In the past two years, TON (The Open Network) has transformed from silence to explosion at an astonishing speed. Relying on Telegram's hundreds of millions of user base, it has quickly established a strong presence in the crypto community. Gamified ecology, robot economy, Stars payment system, official voice - TON's narrative tension was once full. However, in the face of the reality of coin price fluctuations, market value declines, and declining activity, TON has also exposed its deep-seated structural problems: concentrated chips, homogeneous ecology, and weak infrastructure.

This article will systematically sort out TON’s chip distribution, token economy, user and capital flow, development ecology and TAC architecture, and try to answer a core question: Does TON’s short-term prosperity have the structure to support its long-term value?

TON chips are extremely concentrated: the rift between whales and retail investors

TON is a project that did not have a smooth start. From the beginning, it was burdened with structural problems such as huge chip concentration and historical miners' lock-up, and now it is trying to reshape itself with these "sunk costs". We can get a glimpse of the true picture of its ecological development from its chip structure, token trend and capital flow.

The history of TON has resulted in most of the chips being in the hands of a few miners. TON officials have made up for this problem through OTC: TON was created in 2018 and was banned by the SEC when it was preparing to issue coins and launch the main network in 2019. The project was officially terminated in May 20, but was restarted by the developer team new TON. TON coins were also mined by POW during this period (as of June 22) and have now been transferred to POS.

Due to the suspension and being taken over by the development team, in June 2020, 98.55% of the total supply of TON can be used for mining until the mining ends on June 28, 2022, which means that most of the tokens are in the hands of early miners. The TON project has launched a discounted bulk purchase service for tokens from early miners. At the same time, if whales lock tokens for a long time (4 years), they can get 6-7% APY;

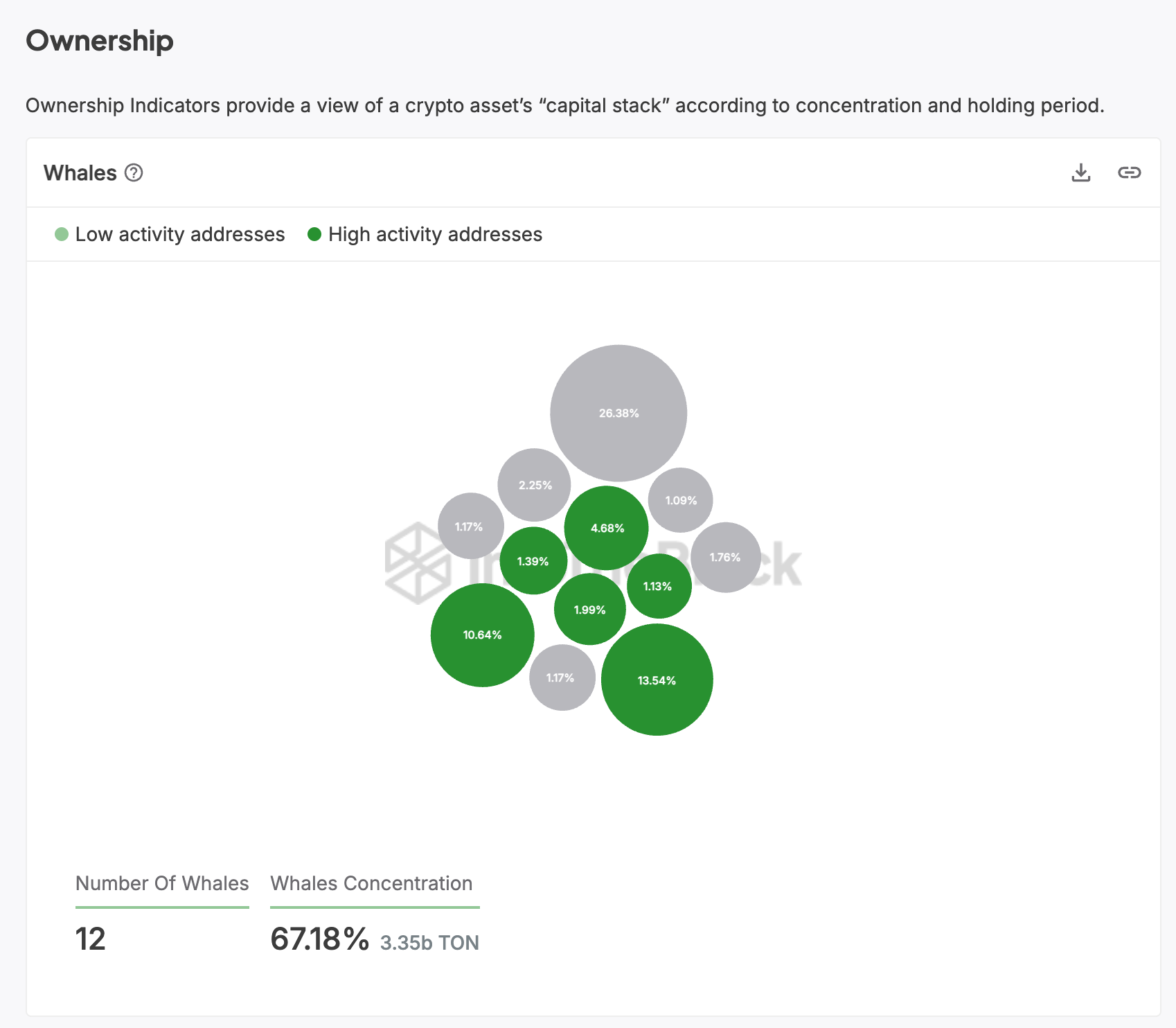

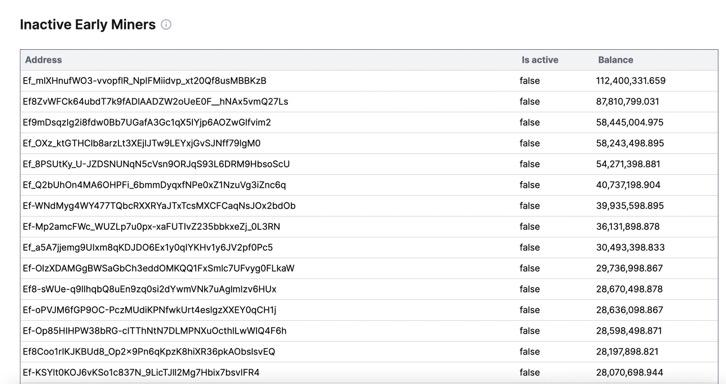

Whales on TON are frozen/inactive miners : According to data from into the block , there are 12 whale addresses that own more than 1% of the total supply, of which 6 are low-activity addresses (addresses with less than 300 transactions in their lifetime). According to the community TON vote, the whale addresses marked as "frozen" are inactive early miner addresses, which can be seen in https://tontech.io/stats/#/early-miners. There are 171 addresses in total, locking 1081m of TON;

