Author: Artemis & Vaults.fyi

Compiled by: Felix, PANews (excerpt)

The DeFi stablecoin yield landscape is undergoing a profound transformation. A more mature, resilient, and institutionally aligned ecosystem is emerging, marking a clear shift in the nature of on-chain yields. Combining insights from vaults.fyi and Artemis.xyz, this report dissects the key trends shaping on-chain stablecoin yields, covering institutional adoption, infrastructure construction, evolving user behavior, and the rise of yield stacking strategies.

Institutional Adoption of DeFi : A Quiet Rise of Momentum

Even as nominal DeFi yields on assets like stablecoins adjust relative to traditional markets, institutional interest in on-chain infrastructure is growing steadily. Protocols like Aave, Morpho, and Euler are attracting attention and usage. This engagement is driven more by the unique advantages of composable, transparent financial infrastructure than by the pursuit of the absolute highest annualized yield, and this advantage is now reinforced by evolving risk management tools. These platforms are more than just yield platforms, they are evolving into modular financial networks and are rapidly becoming institutionalized.

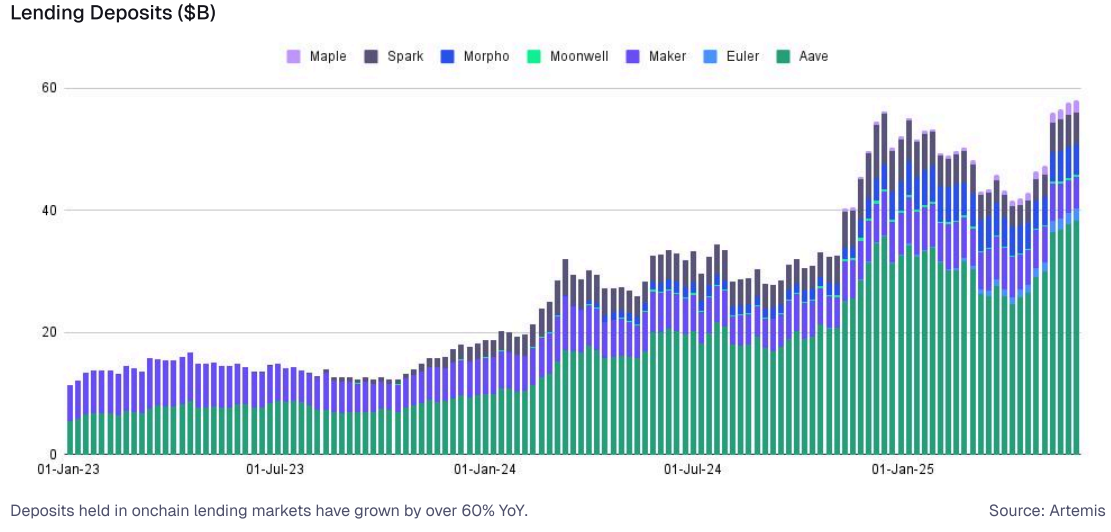

As of June 2025, the TVL of collateralized lending platforms such as Aave, Spark, and Morpho exceeds $50 billion. On these platforms, the 30-day lending yield of USDC is between 4% and 9%, which is generally at or above the yield level of about 4.3% of 3-month US Treasury bonds during the same period. Institutional capital is still exploring and integrating these DeFi protocols. Their enduring appeal lies in their unique advantages: 24/7 global markets, composable smart contracts that support automated strategies, and greater capital efficiency.

