What is DeFi?

Decentralized Finance (DeFi), also known as "decentralized finance" in Chinese, is based on the use of blockchain-based smart contracts to build and operate financial products and protocols within a decentralized network. While its functions are similar to traditional finance, DeFi operates on a blockchain, differing fundamentally in the following aspects:

- Transaction transparency: All smart contract logic and fund flows are publicly traceable, verifiable, and publicly available on the blockchain.

- Automated profit distribution: Profits are automatically distributed according to pre-set smart contract rules, without relying on third-party institutions.

- Reduced operating costs: By eliminating the intermediaries in traditional finance, the cost of participation is significantly reduced.

- Lower barriers to entry: Any digital wallet holder can freely participate.

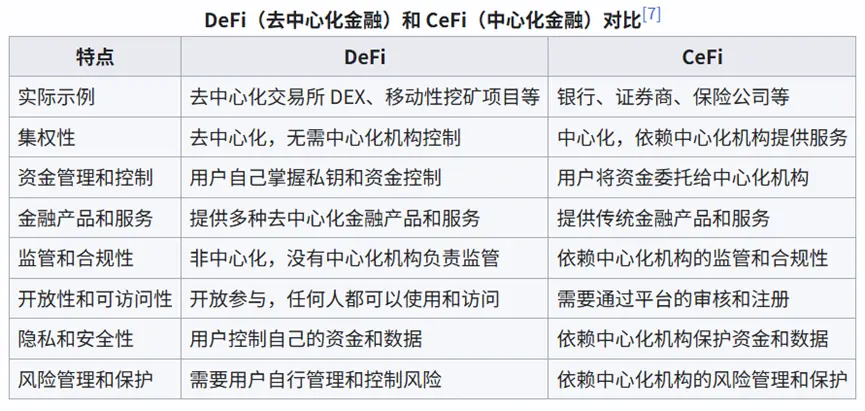

The core of DeFi lies in its decentralized architecture, relying on blockchain technology and automated smart contracts, without the need for traditional financial institutions as intermediaries. Wikipedia defines the difference between DeFi and CeFi as follows:

The DeFi ecosystem is vast and diverse. As of June 23, 2025, there are 69 types of DeFi projects listed on DeFiLlama. Based on total locked-in value (TVL) and the number of protocols, the core sectors of the DeFi ecosystem include stablecoins, lend protocols, bridge protocols, liquid staking, decentralized exchanges (DEXs), real-world asset (RWAs), yield farming, indexes, derivatives, and yield aggregators.

Common application scenarios include the following:

1. Staking Tokens to Participate in Proof-of-Stake Consensus

In blockchains using Proof-of-Stake consensus, a node must stake a certain number of tokens to obtain node operation rights. Nodes also receive rewards for validating new blocks. Participating in network node operation means investors delegate their tokens to high-quality validators—reliable and honest validators—in exchange for a share of the node rewards.

- For DeFi investors, depositing tokens in nodes provides collateral, helping the network operate more efficiently and securely.

- Network users pay network usage fees, and node validators, after receiving these fees, return a portion of the profits to DeFi investors.

2. Providing Loans

Providing loans means investors deposit their idle tokens into a pool of funds, from which borrowers can borrow corresponding tokens by providing certain collateral.

- DeFi investors deposit funds into the pool, providing borrowers with more investment opportunities. When funds are loaned to high-quality borrowers, they indirectly provide value to high-quality projects. Borrowers earn returns by lending tokens, while also providing a portion of these returns (interest) to DeFi investors.

3. Providing Liquidity: LPs

Providing liquidity: LPs deposit tokens into decentralized exchanges. Through the AMM mechanism, traders can leverage these liquidity pools to exchange tokens.

- DeFi investors provide liquidity by depositing tokens into decentralized exchanges, enabling traders to trade tokens at prices with minimal market impact.

- The AMM mechanism distributes transaction fees, AMM native tokens, and other incentive programs to DeFi investors.

4. Using Yield Aggregators: Utilizing Yield Aggregators: Aggregators aggregate yield farming opportunities across the market on a single front-end, allowing users to access multiple yield opportunities from a single interface. Tokens are managed through aggregators in a delegated manner. DeFi investors receive additional rewards for providing liquidity more efficiently.

