Growth signals and capital boom mask structural risks, and the market may enter a high-level oscillation phase

- The macroeconomic outlook is warmer: Moody's downgrade, tariffs and tax cut bills are re-emerging, reducing market risk and gold prices are rising sharply

- Capital momentum: Stablecoins and ETFs are flowing in, and new buying is strong, but the sustainability of the increase in market risk aversion remains to be seen.

- Price and momentum diverge: BTC rises, funds, OTC premiums, and ETFs rise simultaneously, and the risk of a pullback increases.

- Strategic recommendations: Defense first, pay attention to BTC 103,000 support, MSTR rhythm, ethbtc solbtc trend.

1. Macro and market environment

Moody's downgrade, tariffs and tax cut bills pushed up U.S. Treasury yields, triggering fluctuations in the U.S. stock and cryptocurrency markets.

U.S. stocks may pull back, technology stocks will come under pressure, and financial and defense sectors will be relatively resilient; cryptocurrencies may fall to support levels, and attention should be paid to the Federal Reserve's easing signals.

Fiscal stimulus and interest rate cuts are good for U.S. stocks and cryptocurrencies, but we need to be wary of the widening deficit and the risks to the status of the U.S. dollar.

If the Federal Reserve is loose and the US dollar hegemony is stable, the market will continue to rise; otherwise, it is necessary to increase allocation of non-US dollar assets.

Strategy: Increase holdings of mainstream cryptocurrencies and dynamically adjust global asset allocation.

2. Analysis of capital flows & market structure of mainstream currencies

External Funding Flows

- ETF funds: 2.80046 billion inflows this week, with a large inflow

- Stablecoins: 2.3 billion new coins were issued this week, with an average daily increase of 321 million coins, and the issuance level is relatively high.

Market sentiment indicators

- OTC premium: Stablecoin premium continues to rise

Bitcoin (BTC)

