Written by: Tantu Macroeconomics

1. There has been much discussion in the market about Warsh's initial actions upon taking office, with more interest rate cuts and more balance sheet reduction seemingly becoming the market consensus. However, we believe that neither interest rate policy (interest rate cuts) nor balance sheet policy (balance sheet reduction) is likely to substantially affect the original policy path in 2026.

2. First, there is the balance sheet policy: Currently, there are no objective conditions in the US money market for further or faster balance sheet reduction.

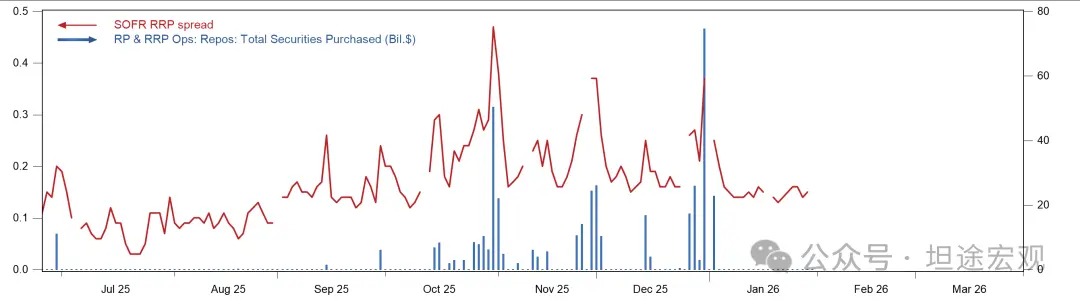

1) After Q4 2025, ONRRP usage essentially dropped to zero, the SOFR-ONRRP spread rose to a historical high of 25bps, and SRF usage remained consistently above zero. These signals indicate that the liquidity situation in the US interbank market has shifted from abundant to slightly tight. Dealer banks, hedge funds, and other overnight funding demanders have encountered difficulties in obtaining funding and high funding costs. This is why the Fed restarted technical balance sheet expansion (RMP) last December (Figure 1).

Figure 1: SOFR-ONRRP Spread vs. SRF Usage

2) Under these circumstances, abruptly stopping the RMP and restarting balance sheet reduction would, on the one hand, trigger a renewed liquidity "crisis" in the repo market and a surge in SOFR, and on the other hand, lead to a significant increase in SRF usage, which would not actually reduce the balance sheet much (when dealer banks use SRF, the Fed passively expands its balance sheet). In other words, forcibly reducing the balance sheet in the current environment would have no substantial impact other than causing liquidity problems in the repo market.

3) For the US interbank market to continue shrinking its balance sheet, or even return to the "scarcity reserve framework," the existing banking regulatory framework must be completely rewritten, including but not limited to Basel 3 (LCR), the Dodd-Frank Act (stress tests, RLAP), and even the self-regulatory constraints (LoLCR) that banks have developed over the past 20 years. This is far beyond the authority of the Federal Reserve Chairman (Dodd-Frank requires Congress, while banks' internal regulatory practices require slow adjustments by large banks).

4) The only thing Warsh can do at present is try to persuade the FOMC to reduce the monthly purchase amount of the Reserve Term Purchase (RMP), or to suspend the RMP when TGA declines significantly and reserves recover rapidly in the future. However, like any Fed voting member, preventing a liquidity crisis in the repo market is a prerequisite for Warsh's advocacy of slowing down the RMP. Considering that the RMP is a policy passed by a unanimous vote of the FOMC, a major rewrite is unlikely.

5) The potential impact will come with the next recession/crisis. If the Fed has already lowered its liquidity limit, but liquidity pressures remain severe and the economic recovery outlook remains poor, Warsh might be more inclined to end QE less or earlier, or start QT earlier. However, this highly depends on the depth of the crisis at that time, Warsh's own mindset (the mindset of an incumbent and an observer are completely different), and whether he is pragmatic enough. We need more time to observe him.

3. The second is interest rate policy: Warsh is unlikely to significantly change the outlook for the existing interest rate path.

1) The threshold for Warsh to significantly turn hawkish is very high. Currently, the US job market is still in a frozen state of "no jobs, no layoffs," and inflation data is still slowly moving towards 2%. In addition, he will most likely still need to "thank" Trump, so it is unlikely that he will significantly turn hawkish in 2026.

2) The threshold for a significant Warsh dovish shift (e.g., more than three rate cuts without significant changes in growth and inflation data) is also very high. On one hand, current interest rates are indeed near the neutral level, giving the Fed the right to "wait and see" and not rush into rate cuts. On the other hand, the unemployment rate is the FOMC's most important indicator in 2026. This is because, observing the past three State of the Economic Projections (SEPs), the FOMC's unemployment rate forecast for 2026 has consistently remained at 4.4-4.5%, meaning that the unemployment rate will be the FOMC's "soft target" in 2026. If the unemployment rate does not significantly exceed 4.5% in Q4 2026, the likelihood of convincing other voting members to support a significant rate cut is not high.

3) Historically, any new Fed president who is too close to the president will face rigorous scrutiny from other voting members, and any "foolish" actions will garner a large number of dissenting votes. One example is G. William Miller, the shortest-serving Fed president in 1978-1979. He was an ally of President Carter and insisted on not raising interest rates in a high-inflation environment, which led to attacks from FOMC voting members. In the end, he was promoted by Carter but demoted in reality and transferred.

4) There are two possibilities for the Warsh Fed to cut interest rates more significantly than expected. One is a substantial increase in the risk of recession, or a stock market crash. The other is a significant drop in inflation in 2026. Currently, the former seems unlikely, but if Trump removes tariffs in the second half of the year (in his bid for the midterm elections), a temporary decline in commodity CPI could provide the Warsh Fed with a brief window (excuse) for interest rate cuts.

4. Thirdly, the policy framework: Warsh may lack the flexibility and pragmatism of Powell.

1) Warsh has repeatedly expressed his opposition to data dependence and forward guidance, emphasizing trend dependence rather than data dependence. He believes the Federal Reserve should only adjust monetary policy when there is a "significant" deviation between employment and inflation targets, rather than responding to monthly reports (such as employment data), because monthly data is highly noisy and easily corrected later. He argues that the Fed should prioritize medium- to long-term economic trends over immediate data points, basing monetary policy on judgments of future economic cycle trends rather than recent economic data.

2) This approach is completely different from Powell's. Powell has always been known for his flexibility and pragmatism, with examples including the turnaround after the market crash in Q4 2018, the unprecedented market rescue in March 2020, the temporary decision to raise interest rates by 75bps during the blackout in June 2022, and the single decision to cut interest rates by 50bps in September 2024 based on a set of employment data, etc.

3) If Warsh's policy philosophy is truly as he has previously advocated, then his monetary policy will be more "rigid" and "subjective," objectively amplifying the volatility of the macroeconomy and the market.

In conclusion, it is expected that Warsh will not, and is unlikely to, immediately implement his policy of interest rate cuts and balance sheet reduction after taking office. He will need to coordinate with the economic and inflationary environment, the stance of FOMC voting members, and, at the same time, maintain his relationship with Trump as much as possible. For the market, whether Warsh is a sufficiently pragmatic, independent, and professional new Fed president remains to be seen over a considerable period of time.