A source familiar with the matter told BlockBeats that Binance's investment team had already begun preparing for the acquisition of a shell company and private equity financing for the BNB Treasury project as early as early July. Another source familiar with the matter stated that to mitigate the risk of insider trading before the shell company was acquired, the team simultaneously acquired several small US-listed shell companies, only finalizing VAPE as their target at the last minute. Behind this unusual stock price movement lies a $500 million private placement financing agreement, jointly led by 10X Capital and YZi Labs, with the intention of transforming VAPE into the world's largest publicly listed BNB treasury. This isn't a retail frenzy, but a meticulously structured capital experiment—a novel arbitrage path between "compliant BNB holdings and public company valuation premiums," and potentially a breakthrough in a parallel narrative for the Binance ecosystem. VAPE, a previously unknown company, is now being recognized by the broader capital market as a key variable in the "BNB treasury" narrative.

Breaking Down the BNB Treasury's Operational Path: From Shell to Valuation Leverage

On July 28th, VAPE (formerly CEA Industries) officially announced a PIPE private placement financing round led by 10X Capital and YZi Labs. The initial financing amount reached US$500 million, consisting of US$400 million in cash and US$100 million in crypto asset subscriptions. Furthermore, if all the additional warrants are exercised, the total financing amount could be increased to a maximum of US$1.25 billion.

Not only is the scale of this financing impressive, it also clearly defines VAPE's goal: to create the world's largest, publicly listed BNB treasury company, introduce BNB to the capital market, and attract compliant capital to participate in the BNB Chain ecosystem through an asset allocation model.

This also means that VAPE is no longer just a hardware or retail supplier, but is transforming into a financial platform focused on BNB, integrating BNB's value and income mechanisms into the capital structure of listed companies.

Following the completion of the PIPE financing, VAPE will be led by a core team with backgrounds in institutional and digital assets. David Namdar (co-founder of Galaxy Digital and current senior executive at 10X Capital) will serve as CEO; Russell Read (former Chief Investment Officer of CalPERS and current CIO of 10X Capital) will serve as CIO; and Saad Naja (a seasoned operator with experience at Kraken and Exinity) will join the company's executive leadership.

Meanwhile, 10X Capital will serve as the asset manager for the BNB treasury, responsible for structure design, capital operations, and subsequent strategic implementation. YZi Labs will provide strategic support to facilitate the smooth execution of the PIPE placement. Over 140 institutional and crypto funds (such as Pantera Capital, Blockchain.com, GSR, and Arrington) participated in this round, providing strong capital backing.

BlockBeats analyzes VAPE's announcement, stating that the proceeds from the financing will be used to establish a long-term treasury strategy focused on BNB. Over the next 12–24 months, VAPE will build an initial BNB holding and increase its holdings at scale through methods such as ATM (At-The-Market) issuance. It will also consider participating in BNB staking, lending, and DeFi protocol yield mechanisms to generate structured returns while maintaining a conservative risk framework.

This operating model is similar to MicroStrategy's BTC treasury model, but focuses on BNB, which has stronger ecosystem applications. It supplements the value-added logic of holding coin with income-generating strategies, ensuring cash flow and premium potential.

After the PIPE closes, VAPE will become one of the largest publicly traded companies providing exposure to a single Layer-1 blockchain.

Simply put, this round of financing ultimately equips the company with a $1.25 billion crypto arsenal to buy BNB. By comparison, SharpLink (SBET), one of the earliest companies to bet on the ETH treasury concept, has only raised $525 million in total funding.

What will happen to the stock price after the deal closes?

After the PIPE was signed, VAPE announced that the financing is expected to be completed by July 31, 2025. At that time, the funds will be received and the company's updated capital management strategy will take effect. According to the announcement, the company's common stock will continue to trade on the Nasdaq Capital Market under the ticker symbol "VAPE."

PIPE financing is essentially a private placement offering a discount for capital. Simply put, the company sells its shares at a discount to specific investors in exchange for a large sum of capital. VAPE's primary financing is $500 million, of which $400 million is in cash, meaning the remaining $100 million is in BNB assets. This comes with a warrant mechanism with a maximum value of $1.25 billion. In short, the company will issue a large number of new shares and warrants to PIPE investors.