- Technical analysis: The market is in a volatile upward range

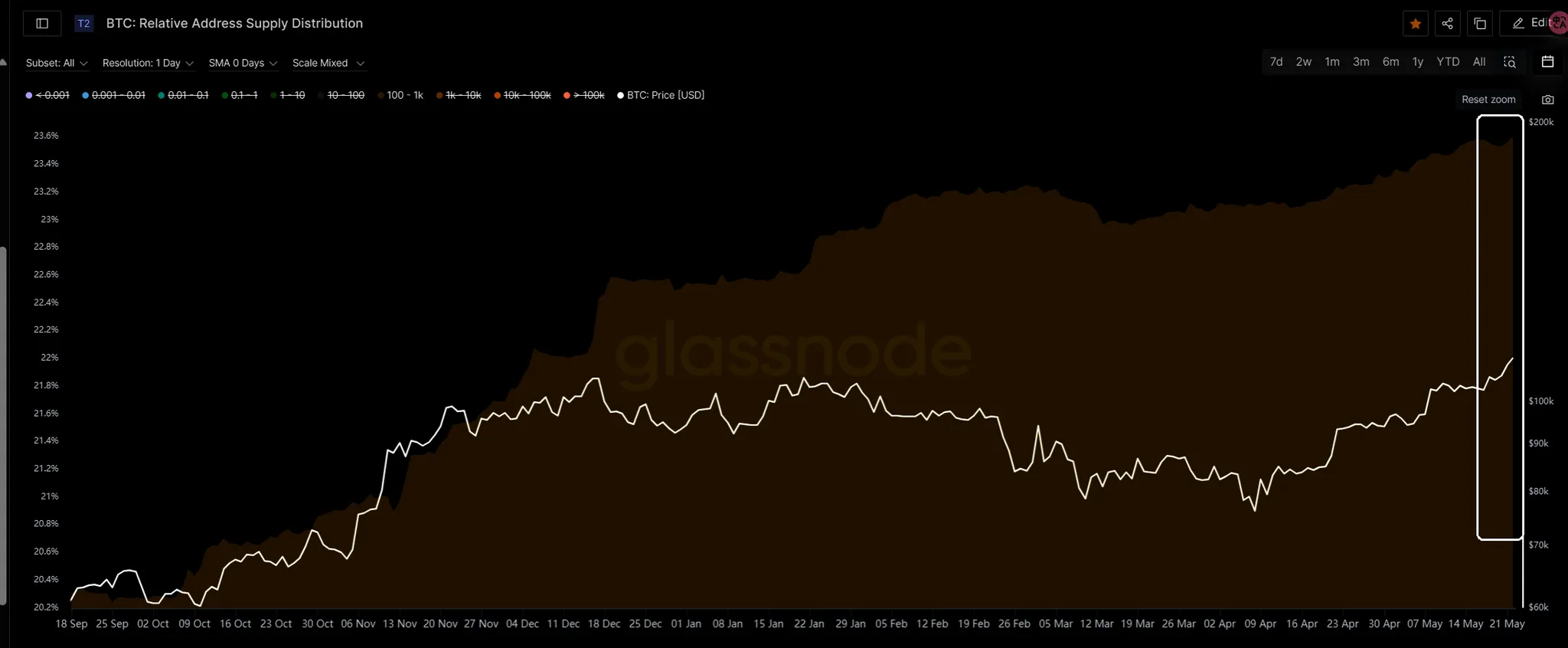

- On-chain chip distribution: 103,000 chips or more

Ethereum (ETH)

The trend is weaker than BTC, ETH/BTC remains volatile, and funds continue to flow back to BTC dominance.

On-chain changes: The increase in active addresses may indicate that the staged bottoming out has been completed.

Macroeconomic Review

What impact will Moody's downgrade have on the market?

background:

On May 16, 2025, Moody's downgraded the US credit rating from Aaa to Aa1, citing the surge in debt (US$36 trillion, 122% of GDP) and high interest expenses (3% of GDP). This is the first time that the US has lost its AAA rating from the three major rating agencies, following the downgrades by S&P in 2011 and Fitch in 2023. The downgrade, coupled with Trump's tariff and tax cut bill (the reconciliation bill, which is expected to increase the deficit by US$3.3 trillion), will exacerbate volatility in the US bond market in the short term.

Historical review:

- 2011: Risk aversion boosts demand for U.S. Treasuries, with the 10-year yield falling to 1.7%.

- 2023: Increased bond issuance leads to selling pressure, and the yield rises to 4.9%, and then fluctuates.

- 2025: Similar to 2023, rating downgrades and policy uncertainty push up yields (30-year bonds have broken 5%), and short-term selling pressure continues.

Supply side:

- Low maturity pressure: The peak of US Treasury maturity in May and June is mostly short-term Treasury bonds (accounting for 80%), with a 4% yield that attracts buying and low rollover risk.

- There is great pressure to issue bonds: the coordination bill will expand bond issuance, push up supply, and yields may rise further.

Demand side:

- Short term: The Fed's interest rate cuts (saving about $90 billion in interest for every 25 basis points) and the cessation of balance sheet reduction can boost demand and lower yields.

- Long term: The demand for US debt depends on the hegemony of the US dollar, and the international status of the US dollar needs to be maintained to ensure rigid buying.

Impact on US stocks and BTC

Short-term impact (until July 2025)

1. US stocks

- Increased market volatility: Moody's downgrade has heightened market concerns about the sustainability of US fiscal policy, coupled with uncertainty over tariff policies (10% tariffs on China, Canada, Mexico and the world) and tax cut bills, which may trigger a rise in risk aversion. The increase in US debt supply due to the increase in the debt ceiling has pushed up yields (30-year bonds have broken 5%) and increased corporate financing costs.

- Plate differentiation:

Pressured sectors: Technology stocks and high-valuation growth stocks are sensitive to interest rates, and rising yields will depress valuations (such as FAANG stocks, which have high price-to-earnings ratios). Consumer goods and retail industries may be under pressure as tariffs push up costs.

Beneficiary sectors: The financial sector (such as banks and insurance companies) benefits from the high interest rate environment, while the defense and energy sectors may perform strongly due to increased spending under the reconciliation bill.

