introduction

On June 22, the "Cross-border Payment Pass" service between the mainland and Hong Kong was officially launched. Small remittances between residents of the two places can be made instantly, and there is no need to submit cumbersome business documents to the bank. You only need to enter the other party's bank account or mobile phone number on the mobile APP to operate it. It is indeed very convenient.

A friend asked Lawyer Liu: Since using Cross-Border Payment is so convenient, can I legally withdraw money in Hong Kong and directly transfer it to a bank card in the Mainland, and then spend it in the Mainland? (Note: The term "withdrawal" in this article refers to the process of selling virtual currency and exchanging it for legal currency)

Lawyer Liu wrote this article to make a simple analysis on this matter.

1. What is Cross-border Payment?

According to a report by Hong Kong Commercial Daily, the cross-border payment service is a connection between the mainland's "interbank online payment clearing system" (IBPS) and Hong Kong's fast payment system "FPS", and must comply with the laws, regulations and financial supervision of both the mainland and Hong Kong. The main service targets are residents (individuals) of both places. Remittances from Hong Kong to the mainland (northbound remittances) must be made by Hong Kong identity subjects ; remittances from the mainland to Hong Kong (southbound remittances) must be made by mainland identity subjects .

In terms of quota limits, the upper limit for remittances from Hong Kong residents to the mainland is HK$10,000 per person per day, and the annual limit shall not exceed HK$200,000; remittances from mainland residents to Hong Kong are still based on the foreign exchange purchase facilitation quota of US$50,000 per year.

In the early stage, cross-border payment is free of charge. In the future, the business may be expanded to individual-to-business (P2B), business-to-person (B2P), and even government-to-business (G2B) applications, and fees may be charged at that time. Currently, the banks that carry out this business in the mainland are: Agricultural Bank of China, Bank of China, Bank of Communications, Construction Bank, China Merchants Bank, and Industrial and Commercial Bank of China; the banks that carry out this business in Hong Kong are: Bank of China (Hong Kong), Bank of East Asia, China Construction Bank (Asia), Hang Seng Bank, HSBC, and Industrial and Commercial Bank of China (Asia).

Lawyer Liu also used his own China Merchants Bank to transfer money to his HSBC account in Hong Kong, and it indeed arrived in less than ten seconds. If you transfer 1,000 yuan, you can choose to receive the money directly in Hong Kong dollars without having to buy foreign exchange.

(Remittance interface of China Merchants Bank APP)

(HSBC Bank APP payment interface, showing that the payment channel is the "FPS" payment system)

2. What are the withdrawal modes in Hong Kong?

Since the cross-border payment service is so convenient, can friends in the cryptocurrency circle use it to withdraw money? Before answering this question, we need to first understand the common withdrawal modes in Hong Kong.

The first is offline OTC stores. Mainstream virtual currencies can be directly exchanged for Hong Kong dollars in such stores. You can choose to receive payment in cash or by bank transfer, but this transfer cannot be transferred to a mainland bank account (it is best to hold a Hong Kong bank card);

The second way is to withdraw funds from a licensed exchange. For example, exchanges such as OSL and HashKey can buy and sell virtual currencies, but withdrawals from the Hong Kong exchange require users to open an account at the exchange. Mainland residents (who also do not have a Hong Kong work permit or actual residence) cannot apply to open an account at the Hong Kong exchange.

The third way is to withdraw funds from securities companies, such as Shengli Securities and Guotai Junan International, which has just applied for a virtual currency trading license, etc. However, even if you are a "pure mainland resident", you cannot open an account in these institutions.

Therefore, if you are a mainland resident who does not have a Hong Kong work permit or proof of residence, you cannot enjoy the second or third withdrawal mode mentioned above. So if you are a pure mainland resident whose identity, work, and life are all in the mainland, it seems that you can only withdraw money through OTC stores in Hong Kong.

3. Are there any legal risks in using Cross-Border Payment to withdraw funds?

Even if the problem of compliance withdrawal of funds by mainland residents in Hong Kong is solved, many mainland residents still have a hard need to transfer the cashed funds back to the mainland. Is the cross-border payment system we are talking about today feasible?

On the surface, it is not possible, because the northbound transfer of cross-border payment (i.e. transfer from Hong Kong to the mainland) must be made by Hong Kong residents to mainland residents. If you are a mainland resident, even if you have a Hong Kong bank card, it is difficult to use the "FPS" system to transfer money to a mainland bank card. Lawyer Liu also tried it himself, and my Hong Kong bank card cannot be used for quick transfer to a mainland bank card (it can only be transferred through the traditional cross-border remittance system through the SWIFT system, which is expected to arrive in about 3 working days).