- By using aggregator protocols, DeFi investors can redistribute liquidity to specific markets faster and more cheaply than single-staking traders. Furthermore, by investing resources in high-value protocols, they receive better returns, save on transaction costs, and reduce workload through automated portfolio management.

5. Lock Tokens and Participate in Governance

Investors purchase and lock tokens in exchange for token allocations. Generally, the longer the lockup period, the greater the rewards. The higher the TVL (total value locked) of a protocol, the more attention and trust it garners, and the more likely it is to become a leader in the space. Projects also offer rewards based on the amount and duration of locked tokens, which may include participation in community governance.

- DeFi investors provide additional TVL value to projects by locking up tokens for a certain period of time.

- Projects provide investors with returns based on the lockup period and value, which may include token rewards, governance rights, airdrops, and fee sharing.

What is a stablecoin?

A stablecoin is a special type of cryptocurrency designed to maintain stable value. It is typically pegged to a fiat currency like the US dollar or an asset like gold. Compared to traditional cryptocurrencies (such as BTC and ETH), stablecoins have extremely low volatility, making them more suitable for everyday payments, value transfers, and as a unit of account for transactions.

According to Coingecko data, as of June 23, 2025, the total market capitalization of stablecoins across various blockchains has exceeded $250 billion. Stablecoins are broadly categorized into four types: fiat-backed stablecoins, commodity-backed stablecoins, over-collateralized stablecoins, and algorithmic stablecoins. The characteristics of various stablecoin types are as follows:

Fiat-backed stablecoins

- Each stablecoin is backed 1:1 by fiat currency.

- Representatives: USDT, USDC

USDT is currently the largest stablecoin by market capitalization. However, not every USDT is backed by US dollars; rather, it is backed by a mix of US dollars and commercial paper reserves. Tether has also been criticized by investors and regulators for its lack of transparency regarding the nature of its backing.

USDC is currently the second-largest stablecoin by market capitalization. Each USDC is backed by $1 (cash or equivalent) held by the center. USDC is the most popular stablecoin on Ethereum.

Commodity-backed stablecoins

- Backed by physical assets (such as precious metals, oil, and real estate). Gold is the most commonly used collateral. Reserves of physical assets are typically maintained by centralized entities.

- Representative: XAUT

Over-collateralized stablecoins

- Over-collateralized stablecoins are backed by other cryptocurrencies. The value of the cryptocurrencies held in reserves exceeds the value of the issued stablecoins. If the value of the collateral falls below a threshold, the user's collateral will be sold on the open market.

- Representatives: DAI, MIM, MAI, YUSD

DAI is the first over-collateralized stablecoin.

Algorithmic stablecoins

- Do not rely on fiat currency or collateral, but instead implement algorithms that influence stablecoin demand/supply to achieve price stability.

- Representatives: UST, FRAX (algorithmic + collateral), BAC, AMPL

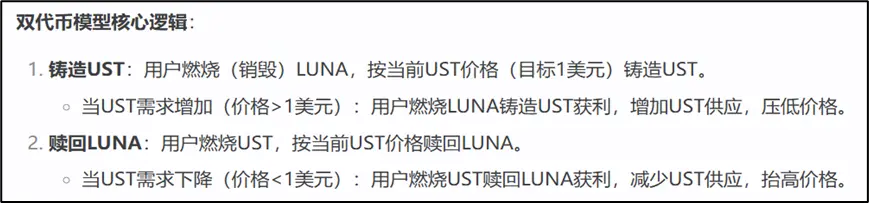

The dual-token model of UST and LUNA is particularly noteworthy. UST uses a smart contract-based algorithm to maintain the UST price peg at $1 by burning or permanently destructing LUNA tokens to create new UST tokens. LUNA serves as a governance token and regulatory tool, absorbing UST price fluctuations. The Anchor Protocol, a lending platform within the Terra ecosystem, offers up to 20% annualized returns on UST deposits, attracting significant capital to UST.

However, this dual-token mechanism design carries significant systemic risks, which were fully exposed in 2022, leading to the famous UST depegging and LUNA crash. The core reason is that when UST depegged due to market panic (e.g., falling below $1), users burned large quantities of UST to redeem LUNA for arbitrage, leading to a surge in LUNA supply. The excess LUNA caused a price crash, further undermining market confidence in UST's stability and exacerbating its depegging, creating a vicious cycle. Furthermore, the ecosystem's overreliance on the Anchor protocol created hidden dangers. Once yield reductions triggered capital flight, UST demand collapsed, ultimately triggering a systemic collapse.