- Fed signal: If the Fed sends a signal of interest rate cuts or stops balance sheet reduction in July, it may ease market pressure and boost the stock market, especially small and medium-cap stocks (Russell 2000 Index).

Strategy:

- Reduce holdings of high-valuation technology stocks and focus on the financial, defense and energy sectors.

- Pay close attention to the Fed’s policy signals and be prepared to capture rebound opportunities amid expectations of rate cuts.

- Allocate to defensive assets like consumer staples ETFs or gold to hedge against volatility.

2. Cryptocurrency

- Interest rate pressure: Rising U.S. Treasury yields make non-yielding assets (such as cryptocurrencies) less attractive, and funds may flow to high-yield Treasury bonds (4% yield).

- Potential positives: If the Fed hints at a rate cut in July, the crypto market will rebound in advance, as the expectation of easing is good for risky assets. Decentralized finance (DeFi) projects may attract some funds due to risk aversion demand.

Strategy:

- If the Federal Reserve sends out easing signals, you may consider increasing your holdings of mainstream cryptocurrencies (such as BTC, ETH) or DeFi tokens.

2. Long-term impact (after 2025)

1. US stocks

- Fiscal policy drive: The $3.8 trillion tax cuts and $200 billion defense/border spending in the reconciliation bill will stimulate economic growth and benefit the overall performance of U.S. stocks. If tariff revenue (estimated at $2.7 trillion) effectively offsets the deficit, market concerns about fiscal deterioration will ease, supporting the continuation of the bull market.

- Interest rates and valuations: The Fed's rate cuts (saving $90 billion in interest expenses for every 25 basis points) can reduce corporate financing costs and boost high-growth sectors (such as technology and clean energy). However, if the deficit continues to expand and the Fed maintains high interest rates, valuation pressure will limit the upside.

- Impact of US dollar hegemony: The long-term performance of US stocks depends on the international status of the US dollar. If the US dollar hegemony is stable (through current account outflows and financial account recovery), foreign capital inflows will support US stocks; if the status of the US dollar is shaken, capital outflows may drag down the market.

2. Cryptocurrency

- Positive effects of loose policies: If the Fed continues to cut interest rates and stops shrinking its balance sheet, the increase in liquidity will drive cryptocurrencies up, similar to the 2020-2021 bull market (Bitcoin rose from $10,000 to $69,000). In the long run, Bitcoin may break through $150,000

- Regulation and adoption: The Trump administration's friendly attitude towards cryptocurrencies (such as supporting Bitcoin reserves) may promote institutional adoption and benefit the market. However, if fiscal deterioration leads to a crisis of confidence in the US dollar, cryptocurrencies may receive capital inflows as safe-haven assets.

- Risk factors: If the Federal Reserve postpones interest rate cuts or the dollar's hegemony is challenged, the crypto market may become more volatile due to a decline in risk appetite.

Strategy:

- Hold mainstream cryptocurrencies (such as BTC, ETH) for a long time and pay attention to on-chain data (such as active addresses, transaction volume) to determine trends.

- Diversify investments into potential projects (such as Layer 2 solutions, Web3) to avoid single asset risks.

- If the status of the US dollar is shaken, increase BTC allocation as a hedge.