This will directly lead to two structural consequences: existing shareholders' shareholdings will be diluted. If calculated on a fully diluted basis, existing shareholders' voting rights and income rights will decline significantly; and the company's capital structure will become more complex. Warrants, associated lock-up clauses, and a phased exercise mechanism will make the company's valuation in the capital market more inclined towards a "structural model" rather than a fundamental model.

With the completion of the PIPE placement, VAPE's equity structure will shift from a "controlling" to a "circulating" structure. In particular, after the warrants are exercised, the company's free float will increase by orders of magnitude.

This point is particularly evident in VAPE's PIPE terms: this round of transactions incorporates a large-proportion warrant mechanism, allowing investors to subscribe for new shares at a price below the market price at a specific time point, forming a typical warrant + placement arbitrage structure.

Image source: crypto-economy

Specifically, these warrants generally have the following characteristics: extremely low pricing: far below the public market share price, creating potential arbitrage opportunities; phased unlocking: some warrants unlock upon financing completion, while others have price triggers, time-based rollover mechanisms, and other mechanisms; and potential dynamic execution based on market prices: when the stock price rises above a certain threshold (such as 2-3 times the PIPE pricing), forced exercise or accelerated conversion clauses may be triggered.

Under this structure, VAPE's stock price behavior is driven not only by fundamentals but also by the behavior of PIPE investors. Once valuations deviate from actual asset levels, this structure creates a strong incentive to cash out, becoming a source of liquidity shocks.

So, when it comes to stock prices, will they rise or fall?

We analyze VAPE based on existing PIPE cases. This structural game unfolds roughly in three stages:

Phase One: Expectation-Driven Stage (Already Occurring)

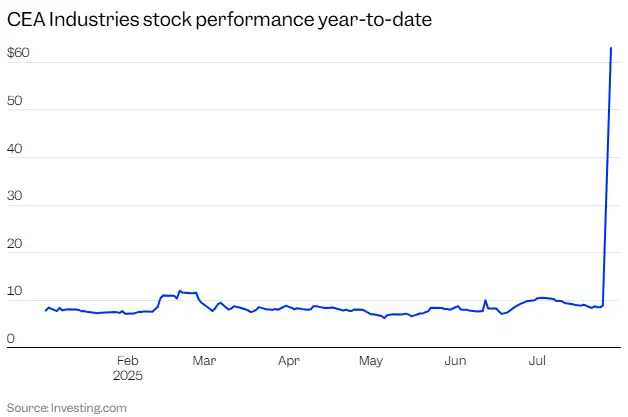

Following the PIPE announcement on July 28, VAPE's stock price soared 800% in pre-market trading, from $8.88 to the $80 range, triggering multiple circuit breakers. At this point, the market wasn't focused on fundamentals, pricing solely on the narrative expectations contained in the announcement, fostering intense speculative sentiment.

Since financing has not yet been received and warrants have not been unlocked, the market is experiencing a "low liquidity, high sentiment, and no supply" structure, making the stock price extremely sensitive to expectations.

Phase Two: Structural Release (After Transaction Completion)

After the transaction is completed on July 31st, funds will be in place, and some PIPE investors will receive initial shares and transferable warrants.

At this point, the market enters a delicate range: If the stock price remains high, warrant holders may choose to quickly exercise and cash out, suppressing the price. If the market loses confidence in the treasury model, early arbitrageurs will exit immediately. If the company discloses that it did not build a BNB position as expected, it will also weaken the expectation of "on-chain NAV anchoring."

During this phase, volatility increases significantly, and pricing shifts from "value anchoring" to "capital behavior."

Phase 3: Valuation Reversion or the Launch of a Secondary Narrative

If BNB performs strongly and the company releases detailed on-chain revenue, the market may refocus on the "Crypto NAV+" model, driving valuations into a secondary rally. If market sentiment cools or PIPE parties continue to cash out, the company's stock price will return to its asset value or enter a liquidity vacuum.

This is also the critical stage at which most PIPE projects ultimately diverge—some entering the secondary, long-term trading model, while others become one-off cases of "storytelling complete, capital exits."

A rise may stem from structural scarcity; a fall often stems from a liquidity stall. Both paths have been repeatedly observed in other PIPE cases. Therefore, the difference between rises and falls is not a matter of value judgment, but rather a competition over the speed of liquidity release.

Shell Company Selection: What Qualities Does VAPE Have?

Tracing VAPE's story back further reveals a completely different starting point.

