Author: Michael Saylor

Compiled by: Deep Tide TechFlow

Introduction : Saylor, founder of MicroStrategy, has proposed a "digital asset stack" theory, positioning Bitcoin as the bottom layer of digital capital, topped by a five-layer structure of digital credit, digital currency, digital income, and digital equity. The core argument is that Bitcoin itself does not require staking, inflation, or protocol modifications; all income is generated by the upper-layer capital structure. This is the theoretical framework he has developed for his STRC and MSTR strategies, and a direct response to debates such as "Stablecoins should pay interest" and "Should Bitcoin follow Ethereum's example?"

Modern Digital Asset Stack

Bitcoin is digital capital.

This is the foundation of the entire modern digital economy.

Bitcoin is scarce, globally circulating, highly liquid, programmable, divisible, and auditable; anyone with an internet connection can obtain it. It is not issued by a government, is not controlled by a company, has no tenants, no maintenance costs, no borders, no physical address, no board of directors, and no central bank can dilute it.

It is the foundational layer of digital value.

But capital itself is only the starting point.

The next stage of Bitcoin is not simply about holding BTC, but about building a complete digital capital stack on top of BTC: digital capital, digital credit, digital currency, digital income, and digital equity.

This is how Bitcoin evolved from a single asset into a global financial architecture.

Bitcoin is still Bitcoin. The world builds upon it.

This stack has five layers.

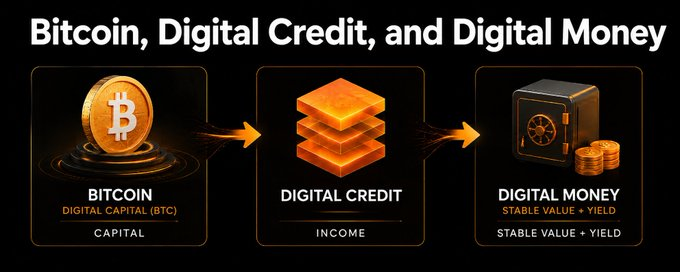

The modern digital asset stack consists of five layers.

The first layer is digital capital, which is BTC, a pure, scarce, and high-energy capital asset.

The second layer is digital credit, similar to tools like STRC, which are yield-generating instruments backed by Bitcoin and designed to mitigate volatility and provide returns.

The third layer is digital currency, a stable-value, interest-bearing instrument. It is pegged to the US dollar and can take the form of tokens, funds, preferred securities, accounts, or other encapsulated forms. The underlying layer is a combination of digital credit and fiat currency cash equivalents.

The fourth tier consists of digital returns, leveraged or structured return products. These are offered to investors willing to take on more risk, leverage, volatility, or illiquidity.

The fifth tier is digital equity, similar to the residual equity in MSTR. It is a secondary tier that absorbs volatility, supports the entire credit structure, and takes the remaining upside returns.

This is not a protocol change, not staking, not currency inflation, and not yet another new token masquerading as Bitcoin. This is a capital market built on Bitcoin.

First-tier digital capital: BTC

At the bottom of the stack is BTC.

Bitcoin (BTC) is equivalent to digital versions of gold, landmark real estate, and sovereign reserve assets, but with greater liquidity, divisibility, scarcity, and global settlement capabilities. It is the most powerful asset in this system.

High energy leads to volatility. Bitcoin's dramatic volatility stems from its status as pure digital capital: scarce, liquid, global, and traded 24/7. This volatility is not a flaw, but rather the raw material for building digital capital markets.

However, not every investor can directly hold BTC. Family offices want capital appreciation, corporations want treasury reserves, banks want collateral, insurance companies want returns, retirees want interest, payment companies want stable settlements, crypto exchanges want a dollar-like asset that can truly pay interest to users, and depositors in emerging markets want dollars, liquidity, and returns.

An asset with a volatility of 40% is perfect for some investors, but completely unsuitable for others.

The answer is not to modify Bitcoin, but to build products on top of Bitcoin that match the needs of each type of funding.

Second-tier digital lending: Bitcoin-backed revenue

Digital lending transforms highly volatile digital capital into low-volatility returns.

STRC is an example: a sophisticated, high-yield, short-duration yield instrument issued by a company backed by Bitcoin. BTC provides the long-term capital base, digital equity absorbs the remaining volatility, and digital credit sits on top of equity, paying dividends to investors who want returns but don't want to directly experience BTC volatility.

The key point is not that digital lending always has a fixed, fluctuating figure. It doesn't.

Credit instruments exhibit low volatility in normal markets but increase volatility in stressed markets. Interest rate spreads widen, liquidity changes, interest rates fluctuate, issuers' market image changes, and market structures evolve.

A more accurate statement would be: digital credit is designed to curb the volatility of digital capital.