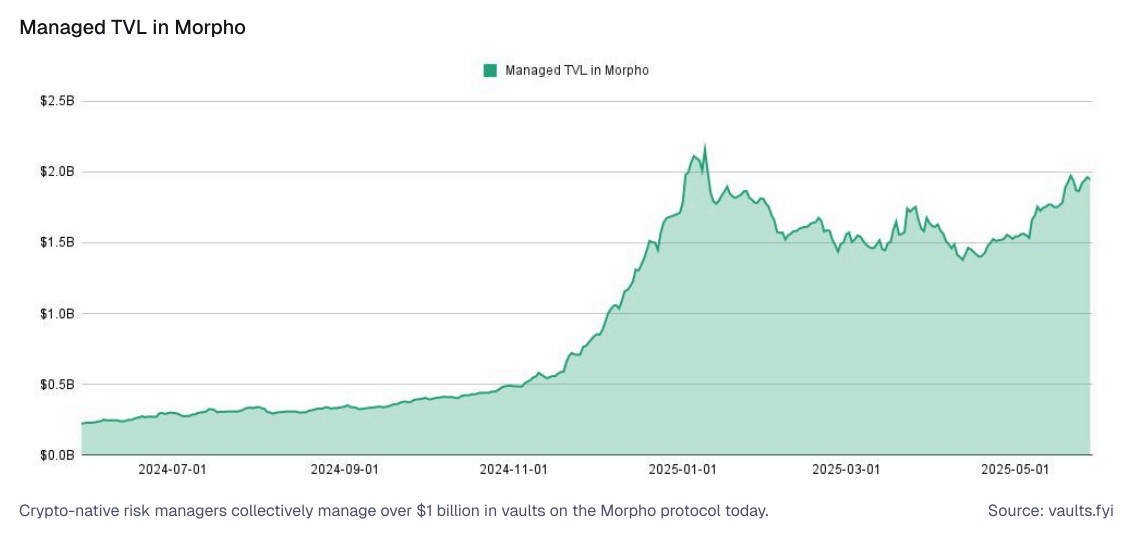

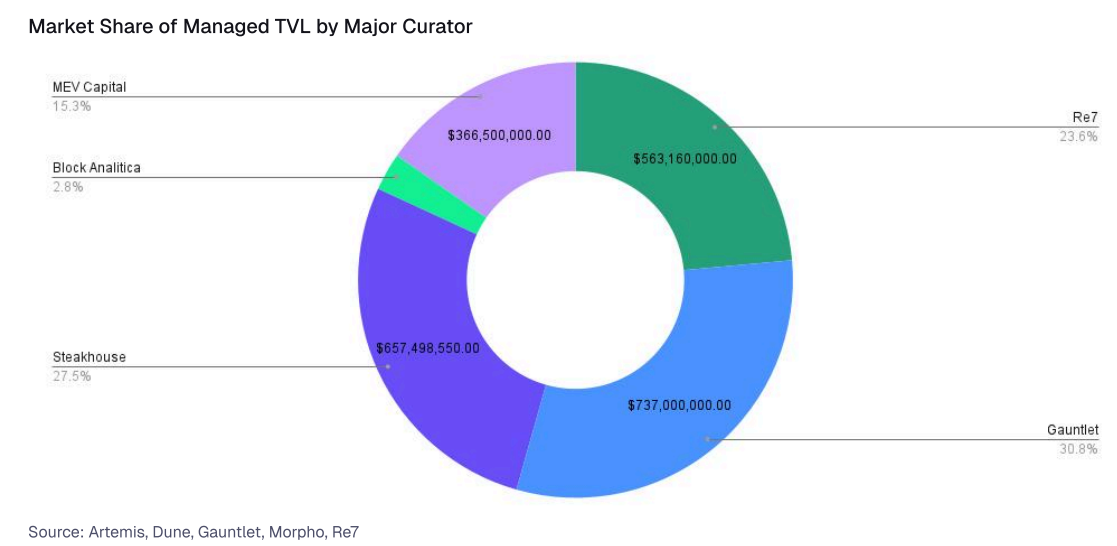

The Rise of Crypto-Native Asset Managers : A new class of “crypto-native” asset managers is emerging, with firms such as Re7, Gauntlet, and Steakhouse Financial. Since January 2025, the on-chain capital base in the space has grown from approximately $1 billion to over $4 billion. These managers are deeply embedded in the on-chain ecosystem, quietly deploying capital into a variety of investment opportunities, including advanced stablecoin strategies. In the Morpho protocol alone, the total locked value (TVL) in custody of major asset managers is approaching $2 billion. By introducing a professional capital allocation framework and actively adjusting the risk parameters of DeFi protocols, they are striving to become the next generation of leading asset managers.

The competitive landscape among the management institutions of these native cryptocurrencies has begun to emerge, with Gauntlet and Steakhouse Financial controlling approximately 31% and 27% of the custody TVL market respectively, while Re7 has nearly 23% and MEV Capital has 15.4%.

Shifting regulatory attitudes : As DeFi infrastructure matures, institutional attitudes are gradually shifting to view DeFi as a configurable, complementary financial layer rather than a disruptive, unregulated space. Permissioned markets built on Euler, Morpho, and Aave reflect active efforts to meet institutional needs. These developments enable institutions to participate in on-chain markets while meeting internal and external compliance requirements (particularly around KYC, AML, and counterparty risk).

DeFi Infrastructure: The Basis for Stablecoin Yields

The most significant progress in the DeFi space today is focused on infrastructure construction. From tokenized RWA markets to modular lending protocols, a whole new DeFi stack is emerging—capable of serving fintech companies, custodians, and DAOs.

1. Collateralized lending : This is one of the main sources of income. Users lend stablecoins (such as USDC, USDT, DAI) to borrowers, and borrowers provide other crypto assets (such as ETH or BTC) as collateral, usually in an over-collateralized manner. Lenders earn interest paid by borrowers, thus laying the foundation for stablecoin income.

- Aave, Compound, and MakerDAO (now renamed Sky Protocol) introduced pool lending and dynamic interest rate models. Maker launched DAI, while Aave and Compound built scalable money markets.