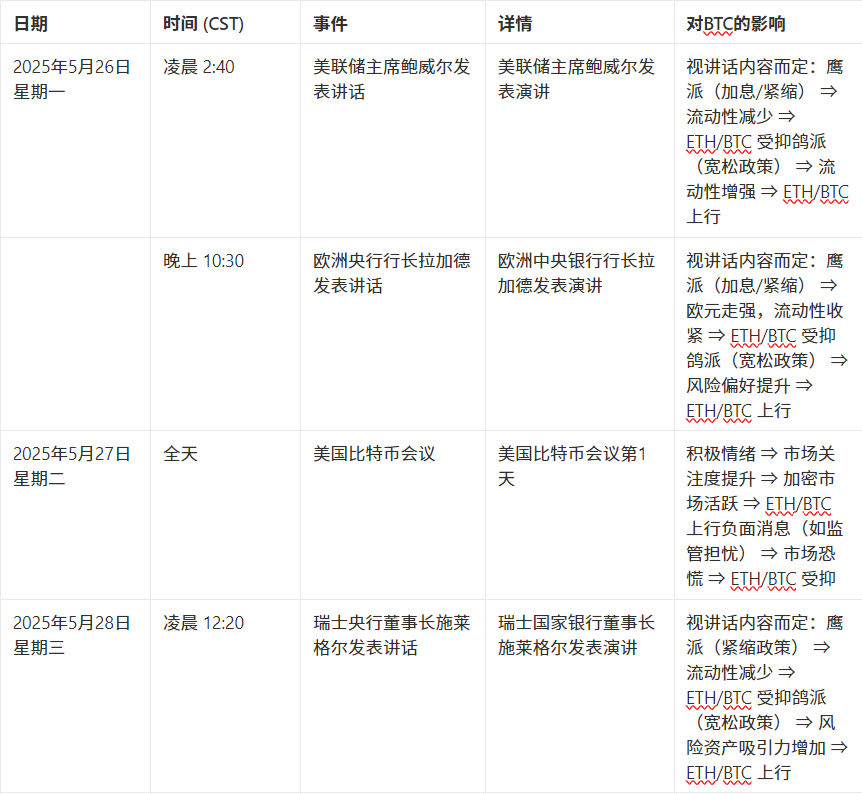

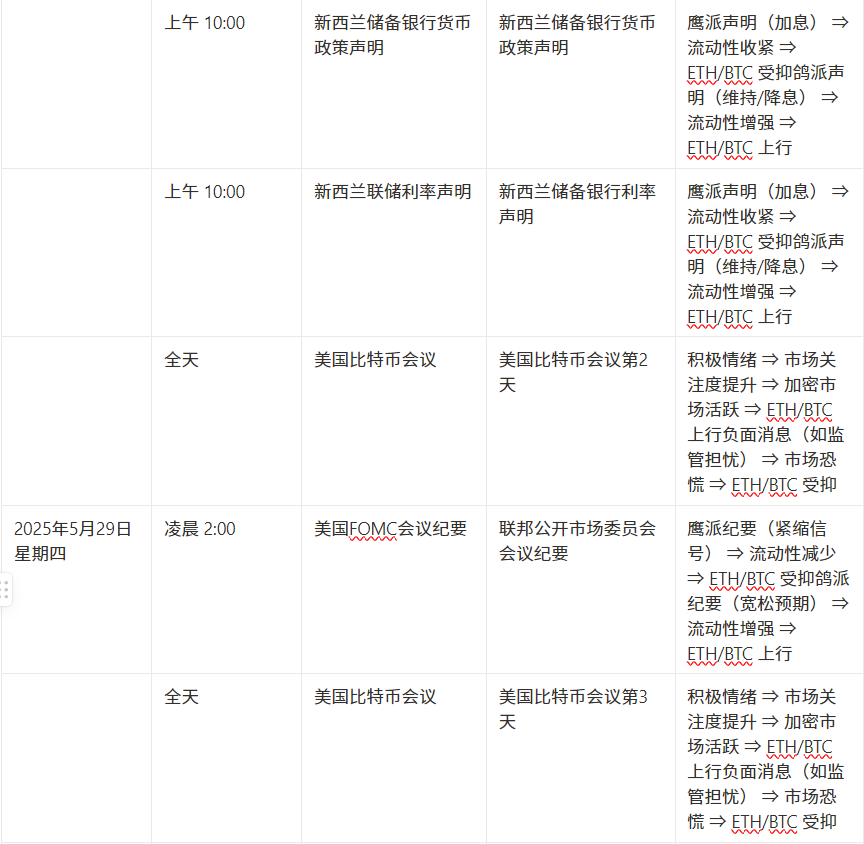

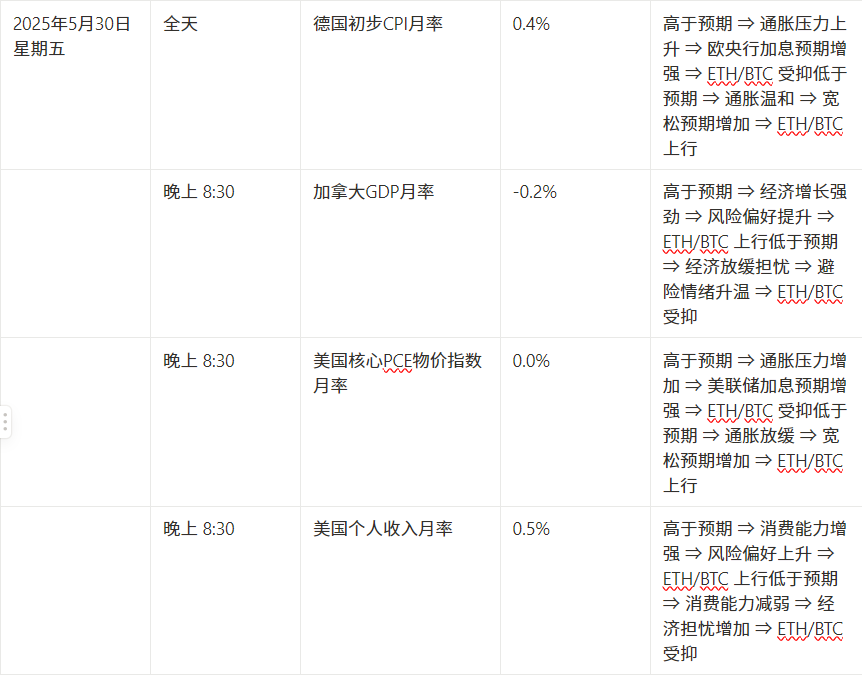

Next week's key events

Key data to watch next week

2. On-chain data analysis

1. Changes in short- and medium-term market data that affect the market this week

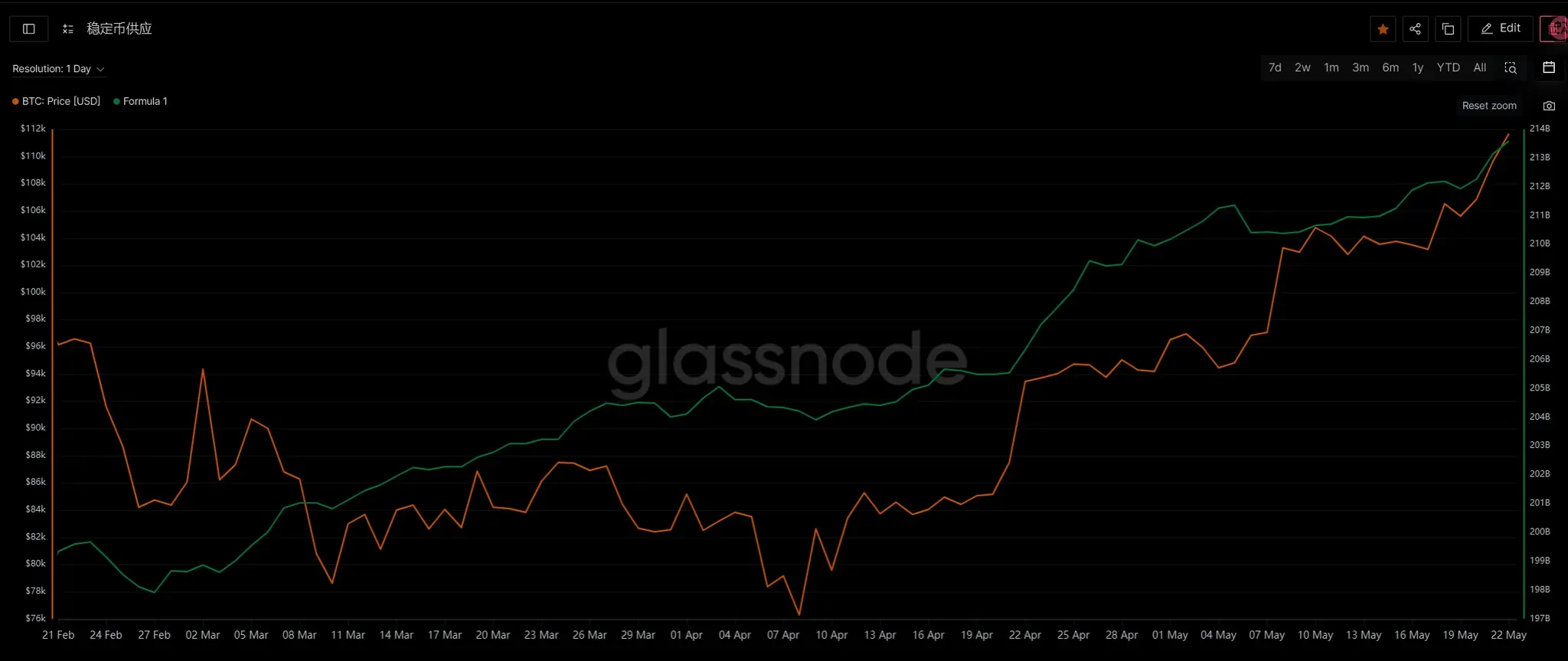

1.1 Stablecoin Fund Flow

This week (May 16 to May 26), the total amount of stablecoins increased slightly to 213.596 billion, and the additional issuance amount was 2.34 billion, which was a significant rebound from the previous period. The recovery period mainly came from the second half of this week. Relative to the total amount of stablecoins (213.596 billion), 2.34 billion is about 1.1% of the increase, which is a relatively obvious rebound. For altcoins, it is a positive marginal change. The additional issuance means that more "purchasing power ready to be invested in the crypto market" is minted.