It achieves this through its capital structure, priority pricing, returns, par value mechanism, liquidity support, and a first-tier equity buffer. The goal is to transform the highly volatile raw capital energy of BTC into a more stable yield stream suitable for credit investors.

Financial professionals have long understood this logic. A mortgage loan is not the same as a house, municipal bonds are not the same as a city, corporate bonds are not the same as common stock, and preferred securities are not the same as the equity underlying them. Assets can be very volatile, but the credit layer can be less volatile.

The purpose of digital lending is not to eliminate risk, but to intelligently allocate it. Equity holders accept residual volatility and upside, credit holders receive returns and higher-level claims, and cryptocurrency holders gain an additional layer of stability and liquidity. Each investor selects a risk level that matches their own authorization.

Bitcoin itself does not need to generate returns. It requires no staking, no inflation, no protocol changes, and it doesn't need to become Ethereum. Returns are generated by the capital structure on top of Bitcoin, not by devaluing Bitcoin.

This distinction is crucial.

Third-tier digital currencies: Stable-value currencies built on digital credit.

Digital currency is the next layer.

It is a stable-value, daily redeemable instrument that functions like money while paying a substantial return. Depending on the jurisdiction, distribution channel, and investor type, it can be packaged as a token, fund, preferred security, account, or other regulated form.

The concept is simple: combine digital credit with fiat cash equivalents. Digital credit acts as the yield engine, while fiat cash equivalents provide liquidity and stability. The structure itself manages duration, redemption, credit exposure, reserves, and market risk, giving the holder a stable, interest-bearing asset.

For example, a product might hold Bitcoin-backed digital credit with a yield of around 10%-12%, coupled with Treasury bills, money market funds, repurchase agreements, or bank reserves. After deducting liquidity reserves, fees, and risk buffers, the target return of this cryptocurrency instrument could fall within the 6%-8% range.

This is the breakthrough point. Digital capital becomes digital credit, and digital credit combined with fiat currency liquidity becomes digital currency.

This is how a stable value instrument backed by Bitcoin can pay interest. This isn't magic; it's structured finance.

BTC is a capital asset, digital equity is the initial loss and upside layer, digital lending is the yield layer, and digital currency is the liquidity layer for stable value. The entire stack transforms Bitcoin's raw volatility into useful financial products without touching Bitcoin itself.

Stable value does not equal risk-free.

This distinction is important.

Cryptocurrencies should not be touted as risk-free, nor should they be sold as unconditionally guaranteed. They should be described as designed to maintain stable value through reserves, liquidity, credit structure, transparency, and risk management.

A well-designed cryptocurrency product should be tested using the same set of questions that financial professionals use to evaluate any money market, stablecoin, or short-duration credit product: What are the underlying assets? What is the credit exposure? What are the liquidity reserves? What is the duration? What is the redemption mechanism? What is the priority? What are the collaterals? How transparent is it? Who bears the first loss? How does it perform under stress scenarios?

This kind of scrutiny is healthy.

Digital currencies do not eliminate risk, but rather package, disclose, manage, and price risk in a form that is useful to depositors, businesses, payment networks, exchanges, and institutions.

Why are cryptocurrencies pegged to fiat currencies?

Many Bitcoin believers ask: Why should digital currencies be pegged to the US dollar or other fiat currencies?

Because the world's debts are still denominated in fiat currency.

Wages are calculated in US dollars, euros, Japanese yen, pesos, and local currencies; invoices are calculated in fiat currency; taxes are calculated in fiat currency; mortgage payments are calculated in fiat currency; credit card payments are calculated in fiat currency; and corporate accounting is done in fiat currency. The banking system, insurance contracts, payroll systems, and financial statements are all denominated in fiat currency.

Most people don't want their current account balance to fluctuate by 5% in a single day. They want a stable unit of account.

This is why stablecoins have found a product-market fit. The world wants a digital dollar because the dollar remains the dominant unit of account in global commerce.

However, the current stablecoin model is incomplete. Stablecoins provide digital liquidity, but holders typically do not receive the full economic benefits of reserve returns. Bank deposits are convenient, but often offer little return. Money market funds offer returns, but lack native 24/7 digital transferability. Staking assets offer returns, but require users to accept cryptocurrency price volatility and protocol risks.

Cryptocurrencies can combine the best attributes: stable value, digital transferability, daily liquidity, transparent reserves, substantial returns, and a Bitcoin-backed capital structure.

Fiat currency addresses the issue of the unit of account, while Bitcoin addresses the issue of capital preservation. The US dollar is the measuring stick, while Bitcoin is the energy source.

Ideal currency experience

A good currency should fulfill three functions: medium of exchange, store of value, and unit of account.

Bitcoin (BTC) is the strongest long-term store of value, but it's not yet a unit of account for most of the world. Cryptocurrencies solve this bridging problem.

