Written by Yangz, Techub News

On April 1, Circle submitted an S-1 filing to the U.S. Securities and Exchange Commission (SEC), planning an initial public offering (IPO) with the stock code CRCL and intends to be listed on the New York Stock Exchange.

In the IPO prospectus submitted, Circle also announced its financial operating data for the past three years, mainly including revenue and expenditure, asset cash flow, and the issuance and reserve status of USDC. It is not difficult to see from the public data that although Circle's revenue increased by 15.6% to US$1.68 billion in 2024, its net profit fell by 41.8% to US$156 million, highlighting the drawbacks of its business model, such as over-reliance on interest-sensitive reserve income.

Income and Expenditure

income

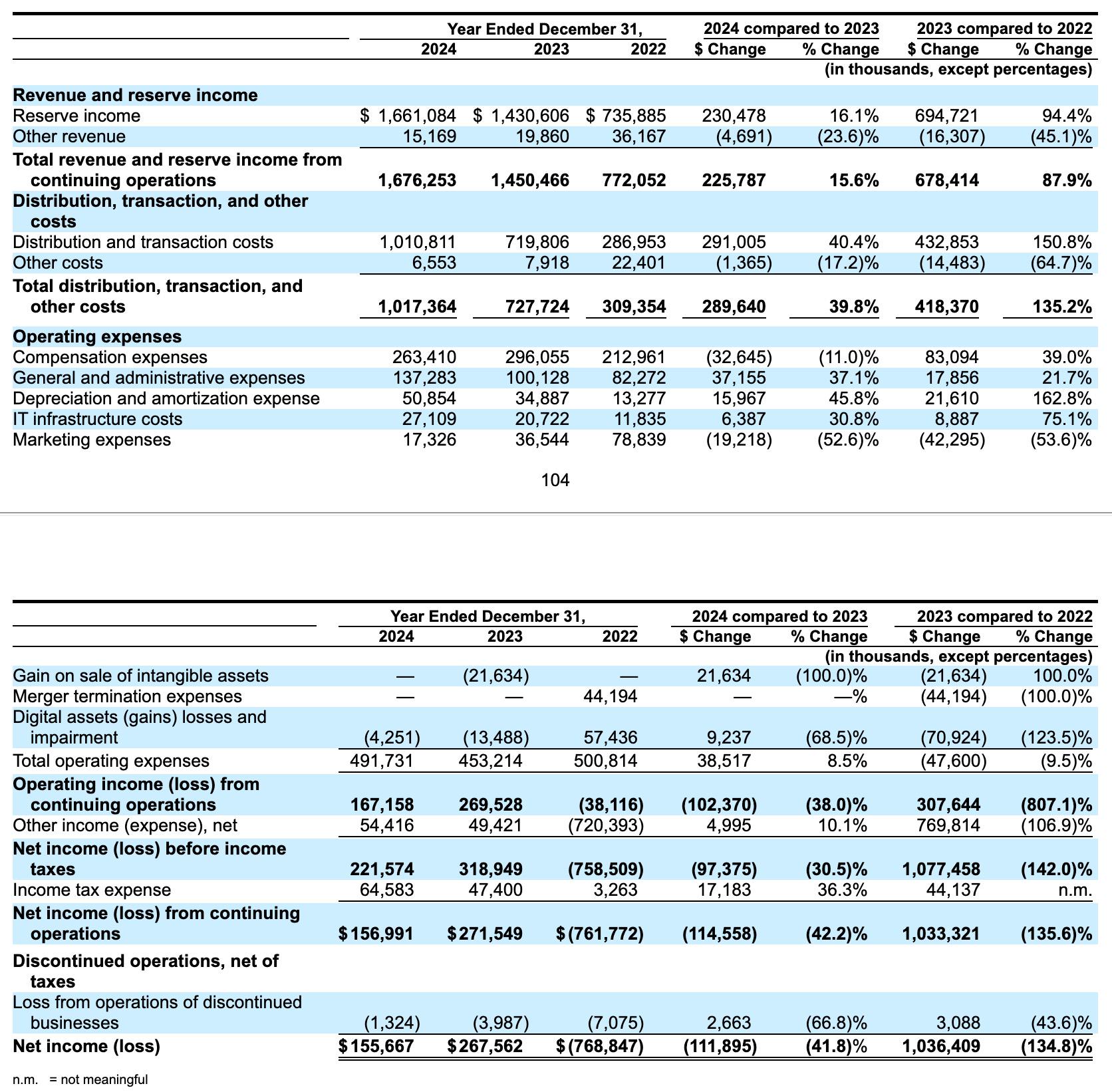

The report shows that Circle's total revenue in 2024 will be approximately US$1.676 billion, an increase of approximately US$226 million, or 15.6%, from US$1.450 billion in 2023. In addition, Circle's total revenue in 2023 will increase by approximately US$678 million, or 87.9%, from US$772 million in 2022.

Reserve Income: Circle's reserve income for 2024 is approximately $1.66 billion, an increase of approximately $230 million, or 16.1%, from $1.43 billion in 2023. Approximately $139.9 million of this increase is attributed to a 9% increase in USDC's average daily circulation. The remaining $89.9 million of growth is primarily due to the Federal Reserve's 25 basis point interest rate hike. In addition, annual reserve income in 2023 increased by $694.7 million, or 94.4%, from 2022, of which approximately $1.2937 billion of growth was attributed to the Federal Reserve's interest rate hike, but the $600.7 million increase was offset by a 39% decrease in USDC's average daily circulation after Silicon Valley Bank collapsed in March 2023.

Other income: Circle's other income in 2024 is approximately US$15.169 million, a decrease of approximately US$4.7 million from US$19.86 million in 2023, a year-on-year decrease of 23.6%. The main reason for the decline is that Circle canceled certain services in 2024, including a decrease of US$3.9 million in transaction service revenue. In addition, Circle's other income in 2023 decreased by US$16.3 million compared with 2022, a decrease of 45.1%. The main reason is that Circle shut down its traditional transaction service products that year, resulting in a decrease in related revenue of US$12 million; the cessation of the Circle Yield product reduced funding service revenue by US$7.5 million; and the cessation of the SeedInvest crowdfunding service reduced other income by US$2.8 million. In addition, revenue related to integration services increased by US$6 million, partially offsetting the above-mentioned decrease in revenue.