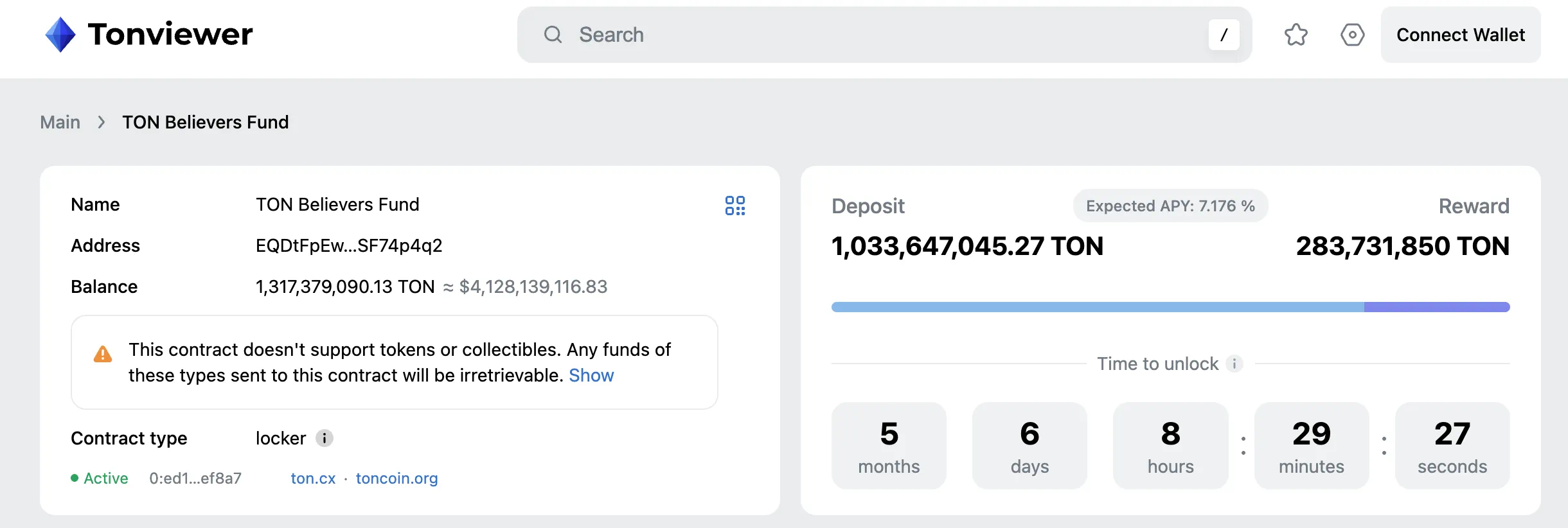

The assets of the address marked as "TON Believers Fund" are confirmed to be frozen until October 12, 2025. Data shows that a total of 1,317 mTON (accounting for about 52%) are locked. In order to stabilize the selling pressure, the APY given to these frozen assets is as high as 7.176%;