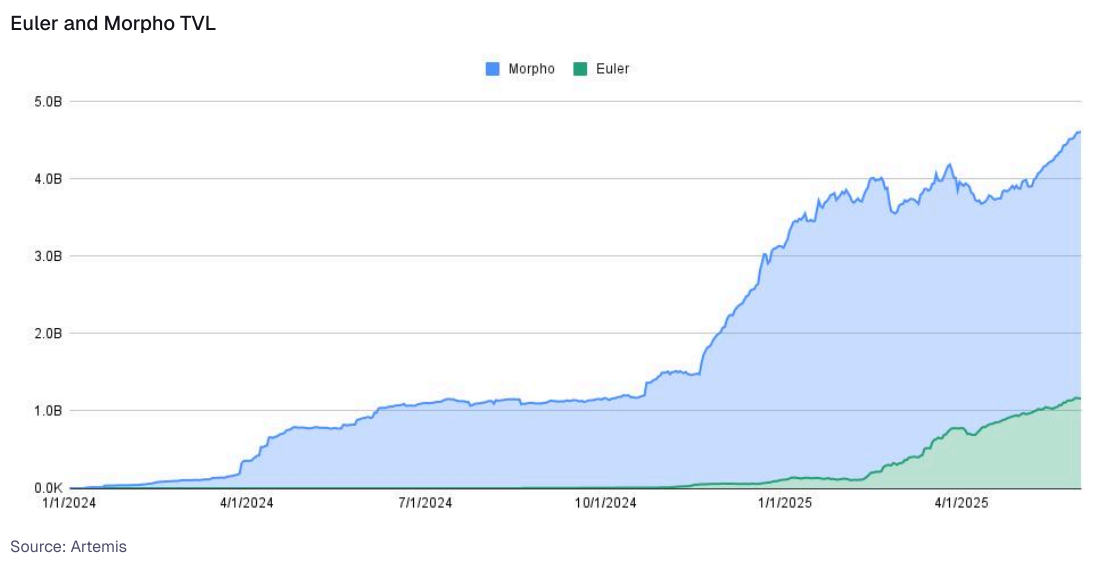

- Recently, Morpho and Euler have transitioned to modular and isolated lending markets. Morpho launched a fully modular lending primitive that divides the market into configurable vaults, allowing protocols or asset managers to define their own parameters. Euler v2 supports isolated lending pairs and is equipped with advanced risk tools, and has gained significant momentum since the protocol was restarted in 2024.

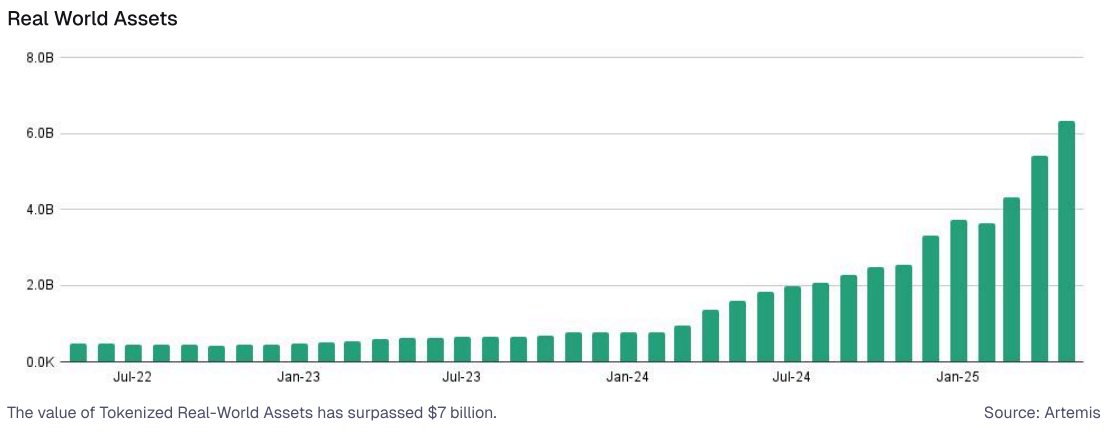

2. Tokenized RWA : This involves introducing the returns of traditional off-chain assets (especially US Treasuries) into the blockchain network in the form of tokenized assets. These tokenized Treasuries can be held directly or integrated into other DeFi protocols as collateral.

- Tokenization of US Treasuries through platforms such as Securitize, Ondo Finance, and Franklin Templeton transforms traditional fixed income into programmable on-chain components. On-chain US Treasuries have grown significantly from $4 billion at the beginning of 2025 to over $7 billion in June 2025. As tokenized Treasury products are adopted and integrated into the ecosystem, these products bring new audiences to DeFi.

3. Tokenized strategies ( including Delta Neutral and Yield Stablecoins): This category covers more complex on-chain strategies that typically pay out yields in the form of stablecoins. These strategies may include arbitrage opportunities, market making activities, or structured products designed to generate returns on stablecoin capital while maintaining market neutrality.