expenditure

Distribution and Transaction Costs: Circle's distribution and transaction costs for 2024 were approximately $1.01 billion, an increase of $291 million, or 40.4%, from 2023. The main reason for the increase was an increase of $216.6 million in distribution costs paid to Coinbase, which was a combined result of increased reserve revenue and increased Coinbase platform balances, while other distribution incentive costs related to new strategic distribution partnerships increased by $74.1 million, including its upfront one-time fee paid to Binance. In addition, Circle's distribution and transaction costs in 2023 increased by $432.9 million, or 150.8%, from 2022, mainly due to an increase of $443.2 million in distribution costs paid to Coinbase. The increase in the percentage of Coinbase's distribution costs was mainly due to the use of a fixed percentage of off-platform balances in the calculation method for distribution cost payments in August 2023, which was previously calculated variably based on the issuance or resale volume of each party. The above amount was partially offset by a decrease of $9.9 million in other market-making and distribution incentive costs for USDC.

Other expenses: Circle's other expenses in 2024 were approximately $6.553 million, a decrease of $1.4 million, or 17.2%, from 2023, mainly due to a decrease of $900,000 in expenses related to the discontinuation of traditional trading service products. In addition, Circle's other expenses in 2023 decreased by $14.5 million, or 64.7%, from 2022, mainly due to a decrease of $9.2 million in fees related to processing transactions through the Circle platform and a decrease of $6.1 million in funding service costs.

Operating expenses: Circle's total operating expenses for 2024 will be approximately $491 million, an increase of approximately $38.52 million, or 8.5%, from 2023. In 2023, Circle's total operating expenses will decrease by $47.6 million, or 9.5%, from 2022.

Compensation expenses: Circle's compensation expenses for 2024 will be approximately $263 million, a decrease of $32.6 million, or 11.0%, from 2023, mainly due to the amortization of certain restricted stock awards related to business mergers, a decrease of $57.8 million in stock compensation expenses, but an increase of $23.4 million in wages, salaries and bonuses partially offset the above decrease. In addition, Circle's compensation expenses in 2023 will increase by $83.1 million, or 39.0%, from 2022, mainly due to an increase of $76.1 million in wages, salaries and bonuses.