1.2 ETF Fund Flow

This week, BTC ETF saw a large inflow, with $2.8 billion flowing in. This is a strong signal of funds, indicating that institutional investors are bullish on BTC again. The second to last column is our estimate of the number of BTC that the ETF may purchase. Of course, this data is not accurate, it is just an estimate. Although this week's figure is slightly lower than the 33,462 coins in the week of April 21, it is significantly higher than the previous weeks (especially the 5,849 coins last week), indicating that there is substantial buying, and the price trend is in good consistency with funds.

1.3 OTC Discounts and Premiums

This week, the OTC premiums of USDT and USDC both rebounded slightly and have returned to 100%, indicating that the demand for stablecoins in the market has risen again. Combined with the stablecoin data, not only the on-chain data is optimistic, but also the OTC capital inflow has a slight recovery trend.

1.4 MicroStrategy Purchase

In this round of price increases (starting from April 14), MicroStrategy purchased 48,045 BTC, spending a total of about $4.5469 billion. We can combine the above stablecoin data and ETF data to see that MicroStrategy's purchases have actually become an important funding driver for this round of price increases. Moreover, the frequency of purchases since last year's relatively high level has increased significantly compared to 2023-2024. Currently, MicroStrategy's cost has risen to $69,726, close to the low point in April. From an analytical perspective, MicroStrategy has become an important force influencing the market, and relevant data monitoring should be strengthened in the future.

