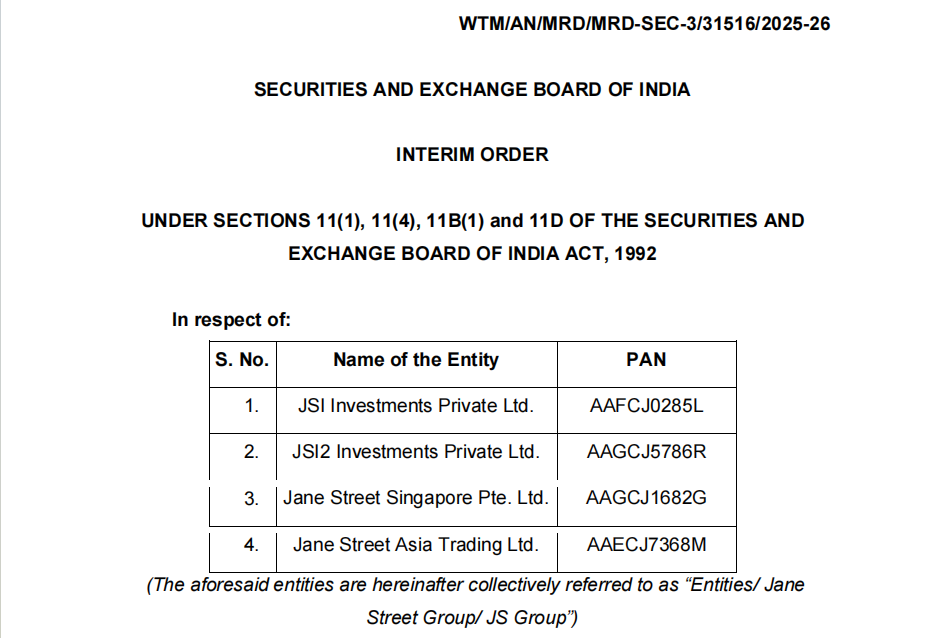

Report link: chrome-extension://blegnhaaimfcklgddeegngmanbnfopog/https://images.assettype.com/barandbench/2025-07-04/aiwwj4zh/SEBI_Jane_Street_order.pdf

In July 2025, the global financial market was shaken by a piece of heavy news. Jane Street, a top quantitative trading giant known for its mystery and eliteness, was fined a record 48.43 billion rupees (about 580 million U.S. dollars) by the Securities and Exchange Board of India (SEBI) for systematic index manipulation in the Indian market, and was temporarily banned from market access. The core document of this incident is a 105-page SEBI interim investigation report, which is like a detailed script, revealing how the top technical "players" take advantage of the asymmetry of the market structure to reap.

This is not only a high-priced fine, but also a profound warning to all trading institutions around the world that rely on complex algorithms and technological advantages, especially virtual asset institutions in the regulatory "gray area". When the ultimate quantitative strategy fundamentally conflicts with market fairness and regulatory intentions, technological advantages will no longer be a "talisman", but may instead become "evidence" pointing to oneself.

Aiying’s research team spent a week analyzing SEBI’s investigation report in depth, from case review, regulatory logic, market impact, technical reflection, to correlation mapping with the Crypto field and future prospects, to interpret the “Sword of Damocles” of compliance hanging over the heads of all participants in the virtual asset market, and explore how to move forward steadily on the tightrope of technological innovation and market fairness.

Part One: Review of the “Perfect Storm”—How did Jane Street weave its web of manipulation?

To understand the far-reaching impact of this case, we must first clearly restore the manipulation methods that Jane Street is accused of. This is not an isolated technical error or accidental strategic deviation, but a set of carefully designed, systematically executed, large-scale and highly concealed "conspiracy". SEBI's report reveals its two core strategies in detail.

1. Analysis of core strategies: the operating mechanisms of the two “open plots”

According to SEBI's investigation, Jane Street mainly used two interrelated strategies, which were repeatedly performed on the option expiration dates of multiple BANKNIFTY and NIFTY indices. The core of these strategies was to take advantage of the liquidity differences and price transmission mechanisms between different markets to make profits.