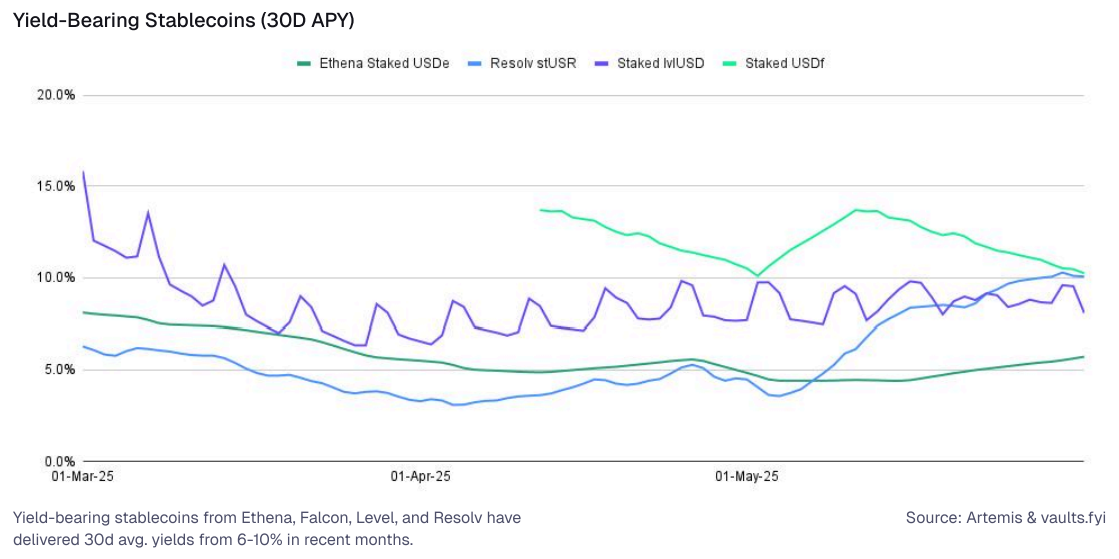

- Yield stablecoins: Protocols such as Ethena (sUSDe), Level (slvlUSD), Falcon Finance (sUSDf), and Resolv (stUSR) are innovating stablecoins with native yield mechanisms. For example, Ethena's sUSDe generates income through "cash and carry" transactions, that is, shorting ETH perpetual contracts while holding spot ETH, and funding rates and staking income provide returns to stakers. In recent months, the yields of some yield-based stablecoins have exceeded 8%.

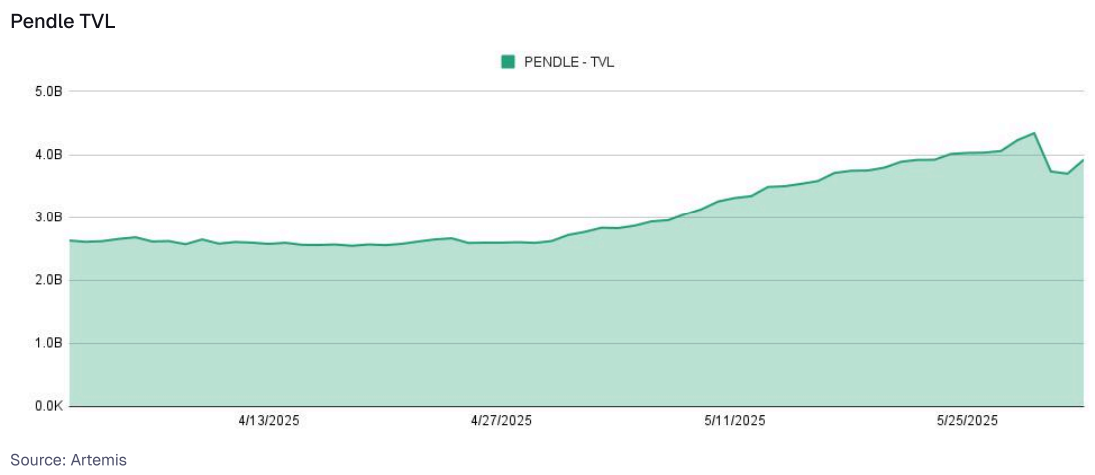

4. Yield Trading Market : Yield trading introduces a novel primitive that separates future yield streams from principal, enabling floating rate instruments to be split into tradable fixed and floating parts. This development adds depth to DeFi’s financial instruments and aligns on-chain markets more closely with traditional fixed income structures. By turning yields themselves into tradable assets, these systems provide users with greater flexibility to manage interest rate risk and yield allocations.

- Pendle is a leading protocol in the space, allowing users to tokenize yield assets into principal tokens (PT) and yield tokens (YT). PT holders receive fixed returns by purchasing discounted principal, while YT holders speculate on variable returns. As of June 2025, Pendle's TVL exceeds $4 billion, mainly composed of yield-based stablecoins such as Ethena's USDe.

Collectively, these primitives form the foundation of today’s DeFi infrastructure and serve a variety of use cases for both crypto-native users and traditional financial applications.

Composability: Stacking and amplifying stablecoin benefits

The “money lego” nature of DeFi is reflected in composability, where the primitives described above for generating stablecoin yields become the building blocks for building more complex strategies and products. This combination enables improved returns, risk diversification (or concentration), and customized financial solutions, all centered around stablecoin capital.