VAPE's predecessor was CEA Industries, an engineering equipment company specializing in indoor agriculture and cannabis temperature control systems. Its subsidiary, Surna, primarily provided services such as LED lighting, air circulation, and hydroponic equipment, primarily targeting North American cannabis growers. The company has long suffered from the "three lows" of low growth, low profits, and low market capitalization.

According to data from StockAnalysis and TipRanks, the company's annual revenue will be less than $6 million by the end of 2024, its market capitalization has consistently hovered below $10 million, and its US stock float is extremely low.

In 2024, the company attempted its first strategic transformation: acquiring Fat Panda, a central Canadian vape chain, for $18 million Canadian dollars. Fat Panda had 33 stores, generated over $38 million in annual revenue, and had an EBITDA margin of nearly 21%. This was an attempt to shift from a "hardware vendor" to a "end-user retailer," marking VAPE's transition from a device supplier to a consumer brand.

However, this was not enough to justify a revaluation of the company.

Thus, VAPE was previously unattractive, even considered a "capital market slumber." However, these very flaws, often criticized, have become the most valuable attributes of a "shell company": a sufficiently small shell; a sufficiently clean equity structure; a market capitalization potential that needs to be activated; and a narrative vacuum in the crypto market (BNB exposure).

Whether VAPE can become a "MicroStrategy for BNB" remains to be seen. But one thing is certain: it's no longer the e-cigarette company it once was. Instead, it's become a programmable shell nestled in the game of capital—the shell a US-listed company, the core a structured financial instrument, and the soul the ability to manipulate narrative and emotion.

Control and the core team: Who is driving this financing?

Behind this transformation experiment of "trading assets for valuation," VAPE plays the role of a financial vehicle, not an operating entity. The true driving force behind this transformation is a team focused on capital structure—a mixed team with backgrounds in finance and crypto. Their goal isn't simply to secure a financing round, but to build a self-consistent valuation cycle: from primary placements to building on-chain asset positions, and finally releasing a narrative in the secondary market. After the PIPE was signed and implemented, the company's control structure shifted significantly. The original management team, primarily from industrial and retail backgrounds, lacked the capabilities to lead on-chain treasury and structured asset management. True control gradually shifted to the financing lead—10X Capital and YZi Labs. 10X Capital, the lead institution in this PIPE, has long focused on SPAC mergers and acquisitions, cross-border capital arbitrage, and structured transactions, and is a classic "leveraged capital engineer." Since 2023, the team has attempted to expand the MSTR model to ETH, SOL, and even LSD. Their recent bet on BNB clearly aims to replicate MicroStrategy's treasury + valuation compounding structure. YZi Labs: The strategic advisor for this round of transactions, widely believed in the industry to have direct ties to the CZ Family Foundation, is a key force behind the treasuryization of BNB and its path to a public company. This firm's endorsement is almost seen as explicit support from the Binance camp. In the VAPE project, it participated in the early screening of shell companies, assisted in media coverage, and collaborated with some investors and the market making team to develop a narrative strategy of "position building, exposure, and valuation derivation." The most significant characteristic of this capital structure is that VAPE is no longer the creator of value itself, but rather a platform for value release. 10X Capital provides the structure and pacing, YZi Labs provides the narrative and channels, and BNB is embedded as the underlying asset. Together, these three parties complete a closed-loop design from the asset side to the market side. Whether this story holds true ultimately depends on whether on-chain positions can be realized and whether market confidence can be sustained. For most retail investors and onlookers, the emergence of vape isn't the end, but rather the prelude to the accelerated arrival of the "era of structural arbitrage."