Of course, some "smart" friends may think that I can just transfer the funds I cash out in Hong Kong to a local Hong Kong person, and then ask him to transfer the funds to my bank card in the mainland. In fact, this also has legal risks: According to the introduction of the cross-border payment service by the relevant person in charge of the central bank, the applicable scenarios of this service mainly include "study abroad payment, public utility payment, medical treatment, salary and subsidy payment, etc.", and at the same time, it is necessary to:

Mainland participating institutions handling cross-border payment services should comply with the relevant business management regulations for cross-border funds settlement, fulfill anti-money laundering, anti-terrorist financing and non-proliferation financing compliance requirements in accordance with the law, establish and improve the risk monitoring mechanism for cross-border payment remittance services, improve risk prevention capabilities, strengthen monitoring of suspicious transactions, and ensure the smooth and orderly development of business. (For details, please see the National Immigration Administration's "Cross-border Payment Service is officially launched to support real-time transfers in three scenarios")

When I use the cross-border payment channel to remit money to Hong Kong, China Merchants Bank also allows me to choose the purpose of the remittance (see the figure below for details). If the real background of a transaction is a virtual currency transaction, I believe that even if it is legal and compliant in Hong Kong, most banks in the mainland will not allow citizens to convert virtual currency into cash overseas.

Although objectively speaking, the cross-border payment service does not review business background information at present, but from the perspective of complete compliance, Lawyer Liu does not strongly recommend that everyone withdraw virtual currency or bring in funds through this business.

4. Final Thoughts

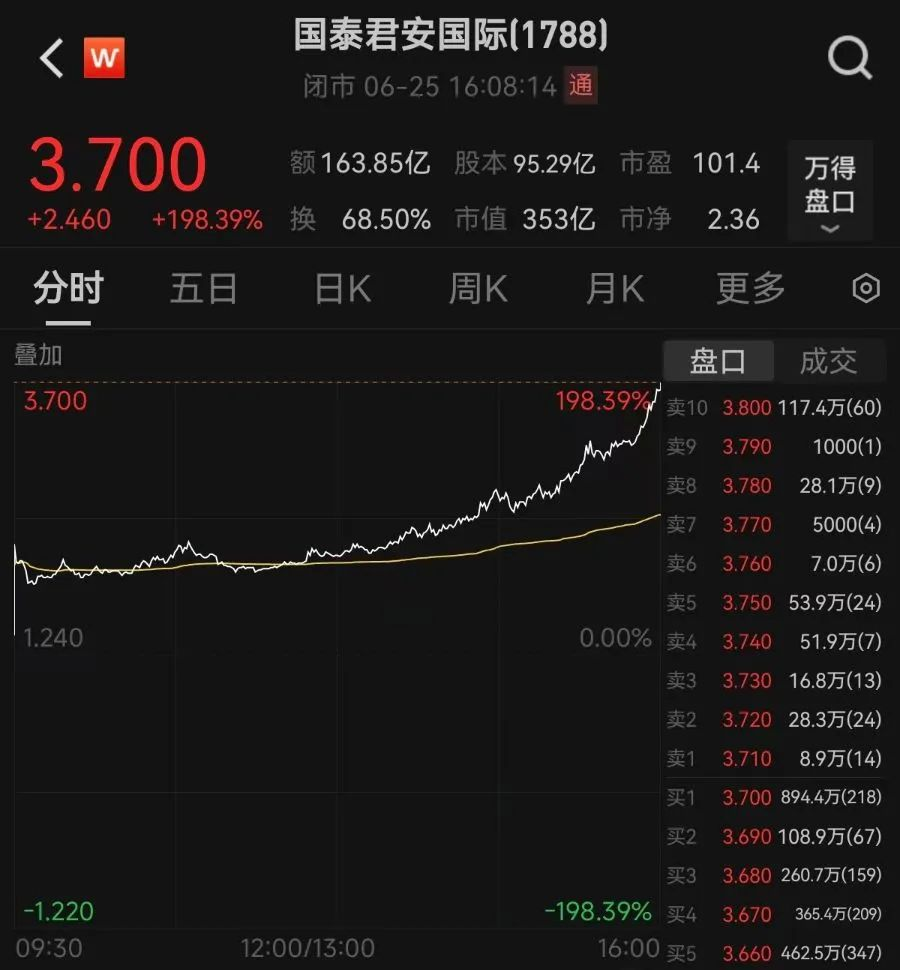

Today, Guotai Junan International obtained the approval of the Hong Kong Securities and Futures Commission in Hong Kong, and its securities trading license has added virtual asset (Bitcoin, Ethereum, Tether, etc.) trading services. As soon as the news came out, Guotai Junan International's stock soared all the way, and today it soared by nearly 200%. By the way, the token HSK of the Hong Kong HashKey Exchange, which has been sluggish for many days, also increased by 80%, because there was news that the virtual currency trading platform that Guotai Junan International cooperated with was the HashKey Exchange.

(Picture from the Internet, please delete if infringed)

We used to say that the cryptocurrency world likes to shamelessly "rub against" the traditional financial market, but it is often looked down upon by the old money in traditional finance: virtual currency is almost equated with fraud, Ponzi schemes, etc. Now, things have changed, and traditional finance has begun to "rub against" the cryptocurrency world.