General and Administrative Expenses: Circle's general and administrative expenses for 2024 were approximately $137 million, an increase of $37.2 million, or 37.1%, from 2023, primarily due to an increase of $17.6 million in legal fees due to ongoing legal matters and an increase of $13.2 million in professional services and consulting fees, including accounting and tax fees. In addition, Circle's general and administrative expenses for 2023 increased by $17.9 million, or 21.7%, from 2022, primarily due to an increase of $6.1 million in travel and entertainment expenses, an increase of $4.7 million in insurance expenses, and an increase of $5.2 million in legal fees due to ongoing legal matters.

Depreciation and amortization expenses: Circle's depreciation and amortization expenses for 2024 will be approximately $50.854 million, an increase of $16 million, or 45.8%, from 2023, mainly due to an increase of $17.2 million in amortization expenses for internally developed software. In addition, Circle's depreciation and amortization expenses for 2023 will increase by $21.6 million, or 162.8%, from 2022, mainly due to an increase of $16 million in amortization expenses for internally developed software and an increase of $4.5 million in amortization expenses for acquired intangible assets.

IT infrastructure costs: Circle's IT infrastructure costs for 2024 are approximately $27.109 million, an increase of $6.4 million, or 30.8%, from 2023, primarily due to an increase of $3 million in cloud-based services and an increase of $3.4 million in software licenses to support infrastructure construction and enhance products. In addition, Circle's IT infrastructure costs for 2023 increased by $8.9 million, or 75.1%, from 2022, primarily due to an increase of $5.7 million in software licenses and an increase of $3.2 million in cloud-based services.

Marketing expenses: Circle's marketing expenses in 2024 will be approximately $17.326 million, a decrease of $19.2 million, or 52.6%, from 2023, mainly due to reduced marketing, sponsorship activities and advertising expenses. In addition, Circle's marketing expenses in 2023 will be $42.3 million less than in 2022, a decrease of 53.6%, also mainly due to reduced marketing activities and advertising expenses.

Gains on sale of intangible assets: Circle's gains on sale of intangible assets in 2023 increased by $21.6 million, or 100.0%, compared to 2022, primarily due to Circle recognizing gains on the sale of SeedInvest assets in that year. In 2024, Circle had no such transactions and related gains.

Merger termination costs: Circle incurred approximately $44.2 million in merger termination costs in 2022, with no such transaction and related expenses in 2023 and 2024.

Digital Asset (Gain) Losses and Impairments: Circle's digital asset (gain) losses and impairments for 2024 were approximately $4.25 million, a decrease of $9.2 million, or 68.5%, from 2023, primarily due to a $10.6 million decrease in Circle's digital asset sales gains. In addition, Circle's digital asset (gain) losses and impairments for 2023 increased by $70.9 million, or 123.5%, from 2022, primarily due to a $426.5 million decrease in impairment charges on digital assets (including digital assets held as collateral related to Circle Yield) and a $13.4 million increase in corporate digital asset sales gains. However, the above values were partially offset by a $211.5 million decrease in the fair value of embedded derivatives on digital assets held as collateral and a $158 million decrease in gains realized on the return of digital assets held as collateral, primarily related to the terminated Circle Yield product.

other

Other income (expense), net: Circle's other income (expense), net for 2024 was approximately $54.416 million, an increase of $5 million, or 10.1%, from 2023, primarily due to a $12.2 million increase in net investment income (loss) and a $5.5 million increase in interest income on the Company's cash and cash equivalents, partially offset by a $13.2 million decrease in fair value adjustments to the mark-to-market of convertible debt, warrant liabilities and embedded derivative instruments.

Income Tax Expense: Circle's income tax expense for 2024 was approximately $64,583,000, an increase of $17.2 million from 2023, primarily due to the release of a portion of the valuation allowance in 2023 resulting from the acquisition of intellectual property related to Centre Acquisition. This increase was partially offset by higher taxable income in 2023, primarily due to higher pre-tax book income than in 2024.

Losses from discontinued operations: Circle's losses from discontinued operations in 2024 were approximately $1.324 million, a decrease of $2.663 million, or approximately 66.8%, from $3.987 million in 2023. Circle's losses from discontinued operations in 2023 were $3.088 million, or approximately 43.6%, less than in 2022.