TON chips are severely unevenly distributed

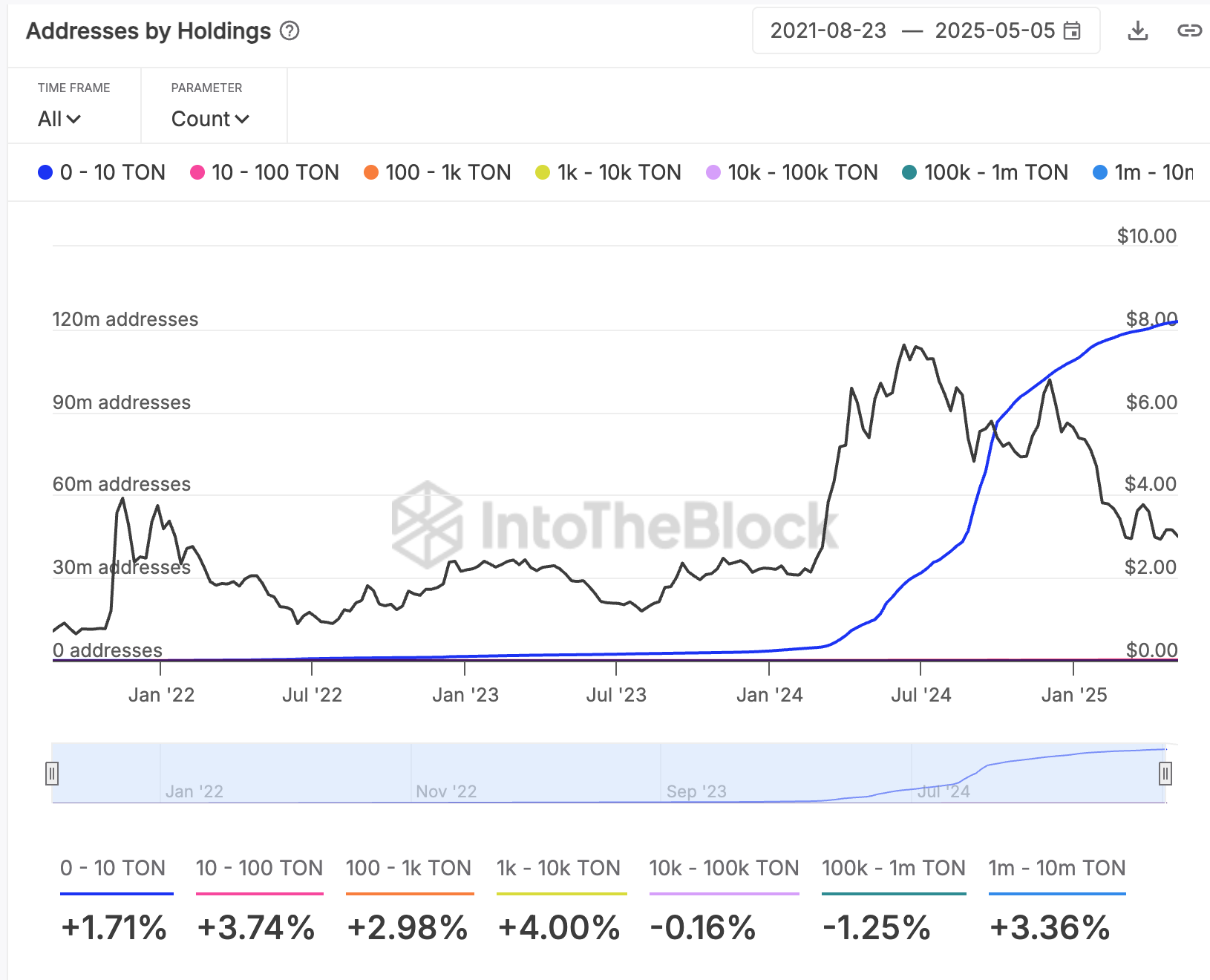

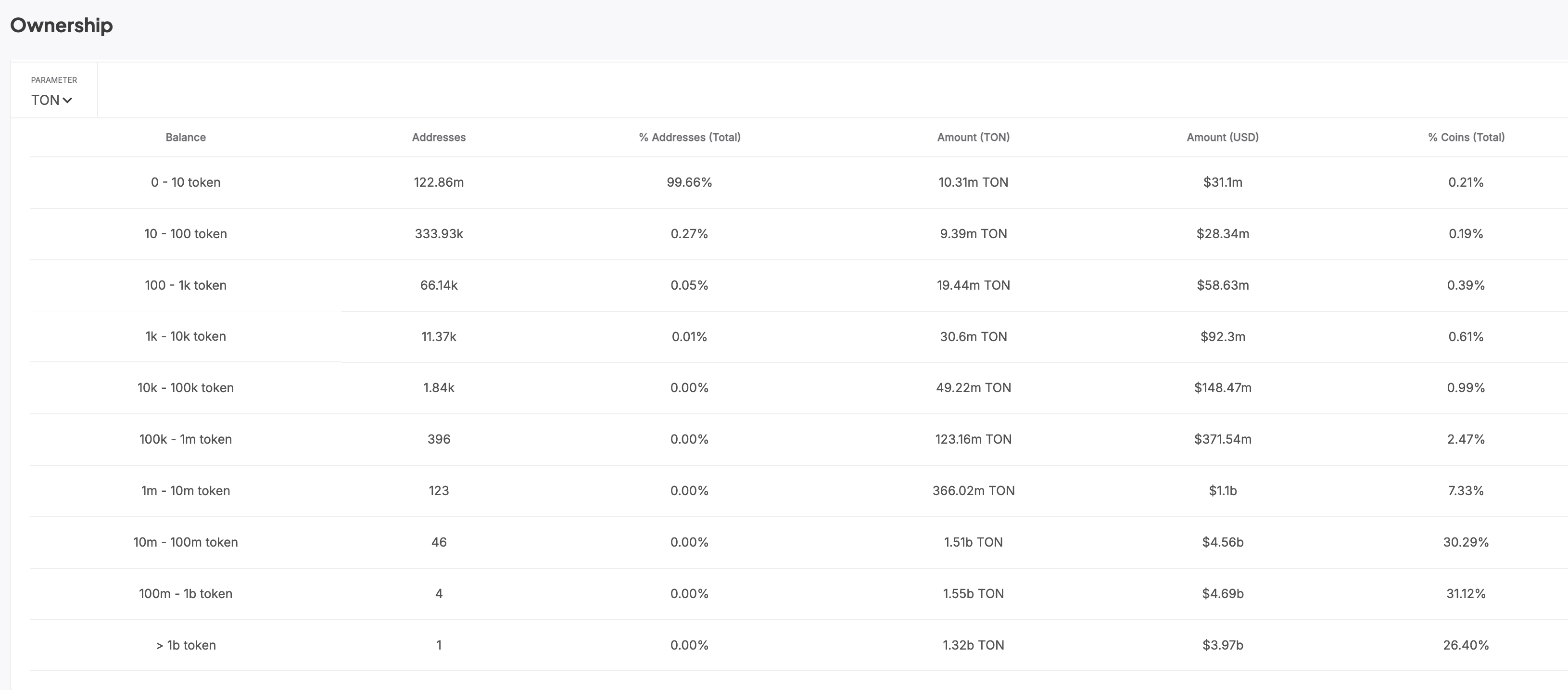

TON is severely polarized, with users holding less than 100 TON accounting for nearly 99.9%. Retail investors have been pouring in since March 2024 : According to Addresses by holdings data , there are currently about 123m addresses holding TON, most of which (122.54m) still only hold less than 10 TONs. Among them, those holding more than 100K TONs were all 500+ before March 2024, and slowly climbed after March, reaching a peak of 1.3K in August 2024. However, the latest data shows that the number of large holders has decreased as the popularity of TON has declined, and is currently around 600.

According to data from into the block : although there are many addresses with less than 1K TON, they only account for a little over 1% of the total tokens.

TON

TON  The situation of blockchain is different from that of other public chains. They need to build a development path that suits them under the constraints of history.

The situation of blockchain is different from that of other public chains. They need to build a development path that suits them under the constraints of history.

TON valuation drops, but upside remains

TON Price, Market Cap, and Liquidity

There are several major rising nodes in the price of the currency :

1⃣️, 2⃣️Listed on an exchange + official support : In November 21, TON was launched on a centralized exchange and received public support from the founder of Telegram;

3⃣️: At the end of February and the beginning of March 24, the overall transaction volume increased significantly, and there was a large inflow of funds. On the one hand, Mirana Ventures invested $8 million in March to support TON, on the other hand, the number of TG users exceeded 900 million, and there was news of IPO;

4⃣️: June to late July 24. Then the arrest of CEO Durov on August 25 caused a drop (about 20%).

According to CMC data , the TON coin price ATL September 21, $0.5194; ATH: June 15, 24, $8.25.

Over the past year, TON tokens have fallen more than 50% from their peak, and their market value has shrunk significantly. At the same time, the total locked value (TVL) of the TON ecosystem has also suffered a sharp decline, from a peak of more than $770 million to today's $140 million, a drop of nearly 80%.

Although the price of the coin has been cut in half from its high point, TON still has room for recovery in terms of market value. The key lies in whether it can transform the popularity of the ecosystem into long-term value : As of May 11, 25, the market value of Ethereum is 306.36B USD. If ETH wants to achieve an annual growth of 10%, it will also need an additional capital inflow of about 30B USD. In comparison, SOL currently has a market value of 91.93B USD. To achieve the same growth rate, it will require 9 billion USD. The current market value of TON is 8.64B USD. Although it has dropped by 65.65% from the highest market value of 25.17B in 24 years, it still shows that it has a lot of room for growth.

TON's market value rose in several stages, from $4B in mid-July 2023 to $7B in early 2024, and then to around $13B (FDV$27B) in August 2024 when it was at its peak. The market value almost doubled every six months. However, the current market value has fallen back to around $8B (FDV$17B).

From November 2022 to June 2023, the construction of the TON ecosystem brought about an increase in market value, which was almost stable at around $3B;

From June to August 2023, TG bot became popular, and from July to August, TON integrated a built-in wallet and launched the TAPP application center. Therefore, the enthusiastic attention to the bot ecosystem and the development of the ecosystem brought about an increase in the ecological narrative of TON itself.

Since March 24, the market value has soared due to financing and continued ecological construction;

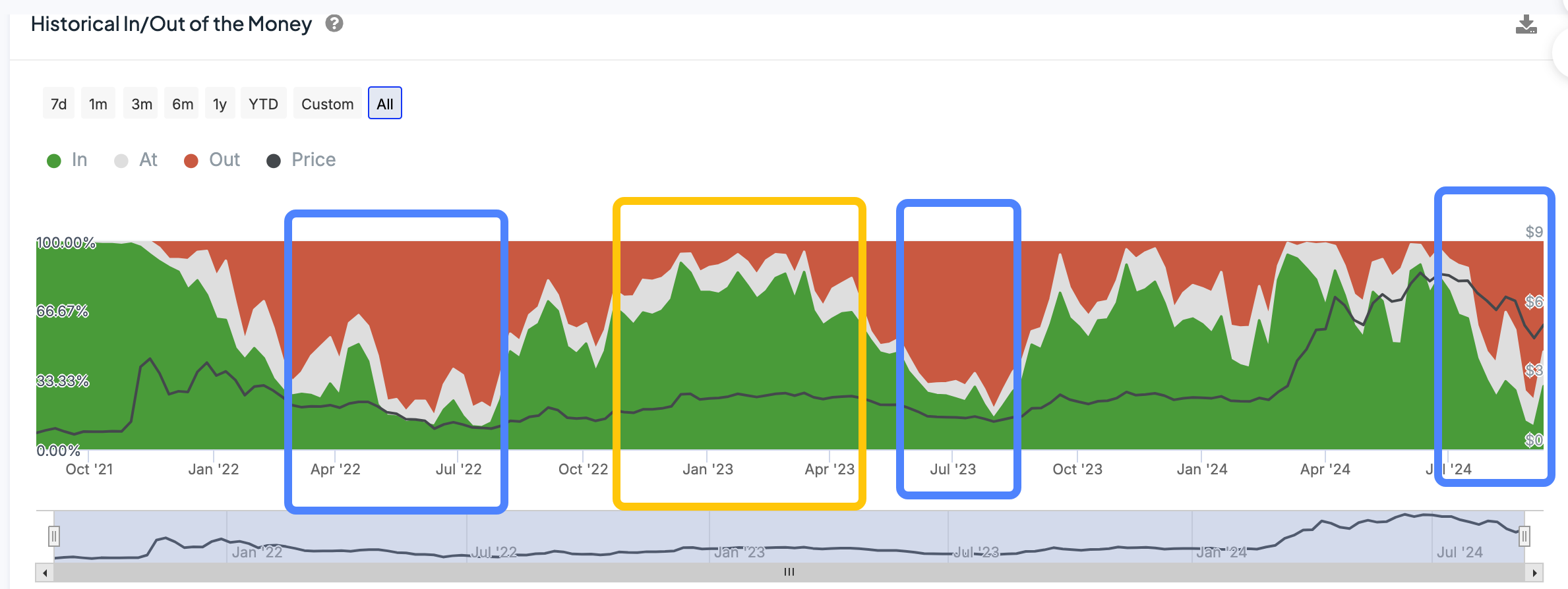

Liquidity inflow/withdrawal history: According to the data from into the block , from the entire time range, the time nodes for large-scale shipments are April-June 2022, June 2023, July 2024, and now April-May 2025. In addition, the end of 2022 and the beginning of 2023 are the times when a large amount of funds flow into TON;