Image source: bankless

Epilogue

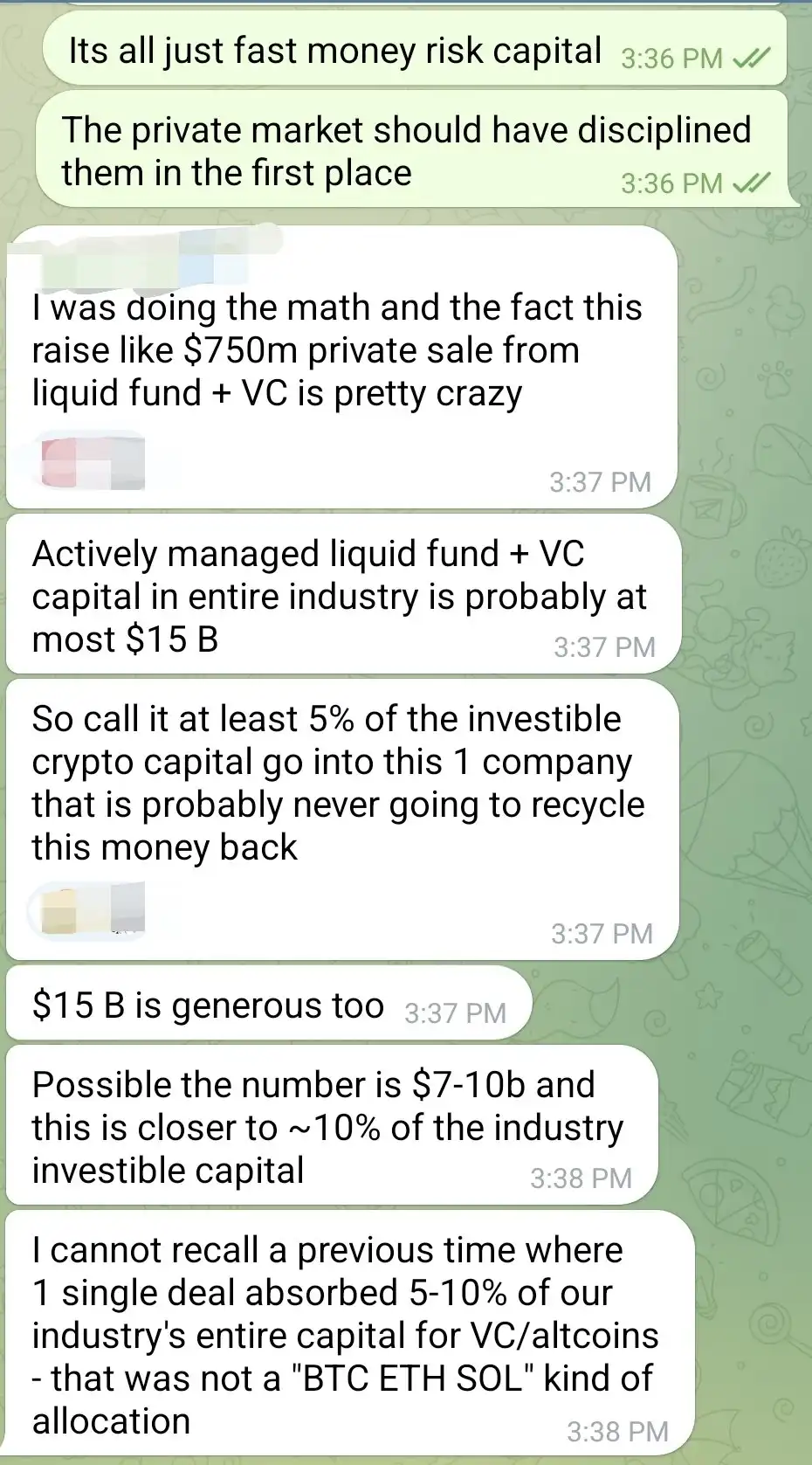

In a Telegram conversation between investors, someone calculated that the total active capital available for VC and liquidity funds in the entire crypto industry might be only $7-15 billion. The maximum financing amount of VAPE’s PIPE this round is expected to be US$1.25 billion, which will absorb about 5-10% of the industry’s investable capital in extreme cases.

"I've never seen a project other than BTC/ETH/SOL siphon off so much capital in a single deal," he said. "And this company will likely never recycle this money back into the industry."

This isn't just a risky issue of excessive capital concentration; it also means that the already tight liquidity in the crypto industry is being "siphoned off" by an unproven model.

During a bull market, liquidity should be used to fuel diverse innovation and provide resilience for early-stage projects like DeFi, payments, and infrastructure. Today, this capital is concentrated on a "story shell" of nested PIPE structures and shell resource speculation. If VAPE succeeds, it will undoubtedly replicate more crypto MicroStrategies; but if it fails, it could become a classic example of industry-wide resource misallocation.

Capital shapes narratives and also creates bubbles. In the intersection of crypto finance, everything looks like a victory for structural arbitrage, until liquidity completely dries up, revealing its ability to generate revenue.