Strategy 1: “Intra-day Index Manipulation”

This strategy is divided into two clear stages, like a carefully choreographed drama, designed to create market illusions and ultimately reap the rewards.

- Phase 1 (Morning/Patch I): Create false prosperity and lure the enemy deeper.

- Behavior: Through its local entity registered in India (JSI Investments Private Limited), it invested billions of rupees in the relatively low liquidity spot (Cash) and stock index futures (Stock Futures) markets, and bought a large amount of key components of the BANKNIFTY index, such as HDFC Bank, ICICI Bank, etc., in an aggressive manner.

- Method: Its trading behavior is extremely aggressive. The report shows that Jane Street's buy orders are usually higher than the latest transaction price (LTP) at the time, actively "pushing up" or strongly "supporting" the prices of constituent stocks, thereby directly raising the BANKNIFTY index. In certain periods, its trading volume even accounts for 15% to 25% of the total trading volume of individual stock markets, forming a force sufficient to guide prices.

- Purpose: The sole purpose of this move is to create the illusion that the index is rebounding strongly or stabilizing. This will directly affect the highly liquid options market, causing the price of call options to be artificially pushed up, while the price of put options is correspondingly depressed.

- Coordinated actions: While making "noise" in the spot market, Jane Street's overseas FPI entities (such as Jane Street Singapore Pte. Ltd.) quietly acted in the options market. They took advantage of distorted option prices to buy a large number of put options at very low costs and sell call options at artificially high prices, thereby building a large-scale short position. The SEBI report pointed out that the notional value (cash-equivalent) of its option positions was several times the amount of money invested in the spot/futures market. For example, on January 17, the leverage ratio was as high as 7.3 times.

- Phase 2 (afternoon/Patch II): Reverse harvesting to achieve profits.

- Behavior: During the afternoon trading session, especially near the close, Jane Street’s local entities would do a 180-degree turn and systematically and aggressively sell all positions bought in the morning, sometimes even increasing their sales.

- Technique: Contrary to the morning, the selling order price is usually lower than the market LTP, actively "suppressing" the prices of constituent stocks, causing the BANKNIFTY index to fall rapidly.

- Profit closed loop: The sharp drop in the index caused the huge put option (Put) value established in the morning to soar, and the call option (Call) value to return to zero. In the end, the huge profit he made in the options market far covered the certain loss caused by "buy high and sell low" in the spot/futures market. This model constitutes a perfect profit closed loop.

Strategy 2: “Extended Marking The Close”

This is another more direct manipulation technique that is mainly concentrated in the last stage of the trading day, especially during the settlement window of options contracts.

'Extended marking the close' refers to a manipulative trading practice where an entity places a large number of buy or sell orders at the end of a trading session with the intent to influence the closing price of a security or index, thereby profiting from its derivative positions.

On certain trading days, Jane Street did not adopt a 24-hour "buy-sell" mode. Instead, after 14:30 p.m., when it held a large number of expiring option positions, it suddenly carried out large-scale one-way transactions (buy or sell) in the spot and futures markets to push the final settlement price of the index in a direction favorable to it.

Key evidence and data support

SEBI's accusation is not groundless, but is based on massive trading data and rigorous quantitative analysis.

- Size and concentration

The report uses detailed tables (such as Table 7, 8, 16, 17) to show Jane Street's astonishing share of trading volume in a specific time window. For example, on the morning of January 17, 2024, its purchase volume in the ICICIBANK spot market accounted for 23.33% of the total market buyer volume. This market dominance is the premise for it to be able to influence prices.

- LTP Impact Analysis

This is a highlight in the SEBI report. The regulator not only analyzed the trading volume, but also used LTP impact analysis to determine the "intention" of its trading. The analysis showed that Jane Street's trading had a huge positive price impact on the index during the pull-up phase, and a huge negative impact during the suppression phase. This strongly refutes the possible excuse of "normal trading" or "providing liquidity" that it may have put forward, proving that its behavior has a clear purpose of "pushing up" or "suppressing" the market.