On May 29, 2024, Durov sold 2,564,103 TON OTC, but it did not affect the price of TON. Prior to this, Durov had been selling TON intermittently since mid-March;

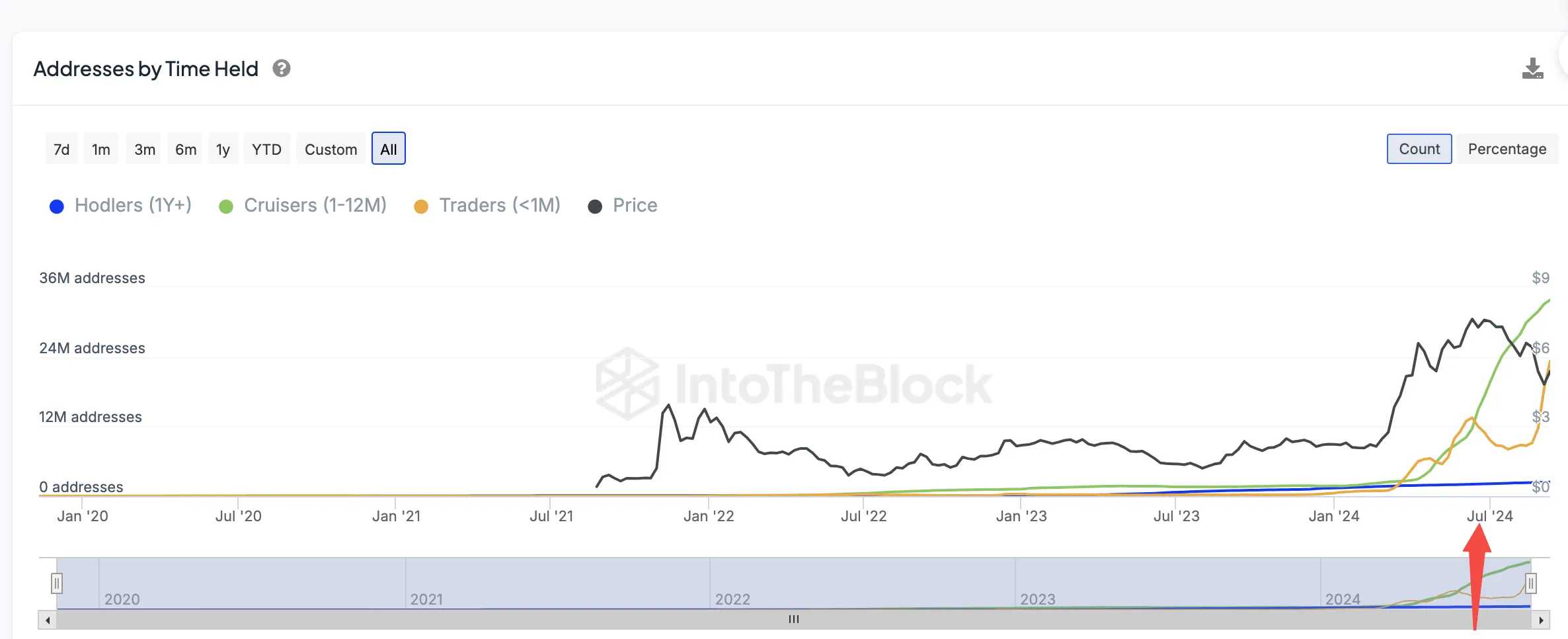

Since June 10, 2024, the price of the coin and the number of short-term traders have continued to fall, and the number of people holding for less than one year has increased. It can be seen that most of them entered the market in June 2023 (buying TON shipped) and continued to hold positions when the price of the coin fell (being trapped);

TON inflation is controllable, and application scenarios need to be expanded

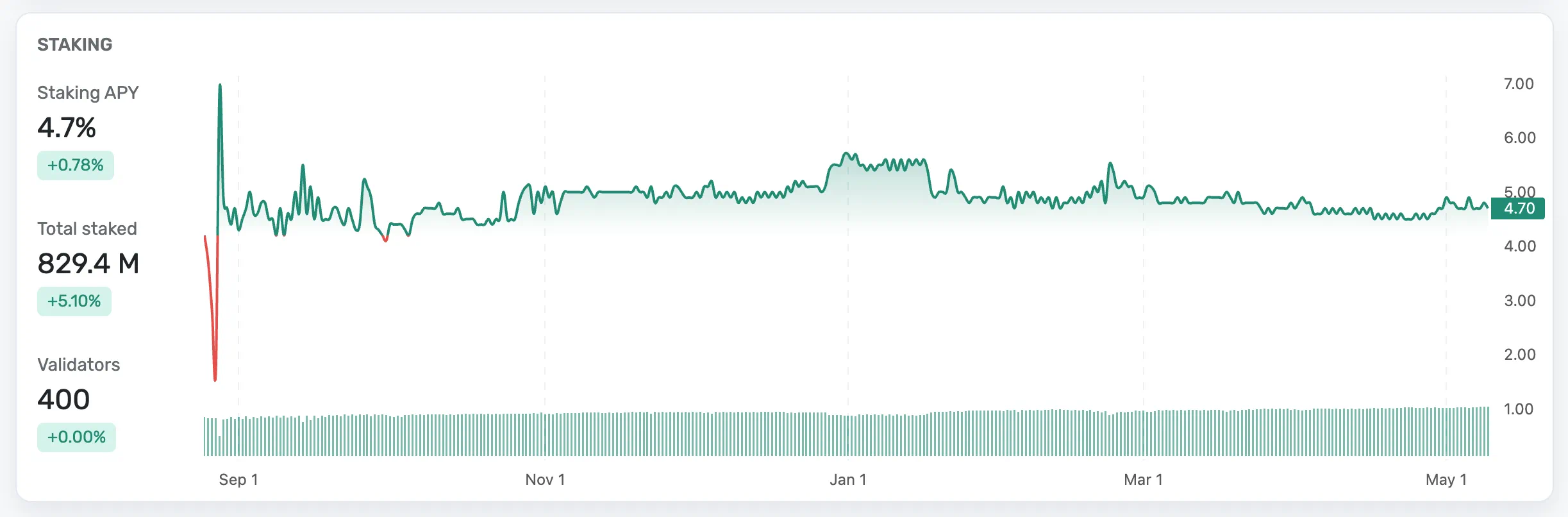

Token supply: The initial supply of TON token is 5 billion, with no upper limit, growing at a rate of about 0.6% per year (about 30 million). The token is used to reward validators. If the validator behaves improperly, the staked tokens will be slashed. Currently, about 4.7% APY can be obtained by staking TON.

Token Utility: Smart contract transaction processing fees, payment platform application services, pledge, cross-chain transactions, TON governance and storage services, and in the future, payment for TON proxy services. Currently, you can directly purchase TON with a credit card, and then purchase virtual goods such as anonymous accounts;

Token Utility: Smart contract transaction processing fees, payment platform application services, pledge, cross-chain transactions, TON governance and storage services, and in the future, payment for TON proxy services. Currently, you can directly purchase TON with a credit card, and then purchase virtual goods such as anonymous accounts;Currently, TG has launched the Telegram Stars transit solution to comply with Apple and Google's supervision and improve user usage. The official has linked the core of its future ecology (advertising, fund transfer) to the TON ecology: Telegram Stars was launched to support the payment of digital goods and services throughout the Telegram ecosystem. Users can obtain Stars through Apple and Google's in-app purchases or PremiumBot, and then use them to purchase digital products provided by robots, such as e-books, online courses, and items in Telegram games.