How do decentralized exchanges work? —AMMMechanism Analysis

Unlike the order book model of traditional financial markets, decentralized exchanges utilize automated market makers (AMMs). They do not require a counterparty and allow for direct transactions.

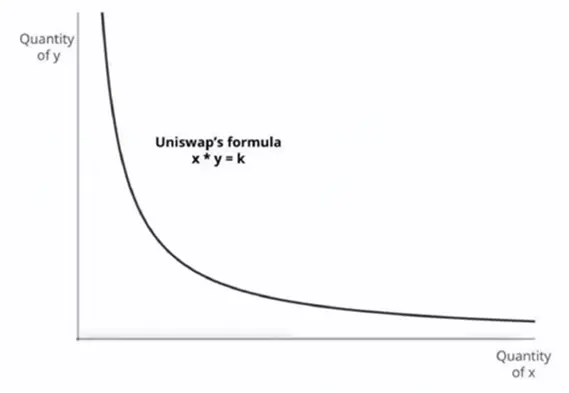

Constant Product AMM

Uniswap uses a constant product AMM model.

Let X be the initial quantity of Token A, and Y be the initial quantity of Token B. X*Y = K, where K is defined as a constant. When a user wants to purchase n Tokens A, the quantity of Token A in the pool becomes (X - n). Based on the constant product formula of the AMM mechanism, we can deduce that the quantity of Token B in the pool becomes K / (X - n).

This can be explained in detail with the following example.

The initial state of a liquidity pool is:

- Amount of ETH: 100 ETH

- Amount of USDT: 400,000 USDT

- Constant product K = 100 × 400,000 = 40,000,000

Suppose a user wants to purchase 5 ETH with USDT.

Pool status before purchase:

- ETH balance: 100

- USDT balance: 400,000

- K = 100 × 400,000 = 40,000,000

Pool status after purchase:

- ETH balance: 100 - 5 = 95

- USDT balance: 40,000,000 / 95 = 421,052.63

- K remains unchanged at 40,000,000

USDT cost to the user:

- USDT increase in the pool = 421,052.63 - 400,000 = 21,052.63 USDT

A user pays 21,052.63 USDT to buy 5 ETH

Average actual transaction price = 21,052.63 / 5 = 4,210.53 USDT/ETH

In practice, Uniswap also requires buyers to pay a 0.3% transaction fee, which goes to limited partners (LPs). The more active the trading pair, the greater the LP share and the greater the fee share. Transaction fees incentivize liquidity provision.

In the example above, we see that the average actual transaction price is 4,210.53 USDT/ETH, while the trader's expected price at the time of the trade was 4,000 USDT/ETH. The difference between these two prices is called "slippage." Generally, the larger the transaction volume, the more significant the price deviation, and the higher the slippage.

Another risk of constant-product AMMs is uncompensated loss. Uncompensated loss occurs when a liquidity provider deposits assets into the AMM pool, but token price fluctuations cause the total value of their assets to fall below the difference between simply holding the tokens.

Let's use a simple example to illustrate.

Initial State:

- Assume ETH price = 4,000 USDT

- User deposits: 1 ETH + 4,000 USDT (total value = 8,000 USDT)

- Total pool liquidity: 100 ETH + 400,000 USDT. This user holds 1% of the liquidity pool

- K = X * Y = 100 × 400,000 = 40,000,000

If the ETH price rises to 8,000 USDT

- Arbitrageurs will buy ETH at a lower price in the pool, and the ETH and USDT amounts in the pool will reach a new equilibrium.

- X' × Y' = K = 40,000,000

- ETH price = 8,000 USDT = Y' / X'

- Solving this, X' = 70.71 ETH, Y' = 565,685 USDT

At this point, the user's LP assets are: 0.7071 ETH + 5,656.85 USDT, for a total value of (0.7071 × 8,000) + 5,656.85 = 5,656.8 + 5,656.85 = 11,313.65 USDT

If the user holds the original assets directly without providing liquidity, the current asset value is 1 ETH + 4,000 USDT = 12,000 USDT. The uncompensated loss is 12,000 USDT - 11,313.65 USDT = 686.35 USDT.

