Author: Deng Tong, Jinse Finance

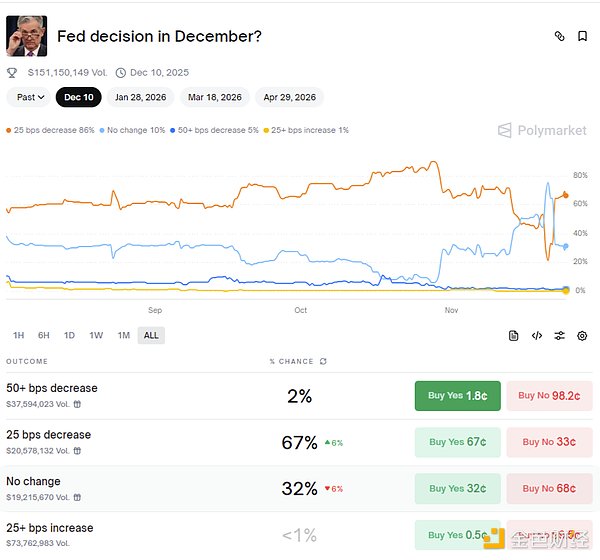

On November 21, according to CME's FedWatch Tool, the probability of the Federal Reserve cutting interest rates by 25 basis points in December was 39.6%, while the probability of keeping rates unchanged was 60.4%. That day, Federal Reserve Vice Chairman and New York Fed President Williams stated that the Fed could cut rates "in the near future" without jeopardizing its inflation target. Influenced by these remarks, Polymarket's forecast of a 25 basis point rate cut in December rose to 61%. Today, according to CME's FedWatch Tool, the probability of a 25 basis point rate cut in December has risen to 69.4%, while the probability of keeping rates unchanged is 30.6%.

Prior to Williams' speech, the price of BTC had been steadily declining, even touching $82,000. After the rate cut comments were made, the price of BTC began a slow recovery, reaching $87,067.46 at the time of writing.

White House economic advisor Hassett pointed out that the new leadership of the Federal Reserve may cut interest rates, Trump may interview Fed candidates in the coming months, and we may determine the Fed chair around the New Year. The market is currently focused on the Fed's FOMC meeting.

I. Voting Mechanism of the Federal Reserve FOMC Meetings

The Federal Open Market Committee (FOMC) of the Federal Reserve makes decisions using a majority vote system, with each voting member having an equal vote. The committee has 12 voting members, consisting of two groups: permanent voting members and rotating voting members.

- All members of the council (maximum of seven);

- President of the Federal Reserve Bank of New York;

- Of the remaining 11 Reserve Bank governors, four serve on a rotating basis, with each governor serving a one-year term.

All seven Federal Reserve Bank presidents, who do not have voting rights, attend Federal Open Market Committee meetings and participate in the committee's discussions.

Voting mechanism

- Majority vote: At the end of each two-day meeting, participants vote on monetary policy proposals (such as whether to adjust the target range for the federal funds rate), and the proposal that receives a majority of votes is adopted.

- Consensus: Despite the existence of a voting mechanism, FOMC members typically engage in extensive discussions and consultations to seek consensus, ensuring that policy decisions have broad support and thus send a consistent message to the market.

- Record of dissent: If a member with voting rights disagrees with the final decision, their dissent will be formally recorded in the meeting minutes, which demonstrates the diversity of opinions within the committee.

Jeffrey Roach, chief economist at LPL Financial, said: "In reality, committee members communicate closely during breaks in meetings to try to reach a consensus, but this does not guarantee that a consensus will be reached."

Achieving consensus among all Federal Reserve members helps send a message to the market that Fed officials are united in their views on the matter. Conversely, a divergent vote could raise questions about the Fed's belief in the correctness of its actions and the motivations of its officials.