TG stars is TON's solution for gradually transferring web2 users into crypto, and can be topped up directly with a credit card:

For users: easy to use, only requires credit card purchase, no encryption involved;

For merchants: cash withdrawals must be made using TON (some people describe it as crypto grift, which is only useful when cashing out);

For TG: using stars instead of real currency to follow Google Play/App Store rules, while on the other hand it can be converted into TON;

App stores will support it in the future, and the official statement is that Telegram Stars is the only payment channel for digital goods. The official statement is that Telegram Stars is just the beginning. Future updates will bring more functions and features to Stars, such as providing gifts for content creators, micropayments, etc.

However, TG officials linked the two most important parts of MKT - traffic generation and withdrawals - with TON: 1) Tons must be topped up before advertising can be placed; 2) Developers must withdraw earnings through TON, which means that the "beginning" and "end" of the product are surrounded by TON .

The reality after the TON traffic ebbs: the pain of ecological transformation

TON is currently crowded and the official no longer focuses on the game ecosystem, but on the payment side : there are only 20 subcategories for 1,000+ projects, but there are actually only 5 major categories, such as NFT-related (120+), game-related (700+ including gamble), trading (CEX, wallets, bridge), social (channels, chats, etc.) and tools (explorers, dev tools, VPN, launchpad). It can also be seen that TON is not currently focusing on the previously popular game ecosystem, and the game category is even the second to last category on the official website classification page.

However, there is a lack of products in other categories : except for games and memes, other tracks are generally less well-known. Even in the shopping category, there are problems such as single user base (only supporting Russian-speaking areas) and basic functions (mostly helping TON payments).

The continued decline in activity on the TON chain is clearly revealing the decline in the economic vitality within its ecosystem. Both user participation and transaction frequency have fallen, reflecting the obvious weakening of the ecosystem's growth momentum.

This dilemma stems from the interweaving of multiple factors. On the one hand, TON relied on Telegram's traffic dividend in the early days to quickly attract users with mini-programs and "Tap to Earn"-type mini-games, but failed to establish an effective user retention and value precipitation mechanism. After the wealth-creating effect faded, user interest dropped sharply and the traffic dividend quickly dried up.

On the other hand, the TON ecosystem narrative is relatively single, mainly focusing on social networking and games, and lacks in-depth layout of diversified tracks such as DeFi, AI, and DePIN. According to DeFiLlama data , there are only more than ten projects on TON with a TVL of over 10 million US dollars, among which Tonstakers stands out. The concentration of ecological projects is high, and the problem of unbalanced development is prominent.

In addition, TON's unique development architecture and programming language are not developer-friendly, which limits the efficiency of project incubation and innovation, and further weakens the vitality of the ecosystem. Although Mini Apps has seamless authorization and payment integration functions, and can theoretically reach 950 million Telegram users, the ecosystem is actually highly concentrated on games and NFTs, and general applications such as tools, payments, and infrastructure are still scarce.

If TON cannot get out of the path dependence on short-term popularity and expand the application scenarios that can be implemented from TON tokens, it will be difficult to precipitate into sustainable on-chain value. Once the traffic dividend fades, what can truly support the ecology must be the structural health and diversified capabilities of the project. Judging from the current ecological structure of TON, the pressure of transformation is gradually emerging.

Where are TON’s users and developers?