This example clearly demonstrates the risk of uncompensated loss that liquidity providers may face when the price of the asset in the pool fluctuates drastically.

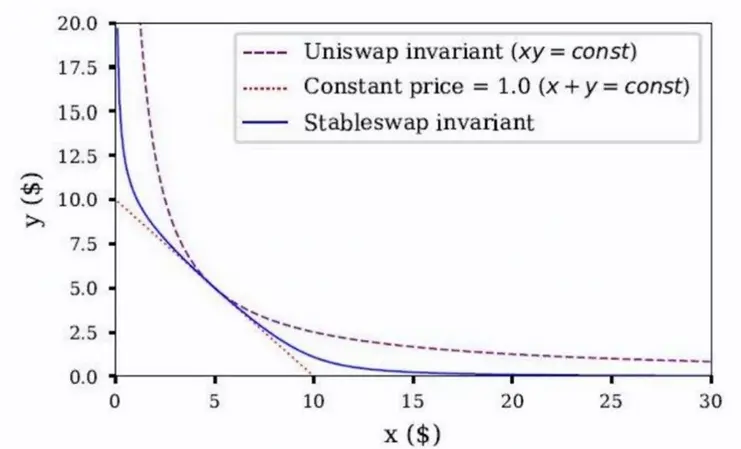

Hybrid AMM

To address the slippage and high impermanent loss issues faced by constant-product AMMs, Curve Finance innovatively employs a hybrid AMM combining constant-sum and constant-product functions. This creates a relatively flat curve near the equilibrium point, similar to a constant-sum function, to maintain relative price stability, while making the ends more sloped, similar to a constant-product function, ensuring liquidity at every point on the curve.

In addition to reducing slippage, Curve's transaction fees, slippage, and impermanent loss risk are far lower than those of current mainstream Dex exchanges. The fees distributed to LPs are also significantly lower than those of other Dex exchanges. Therefore, Curve relies on an incentive mechanism that relies on providing staking amount and time to attract LPs to inject liquidity.

Curve's token economics model is also very interesting.

- Providing liquidity on Curve not only earns transaction fees, but also rewards CRV tokens.

- Staking CRV can earn voting tokens, veCRV, based on a time-weighted basis. The longer the lockup period, the greater the voting weight.

- Holding veCRV also allows you to receive airdrops from many similar projects.

$veCRV token holders will enjoy the following five specific benefits:

- Governance voting rights regarding $CRV reward distribution: $veCRV holders can participate in regular votes to determine the weighting of rewards among Curve's liquidity pools, thereby influencing the amount of $CRV emission rewards each pool receives. This is also the most core benefit.

- Other governance voting rights: Participate in Curve DAO governance, submit proposals, and vote on them, including those related to adding new liquidity pools, setting and modifying protocol parameters, and more.

- Receive platform transaction fees: Based on the amount of $veCRV you hold, you can earn a 50% share of the protocol's transaction fees. Profits are distributed via 3CRV tokens (3CRV is the liquidity pool token (hereinafter referred to as "LP") of the stablecoin exchange pool 3POOL, redeemable at a 1:1 ratio for other stablecoins. 3POOL consists of three stablecoins: $DAI, $USDC, and $USDT).

- Increasing liquidity providers' market-making returns: When liquidity providers lock up $CRV, they can increase the $CRV rewards earned by LPs in the Curve pool (up to a maximum of 2.5x). The amount of $CRV required to increase returns depends on the Curve pool and the LP amount.

- The longer the $CRV is locked, the greater the amount of $CRV earned and the corresponding benefits.

Summary

DeFi, with its core characteristics of transparency, openness, and composability, has become a key engine driving innovation and growth in the cryptocurrency market. From basic lending and trading to complex yield strategies and governance models, DeFi continues to expand the boundaries of financial services.

In 2025, the tokenization of real-world assets (RWA) became one of the most anticipated areas in the DeFi space. RWA aims to bring traditional financial assets (such as government bonds, real estate, and credit) onto the blockchain, transparently managing and trading them through DeFi protocols. This not only introduces a massive influx of incremental assets and a user base (including traditional financial institutions) to the DeFi ecosystem, but also signals that DeFi is moving from purely "on-chain" financial experiments to a new stage of deeper integration with the traditional world and the creation of real value. A new financial landscape that connects the traditional and the on-chain, and integrates innovation and practicality, is rapidly emerging.