- Cross-entity coordination and regulatory evasion

SEBI clearly pointed out that Jane Street cleverly circumvented the restriction that a single FPI could not conduct intraday trading by combining its local Indian entity (JSI Investments) and overseas FPI entities. The local entity was responsible for high-frequency intraday reversal trading (buy and then sell) in the spot market, while the FPI entity held and benefited from the huge option position. This "left hand hitting the right hand" coordinated manipulation model shows the premeditation and systematic nature of its behavior.

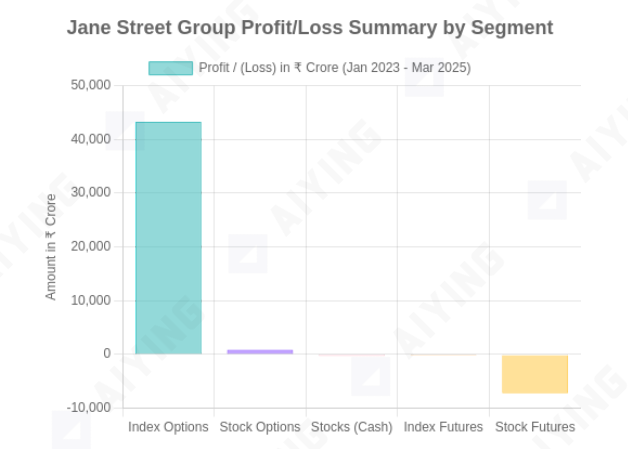

Data source: SEBI interim investigation report (Table 4). The chart clearly shows that Jane Street made huge profits in the options market, while incurring significant losses in other markets (especially stock futures), which confirms the operational logic of "exchanging losses for greater profits" in its strategy.

Part II: The “Skynet” of Supervision: SEBI’s Penalty Logic and Core Warnings

Faced with such a complex and highly technical trading strategy of Jane Street, SEBI's penalty decision did not fall into an endless exploration of its algorithmic "black box", but went straight to the point, starting from the nature of its behavior and the damage to market fairness. The regulatory logic behind this is a strong warning to all technology-driven trading institutions, especially those involved in the virtual asset field.

The logo outside the Securities and Exchange Board of India (SEBI) headquarters building

1. SEBI’s penalty logic: characterizing based on “behavior” rather than “result”

The core of SEBI's legal weapon is its "Prohibition of Fraudulent and Unfair Trade Practices Regulations" (PFUTP Regulations). Its punishment logic is not based on "Jane Street makes money" but on "Jane Street's way of making money is wrong."

The key qualitative basis is as follows:

1. Creating false or misleading market appearances (Regulation 4(2)(a)): SEBI believes that Jane Street artificially created the rise and fall of the index through its large-scale and high-intensity buying and selling behavior, which sent false price signals to the market and misled the judgment of other participants (especially retail investors who rely on price signals to make decisions). This behavior itself constitutes a distortion of the real supply and demand relationship in the market.

2. Manipulation of securities prices and benchmark prices (Regulation 4(2)(e)): The report clearly states that the direct purpose of Jane Street’s actions was to influence the BANKNIFTY index, an important market benchmark price. All of its operations in the spot and futures markets were aimed at moving this benchmark price in a direction that was favorable to its derivatives positions. This is considered typical price manipulation.

3. Lack of independent economic rationality: This is the "winner" in SEBI's argument. The regulator pointed out that Jane Street's intraday buy high and sell low reversal transactions in its spot/futures market will inevitably lead to losses from a single business perspective. Reported data shows that in the 15 trading days of "intraday index manipulation", it has accumulated losses of 1.997 billion rupees in the spot/futures market. This "deliberate loss" behavior proves that these transactions are not for investment or normal arbitrage, but as a "cost" or "tool" to serve the purpose of manipulation to obtain greater profits in the options market.