A digital currency instrument pegged to the US dollar and backed by Bitcoin, which generates interest, can serve as a medium of exchange because it is stable and transferable; it can serve as a store of value for people who use fiat currency because it pays interest rather than sitting idle; and it can function as a unit of account because it is denominated in the same currency that people already use to price wages, bills, taxes, and debts.

This is not a denial of Bitcoin, but rather a bridge from the world of fiat currency to the world of Bitcoin.

This is Bitcoin's killer use case.

Bitcoin's killer use case is not just payments.

The real killer use case is rebuilding the global monetary, credit, and capital markets on top of digital capital.

Bitcoin is a superior asset, but the world isn't just about one type of investor. Some want raw BTC, some want yield, some want stable value, some want collateral, some want leverage, some want payments, some want growing equity, some want treasury reserves, and some want an instant-transferable, interest-bearing dollar balance.

The digital asset stack allows Bitcoin to serve all of these people. BTC serves capital allocators, digital credit serves yield investors, digital currency serves depositors and payment users, digital yield serves return-seeking investors, and digital equity serves growth investors. The same Bitcoin foundation supports every layer.

This is how Bitcoin expanded from a trillion-dollar asset into a global financial system.

Bitcoin doesn't have to replace all fiat currencies tomorrow. It can back the tools the world already uses today: the US dollar, credit, accounts, funds, securities, payment assets, and treasury products. That's the bridge.

Why did this financial professional establish it?

This framework should look familiar to those working in the financial industry.

Innovation lies not in the disappearance of risk, but in Bitcoin becoming the underlying collateral and capital asset of a modern tiered financial system.

Traditional finance has long been stratifying risk: common stock, preferred stock, senior debt, secured credit, money market instruments, leveraged funds, structured products, bank deposits, and payment balances. The digital asset stack applies the same logic to Bitcoin.

The key variables are all conventional: priority, collateral ratio, liquidity, duration, yield, credit spread, redemption, market depth, disclosure, regulatory treatment, accounting treatment, tax treatment, and counterparty exposure.

Bitcoin introduces a superior underlying asset, and the capital market transforms this asset into products with different licenses.

This is not anti-finance, it's better finance.

Why this applies to Bitcoin investors

For Bitcoin investors, the most important principle is simple: Bitcoin is still Bitcoin.

No need to change the protocol, no need for base layer returns, no need for staking, no need for inflation, no need to change the supply cap of 21 million, and no one is forced to give up self-custody.

Those who want pure BTC can get pure BTC, those who want to run nodes can run nodes, and those who want to self-host can self-host.

The digital asset stack does not undermine Bitcoin's core principles; it merely extends its reach. This is a disciplined expansion. The foundational layer should remain sacred, and most innovation should occur on top of it: custody, applications, securities, credit instruments, payment systems, wallets, exchanges, funds, and capital markets.

Bitcoin serves billions of people without forcing everyone into a narrow adoption model. It can be a self-custodied currency for individuals, digital capital for companies, collateral for banks, national reserves, family property, market infrastructure, and hope for anyone facing economic hardship.

The world is building skyscrapers on Bitcoin because Bitcoin is worth building.

Why did this MSTR investor form?

For MSTR investors, the digital asset stack explains the role of digital equity.

Digital equity is the secondary tranche. It absorbs volatility, supports the credit structure, benefits from the appreciation of Bitcoin, and takes the remaining upside after the senior debt is satisfied, providing the capital structure that allows digital credit and digital currencies to exist.

MSTR equity is not equivalent to BTC, STRC, or any other cryptocurrency. Each role is distinct.

BTC is digital capital, STRC securities are digital credit, digital currency is stable value return, digital returns are amplified returns, and MSTR common stock is digital equity.

Equity is more volatile because it involves residual claims; credit is less volatile because it is more sophisticated; and money is designed to be more stable because it combines credit and liquidity reserves. This is the logic behind the capital stack.

Digital equity makes the above layers possible because someone always has to bear the remaining risk and earn the remaining returns.

Why did this pair of crypto innovators form?

Digital currency presents a huge opportunity for crypto innovators.

Stablecoins proved the world wanted digital fiat currency. DeFi proved users wanted yield. Exchanges proved global markets wanted 24/7 liquidity. Wallets proved value could move at internet speed. Bitcoin proved digital scarcity could be secure, decentralized, and global.

The next step is to combine these breakthroughs into better products.

A Bitcoin-backed, interest-bearing, and stable-value dollar instrument can become a native asset for wallets, exchanges, payment networks, fintech applications, DeFi protocols, treasury platforms, and global businesses.

It can compete with stablecoins that pay almost no interest to users, bank deposits that pocket the interest rate spread, money market funds that offer returns but lack native digital transferability, and staking assets that require users to accept token volatility in order to earn returns.