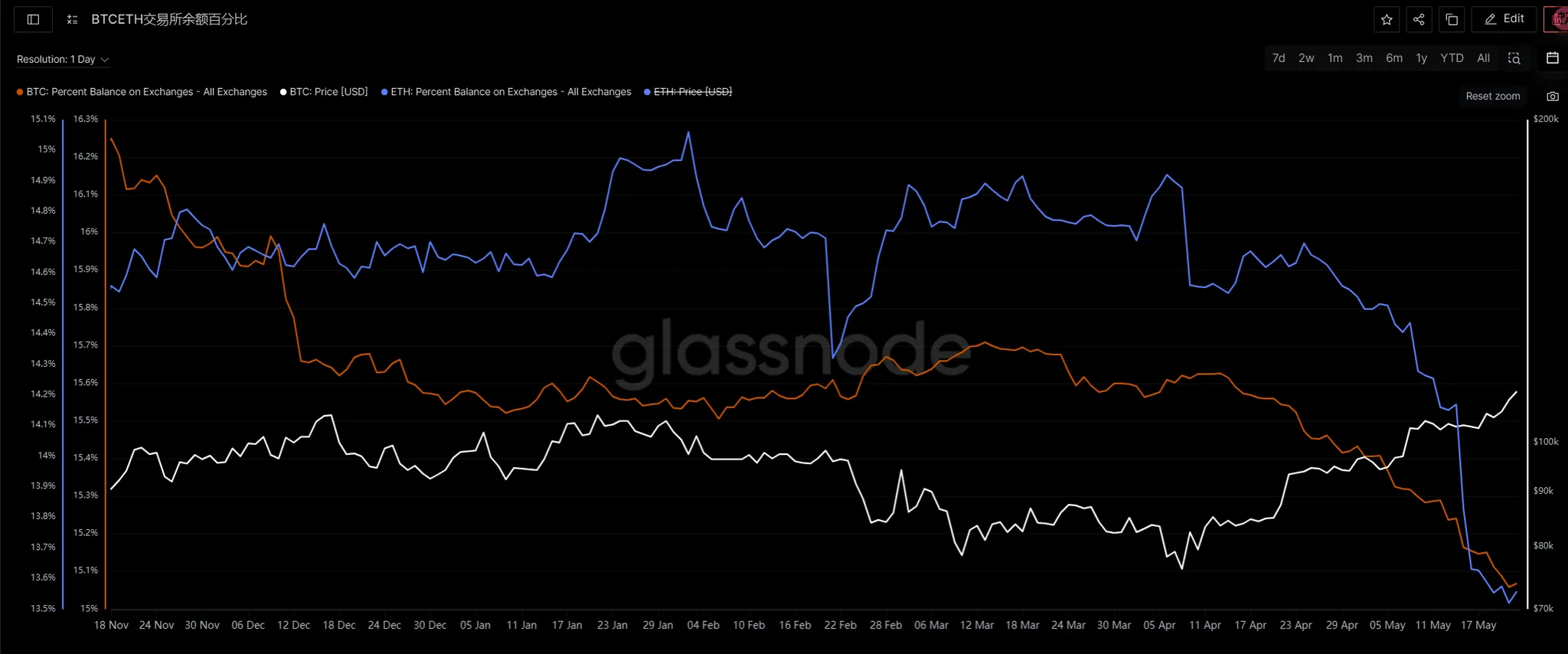

1.5 Exchange Balance

In the second half of this round of rising process, when the price was 95,000, the market saw that both BTC and ETH were continuously withdrawn from the exchange, indicating that investors were unwilling to sell. Especially for ETH, after the short squeeze (to 2,500), funds quickly withdrew from the exchange, releasing a strong "lock-up intention", showing that investors have regained confidence, which is actually an important force supporting the rise in the second half of this round. However, it should be noted that the speed of balance reduction has slowed down at present, and close attention should be paid to whether the liquidity of the exchange will continue to be squeezed.

2. Changes in mid-term market data that affect the market this week

2.1 Coin holding address ratio and URPD

The change in the percentage of coins held by addresses this week is not particularly large, especially the 100-1K addresses have not continued to increase their holdings significantly. URPD presents a relatively healthy column structure. Judging from these two data, there is no abnormal data.

At the data level, this week's funding and on-chain data performed quite well, and coupled with the relatively smooth trend of the K-line, the overall stage is still characterized as a strong state (unless there is a destructive adjustment next week). Even if there is an adjustment next week, we cannot predict or take it for granted how deep the adjustment will be.

Special thanks

Creation is not easy. If you need to reprint or quote, please contact the author in advance for authorization or indicate the source. Thank you again for your support.

Written by: Sylvia / Jim / Mat / Cage / WolfDAO

Edited by: Punko / Nora

Thanks to the above partners for their outstanding contributions to this weekly report. This weekly report is published by WolfDAO for learning, communication, research or appreciation only.