TON users surge, but activity declines

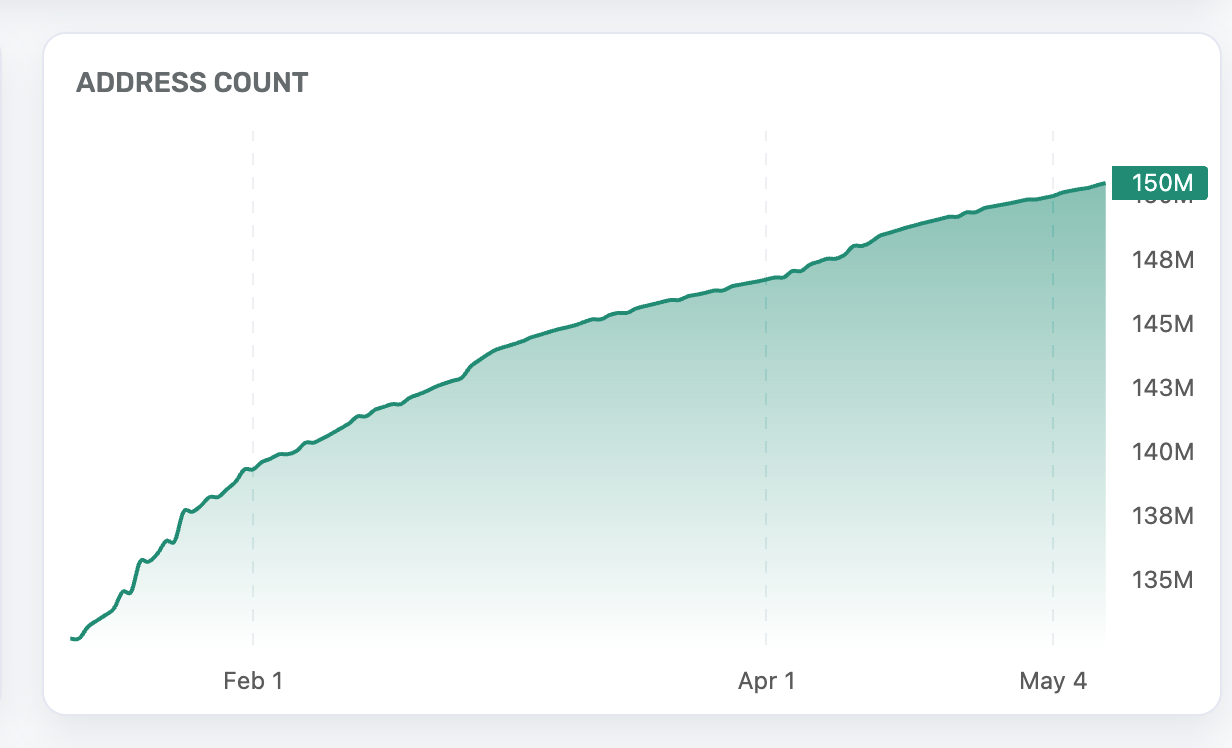

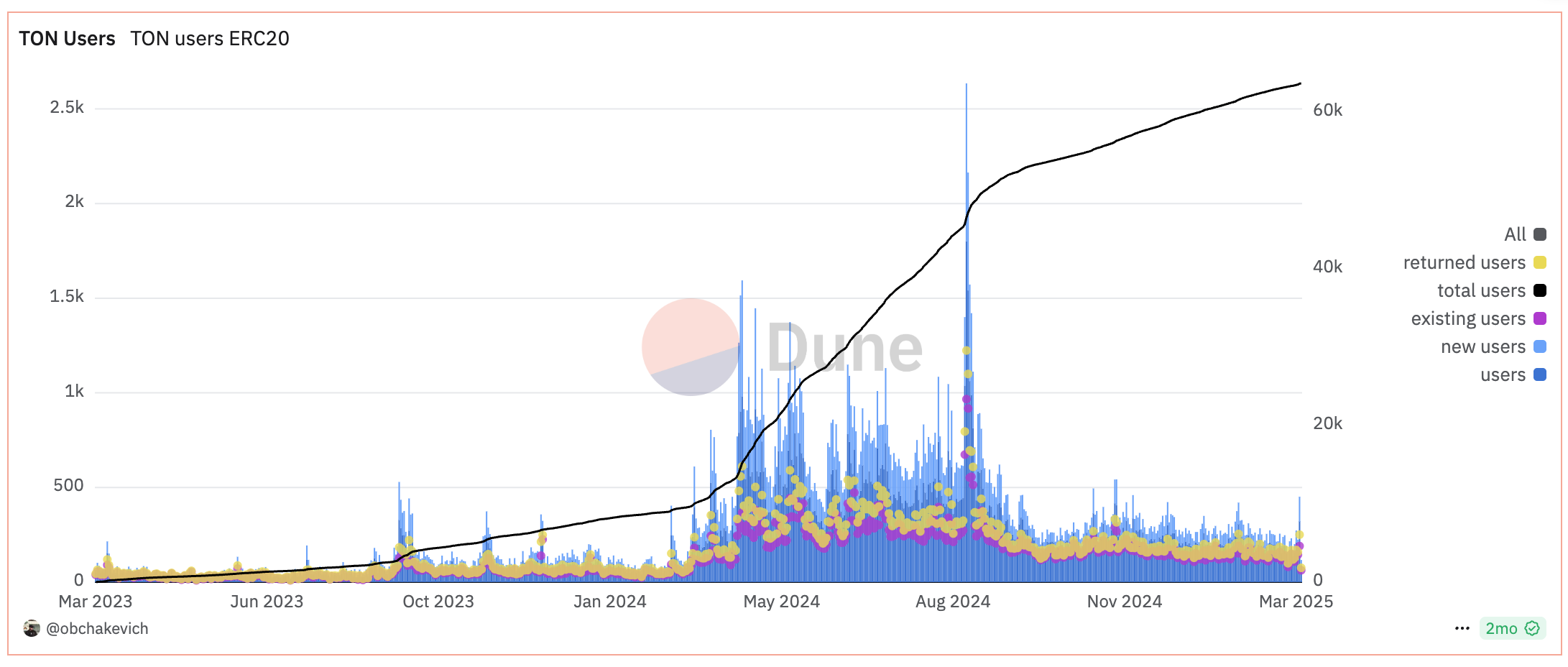

TON users are growing fast : According to tonscan data, from mid-May to early September 2024, TON's addresses increased from 20m to 70m users, of which the number doubled in August alone (45m-70m). From September 2024 to date, TON's addresses have doubled again, and currently there are 150m users, which is a very rapid increase;

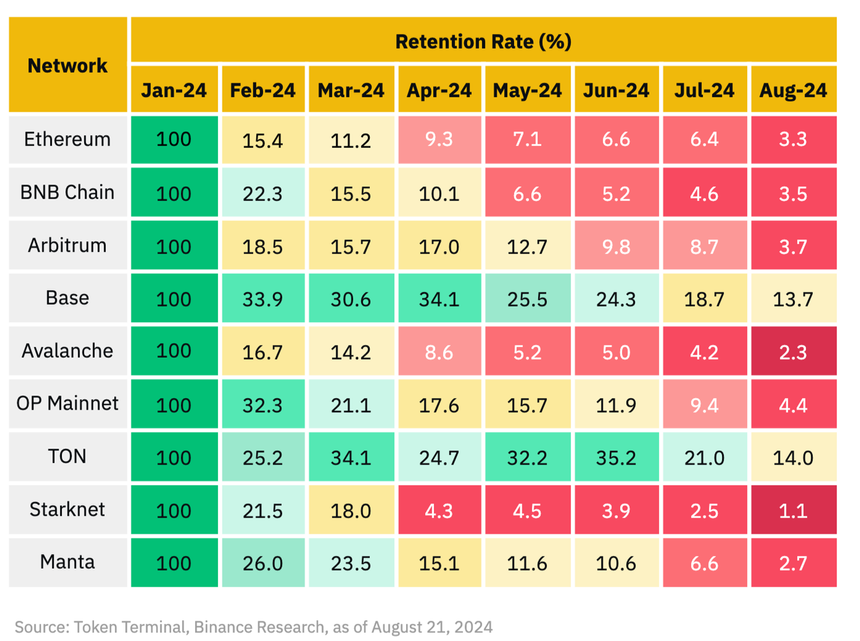

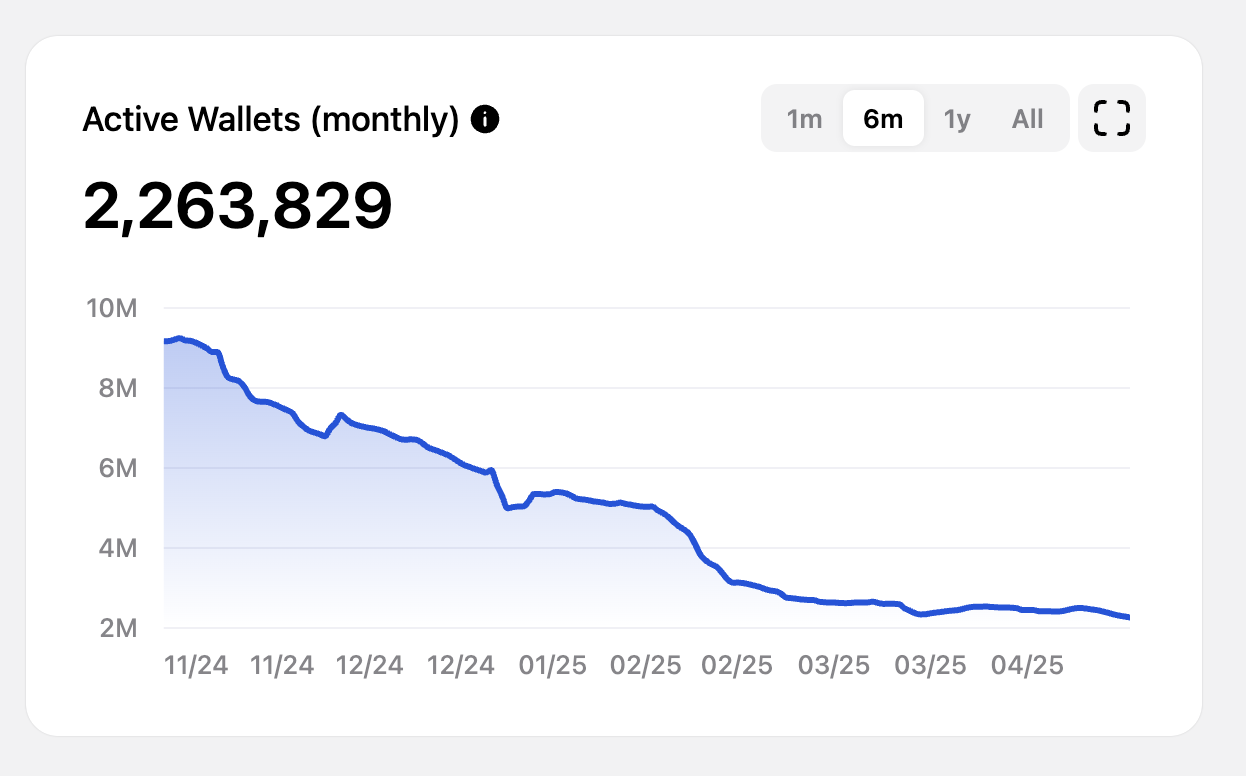

TON has strong user stickiness, but the number of active addresses has dropped significantly as the ecosystem has become less popular: According to Binance's 24-year report "Web3: The Household Name in the Making", the average retention rate of each chain is 5.4%, and TON has the highest retention rate among all well-known public chains. The reason is simple: it is more focused on building a strong consumer ecosystem and has a solid product-market fit. Currently, the number of active addresses of TON last month is 2 million (30,000 daily active addresses). Compared with the monthly active addresses of over 10 million at the end of 24, the current data has dropped significantly, considering that the market's attention and funds have shifted to other ecosystems.