Based on the above data, Circle's net income in 2024 will only be US$156 million, a decrease of approximately US$112 million from US$268 million in 2023, a year-on-year decrease of approximately 41.8%.

It is not difficult to see from the above data that Circle's financial performance in 2024 presents a contradictory situation of revenue growth but declining profits. From the perspective of revenue structure, Circle's current business is overly dependent on reserve income. This single revenue structure will expose it to huge market risks. Once interest rates are lowered or user demand for USDC decreases, revenue will be directly affected. In addition, expenditure issues are also prominent. The growth rate of distribution and transaction costs far exceeds the growth of revenue, and this part of the cost is mainly paid to partners such as Coinbase, reflecting that Circle's business model is highly dependent on institutional networks. It is worth noting that in Circle's operating expenses in 2024, legal consulting fees increased significantly by 37%, highlighting the challenges it has faced in compliance in recent years.

In general, Circle's financial performance shows the characteristics of "increasing revenue but not increasing profits". The core problem lies in the single business model (interest rate driven revenue) and out-of-control channel costs (distribution partners grab most of the profits). If the above problems cannot be solved, Circle's profitability may further deteriorate during the interest rate cut cycle.

USDC issuance and reserves

The report shows that as of December 31 last year, the total circulation of USDC was about 43.857 billion. In 2024, Circle will issue a total of about 141.342 billion USDC, redeem about 121.897 billion, and increase the circulation by about 19.445 billion; in 2023, Circle will issue a total of about 95.833 billion USDC, redeem about 115.975 billion, and reduce the circulation by about 20.142 billion; in 2022, Circle will issue a total of about 167.609 billion USDC, redeem about 165.471 billion, and increase the circulation by about 2.138 billion.

In terms of reserves, USDC's reserves in 2024 will be approximately US$43.921 billion, of which US$6.407 billion will be held in cash (14.6%), and US$37.514 billion will be deposited in the Circle Reserve Fund (85.4%); USDC's reserves in 2023 will be approximately US$24.472 billion, of which US$2.234 billion will be held in cash (9.1%), and US$22.238 billion will be deposited in the Circle Reserve Fund (90.8%); USDC's reserves in 2022 will be approximately US$44.714 billion, of which US$10.518 billion will be held in cash (23.5%), US$23.664 billion will be deposited in the Circle Reserve Fund (52.9%), US$1.783 billion will be held in cash equivalents (4%), and US$8.749 billion will be held in available-for-sale debt securities (consisting only of bonds with maturities of 91 to 100 million). days) (19.6%).

The obvious changes in the USDC reserve structure from 2022 to 2024 reveal Circle's strategic adjustments in risk management. The most notable trend is the sharp fluctuation in the proportion of cash holdings: it plummeted from 23.5% in 2022 to 9.1% in 2023, and then rebounded to 14.6% in 2024. This swing reflects Circle's cautious attitude towards banking system risks after the Silicon Valley Bank incident, and the subsequent rebalancing between yield and security. At the same time, the proportion of reserve funds continued to climb from 52.9% in 2022 to 85.4% in 2024, indicating that Circle is allocating more assets to regulated money market funds to obtain stable returns.