2. Core warning: Technology is neutral, but people who use technology have a stance

The most profound warning from this case is that it clearly draws a red line:

Today, as regulation becomes increasingly sophisticated and principled, pure technical and mathematical advantages, if lacking respect for market fairness and regulatory intent, may cross the legal red line at any time.

- The boundaries of technological advantage: Jane Street undoubtedly has the world's top algorithms, low-latency execution systems, and excellent risk management capabilities. However, when this capability is used to systematically create information asymmetry and undermine the market's price discovery function, it is transformed from a "tool to improve efficiency" to a "weapon for manipulation." Technology itself is neutral, but its application method and intention determine the legitimacy of its behavior.

- A new regulatory paradigm based on principles: Global regulators, including SEBI and SEC, are increasingly evolving from a rule-based to a principle-based regulatory philosophy. This means that even if a complex trading strategy does not explicitly violate a specific rule, it may be considered manipulation as long as its overall design and final effect violate the basic market principles of "fairness, justice, and transparency." Regulators will ask a fundamental question: "What benefit does your behavior bring to the market, other than harming the interests of others to make a profit for yourself?" If the answer is no, then the risk is extremely high.

3. “Arrogance” in Ignoring Warnings: Catalyst for Severe Punishment

SEBI highlighted an aggravating circumstance in the report: In February 2025, the National Stock Exchange of India (NSE) had issued a clear warning letter to Jane Street in accordance with SEBI's instructions, requiring it to stop suspicious trading patterns. However, the investigation found that Jane Street continued to manipulate the NIFTY index in May of the following year using similar "closing price manipulation" techniques.

This behavior was regarded by SEBI as a blatant disregard for regulatory authority and "not a good faith actor". This was not only one of the reasons for the high fine imposed on it, but also an important catalyst for SEBI to take the severe temporary measure of "prohibiting market access". This is a lesson for all market participants: communication and commitments with regulators must be taken seriously, and any form of fluke and arrogance may lead to more severe consequences.

Part 3: No snowflake is innocent in the avalanche - market impact and breadth of victims analysis

The impact of the Aiying Jane Street case goes far beyond the fine and reputational damage of one company. Like a boulder thrown into a calm lake, it has caused ripples throughout the entire quantitative trading ecosystem and redefined our understanding of “victims.” The breadth and depth of its impact is worth pondering for all market participants.

1. Direct impact on market ecology

Liquidity paradox and declining market quality

In the short term, the ban on top market makers like Jane Street will undoubtedly have an impact on the liquidity of its active derivatives markets (such as BANKNIFTY options). The bid-ask spread may widen, and transaction costs will rise accordingly. As Nithin Kamath, CEO of Zerodha, a well-known Indian brokerage, pointed out, the top proprietary trading companies contribute nearly 50% of option trading volume, and their retreat may significantly affect market depth.

Trust crisis and industry chilling effect

This case has seriously shaken the market's trust in quantitative trading, especially high-frequency trading (HFT). The negative perception of the public and regulators has intensified, which may lead to "stigmatization" of the entire industry. Other quantitative funds, especially foreign institutions, may become more cautious because of this case, reassess the regulatory risks in emerging markets such as India, or actively shrink their business scale, forming a "chilling effect."

The beginning of a comprehensive tightening of regulation

The Chairman of SEBI has made it clear that it will strengthen monitoring of the derivatives market. This indicates that all quantitative institutions will face stricter algorithmic reviews, more transparent position reporting requirements and more frequent compliance checks in the future. An era of stricter regulation has arrived.

2. Victim spectrum analysis: chain reaction from retail investors to institutions

Traditional analysis tends to focus on the victims, namely retail investors who are directly “harvested”. However, in an interconnected market, the harm of manipulation is systemic.