Lending markets for yield-bearing assets: Tokenized RWAs or tokenized strategy tokens (such as sUSDe or stUSR) can become collateral for a new type of lending market. This enables:

- Holders of these yield-yielding assets can borrow stablecoins against these assets, thereby freeing up liquidity.

- Creating lending markets specifically for these assets can generate further stablecoin yields if holders lend their stablecoins to those who wish to borrow against their yield positions.

Integrate diversified income sources into stablecoin strategies : Although the ultimate goal is usually stablecoin-dominated income, strategies to achieve this goal can be incorporated into other areas of DeFi and carefully managed to produce stablecoin income. Delta-neutral strategies involving lending non-USD tokens (such as liquidity staking tokens LST or liquidity re-staking tokens LRT) can be constructed to generate stablecoin-denominated income.

Leveraged yield strategies: Similar to arbitrage trading in traditional finance, users can deposit stablecoins into a lending protocol, borrow other stablecoins against that collateral, exchange the borrowed stablecoins back to the original asset (or another stablecoin in the strategy), and then deposit them back in. Each “cycle” increases exposure to the underlying stablecoin’s yield, while also amplifying risks, including liquidation risk when the value of the collateral declines or borrowing rates suddenly spike.

Stablecoin Liquidity Pool ( LP ):

- Stablecoins can be deposited into automated market makers (AMMs) like Curve, often alongside other stablecoins (like the USDC-USDT pool), earning revenue through transaction fees, which in turn generates income for the stablecoin.

- The LP tokens obtained from providing liquidity can themselves be staked in other protocols (for example, staking Curve’s LP tokens into the Convex protocol) or used as collateral in other vaults, further increasing returns and ultimately increasing the return on the initial stablecoin capital.

Yield Aggregators and Automatic Compounders : Vaults are a classic example of stablecoin yield composability. They deploy user-deposited stablecoins to underlying yield sources, such as collateralized lending markets or RWA protocols. They then:

- Automates the process of harvesting rewards (which may be in the form of another token).

- Redeem these rewards back to the originally deposited stablecoin (or other desired stablecoin).

- Re-depositing these rewards automatically compounds your earnings, significantly increasing your Annual Percentage Yield (APY) compared to manually claiming and reinvesting.

The overall trend is to provide users with enhanced and diversified stablecoin returns, managed within established risk parameters, and simplified through Smart Accounts and goal-focused interfaces.

User behavior: Revenue is not everything

While yield remains an important driver in the DeFi space, data shows that users’ decisions on capital allocation are driven by more than just the highest annualized yield (APY). Increasingly, users weigh factors such as reliability, predictability, and overall user experience (UX). Platforms that simplify interactions, reduce friction (such as fee-free transactions), and build trust through reliability and transparency tend to be better able to retain users over the long term. In other words, better user experience is becoming a key factor in not only driving initial adoption, but also promoting the continued “stickiness” of funds in DeFi protocols.

1. Capital prioritizes stability and trust: During periods of market volatility or downturn, capital tends to turn to mature “blue chip” lending protocols and RWA vaults, even if their nominal yields are lower than newer, riskier options. This behavior reflects a risk-averse sentiment, behind which is the user’s preference for stability and trust.

Data consistently shows that during periods of market stress, mature stablecoin vaults on established platforms retain a higher share of total value locked (TVL) than newly launched high-yield vaults. This “stickiness” reveals that trust is a key factor in user retention.

Annualized return (7-day average) and number of holders:

Protocol loyalty also plays a role. Users of mainstream platforms like Aave tend to prefer native ecosystem vaults, even though other platforms offer slightly higher interest rates - similar to the traditional financial model, where convenience, familiarity, and trust often outweigh small yield differences. This is even more evident on Ethena, where the number of holders remains relatively stable despite yields falling to historical lows, indicating that yield itself is not the main driver of user retention.

Despite the risk characteristics of stablecoins, there is still a huge demand for them. Platforms that can achieve permissionless reward accumulation hold huge opportunities in the crypto space, and their value even exceeds the current volatile value storage or stablecoins.

2. Better user experience improves retention rate: No Gas, seamless and automated: As DeFi matures, simplifying complex operations is becoming a key driver for improving user retention. Products and platforms that can simplify the complexity of underlying technologies are increasingly favored by new and old users.

Account abstraction (ERC-4337)-based features such as gas-free transactions and one-click deposits are becoming increasingly popular and help make user interactions more fluid and intuitive. These innovations reduce cognitive load and transaction costs, ultimately driving higher capital retention and growth.

