regulatory authorities in advance, but they grew naturally from real demand.

In contrast, if the digital yuan continues to rely primarily on subsidies, administrative promotion, or demonstration projects to expand its use cases, it will be difficult to create a genuine network effect, no matter how advanced the technology or how high its credit rating. Once a currency fails to create a network effect, it will forever remain "required to use" rather than "actively chosen."

This is why the real dividing line is not whether or not to uphold legal tender status. Legal tender status is the bottom line, not an obstacle. The real challenge lies in whether, while upholding legal tender status, we can accept a more market-oriented approach to exploration, allowing some applications to emerge before the rules, and then for the rules to absorb and regulate them.

In this sense, the "dual-track design" of onshore and offshore regulation is not a weakening of supervision, but a more refined risk stratification:

- High-risk, exploratory demands will be tested within the offshore system.

- Highly certain and stable demands will continue to operate within the onshore system.

This is not laissez-faire, but a conscious choice to allow for mistakes in innovation.

If the digital yuan in the M0 phase addressed the question of whether the central bank could issue digital currency, then starting with M1, the real issue becomes: can a digital currency issued by the central bank learn how to coexist with the market without spiraling out of control?

There is no ready-made answer to this step, nor can it be accomplished overnight. But what is certain is that if this step is not taken, the digital yuan will forever remain a "safety cornerstone" in the financial system, and will hardly become a truly circulating currency in the global system.

In conclusion: It's not that the route was wrong, but rather that we've finally reached the stage where we should "run freely."

Returning to the original question: Why did the digital yuan seem "lukewarm" in the past?

The answer may not be complicated—it is locked in an overly restrained position by the correct theory of M0.

Today, the shift from M0 to M1, from engineering-driven advancement to infrastructure-based operation, and from a singular domestic logic to a dual design encompassing both onshore and offshore aspects, sends a very clear signal:

The route hasn't changed, but the stage has.

Next, the real question that the digital yuan needs to answer is no longer whether it is "legal," but rather:

Can it truly learn to work like money, while maintaining sovereign credit and financial stability?