Author: Fairy, ChainCatcher

Strategy has come up with a new trick.

In order to continue to increase its Bitcoin positions, MicroStrategy has frequently "raised funds" in recent years, advancing along three paths from common stock, convertible bonds to preferred stock, and continuously raising funds.

The bull market is not over yet, and the chips are doubled. Yesterday, Strategy announced the launch of a new preferred stock product, STRD, which is another chip on its path to heavy Bitcoin holdings. What is the difference between this "new card"? What signals does its structural design, potential risks and market game release?

STRD: High interest, but no guarantee of receipt

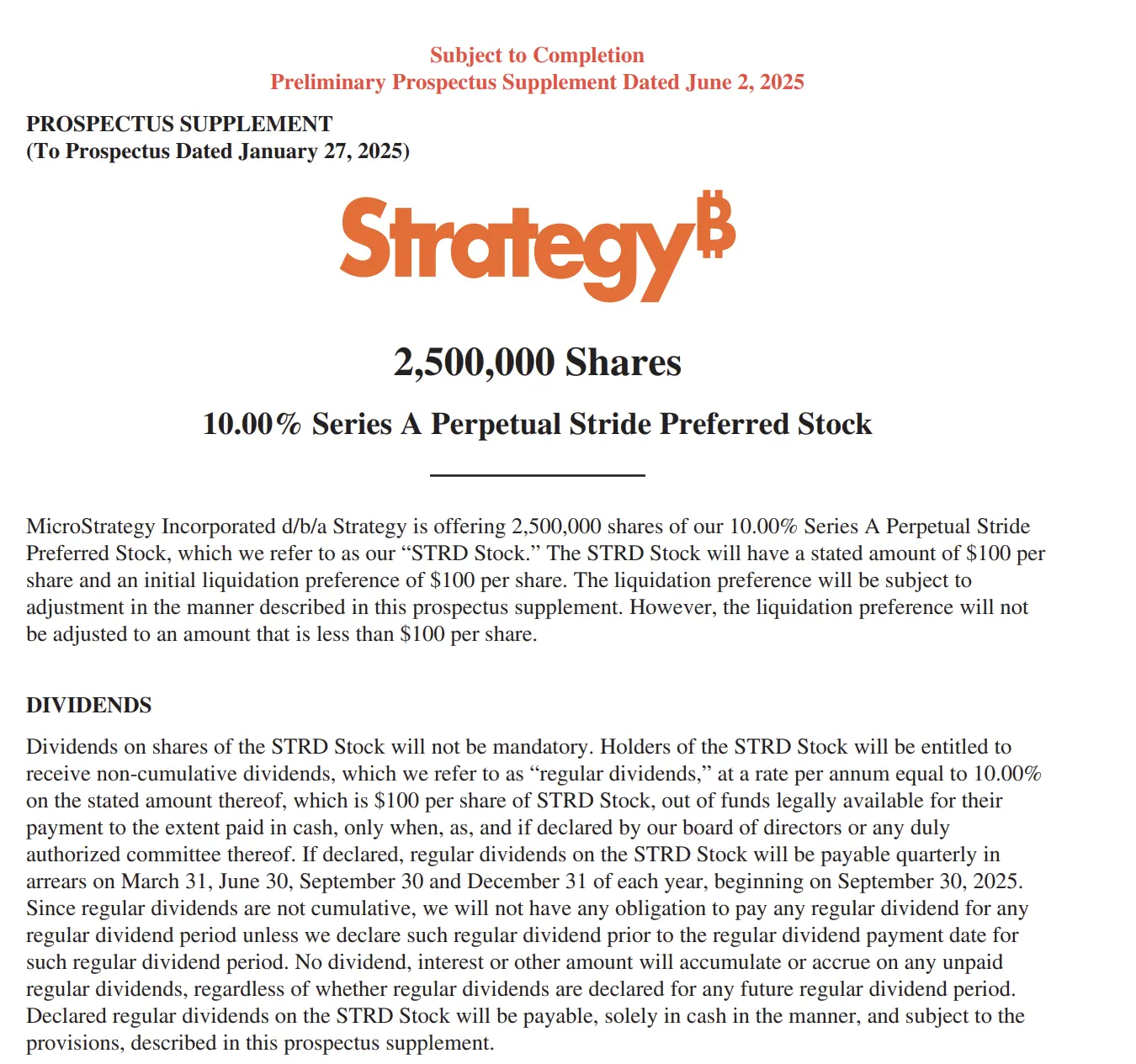

STRD is the third type of preferred stock product launched by Strategy. It plans to issue 2.5 million shares to the public. The funds raised will be mainly used for Bitcoin acquisition and working capital replenishment. STRD is essentially another structured expression of the BTC long strategy, continuing the framework of STRK and STRF, and making new designs in the profit distribution and exit mechanism.

Similar to its predecessor, the underlying asset behind STRD is still Bitcoin, but this time Strategy has adopted a more "defensive and offensive" structure: the annualized coupon is 10%, but there is no mandatory payment obligation, and interest does not accumulate.

Crypto KOL Phyrex explained it in one sentence: "The essence of STRD is to lend money to Strategy at an annual interest rate of 10%, but Strategy may not distribute the 10% annual interest as promised. If it does not, it will not be reissued in the future. In the description, Strategy promised to pay on time, provided that the company's profits are good."

As for where this interest comes from, Strategy theoretically has three possible payment paths:

- Selling BTC holdings: If Strategy liquidates part of its Bitcoin holdings, it will be able to generate cash flow, but this will face capital gains tax and is contrary to its long-term holding strategy.

- Continuous financing rollover: It may be possible to raise money to pay interest by reissuing debt or other instruments, which may be the approach that Strategy currently prefers.

- Business operating cash flow: If the company's other businesses are profitable, it may also be used to pay interest.

Although Strategy has the right not to pay interest, the cost of doing so will be extremely heavy. Once the interest is stopped, the market price of STRD will inevitably be under pressure, investor confidence will be frustrated, and future refinancing will also face greater resistance. Therefore, the market generally believes that as long as the Bitcoin market performs steadily, Strategy will most likely choose to fulfill its contract on time to maintain its market reputation and the sustainability of its capital chain.

"Three Swords at Once": Strategy's Multi-Level Preferred Stock

After talking about the characteristics of STRD, let's take a look at Strategy's three current preferred stock products. STRK, STRF and STRD have their own positions in terms of liquidation order, return design and risk structure, and constitute the key puzzle of Strategy's multi-layer capital structure. The following is a comparison table of the three products compiled by Juan Leon, senior investment strategist at Bitwise (the table content is translated by ChainCatcher):

From the perspective of investor adaptation, STRK is more in line with the conservative allocation needs that pursue stable returns and have a lower risk appetite; STRF is aimed at neutral investors who expect to lock in higher fixed returns but can accept a certain degree of credit risk; STRD focuses on offensive funds with high risk tolerance.