Cross-chain yield gap: How capital flows

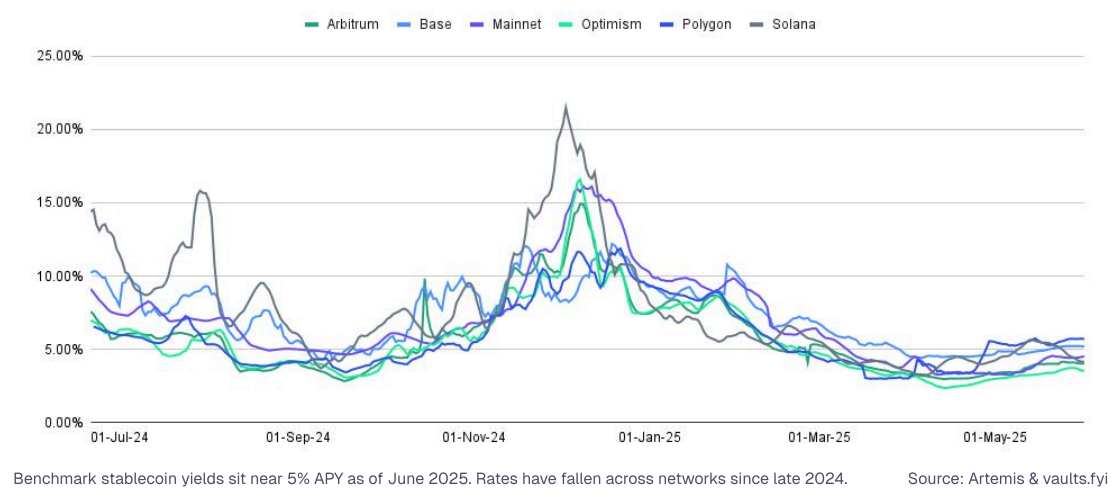

Similar assets (especially stablecoins) can have significantly different yields on different blockchain networks. Data shows that capital moves opportunistically between ecosystems based on these APY gaps, and the infrastructure to automate this migration is improving rapidly.

As of June 2025, the average lending yield on Ethereum hovered around 4.8%, while Polygon’s yield was as high as 5.6%.

Automated routing: Applications and aggregator protocols are increasingly equipped to route funds across chains to achieve higher annualized yields with minimal user intervention. However, this yield optimization also comes with risks. Bridging assets may expose users to bridge infrastructure risks and slippage risks when liquidity is insufficient.

Intent-centric user experience: Wallets and dApps are evolving to provide users with simple options such as “highest yield” or “best execution.” The underlying application then automatically fulfills these user intents, abstracting away the complexities of cross-chain routing, asset swapping, and vault selection.

Capital allocators can use deep cross-chain yield analysis to optimize back-end stablecoin strategies. By tracking cross-chain annualized yield differences, capital stickiness, and liquidity depth, these participants can:

- Improve fund management and optimize stablecoin distribution

- Provides users with competitive benefits without manual adjustments

- Identify sustainable arbitrage opportunities driven by structural yield gaps

DeFi revenue realization: the path for fintech companies and new banks

DeFi is increasingly being adopted by cryptocurrency native users as well as fintech companies, wallets, and exchanges, becoming an "invisible" backend infrastructure. By simplifying the complexity of DeFi, these platforms can embed benefits directly into the user experience, thereby improving retention, opening up new monetization paths, and improving capital efficiency.

There are three main ways for fintech companies to monetize:

1. Stablecoin Yield Integration : Unlocking New Revenue Streams: Fintechs and centralized platforms are increasingly offering stablecoin yields directly in their applications. This is a proven strategy that can:

- Driving net deposit growth

- Increase Assets Under Management (AUM)

- Enhance platform user stickiness and cross-selling potential

Example:

- Coinbase offers yield on USDC deposits to increase participation and trading volume in its ecosystem.

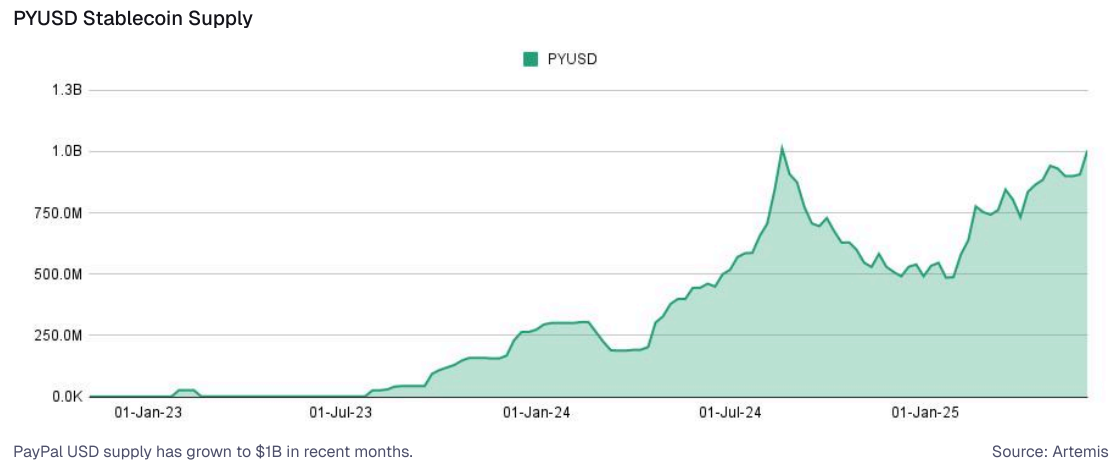

- PayPal's PYUSD yield product (approximately 3.7% annual interest rate) attracts funds into Venmo and PayPal wallets, achieving profits through reserve asset returns and increased payment activity.