Direct victims: retail investors who were “harvested”

This is the most obvious group of victims. SEBI reports repeatedly mention that as many as 93% of retail investors in India lose money in F&O (futures and options) transactions. Jane Street's strategy takes advantage of the retail investor group's reliance on price signals and insufficient information processing capabilities. When the index is artificially raised, retail investors are lured into a long trap; when the index is artificially suppressed, their stop-loss orders aggravate the market's decline. They have become the direct "counterparties" to Jane Street's huge profits, and with the dual disadvantages of information and funds, they have almost no ability to fight back.

Indirect victims: other quantitative institutions misled by "contaminated" signals

This is an often overlooked but crucial group of victims. Jane Street and retail investors are not the only ones playing the market game. There are hundreds of other small and medium-sized quantitative institutions whose trading models also rely on public market data - prices, volumes, order book depth, etc. - to make decisions. Their way of survival is to find tiny arbitrage opportunities in a fair and efficient market through better models or faster execution.

However, when “whales” like Jane Street use their overwhelming financial advantages to systematically “pollute” the price signals that are the cornerstone of the market, the rules of the entire game are changed. The models of other quantitative institutions receive distorted data, which are market conditions that have been “directed” by humans.

This will lead to a series of chain reactions:

- Strategy failure

Models based on trend following, mean reversion or statistical arbitrage may completely fail when faced with such artificially created violent reversals, leading to erroneous trades and losses.

- Risk model misjudgment

Risk management models, such as VaR, are calculated based on historical volatility. When market volatility is artificially amplified, these models may underestimate the true risk or trigger risk control instructions at the wrong time.

- Missing a real opportunity

When markets are primarily driven by manipulation rather than fundamentals or true sentiment, strategies designed to uncover true value are left to falter.

Therefore, Jane Street's actions not only harvested retail investors, but also caused a "dimensionality reduction attack" on other professional institutions in the same track. They thought they were playing against the "market", but in fact they were playing against a "fake market" with a God's perspective. This breaks the simple cognition of "quantitative involution, the strong will always be strong", and reveals how fragile the market's price discovery function is in the face of absolute power. From this perspective, all participants who rely on fair signals, regardless of their technical level, have become potential victims of this manipulation drama.

Part 4: Mirror of Crypto Field - Cross-market Mapping of Jane Street Strategy

For virtual asset institutions, the Jane Street case is by no means a spectator's tale. Its core manipulation logic is highly isomorphic to the "technical original sin" commonly seen in the Crypto market. Using this case as a mirror, we can clearly see the huge compliance risks hidden in the Crypto field.

1. Jane Street’s layout and behavior in the Crypto field

Jane Street is one of the earliest and most important institutional players in the crypto world. Its behavior is consistent with that in the traditional financial market: low-key, mysterious, but hugely influential.

According to Aiying, Jane Street is not only a major cryptocurrency market maker in the world, but also an important liquidity provider for leading exchanges such as FTX and Binance. Recently, it has become an authorized participant (AP) of several Bitcoin spot ETFs such as BlackRock and Fidelity, playing a key role in bridging traditional finance and crypto assets. It is worth noting that after the tightening of the US regulatory environment in 2023, Jane Street reduced its cryptocurrency trading business in the United States, but remained active in other parts of the world. This shows that it is highly sensitive to regulatory risks and has the ability to flexibly adjust strategies globally. It can be concluded that Jane Street's quantitative models, technical architecture and risk management philosophy, which have been tempered in the traditional financial market, are also applied to its crypto asset transactions. Therefore, its manipulation techniques in the Indian market are of great reference value for understanding its potential behavior patterns in the Crypto world.

Compared with traditional financial markets, the manipulation methods in the crypto asset market are closely integrated with technical protocols, market structure and community ecology. The following cases cover multiple dimensions from DeFi to CEX, from algorithms to social media, revealing the diversity and complexity of its manipulation behaviors.

Case 1: Mango Markets Oracle Manipulation Case (DeFi)

Manipulation method: In October 2022, the manipulator Avraham Eisenberg took advantage of the structural loopholes of the Mango Markets protocol and significantly increased the value of its collateral by raising the price of its governance token MNGO on multiple platforms. He then used this highly inflated collateral as evidence to borrow and exhaust various mainstream crypto assets worth approximately US$110 million from the protocol treasury.