This is constructive competition. Crypto doesn't need more things that are just for speculation. It needs useful, durable, transparent, interest-bearing financial products that solve real problems for real users. Digital currency is one of those.

Digital benefits: Not money, but useful.

Above digital currency is digital revenue.

Digital earnings are not money; they are investment products.

It can be built using leveraged digital credit, leveraged digital currency, structured funds, private equity vehicles or other tools, targeting investors who seek higher returns and are willing to accept higher risks, leverage, volatility or poor liquidity.

A leveraged cryptocurrency strategy may target returns far higher than unleveraged products. But it's not a current account, not a stablecoin, and not a savings product for everyone. It's digital returns.

This distinction is crucial. Cryptocurrencies are used for stability, liquidity, payments, savings, and working capital. Digital yield is for sophisticated investors seeking to amplify returns. Digital equity is for investors seeking residual upside. The power of this stack lies in the clear role each product plays.

Three-layer breakthrough

The key innovation lies in these three layers of transformation.

Digital Capital: High Volatility, High Energy BTC.

Digital credit: Bitcoin-backed revenue, designed to mitigate a significant portion of BTC volatility through priority, structure, yield, and equity backing.

Digital currency: A tool that combines digital credit, fiat currency cash equivalents, and liquidity reserves to create stable value and generate interest.

This is the breakthrough. Bitcoin has given us the world's strongest digital capital asset, which the capital market converts into credit, and the credit plus liquidity reserves convert this return into currency.

The world doesn't need everyone to be smart enough to price coffee with SATs tomorrow. The world needs a better currency today: one that moves at internet speed, remains stable in users' accounting units, pays substantial returns, and is ultimately driven by the strongest digital capital asset ever.

That is digital currency.

Why this is good for BTC

Digital currencies have increased the utility of BTC.

Every dollar of digital currency backed by Bitcoin creates incremental demand for the Bitcoin-backed capital structure, creating new reasons to hold BTC, finance BTC, custody BTC, audit BTC, insure BTC, and build services around BTC.

It also exposes Bitcoin to investors who can't tolerate the volatility of raw Bitcoin. Retirees may not want the volatility of raw BTC, businesses may not want it, banks may not want it, payment companies may not want it. But they may want a stable-value dollar asset with a yield of 6%-8% backed by Bitcoin-backed digital credit.

This brings new capital into the Bitcoin ecosystem. More capital means more adoption, more adoption means more liquidity, more liquidity means greater resilience, and greater resilience means a stronger Bitcoin.

Why this is good for the crypto industry

The crypto industry needs a better monetary foundation.

Many crypto users want US dollars, many crypto investors want returns, many crypto builders want programmable assets, many crypto platforms want liquid collateral, and many crypto applications need stable units of account.

Digital currencies built on Bitcoin-backed credit provide the industry with a better foundational product: a stable-value, interest-bearing digital dollar driven by Bitcoin.

It can thrive on exchanges, in wallets, in funds, in accounts, in payment networks, and ultimately wherever digital value flows. Instead of forcing users to choose between zero-yield stablecoins and volatile staking tokens, it gives them another option: a yield-bearing digital currency built on Bitcoin-backed capital. This is good for crypto.

Why this is good for investors

Investors should not be forced into a single risk level.

The digital asset stack offers every investor a choice. If you want digital capital, take BTC; if you want digital credit, take STRC-style instruments; if you want digital currency, take stable-value interest-bearing instruments; if you want digital returns, take leveraged or structured products; if you want digital equity, take MSTR-style common stock.

This is a complete menu. Depositors can take digital currency, yield investors can take digital credit, growth investors can take digital equity, long-term believers can take BTC, and sophisticated investors can take digital yield. The same Bitcoin foundation supports everyone. This is how Bitcoin makes every form of empowerment accessible.

Why this is a good thing for the world

The world needs a better currency.

Billions of people want the dollar because it's liquid, familiar, and widely accepted. But they also want returns, transparency, liquidity, and protection from devaluation.

Today, many people are forced to choose between unstable local currencies, low-yield bank deposits, zero-yield stablecoins, volatile crypto assets, or financial products that are difficult for them to access.

Cryptocurrencies can improve this. They offer stable value, digital liquidity, daily redemption, and substantial returns. They can help depositors, businesses, payment companies, emerging markets, exchanges, institutions, and anyone who wants a better currency but doesn't want to experience the volatility of raw Bitcoin.

The simulated world builds its economy on gold, real estate, banks, deposits, credit, equity, funds, and payment networks. The digital world will be built on Bitcoin, digital credit, digital currency, digital income, and digital equity.

Bitcoin is digital capital. Digital lending turns it into returns. Digital currency turns it into everyday utility. Digital returns amplify it. Digital equity finances it.

The foundation layer remains sacred, and the capital stack remains open.

This is the modern digital asset stack. This is how Bitcoin became the foundation of a better financial system.