- The integration of Bitget Wallet with Aave enables users to earn an annual interest rate of approximately 5% on USDC and USDT on multiple chains, thereby driving wallet deposits and achieving potential profits through referrals and trading.

These integrations remove the complexity of DeFi, allowing users to seamlessly access yield products while platforms earn profits through interest rate spreads, partner incentives, and increased trading traffic. As the stablecoin PYUSD gains new demand through yield-focused integrations and institutional adoption beyond traditional DeFi, its supply has reached an all-time high, solidifying its position as a core tool for passive income.

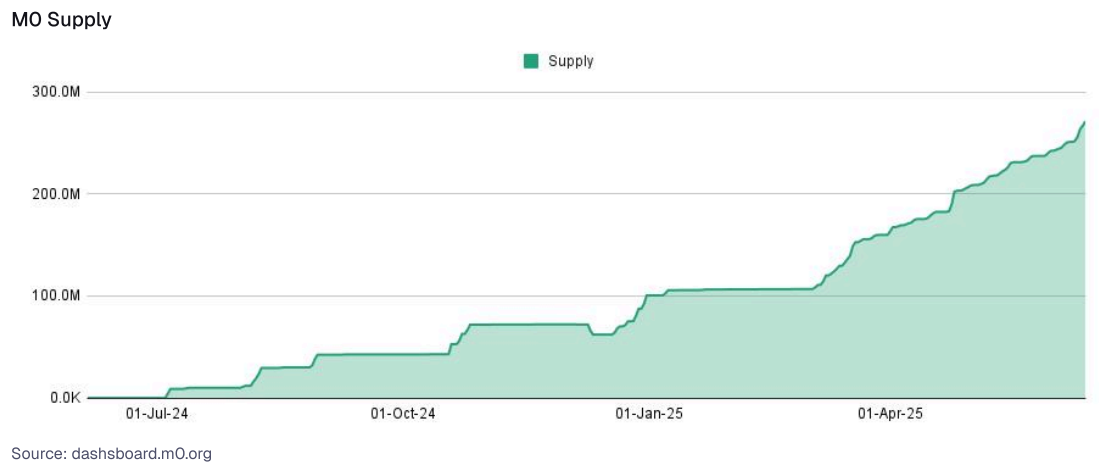

Fintech Opportunities: Integrating yield products or backend DeFi strategies can turn users’ idle balances into revenue streams and deeper engagement. Earning opportunities include net interest differential sharing, premium service fees, and building a stickier user base that is cheaper to serve and more receptive to cross-selling. M0 is a stablecoin infrastructure provider that enables platforms to launch custom stablecoins with built-in yield strategies without fragmenting liquidity or the ecosystem. The supply of stablecoins supported by M0 has been steadily increasing and is now close to $300 million.

2. Borrowing with cryptocurrencies as collateral: Seamless credit driven by DeFi . Fintech companies and exchanges now offer non-custodial collateralized borrowing services with crypto assets such as Bitcoin and Ethereum through embedded DeFi protocols.

Example:

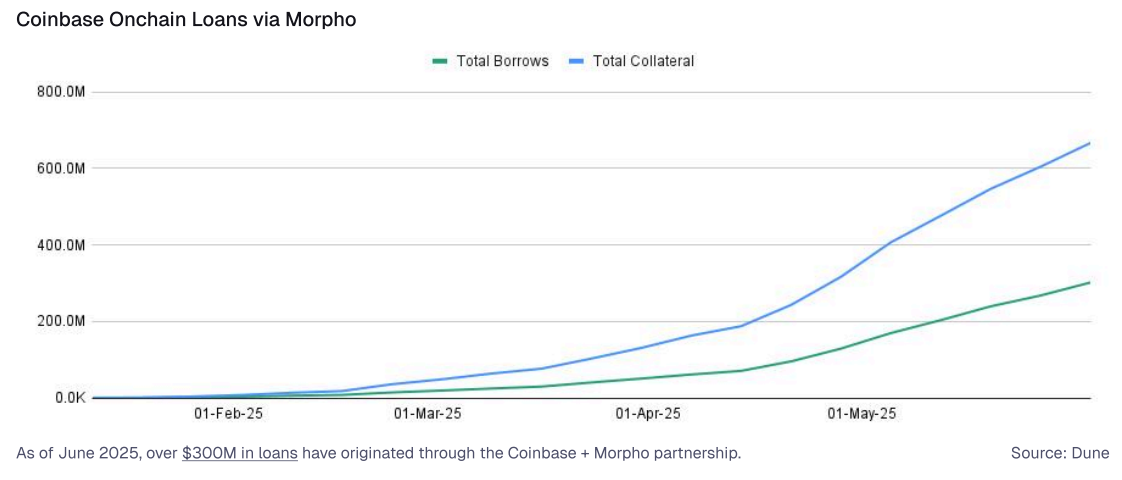

Coinbase’s on-chain lending integration with Morpho (over $300M issued as of June 2025) allows Coinbase users to seamlessly borrow against their BTC holdings, powered by Morpho’s backend infrastructure. This model is often referred to as the “DeFi Mullet” and enables:

- Issuance Fee

- Interest income

- The platform can carry out additional lending activities without taking direct custody risk

Fintech Opportunities: Fintech companies with a crypto user base (e.g., Robinhood, Revolut) could adopt a similar model to create new fee-based revenue streams by offering stablecoin lines of credit or asset-backed loans through permissioned on-chain marketplaces.

3. Consumer yield products : Embedded, passive yield: DeFi yields are finding their way into consumer-facing financial products in novel and sticky ways:

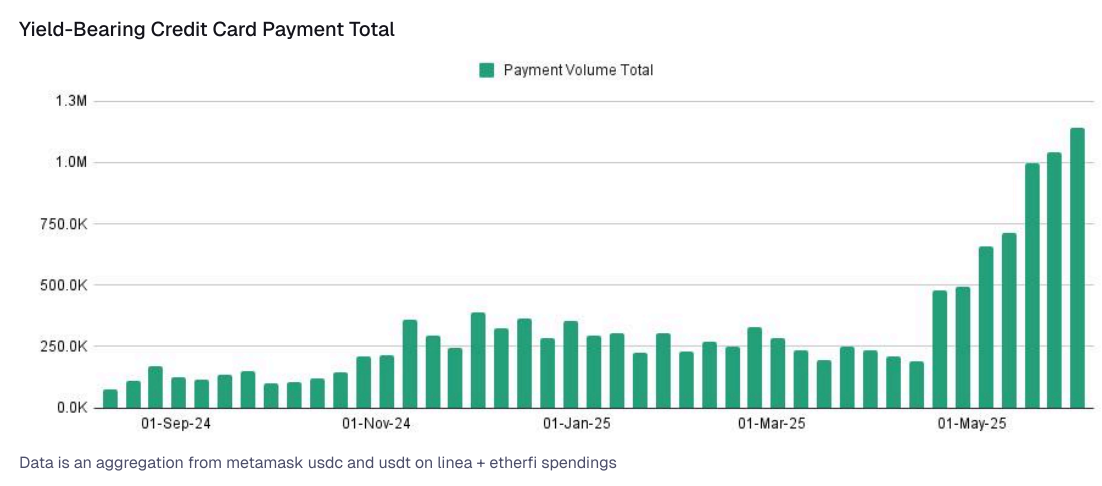

- Yield-backed debit cards: The concept of “cashback” could evolve into “yield-backed,” where stablecoin earnings automatically fund rewards or spending balances. Stablecoin spending on yield-backed debit cards has steadily grown to over $1 million per week.

- Automatic Yield Wallet: A programmable savings account that leverages account abstraction (ERC-4337) to enable gas-free deposits, automatic rebalancing, and the ability to generate yield without user intervention.

- Mainstream examples: Robinhood’s idle cash earnings, Kraken’s USDG rewards, and PayPal’s PYUSD savings product all demonstrate this broader shift toward frictionless, yield-generating consumer experiences.

Across these avenues, platforms that can simplify complexity, reduce friction, and leverage the flexibility of DeFi backends will lead the next wave of stablecoin monetization and user engagement.

in conclusion

The next evolution of DeFi returns is moving away from the speculative frenzy of earlier cycles. In today’s environment, DeFi is becoming:

- Simplification: Users will increasingly not need to understand (or care) which specific protocols or complex strategies are behind the returns of their assets; they will only need to interact with a simplified front end.

- Integration: DeFi yields will increasingly appear as a default or easily accessible option within existing wallets, exchanges, and mainstream fintech applications.

- Risk Awareness: Institutional partners and discerning users will demand robust risk scoring, comprehensive audits, insurance options, and greater transparency into the underlying mechanisms.

- Regulated and interoperable: Protocols will continue to explore the regulatory environment, with some choosing a licensed environment or working directly with regulators to meet the needs of institutional and traditional financial clients. Cross-chain interoperability will become smoother.

- Programmable and Modular: As DeFi matures, its core components (lending pools, collateralized derivatives, automated market makers, and RWA bridges) will increasingly become modular “money Lego”, fitting into familiar interfaces while building powerful financial solutions behind the scenes.

The platforms that thrive in this new era will not simply offer the highest short-term returns. As the sector develops and matures, the focus is shifting from chasing short-term excess returns to building sustainable, value-added financial infrastructure.

Related reading: DeFi bull market strategy: The US SEC has released positive news, and three categories are worth paying attention to