Market impact and legal consequences: This incident caused the Mango Markets protocol to go bankrupt instantly and user assets were frozen. Eisenberg later argued that his actions were a "high-profit legal trading strategy" and challenged the boundary of "code is law". However, the US Department of Justice eventually arrested and convicted him on charges of commodity fraud and commodity manipulation. This case became the first landmark case to successfully prosecute DeFi market manipulation, establishing the applicability of traditional market manipulation regulations in the DeFi field.

Case 2: FTX / Alameda Research Internal Related Party Manipulation Case (CEX)

Manipulation methods: There is a systematic transfer of interests and market manipulation between FTX Exchange and its affiliated trading company Alameda Research. Alameda used its special permissions at FTX (such as exemption from automatic liquidation) to embezzle customer deposits for high-risk investments. At the same time, the two parties worked together to manipulate the price of FTX platform currency FTT and used it as false collateral to cover up Alameda's huge losses.

Market impact and legal consequences: The manipulation ultimately led to the collapse of the FTX empire, triggering a liquidity crisis that affected the entire industry, and investors lost billions of dollars. Founder Sam Bankman-Fried was convicted of multiple charges including securities fraud and wire fraud. This case reveals the extreme systemic risks that can arise when centralized platforms lack external supervision and internal risk control.

Case 3: BitMEX Derivatives Market Manipulation Case (Derivatives)

Manipulation tactics: The U.S. Commodity Futures Trading Commission (CFTC) and the Financial Crimes Enforcement Network (FinCEN) accused BitMEX of operating illegally for a long time and failing to implement necessary anti-money laundering (AML) and know your customer (KYC) procedures. This created conditions for market manipulators (including its internal employees) to influence derivatives prices through means such as "spoofing" and "wash trading." Its unique "liquidation engine" was also accused of exacerbating user losses during violent fluctuations.

Market impact and legal consequences: BitMEX's actions undermined the fairness of the derivatives market and harmed the interests of traders. In the end, BitMEX reached a settlement with regulators and paid a huge fine of $100 million. Its founders also admitted to violating the Bank Secrecy Act. This case marks the beginning of the tightening of regulators' supervision of crypto derivatives platforms.

Case 4: Hydrogen Technology Algorithm Manipulation Case (Algorithmic)

Manipulative tactics: The U.S. Securities and Exchange Commission (SEC) accused Hydrogen Technology and its market makers of engaging in large-scale “wash trading” and “spoofing” operations on its HYDRO token through specially designed trading robots between 2018 and 2019. These algorithmic trades created more than $300 million in fake trading volume, accounting for the vast majority of the token’s total global trading volume, in an effort to create the illusion of market activity to attract investors.

Market impact and legal consequences: The manipulation misled the market, artificially inflated token prices, and caused ordinary investors to suffer losses after the price collapsed. The SEC ultimately ruled that it violated the anti-fraud and market manipulation provisions of the federal securities laws. This case is a typical example of regulators using data analysis technology to successfully identify and combat algorithm-driven manipulation.

Case 5: Social Media Influence Manipulation Case (Social Media)

Manipulation techniques: This type of manipulation does not rely on complex technology, but rather uses the influence of social media (such as X, Telegram, Discord). The typical model is "pump and dump", that is, the manipulation group pre-buys a certain low-liquidity token at a low price, and then releases false positive news through KOLs or social networks to attract a large number of retail investors to buy at high prices, and finally sells at high prices to make a profit.

Market impact and legal consequences: This behavior caused the target token price to soar and plummet in a short period of time, and the vast majority of retail investors who followed suit became "buyers". The SEC has filed lawsuits in many such cases, accusing the relevant influencers and project parties of promoting security tokens without disclosing their remuneration, which constitutes fraud. This shows that the scope of supervision has extended to the level of marketing and community opinion guidance.