II. Voting Members and Their Preferences for the 2025 FOMC

Permanent voting members (Members of the Federal Reserve Board of Governors and President of the Federal Reserve Bank of New York)

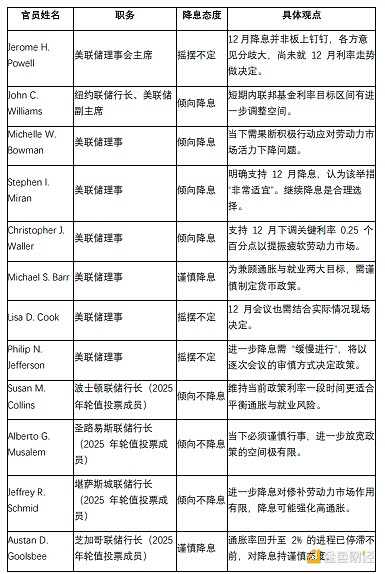

Jerome H. Powell, Chairman (Federal Reserve Board): Wavering

On October 29, at the press conference following the Federal Reserve's decision to cut interest rates by 25 basis points, Powell stated that the rate cuts might not necessarily continue into December as widely predicted. "Further rate cuts at the December meeting are not a done deal, far from it. There is a great deal of disagreement today. Therefore, we have not yet made a decision on the direction of interest rates in December." Powell acknowledged the Fed's difficult situation, stating that economic trends are pulling monetary policy in the opposite direction. "We are now facing upside risks to inflation and downside risks to employment. We only have one tool…you can't deal with both problems at the same time."

John C. Williams, Vice Chairman (President of the Federal Reserve Bank of New York): Leaning towards interest rate cuts

Speaking at a meeting of the Central Bank of Chile, Williams said that U.S. interest rates could fall without jeopardizing the Federal Reserve's inflation target, while also helping to prevent a decline in the job market. "I think monetary policy will tighten slightly…so I think there is still room for further adjustments to the target range for the federal funds rate in the near term to bring the policy stance closer to the neutral range," Williams said. He added that the Fed needs to achieve its inflation target without "excessively jeopardizing its goal of full employment."

Michelle W. Bowman, Federal Reserve Governor: Leaning towards interest rate cuts

Speaking after the Federal Open Market Committee (FOMC) decided to cut interest rates for the first time since 2025 in September, Bowman said, "Now is the time for the Committee to take decisive and aggressive action to address signs of declining labor market activity and fragility. We are likely already behind the times in addressing the deteriorating labor market conditions."

Stephen I. Miran, Federal Reserve Governor: Leaning towards interest rate cuts

Milan explicitly supports a December rate cut, deeming it "very appropriate." On November 15th, he emphasized that data since September had been generally dovish, supporting a more dovish stance from the Federal Reserve. Earlier, he had suggested a 50-basis-point cut, or at least a 25-basis-point cut. He believes that continued rate cuts are a "consistent and reasonable choice" if economic data remains largely unchanged. Milan, a former White House chief economic advisor appointed by Trump, has faced scrutiny regarding his independence—his aggressive stance has exacerbated divisions within the Federal Reserve.

Christopher J. Waller, Federal Reserve Governor: Leaning towards interest rate cuts

On November 17, Waller stated that he supports another 0.25 percentage point cut in the key U.S. interest rate in December to help boost the weak U.S. labor market—and he doubts he will change his mind. Waller said that based on surveys of consumers and businesses, as well as his own contacts with large employers, he is convinced that labor market conditions have deteriorated. He pointed out that key employment data, delayed due to the record 43-day government shutdown, is likely to show the opposite once released. “The labor market remains weak, near stagnation.” Meanwhile, inflation has not risen significantly in recent months. He stated that the economic slowdown and high interest rates have dampened consumer spending, thus helping to control inflation. “Given signs of slowing economic growth, and the possibility that a weak labor market could lead to modest wage growth, I don’t see anything that could cause inflation to accelerate.”

Michael S. Barr, Federal Reserve Governor: Cautious Rate Cuts

On November 20, Michael Barr stated, "I am concerned that inflation is still around 3%, while our target is 2%. So we need to be cautious with monetary policy now, as we want to ensure we achieve both ends of our mission."

Lisa D. Cook, Federal Reserve Governor: Uncertain

In an interview with the Brookings Institution in Washington, Cook stated, "At each meeting, I determine my monetary policy stance based on the latest data from various sources, changes in my expectations, and the balance of risks. Every meeting, including the December meeting, has been an in-person meeting."