Assets and Cash Flow

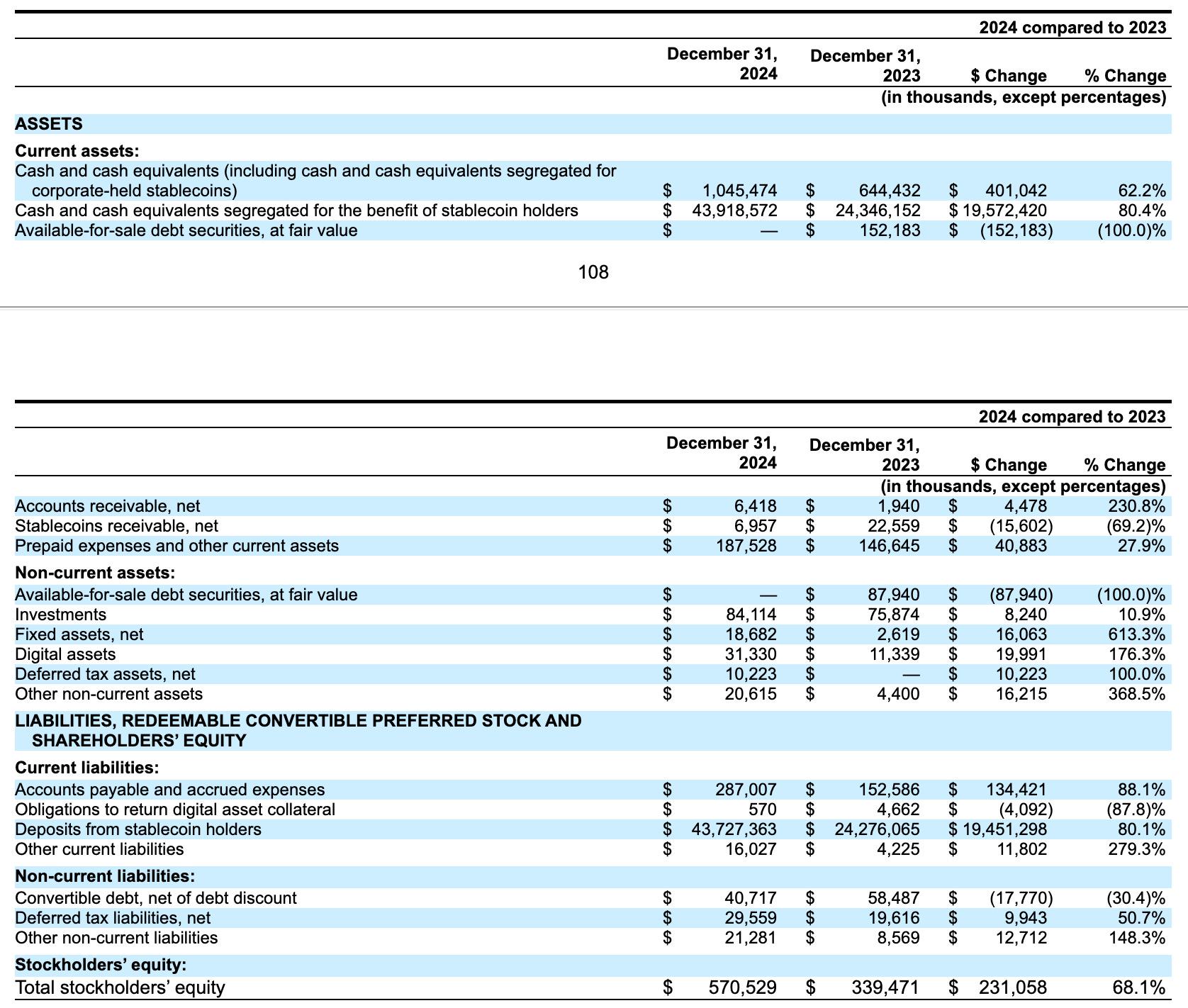

The report shows that Circle's assets are mainly composed of liquid assets, non-liquid assets, liquid liabilities, non-liquid liabilities and shareholders' equity. Among them, liquid assets include cash and cash equivalents, available-for-sale debt securities valued at fair value, net accounts receivable, net stablecoin receivable, prepaid expenses, etc.; non-liquid assets include available-for-sale debt securities valued at fair value, investments, fixed assets, digital assets and net deferred tax assets, etc.; liquid liabilities include accounts payable and accrued expenses, deposits from stablecoin holders, etc.; non-liquid liabilities include convertible debt (net of debt discount), net deferred tax liabilities, etc.

Cirlce's total current assets in 2024 are approximately US$45.16 billion, an increase of approximately US$19.85 billion, or 78.4%, from US$25.31 billion in 2023; Circle's non-current assets in 2024 are approximately US$165 million, a decrease of approximately US$17.208 million from US$182 million in 2023, a decrease of approximately 9.3%; Circle's current liabilities in 2024 are approximately US$44.03 billion, an increase of approximately US$19.6 billion, or 80.2%, from US$24.44 billion in 2023; Circle's non-current liabilities in 2024 are approximately US$91.557 million, an increase of approximately US$4.885 million, or 5.6%, from US$86.672 million in 2023; Circle's shareholders' equity in 2024 is approximately US$570 million, an increase of approximately US$230 million, or 68.1%, from US$340 million in 2023.