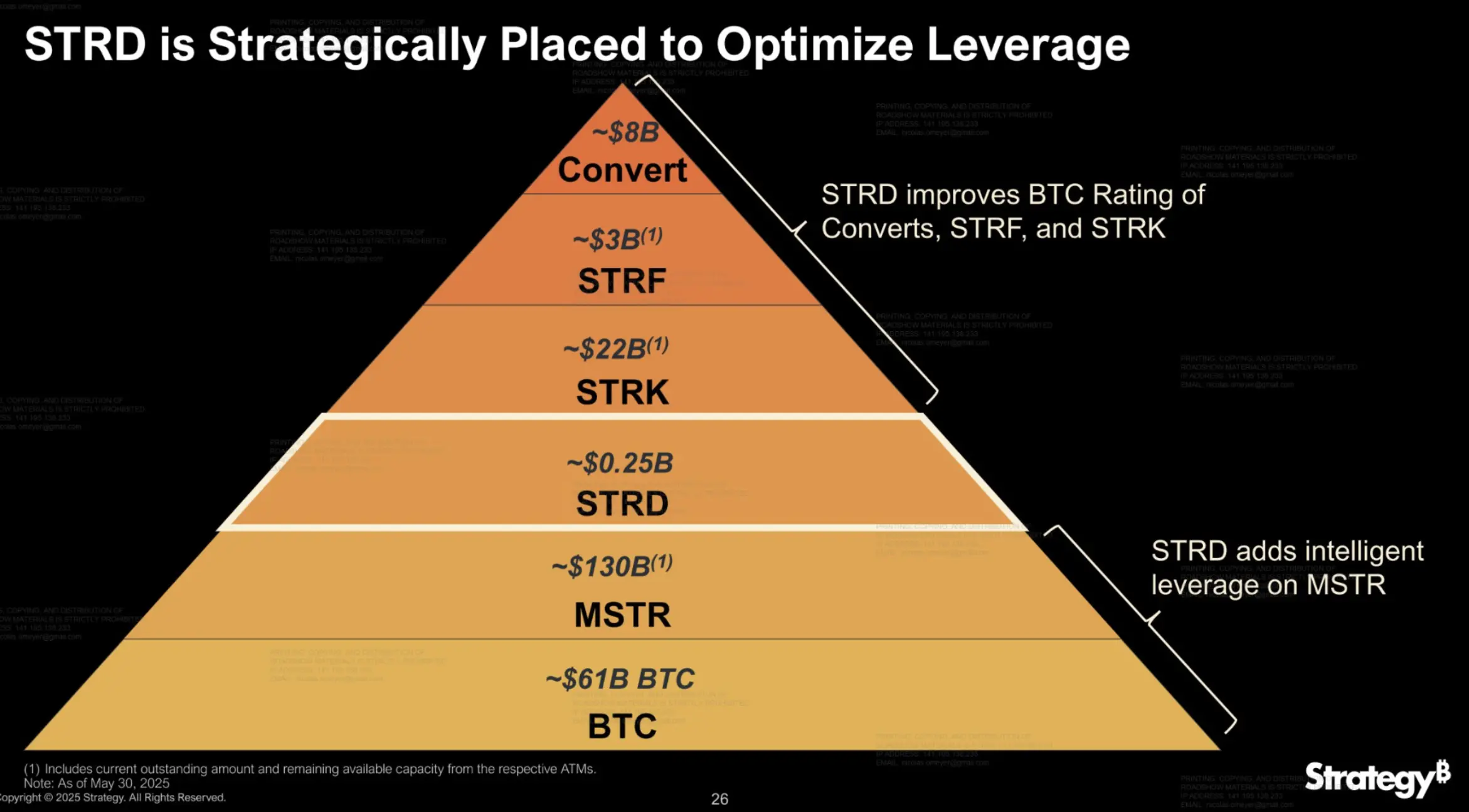

In addition to product extension, the launch of STRD may also be a boost to Strategy's capital structure. According to a chart shared by community member @DogCandles, STRD has a "low status" but a "big role", optimizing the overall capital structure by improving the credit support of upper-level products.

The community is not buying it, and STRD is controversial

The release of STRD was a carefully planned move by Strategy, but the community did not unanimously applaud. Many voices pointed directly to its "capital magic":

- @chaojidigua: Jiang Taigong fishes, and those who are willing will take the bait.

- @MemeSiguoyi: Even though the cryptocurrency world can print money with virtual coins, we stocks also have our own method of printing money out of thin air.

- @Softelectrock: Ponzi doll.

Adam Livingston, author of Bitcoin Times, directly pointed out that STRD is essentially a BTC holding option disguised as an income tool. When BTC rises sharply, Strategy redeems at par value; when BTC falls sharply, no dividend is paid. Investors are actually paying for his belief in "ultimate adoption of Bitcoin".

Dylan LeClair, director of Bitcoin strategy at Metaplanet, called it a "genius design" from a structural perspective: "The issuance of STRD actually improves the credit quality of STRF."

Regarding Strategy’s future development path, crypto KOL Phyrex gave a bolder prediction: “It is possible that Strategy will make some plans to store Bitcoin, such as lending BTC, or participating in some quantitative transactions to maintain cash flow. Strategy may become a BTC-based bank in the future.”

Strategy's chips have been pushed to the center of the table. Structured products are used to wrap up beliefs, risk-return models are used to cover up unilateral bets, and "high interest rates" are used to attract market sentiment.

This faith-based financial experiment is becoming increasingly complex and worthy of more attention.