Cross-market comparative analysis of manipulation logic

After analyzing the above specific cases, we can make a deeper comparison between the Jane Street case and the manipulation logic of the crypto world. Although the market carriers and technical tools are different, the underlying manipulation philosophy - using information, capital or rules advantages to create unfairness - is the same.

Control Mode | Traditional financial market case (Jane Street case) | Logical peers and examples in crypto asset markets |

|---|---|---|

| Cross-market price distortions | “Intraday Index Manipulation” : Large-scale transactions are carried out in the less liquid spot market to artificially influence the index price, thereby making profits from the reverse positions held in the more liquid derivatives market. The core of this is to use the trading behavior of one market as a tool to serve the profit goals of another market. | Internal Affiliate Manipulation (FTX/Alameda) : One entity (Alameda) exploits loopholes in the rules and customer assets of another related entity (FTX) to manipulate the market for its own profit. Both take advantage of the structural advantages of cross-entity or cross-market. |

| Price impact at key points | “Closing Price Manipulation” : At key time points such as contract settlement, through large transactions, the intention is to push the final settlement price of the underlying asset to a direction that is favorable to one's own position. The key point of this behavior is Precisely influence the benchmark price at a specific moment. | Price Oracle Manipulation (Mango Markets) : At a critical moment (such as before a lending operation), the price of an asset is instantly impacted through flash loans and other means, distorting the price oracle that the DeFi protocol relies on, thereby achieving fraudulent profits. |

| Creating a false market appearance | Through large-scale, high-intensity buying and selling activities, they artificially create ups and downs of the index, send false price and trading volume signals to the market, and mislead other participants. | Algorithmic manipulation and social media manipulation (Hydrogen, Pump & Dump) : Creating false trading volume (wash trading) through algorithmic robots, or posting false information through social media, with the common goal of creating a false sense of prosperity or urgency to induce others to make wrong investment decisions. |

Aiying’s conclusion: The mantis stalks the cicada, who is the oriole?

The Jane Street case and a series of precedents in the crypto world together paint a vivid picture of the financial market where “the mantis stalks the cicada, while the oriole waits behind.” However, in this game, who is the mantis and who is the oriole?

For many retail investors and small and medium-sized institutions who are immersed in the ups and downs of candlestick charts and chasing short-term hot spots, they are like the "praying mantis" that focuses on the prey in front of them (market Alpha). They often do not realize that every tiny pattern of their trading behavior and every emotional pursuit of rising and falling may be observed and used by more powerful predators, such as top quantitative institutions such as Jane Street. These "yellow sparrows", with their financial, technical and information advantages, are not playing games with the "market", but are systematically "hunting" for predictable behavior patterns.

This reveals the first cruel truth of market game: your opponent may not be the "market" or other retail investors as you imagine, but a highly rational professional hunter with a God's perspective. Losses are often not due to bad luck, but because the position in the food chain has long been determined. However, the story does not end there. When the "yellow bird" thinks it is at the top of the food chain and is intoxicated with the success of hunting, it is also exposed to the vision of the real "hunter" - the regulator. The fine in the Jane Street case just shows that even the most powerful "yellow bird" will also become the target of hunting once its behavior crosses the red line of market fairness and destroys the foundation of the entire ecosystem.

Therefore, for all market participants, the real wisdom of survival lies in two aspects: first, we must recognize the real opponents, restrain the "praying mantis" instinct driven by short-term profits, and understand our position in a jungle surrounded by "yellow sparrows". Second, we must have real respect for market rules. Rational and strategic thinking should not only be used to design more sophisticated hunting strategies, but also to understand the boundaries and bottom lines of the entire ecosystem. Any attempt to obtain excess returns by damaging the fairness of the system may lay the groundwork for future overturning.

In this never-ending game, the ultimate winner is not the most ferocious "oriole" nor the most diligent "praying mantis", but the wise participants who can see through the entire food chain, know how to dance with the rules, and always remain aware of the risks.