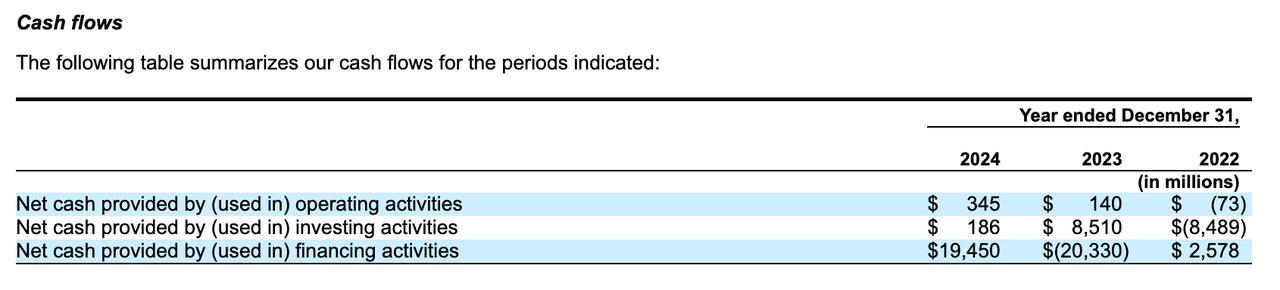

In terms of cash flow, it is mainly divided into three parts: operating activities, investment activities and financing activities.

In 2024, Circle's net cash from operating activities was $345 million, an increase from $140 million in 2023. The main reason was the increase in USDC circulation balance, as well as the increase in average yield and average reserve deposits, which led to an increase in cash income in reserves of $142.5 million, partially offset by an increase in distribution and transaction costs of $32.3 million. In addition, Circle used $72.7 million in cash in operating activities in 2022.

In 2024, Circle had net cash from investing activities of $186 million. That year, Circle received $341.6 million in cash from the sale and maturity of available-for-sale securities, but then spent $99.3 million on the purchase of available-for-sale securities, $39.1 million on software development, and $18.1 million on the purchase of long-term assets. In 2023, Circle had net cash from investing activities of $8.51 billion, mainly due to the maturity of U.S. Treasury bonds and an increase of $8.7 billion in cash and cash equivalents separated for the benefit of stablecoin holders. In contrast, in 2022, Circle used approximately $8.5 billion in cash in investing activities.

In 2024, Circle's net cash provided by financing activities was $19.45 billion, an improvement from $20.33 billion in 2023. In 2024, stablecoin holders' deposits increased by $19.4521 billion due to the increase in USDC circulation, while in 2023, stablecoin holders' deposits decreased by $20.3222 billion due to the decrease in USDC circulation. In addition, Circle's net cash provided by financing activities in 2022 was $2.5782 billion.

Judging from the above data, Circle's asset structure is highly liquid but has a single profit model. In 2024, Circle's liquid assets surged 78% to $45.16 billion, but almost all of it came from the growth of USDC reserve funds, while liquid liabilities also increased by 80% to $44.03 billion during the same period. Although this strict asset-liability matching ensures repayment ability, the low proportion of shareholders' equity indicates that its risk resistance is weak; from the perspective of cash flow, Circle's business shows obvious cyclicality. In 2024, operating cash flow improved to $345 million, mainly due to reserve income brought about by the Fed's interest rate hike, but the growth rate of distribution costs has exceeded 50% of revenue growth, and profit margins continue to be under pressure. More noteworthy is that financing cash flow is completely linked to the circulation of USDC. The net inflow of $19.45 billion in 2024 directly reflects the recovery in demand for USDC. This single dependence makes the stability of the business questionable.

Summarize

Circle’s financial report data highlights the deep contradictions in its business model. Although it occupies an important position in the stablecoin market with USDC, its structural problems of over-reliance on interest-sensitive income and high channel costs have caused it to face the valuation dilemma of "increasing revenue but not profits" when it rushed to IPO.

This IPO is not only a key battle for Circle to break through the bottleneck of development, but also an important touchstone to test the market's recognition of the "stable currency business model". If successfully listed, Circle will become another heavyweight cryptocurrency company to land on the US stock market after Coinbase, and will also be the first listed stable currency company.