Philip N. Jefferson, Federal Reserve Governor: Uncertain

On November 17, Jefferson noted that as the Federal Reserve has eased policy to a point where the slowdown in inflation may have stalled, it needs to proceed "slowly" on further rate cuts. "In recent months, I think the balance of risks in the economy has shifted, with downside risks to employment increasing relative to upside risks to inflation, while upside risks to inflation may have recently decreased." Jefferson will be data-driven and will adopt a "meeting-by-meeting" approach to policy decisions. "At this point in time, this is a particularly prudent approach." Before the December Fed policy meeting, "it remains unclear how much official data we can expect."

Rotating voting members in 2025 (Regional Federal Reserve Presidents)

Susan M. Collins, President of the Boston Federal Reserve: Inclined to not cut interest rates

On November 12, Collins stated that due to concerns about high inflation, she considered the threshold for further monetary easing in the near term to be "relatively high." "I would not easily ease policy without clear evidence of a deteriorating labor market, especially given the limited inflation information resulting from the government shutdown. In the current highly uncertain environment, maintaining the policy rate at its current level for some time may be appropriate to balance inflation and employment risks."

Alberto G. Musalem, President of the Federal Reserve Bank of St. Louis: Inclined to not cut interest rates

On November 10, Mussalem expressed clear skepticism about the prospect of further monetary easing. In a media interview, he stated, "It is crucial that we proceed with caution at this moment. I believe there is very limited room for further easing without making policy overly loose." Mussalem believes that current inflation is closer to 3%, rather than the Fed's 2% target. He added that financial conditions, including stock valuations and housing prices, are already high; monetary policy is closer to neutral than mildly restrictive; and the labor market has cooled in an orderly manner. "I think we need to continue taking measures to curb inflation."

Jeffrey R. Schmid, President of the Kansas City Federal Reserve: Inclined to hold off on rate cuts

On November 14, Schmid stated that further rate cuts might play a greater role in reinforcing high inflation than in supporting the labor market: "I don't think further rate cuts will do much to mend the cracks in the labor market—those pressures are more likely to come from structural changes in technology and immigration policies. However, rate cuts could have a more lasting effect on inflation because it would raise increasing questions about our commitment to the 2% inflation target." This reasoning is guiding his thinking for the upcoming December Fed policy meeting, and he added that he remains open to new information in the coming weeks.

Austan D. Goolsbee, President of the Federal Reserve Bank of Chicago: Cautious Interest Rate Cuts

Goolsby stated at an event hosted by the Indianapolis Institute of Financial Analysts that the process of inflation returning to 2% "seems to have stalled." "This makes me a little uneasy."

In summary, four of the 12 voters clearly favored a rate cut, while the other eight were undecided or opposed to a rate cut.

III. External Expectations for a Federal Reserve Rate Cut in December

- Barclays research points out that uncertainty remains surrounding the Federal Reserve's interest rate decision next month, but Chairman Powell is likely to push the FOMC to cut rates. Based on recent speeches, Barclays believes that Governors Milan, Bowman, and Waller are likely to support a rate cut, while regional Fed presidents Mussallem and Schmid prefer to keep rates unchanged. Recent statements from Governors Barr and Jefferson, as well as Goolsby and Collins, suggest their stance is not yet clear, but they lean towards maintaining the status quo. Governors Cook and Williams rely on data but appear to favor a rate cut. Barclays states, "This means that before considering Powell's position, there may be six voters who prefer to keep rates unchanged and five who prefer a rate cut." The bank adds that Powell will ultimately lead the decision, as the threshold for governors to publicly oppose his position is high.

- A research report from CITIC Securities states that New York Fed President Williams hinted at a further rate cut in December, reversing market expectations for a rate cut. Currently, the market believes there is a 70% probability of a Fed rate cut in December. The Fed will enter its blackout period on November 29th. Before this period, Powell has no scheduled public speeches or media interviews, and Williams' remarks may be the last Fed official statement to influence market expectations. Continuing the previous view, a "close call" rate cut of 25 basis points is expected in December. For the market, the reversal of rate cut expectations, coupled with the progress of the "28-point" plan and news of the Trump administration considering exporting H200 chips to China, means that macroeconomic factors are no longer a source of market pressure in the short term. The market may focus more on issues such as AI company bond issuance and cryptocurrency trends.

- Polymarket predicts the probability of a 25-basis-point rate cut by the Federal Reserve in December has risen to 67%.