TON transaction volume has dropped significantly compared to before, but it is generally stable : According to tonscan data, TON's transaction volume has been an average of 4 million transactions per day at the end of 24, and the current transaction volume has dropped to 2.5 transactions. In comparison, the number of daily transactions on the BTC chain is between 300,000 and 400,000, and ETH is between 1.1 million and 1.3 million, which has been very stable.

TON developer ecosystem is under pressure, infrastructure needs to be strengthened

The small number of TON validators leads to a certain degree of centralization : the current number of TON validators is 400, an increase from 361 at the end of 24 years, distributed in 26 countries, with a stake of nearly 700 million TON, accounting for 12% of the total tokens and 28% of the circulating tokens;

The problems with the TON network are: 1) TON has high hardware and network requirements for validators. To become a validator, you need to stake at least 300,000 TON; 2) There are not enough validators. Compared with other PoS public chains, the number of TON validators is significantly smaller. Currently, the TON network has only 400 validator nodes, while the number of Ethereum validators has exceeded 1 million, and the number of Solana validators is far more than TON.

This difference in the number of validators results in each validator having to process more transaction requests (centralization). When the transaction volume increases suddenly, the validators may not be able to process all transactions in time, resulting in block delays or even interruptions (this may be the reason why TON blocks were suspended after Durov was arrested): On August 28, the TON blockchain experienced two interruptions in one day, totaling 10 hours.

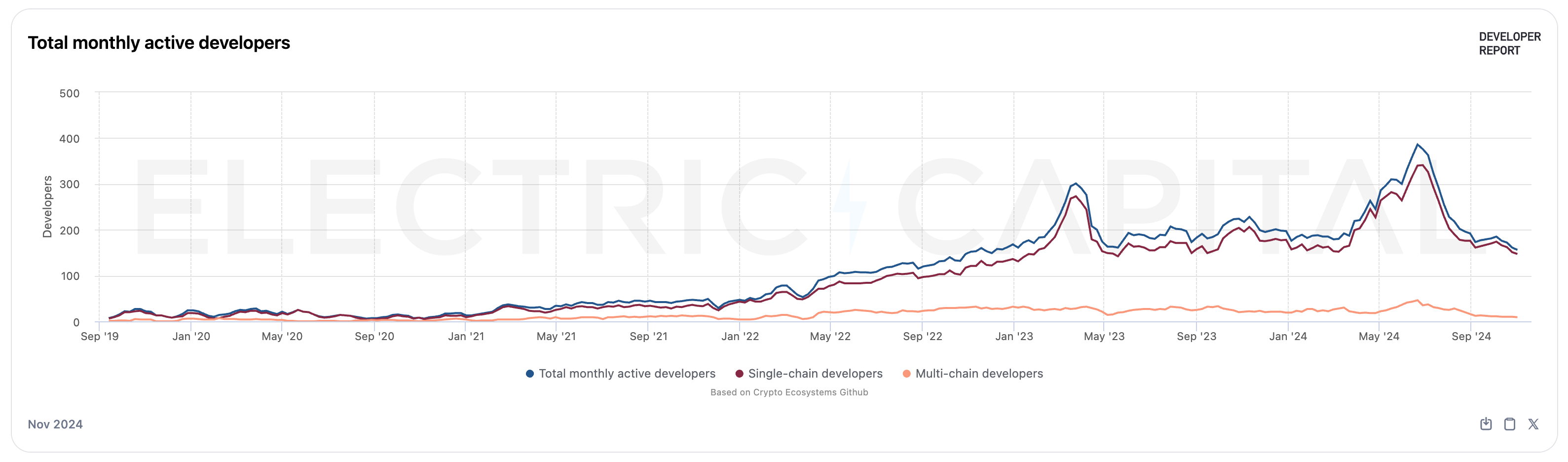

The number of developers is stable, but has declined: many developers come from Telegram, and most of the core devs come from South Korea and Russia. They are characterized by strong technical capabilities, but average product experience. According to the data from the development report , as of May 2025, there will be 30 full-time developers on Ton (daily code increase or decrease of 10+), and 150+ monthly active developers, which is 100 less than at the end of 24. Compared with other ecosystems, the number is average (ETH is up to 2000+, and others such as polygon, arbi, and Solana are between 500-600);

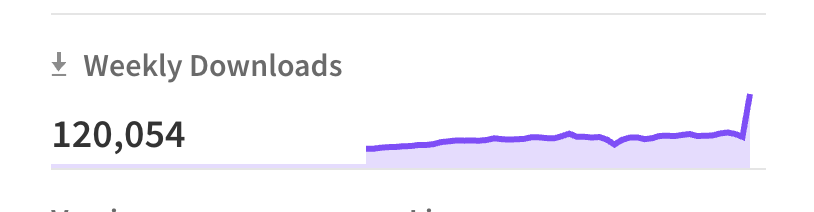

TON Connect SDK is a must-have SDK for developers to connect to the TON ecosystem (connect your app to TON wallets via TonConnect protocol). Its download volume has increased from an average of 10,000 per week in early 2024 to over 25,000 per week in August 2024, when the ecosystem was booming, to an average of 12,000 per week now.

TON’s growth shows a typical “user-first” feature, but this also masks the problems of unstable ecological foundation and insufficient developer support. If TON does not continue to find a sustainable development direction that can adapt to TG applications, it will be difficult to compete with other public chains.

