Author: Balaji (Angel Investor, Former Coinbase CTO)

Compiled and edited by: BitpushNews

The era of tech mergers and acquisitions may be ending, but the era of crypto may just be beginning.

Because the combined effect of the new policies makes it more difficult for startups to exit through IPOs or mergers and acquisitions, but it has become easier to issue equity-backed security tokens (STOs) on the Internet. Why? This article will explain one by one:

1) IPOs become difficult

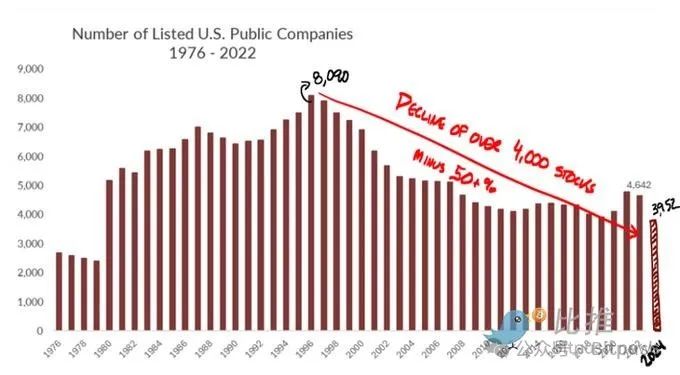

For decades, the SEC’s Sarbox rules made it cumbersome for small companies to go public. The rules were meant to prevent the next Enron, but they didn’t work (nor did they prevent the financial crisis). Yet they cut the number of public companies in the U.S. in half from their 1999 peak:

2) Mergers and acquisitions also become difficult

Therefore, starting in the mid-2000s, conventional wisdom held that tech companies should stay private longer. As IPOs became difficult, mergers and acquisitions became the primary exit path for venture-backed tech startups. This roughly 20-year period included huge exits such as Instagram ($1 billion), Oculus ($2 billion), and WhatsApp ($19 billion).

However, since Lina Khan led the Federal Trade Commission (FTC), large mergers have been blocked on the grounds of “increasing competition”, on the grounds that the big fish are prohibited from eating the small fish. This was the (ostensible) rationale behind the joint EU, US and UK regulators’ crackdown on Adobe’s acquisition of Figma, which was supposed to be a huge exit to fund more startups:

Khan’s logic is fundamentally flawed because when a large company buys a small competitor at a high price, it is effectively a capitulation — and a huge injection of capital into the venture capital ecosystem to create more of these competitors. If such exits (whether IPOs or M&A) decline, then tech startups will have no access to capital and no competition.

3) Trump’s new administration is still against mergers and acquisitions!

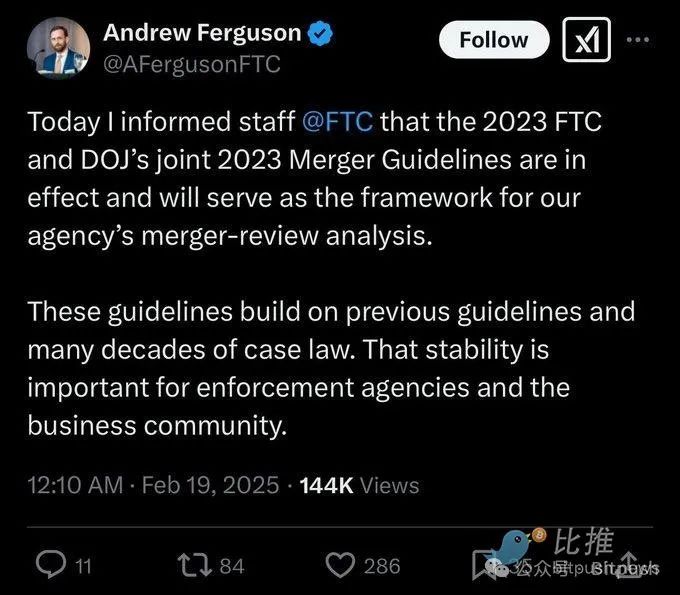

Tech insiders had expected the new administration to be friendlier to mergers and acquisitions. But surprisingly, the new administration has accepted Lina Khan’s logic — and is apparently continuing her policies:

I think this is partly due to their (understandable) tribal hostility toward Big Tech for media-driven censorship during the 2020 election. But unless things change, this means tech M&A isn’t coming back.

In addition, the new administration has continued Biden's anti-merger policy in another aspect. Japan's Nippon Steel was blocked by Biden from acquiring US Steel, and the new administration has maintained this block. However, they seem to offer a different path, where Nippon Steel invests in the US company but does not own it.

No matter what: It’s not easy for a company, big or foreign, to acquire an American company. And M&A itself is already difficult. It’s like getting married nowadays, it’s a big project. If you add some unpredictable government risk to an already difficult deal, many M&A won’t even be considered.

4) But the encryption window is already open

However, when the government closes a door, sometimes a window opens. Although IPOs are still expensive, and although mergers and acquisitions have become more difficult… the new administration has actually loosened regulations on cryptocurrencies by launching presidential meme coins and pro-crypto executive orders.

While no one knows what the new rules will be yet, if you can issue unbacked meme coins, then you can almost certainly also issue equity-backed ICOs, also known as security token offerings (STOs):

In fact, STOs actually align with the administration’s vision that “the world should invest in American-created tokens” and that “small entities should be able to remain independent longer.”

Remember their idea that it was OK for Nippon Steel to invest in U.S. Steel, but not to own it? That could be one way to solve the problem. If you don’t allow big tech to buy small tech, you need to allow the latter to raise money in a way that allows them to compete with big tech.

So let the world invest in them on-chain without owning them, just like Nippon Steel invested in U.S. Steel. Just like Masa and Saudi Arabia are investing hundreds of billions of dollars in U.S. companies without owning them outright.

It’s a financial win-win while preserving sovereignty.

In addition, in theory, small businesses (such as restaurants, etc.) can also do STOs. In theory, STOs reduce the cost of listing capital from millions to zero. But you need to overlay new decentralized regulatory mechanisms on such markets, similar to Uber/Airbnb/Amazon's star ratings and bans on bad actors.

5) From Blue States to Blockchain

Anyway: there are countless details that need to be worked out in terms of putting the equity table on-chain and doing a high-confidence public offering (with lock-up periods, etc.).

But that’s ultimately where we want to be. California is no longer the only place to operate, Delaware is no longer the best place to incorporate, and New York is no longer a place where the rule of law can be trusted.

The era of blue states is over, but blockchain is on the rise.

Because obviously, Internet companies should exist on-chain in an Internet-native form and be able to access Internet-scale capital markets through encryption. In fact, while the number of stocks listed in New York has been declining, the number of Internet-listed digital assets has been rising.

So, I say this to my tech friends: yes, the window for tech IPOs and M&A may have closed, but the window for tech STOs may be wide open.