The future of TON: towards compatibility and connectivity

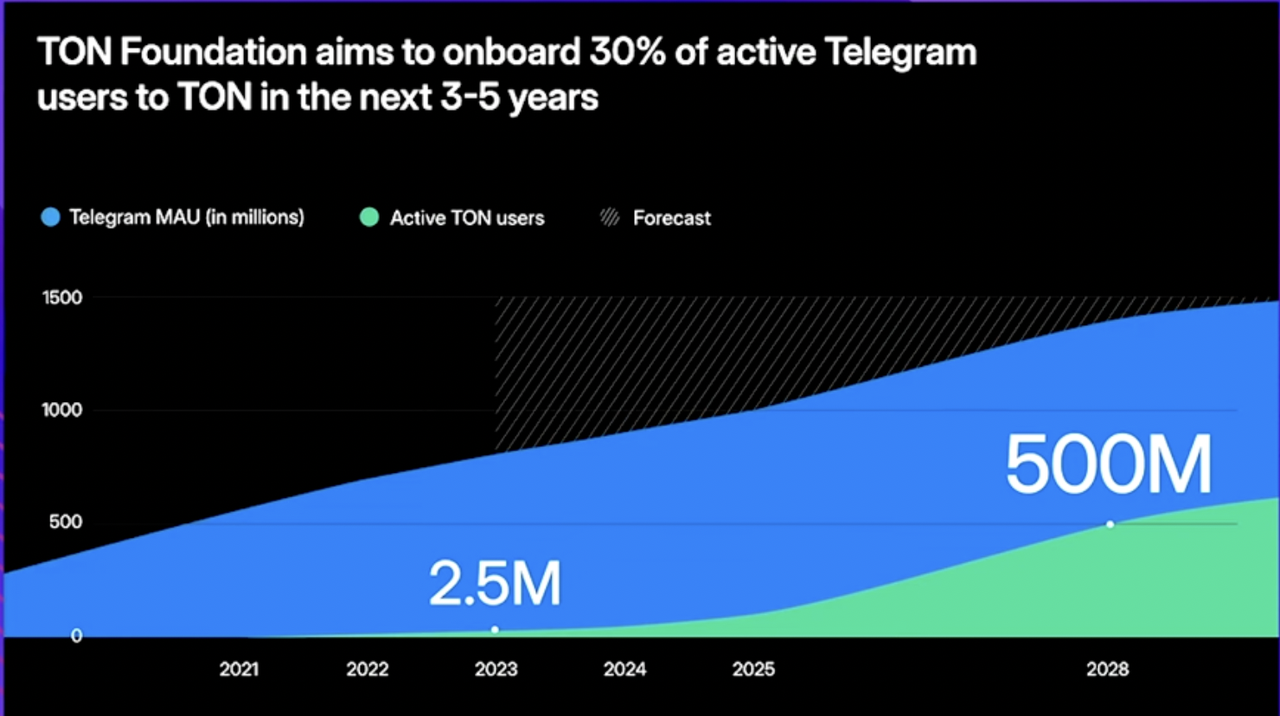

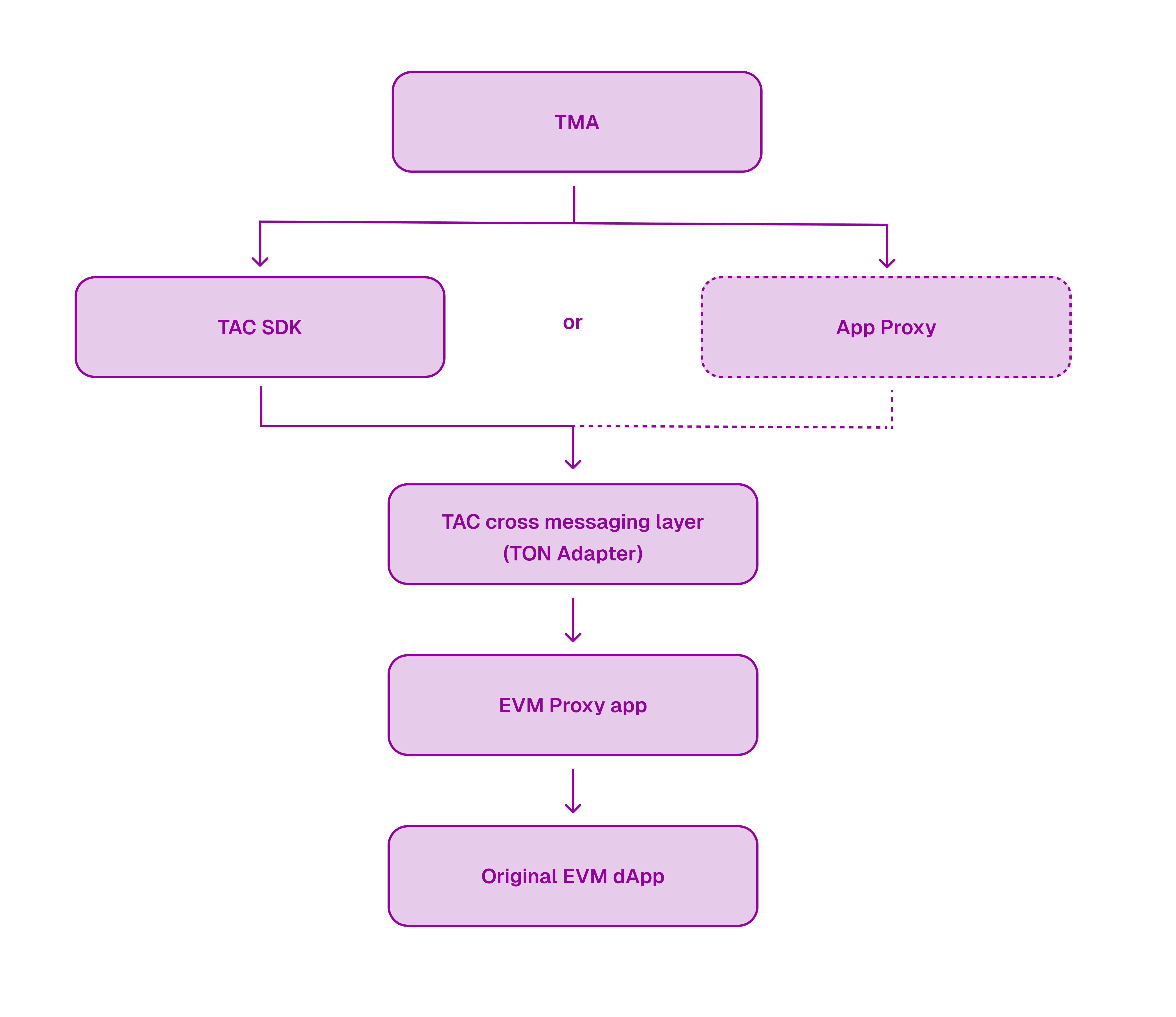

Although TON has a huge potential user base, the development of its ecosystem faces a significant obstacle: incompatibility with mainstream Ethereum Virtual Machine (EVM) applications. Among them, TAC, as an independent project designed for EVM dApps, is committed to providing a channel for it to access the ecosystem of more than 1 billion users of TON and Telegram.

TAC is a TON network extension that connects TON with EVM-compatible applications to create a unified experience for users and developers. With TAC, users can interact with any EVM application using the TON wallet, and developers can migrate EVM applications to TON without rewriting code or learning a new framework.

Its core is not a compatibility layer, but an independent EVM public chain, built by Cosmos SDK + Ethermint, using dPoS consensus and achieving BTC pledge security through Babylon. This chain supports full EVM smart contract execution and is the "EVM native zone" on TON.

Cross-chain communication is handled by TAC's sorter network. Each cross-chain transaction must first reach a 66% consensus in the sorter group, and then undergo cross-group verification to ensure that the message is delivered securely and the process cannot be tampered with.

The entire process is supported by the Proxy smart contract system: the Proxy contract on TON is responsible for initiating messages and locking assets, and the Proxy contract on the EVM side (written in Solidity) receives messages and completes the interaction. For users, the entire cross-chain process is transparent, and the experience is like using a native DApp.

TAC also enhances economic security through a staking mechanism. Sorters and validators need to pledge assets to participate in verification, and they will be rewarded for good behavior and punished for bad behavior, thus ensuring stable and efficient network operation.

In general, TAC is not a bridge, but more like a native high-speed channel from TON to EVM, which expands the ecological boundaries of TON and allows Web3 users to truly "carry only one wallet and travel around the world" between multiple chains.

In general, TAC is not a bridge, but more like a native high-speed channel from TON to EVM, which expands the ecological boundaries of TON and allows Web3 users to truly "carry only one wallet and travel around the world" between multiple chains.The actual application logic of TAC is not complicated. The following is a real scenario showing how a user completes a token exchange operation on EVM DEX through the TON wallet - TON users exchange tokens on EVM DEX: 1) The user connects the DEX front end with the TON wallet and chooses to exchange tokens; 2) The TON Proxy contract locks assets and generates cross-chain messages; 3) The Sequencer network performs verification and consensus; 4) The EVM Proxy contract receives the verification message and completes the exchange logic; 5) The transaction result is returned to the user wallet through the reverse path.

The story of TON is not a simple "surge" or "collapse". Its past is the sedimentation of the decentralized restart after the SEC ban, the chip structure is complex, and the ecological narrative relies more on Telegram's platform capabilities. Its present has both explosive growth in the number of users and bottlenecks in activity and development support. Its future is betting on the compatibility path opened by the TAC architecture, that is, whether it can access the mainstream world of EVM, build a robust developer ecosystem, and break through the bottleneck of payment and scene landing, which will determine whether TON can truly break out of its own paradigm from the platform dividend.

After the traffic fades, what will really remain is the chain's ability to generate revenue. TON is still at a crossroads.

References

TON's open network dream is hidden in TAC https://www.techflowpost.com/article/detail_25132.html

Telegram founder regains his freedom, TON officially announces $400 million in financing, and the development dilemma may usher in a turnaround https://www.techflowpost.com/article/detail_24472.html